Blogging this time around is quite a different experience to last time. Then I was still relatively unknown and didn’t have the wide circle of cool progressive friends that I do now.

I tried out various types of subjects and – much like now – went broadly where my interest and the topics of the day were trending. The post that got me noticed was the review of TOP’s tax policy – including getting noticed by Gareth Morgan and the one that went the widest was my push for Deborah Russell.

The one that got most hits on the day – and it is still the number one – was when I got upset about the Inland Revenue restructure of the investigation function. My friends were hurting and so I was hurting too.

Since then my LinkedIn feed has shown a steady stream of talented people leaving Inland Revenue for other opportunities. I have heard it said that the people who left were change resistant and/or deadwood. The fact that they left would put lie to the change resistant angle. And given they have all moved on to senior positions in government, the Big 4, international organisations or their own successful practices – I think deadwood is a stretch too.

The Commissioner recently told the Finance and Expenditure committee that there had been no drop in technical expertise (1). And I think that is probably right. While there has been a net loss of talent, there are still lots of very capable competent people there. A number of people who were senior team leaders have gone back to doing the work. They were kick arse before they became team leaders and will be kick arse now. The tax system is safe with them.

Similarly the managers who were ultimately appointed. All very sane, experienced and competent. Yes some took redundancy but they are now doing different cool things with their lives.

So for these reasons I haven’t felt any need to reopen this topic. My friends who were affected have now either moved on and happy in their new roles or accepted the pay cut – after equalisation wears off – given the other benefits working for the Revenue entails. And there are quite a number. Flexibility, intellectual interest, and socially productive work – to name but three.

Yes there is still the matter of a 27% engagement score (2) but that is between the Commissioner, the Minister and the State Services Commissioner. Nothing I can add to that. There should still be the capability and capacity to run a decent audit programme even after the restructure.

Like most of the tax community, I had heard that this year people were being moved out of investigating into correspondence or the phones to help the BT transition. But they were only mumurings – there was no proof of that.

Until now.

Andrew Bayly Opposition spokesman for Revenue has put in a number of written parliamentary questions – it appears – looking to get to the bottom of the mumurings.

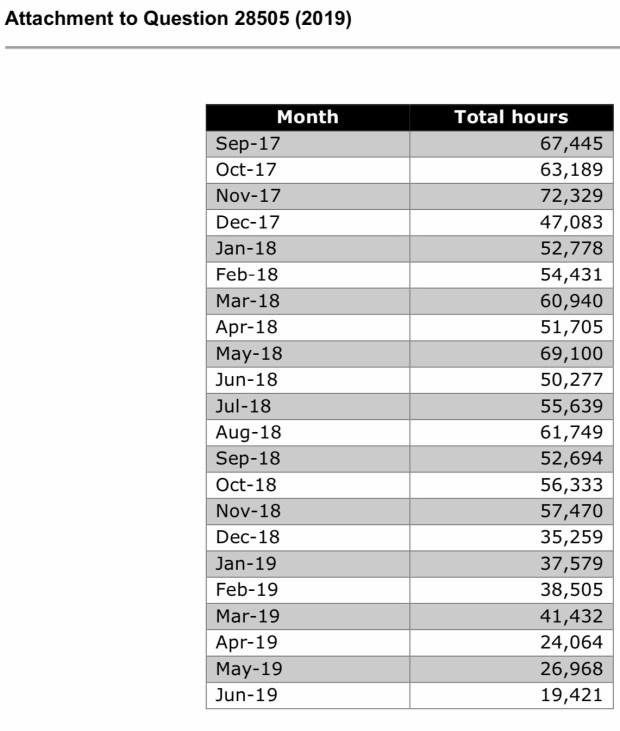

He asked quite a number of questions but the one I homed in on was audit hours. (3) Dear readers they have plumeted. June 19 is a third of June 18 – yes a third. To be fair that is probably the worst month. At best they are 2/3 of the previous year.

So the murmurings were true.

Ok so during an important stage the Commissioner moved her resources around. Fair enough.

What I don’t understand is if they were to fall like that why not come clean? Front foot it to the tax community. Say yeah audit activity will drop over this period because [insert reasons here] but – much like Arnie – we’ll be back baby. Don’t get complacent.

