Where have all the audits gone?

Blogging this time around is quite a different experience to last time. Then I was still relatively unknown and didn’t have the wide circle of cool progressive friends that I do now.

I tried out various types of subjects and – much like now – went broadly where my interest and the topics of the day were trending. The post that got me noticed was the review of TOP’s tax policy – including getting noticed by Gareth Morgan and the one that went the widest was my push for Deborah Russell.

The one that got most hits on the day – and it is still the number one – was when I got upset about the Inland Revenue restructure of the investigation function. My friends were hurting and so I was hurting too.

Since then my LinkedIn feed has shown a steady stream of talented people leaving Inland Revenue for other opportunities. I have heard it said that the people who left were change resistant and/or deadwood. The fact that they left would put lie to the change resistant angle. And given they have all moved on to senior positions in government, the Big 4, international organisations or their own successful practices – I think deadwood is a stretch too.

The Commissioner recently told the Finance and Expenditure committee that there had been no drop in technical expertise (1). And I think that is probably right. While there has been a net loss of talent, there are still lots of very capable competent people there. A number of people who were senior team leaders have gone back to doing the work. They were kick arse before they became team leaders and will be kick arse now. The tax system is safe with them.

Similarly the managers who were ultimately appointed. All very sane, experienced and competent. Yes some took redundancy but they are now doing different cool things with their lives.

So for these reasons I haven’t felt any need to reopen this topic. My friends who were affected have now either moved on and happy in their new roles or accepted the pay cut – after equalisation wears off – given the other benefits working for the Revenue entails. And there are quite a number. Flexibility, intellectual interest, and socially productive work – to name but three.

Yes there is still the matter of a 27% engagement score (2) but that is between the Commissioner, the Minister and the State Services Commissioner. Nothing I can add to that. There should still be the capability and capacity to run a decent audit programme even after the restructure.

Like most of the tax community, I had heard that this year people were being moved out of investigating into correspondence or the phones to help the BT transition. But they were only mumurings – there was no proof of that.

Until now.

Andrew Bayly Opposition spokesman for Revenue has put in a number of written parliamentary questions – it appears – looking to get to the bottom of the mumurings.

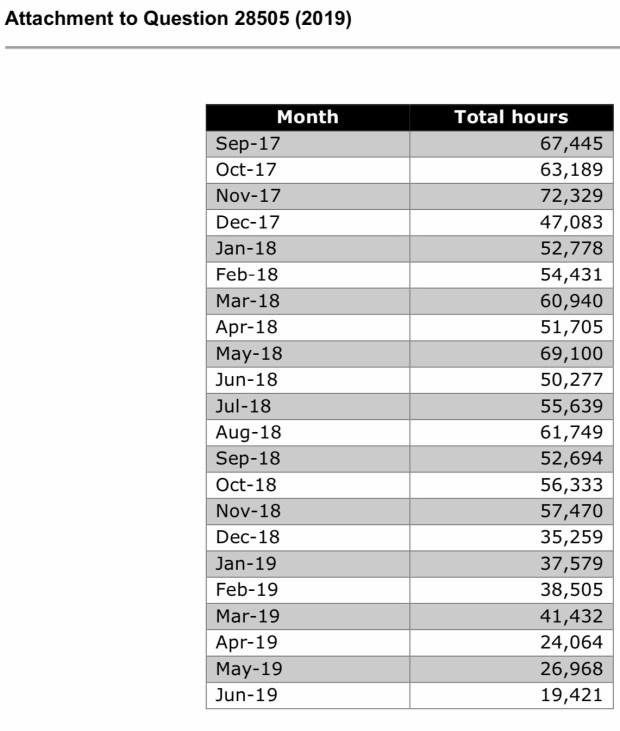

He asked quite a number of questions but the one I homed in on was audit hours. (3) Dear readers they have plumeted. June 19 is a third of June 18 – yes a third. To be fair that is probably the worst month. At best they are 2/3 of the previous year.

So the murmurings were true.

Ok so during an important stage the Commissioner moved her resources around. Fair enough.

What I don’t understand is if they were to fall like that why not come clean? Front foot it to the tax community. Say yeah audit activity will drop over this period because [insert reasons here] but – much like Arnie – we’ll be back baby. Don’t get complacent.

But it does mean that if this level of resources are being shifted from BAU to BT, BT is costing more than originally forecast. And these extra costs should be booked against BT. Or if they are being booked against BT – then the BAU money should be given back. It’s not like the Government doesn’t have uses for it.

Now none of this, as far as I can tell, is being mentioned in the monthly reporting to Joint ministers. This focus is solely on the BT programme and no mention, that I can see, on the affect on BAU.

There is, however, a mention in the paper Minister Nash took to Cabinet in November

The department’s service performance may dip while these changes are embedded. I will be kept regularly informed of any issues that arise. (4)

So I can only assume there has been parallel reporting on BAU to the Minister of Revenue on this and he and Treasury are happy with the reallocation of resources.

Of course if I have any of this wrong Inland Revenue – as I know you read the blog – please let me know and I’ll retract accordingly. But otherwise – Andrew Bayly is doing his job.

Andrew, our politics may not be the same, but dude – respect. I now have your wpq link on speed dial. Thank you for your service.

Andrea

(1) Second paragraph page 4

(2) Page 12 question from Dan Bidois

(3) The answer to audit commencements about not having information that predates START is odd. We all used to put our time into eCase. Clumsy and annoying. But it was all there. I can’t believe that Inland Revenue would be in breach of the Public Records Act and not have that information anymore. Would be a really back look too given taxpayers have to hold records for 7 years. Must be a mistake.

(4) Paragraph 32

When Harry met FATCA

Let’s talk about tax.

Or more particularly let’s talk about the taxation of US citizens living abroad.

I just love the Royal Family. Yeah I know it goes against any and every possible progressive and egalitarian ideal I hold but phish.

I grew up reading my grandmother’s Women’s Weekly and their coverage of Princess Anne’s (first) wedding and the Silver Jubilee. Over time this progressed to Diana, Fergie and their babies. And the Womens Weekly became the Hello magazine. Complete with Princess Beatrice aged two at a society wedding. So good.

And season two of The Crown has landed. Brilliant. I mean seriously- what about Philip?

Of course season one was dominated by the spectre of the abdication of a King who wanted to marry a divorced American woman. As well as the sister of the Queen who wanted to marry a divorced man.

So it was with every sense of delighted irony that I watched the recent engagement of Prince Harry to a divorced older mixed race American woman. Whose father might be catholic. ROFLMAO.

And my delight became complete when the Washington Post pointed out Meghan and Harry’s children will be subject to FATCA and US residence taxation. Oh and I have been meaning to write about the joys of US citizen taxation since like forever. So finally here was my angle.

The British Royal family – the gift that keeps on giving.

First key thing is that all people born in the United States or born to at least one US parent – like Harry’s children will be – are US citizens. And at this point such people who don’t live in America can get a little over excited. I can work in America woohoo. No green card or resident alien stuff for me! Transiting through LAX will be a breeze.

All true. But much like the British Royal Family – US citizenship is also the gift that keeps on giving.

Now dear readers we have covered tax residence of individuals before. The tests that determine whether a country can tax on the foreign income of its inhabitants. And most countries have some version of the being here or owning stuff rule to work out whether someone is tax resident.

But thanks to American exceptionalism they go one step further. The US applies residence taxation to its citizens even the ones who don’t live there. So with foreign income and US citizens it is now possible to have the country of the source of the income, the country of ‘main’ residence and the US in the mix. So for Harry’s kids: with that Bermuda dosh: there could be Bermuda; United Kingdom and the United States all with their hand out. Just as well Bermuda not big on taxation. Such a relief. That is if Hazza pays tax in the first place.

Now for lesser New Zealand mortals who might be born in the US or have a Meghan Markle equivalent mum or dad: the US/NZ tax treaty is kinda important. And if they have income from any other country that country’s US treaty will also be your friend.

Because in all those treaties is a nifty little clause called Relief of Double Taxation. Aka such a relief – no double taxation. So let’s look a a situation where a New Zealand tax resident with a US born mum – NZUSM – earns $100 Australian interest income. Australia will deduct 10% tax or $10. New Zealand will also tax that income and another $23 ($33-$10) tax will be paid in New Zealand.

Then – because who doesn’t love a party – so will the United States. Giving an Australian tax credit of $10 and a New Zealand tax credit of $23. Depending on the US tax rate for the NZUSM – they will have to pay more tax; pay no more tax; or get surplus credits to carry forward.

Now for something like interest or any other income source New Zealand taxes; this is just annoying. Maybe a bit more tax to pay but not the end of the world.

The full horror comes when NZUSM has types of income that the US taxes but NZ doesn’t. You know like capital gains? Taxable in the US. And the horror becomes squared when NZUSM realises that the US uses its – not NZ’s – tax rules and classifications to calculate the income. Who would have thought?