But it does mean that if this level of resources are being shifted from BAU to BT, BT is costing more than originally forecast. And these extra costs should be booked against BT. Or if they are being booked against BT – then the BAU money should be given back. It’s not like the Government doesn’t have uses for it.

Now none of this, as far as I can tell, is being mentioned in the monthly reporting to Joint ministers. This focus is solely on the BT programme and no mention, that I can see, on the affect on BAU.

There is, however, a mention in the paper Minister Nash took to Cabinet in November

The department’s service performance may dip while these changes are embedded. I will be kept regularly informed of any issues that arise. (4)

So I can only assume there has been parallel reporting on BAU to the Minister of Revenue on this and he and Treasury are happy with the reallocation of resources.

Of course if I have any of this wrong Inland Revenue – as I know you read the blog – please let me know and I’ll retract accordingly. But otherwise – Andrew Bayly is doing his job.

Andrew, our politics may not be the same, but dude – respect. I now have your wpq link on speed dial. Thank you for your service.

Andrea

(1) Second paragraph page 4

(2) Page 12 question from Dan Bidois

(3) The answer to audit commencements about not having information that predates START is odd. We all used to put our time into eCase. Clumsy and annoying. But it was all there. I can’t believe that Inland Revenue would be in breach of the Public Records Act and not have that information anymore. Would be a really back look too given taxpayers have to hold records for 7 years. Must be a mistake.

(4) Paragraph 32

Hi Johnno. I am delighted you are enjoying the blog. My objective has always been to make tax accessible to a non-tax audience – sometimes better than others.

I try though to only write about topics that I have some degree of expertise or experience. I try to stay away from ‘reckons’ as I think there is enough of that around already. Both those topics unfortunately would just involve reckons from me.

My understanding about a financial transaction tax is that it is a great tax if all countries in the world have one. Otherwise we risk our banking industry moving to Australia where there wouldn’t be the tax. Officials provided this paper for the TWG and I am not sure I could add anything to it. https://taxworkinggroup.govt.nz/sites/default/files/2018-09/twg-bg-3959227-financial-transaction-taxes.pdf

On aligning definitions I would agree with you. I am very sympathetic to your suggestion. I had heard that one reason for the difference was that ‘poverty is a household’ occurrence in the way income and tax isn’t. I am not sure that survives much analysis and the welfare difference would largely be for ‘historic reasons’.

As an aside I note that the appalling debt rules in welfare also used to be there for tax. Tax changed but welfare stayed the same. Tax also used to apply on a household basis too but changed [insert time period here].

Robin Oliver wrote a paper on the different concepts of income for the TWG which you may be interested in. https://taxworkinggroup.govt.nz/sites/default/files/2018-09/twg-bg-3950999-concepts-of-income.pdf

I am not sure if any of this helps but I really appreciate your engagement.

Cheers Andrea

LikeLike

Although not a tax professional I am enjoying your blog. I have two issues I think may be worthy of blogging.

The first is the idea of a low say (o.oo5%) universal financial transaction tax, (to replace gst, and efforts to tax transnational entities and digital services). Primary targets being simplification, ease of enforcement, and acheiving what gst has not – universalisation of the tax burden.

The other issue is that of the wild discrepancy between the way Tax accounting and WINZ accounting treats the notions of business income and expenses. WINZ for example can refuse a valid business expense such as electricity used by a bitcoin mining business as “usual household expenditure” even when the business activity doubles or quadruples the households usual electricity bill. The result the individual small business owner’s income is WINZ assessed more on turnover than upon returned income ( above the legislated requirement to ignore negative income from a business). This issue reflects another discrepancy between the tax system and the Welfare sytem. Another is the failure of MSD to publish accounting guidelines, and determinations, c.f., IRD. The result a small business owner budding, or failing, who finds themselves personally dependant on a top up via welfare must maintain two sets of books, one of which even accountants can not provide cogent advice upon – because MSD does not communicate well, beyond the courtroom.

The latter issue is a further twist to the joined up but incoherant tax/welfare system. Surely it would be sensible for both to share common explicit definitions, and accounting standards. If so perhaps the numbers investigated and prosecuted for welfare fraud would plumet. And the assumptions of non beneficiaries regarding the administration welfare lbludgersl would be better grounded. After all the playing feild is far from level in regards to notions of income and expense.

Hopefully, you have some insight, or perspective on these matters.

LikeLiked by 1 person