So that look through company or loss attributing qualifying company where income has been taxed in hands of shareholders – treated as company the US – maybe not so clever after all. Coz what about a LTC loss that was offset against the taxable income of NZUSM – coz it is all like the same economic owner? US – no loss offset allowed – full tax now due. In the US the LTC is discrete NZ company. Nothing to do with NZUSM.

And then of course there is FATCA. For like ever the US has a requirement that its foreign based citizens report their balances with foreign banks. Now quelle surprise – compliance wasn’t great. So the US then said they would collect the information from the foreign banks directly and if they didn’t comply they’d impose a 30% tax on fund flows from the US. Did concentrate the mind somewhat.

Now the US is using this information to enforce compliance. And the NZUSMs of the world are not best pleased. Finding out there was a dark side – albeit one pretty well known – to the whole I can work in the US thing. Unsurprisingly there is a wave of people seeking to renounce their citizenship. Alg except the tax thing goes on for ten years after such renunciation. And such renunciation can’t be done by parents for their children.

So while Harry may have finally found his bride; he has also found the US tax system. What could possibly go wrong?

Andrea

Deregos

Let’s talk about tax.

Or more particularly let’s talk about the tax rules for deregistering charities.

It has been a big intellectual week for your correspondent. Tuesday night White Man Behind a Desk. No tax. An interesting riff on immigration that Michael Reddell clearly wasn’t the tech checker for. Wednesday night Aphra Green Harkness Fellow on US criminal justice reform coz States just ran out of money. I tried to run an argument that this was the good side of low taxes. Didn’t resonate – go figure. And Wednesday morning – Roger Douglas on turning taxes into savings coz #taxesaregross.

And it was on the lovely Roger I planning to write but on Friday was the Greens on how there were bugg@r all foreign trusts reregistering. So I thought I’d write about that and the genius decision to require disclosure rather than taxation.

And as if that wasn’t enough. Saturday morning the latest Matt Nippert on a US and charities thing. An elderly couple with no heirs wanting to transfer wealth to a charitable institution – awh lovely. So nice they chose NZ. But also Panama, low distributions and references to the IRS. Ok. Initial reaction was it looks like FATCA avoidance coz NZ charities are outside its scope of reporting to IRS. Really must get on to my ‘US citizenship is not a good thing for tax’ post. It has been in the can for longer than this blog has been running. So embarrassed.

But one thing really caught my eye. The charities had voluntarily deregistered. Mmm interesting.

Your correspondent now moves a tiny bit in the Charities NGO sector. And from time to time I hear ‘should we stay a charity? Coz need to be careful over advocacy and ActionStation isn’t a charity and it is alg for them.’

To which I try to reply in my best talking to Ministers language: ‘ That’s one option. It would mean handing over a third of your reserves in taxes or all of your reserves to another registered charity. But totes – if that is what you want.’

Strangely the conversation doesn’t continue.

Coz the law changed in 2014 to stop the rort of charities getting lots of lovely tax subsidised donations, not distributing; deregistering and then keeping all that lovely taxpayer dosh for themselves. Go Hon Todd!

Now on the face of it this should apply to our friends here very soon. Section HR 12 applies a year after deregistration and turns the reserves – less wot go to another charity – into taxable income.

Except there doesn’t seem to be anything explicit that makes it New Zealand source income. Possibly personal property or maybe indirectly sourced from New Zealand. But the source rules are kind of old school and want to bite on real stuff not deemed income. No matter how worthy of New Zealand source taxing rights it should be.

And of course none of this matters dear readers if the entity is New Zealand resident. Coz everything gets taxed! And as the trustees are a New Zealand company – high chance it will be. So alg.

Well almost.

Coz if the dosh in the charity all came completely from non-residents – the trust rules make it a foreign trust. And foreign source income aka income wot doesn’t have a New Zealand source is not taxed. So initial view – unless the source rules can bite on this deemed income or the trust isn’t a foreign one – there will be no wash up for our friends here.

Now on one level that is cool. The final tax was all about clawing back the tax benefits given on the initial donations and the charitable tax exemption on income. Here it would have been tax exempt anyway. So alg.

The other argument is that these guys intentionally registered as a New Zealand charity. Got all the good stuff like potentially non- disclosure to IRS as well as being to say they are a legit NZ charity. But now don’t get the bad stuff.

And NZ gets the bad name but not the income. What does that sound like? Oh yes the NZ Foreign Trust rules.

So glad that – according to the Greens – is coming to an end. Shame it had to be such a resource intensive way of doing it.

Andrea

‘Taxes are gross’

Let’s talk about tax.

Or more particularly let’s talk about the deadweight costs of taxation.

For those of you who have liked this blog’s Facebook page you will know that your correspondent was recently a little over excited at getting a credit for tech checking White Man Behind a Desk‘s video on Tax Avoidance.

For those who have yet to watch it. Do it now! Like immediately. The rest of this post can wait.

There are a number of videos in their stable including indigenous rights; prisons and now Tax. My world is complete.

Particular favourite is the one on Social Bonds. ‘That’s friendly Pierce Brosnan and friendly Daniel Craig’. Again its like they made it specially for me. It has tax and prisons. Including a brilliant discussion of contracting out and Serco’s role. Who are now apparently also bidding for: ‘the nighttime; the colour Magenta; and the feeling of hope.’

If I could just like teach Robbie some more tax – he could so take over this blog.

Anyway no more spoilers – go and watch this one too. Please come back though. You can like us both. Wellington peeps WMBAD is live at Circa. Go and see him!

Now in Social Bonds is a quite inspired discussion of tax economics – aka taxes are gross. And also a pretty good imitation of tax economists. Robbie – if you are reading this change ‘incentives’ to ‘distortions’ and you will have totally nailed it.

For the rest of you as a bit of a public service I thought I might unpack the ‘nya, you know ahh, mnew, gross’ discussion at 1 minute 30. Coz in that Robbie is talking about the deadweight cost of taxation.

Now we all know about the compliance cost aspect of taxation. And should we ever doze off on that one the Business lobby groups will be more than happy to remind us. And we all also know about the administrative costs of taxation – aka the great public service that is Inland Revenue. But the cost of taxation through behavioural changes is often hidden or not acknowledged.

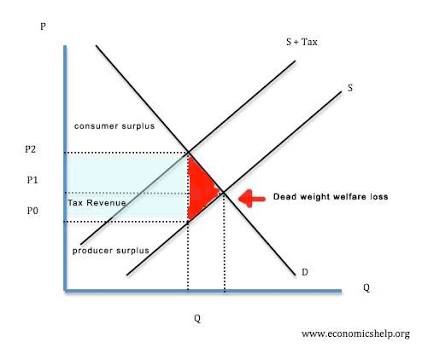

And these behavioural changes are called deadweight losses or excess burden or efficiency losses. They relate to the activity or production or purchase that won’t happen simply because there is a tax on it. The other costs – compliance and administration – are still real ones but in these diagrams they are assumed away to explicitly show the economic costs.

This is to be contrasted with the loss of income or wealth that has simply been transferred to the government in the form of taxation. In our diagram the deadweight cost is in red and the tax collected in blue. Interesting colours politically. Possibly an American diagram.

Now the degree to which this happens is a function of the ‘elasticity’ of whomever or whatever is subject to the tax. Aka the slope of the demand or supply curve.

And the textbook example of a product that is highly inelastic is insulin for diabetics. The demand for it will occur irrespective of its price. Taxing it will be a one for one transfer from the diabetic to the consolidated fund. This is the theory. And as the mother of a Type 1 diabetic can confirm it is also totes the practice. In this case the demand curve will be completely vertical meaning no deadweight cost. Woohoo or total tax grab – up to you which one.

All blue now no nasty red.

Cigarettes from memory has an elasticity of .5 meaning it isn’t a total tax grab as there will be a reduction in actual demand with a tax increase. But still fairly inelastic.

Income tax is much harder. I do know in the early 2000s when I returned to work and still had young children, the 39% tax rate actually made my decision to cut my hours easier.

And Treasury looked at this for the natural experiment that was the 39% tax rate. They found for wage income the elasticity was 0.414 – so more elastic than insulin but less than cigarettes. And for non-wage income it was 0.909. Although with non-wage income the genius decision not to lift the trust rate at the same time means it could be recharacterisation of the income rather than no longer earning it.

And yeah I know I have mixed up demand and supply in the chat above but the guts is all the same. More inelastic the whatever is – if you impose a tax on it the lesser the behavioral change and the lower the deadweight cost.

Now the decision to talk about all this stuff dear readers isn’t just a mind w@nk on my part. Last week as you may remember the lovely Hon Steven announced that his benevolent government was planning to cut taxes through the increase in thresholds. Well only if you like vote them back in. Coz its not like the red team will give it to you even if the green team voted for it …? Too hard for me. Think I’ll stick to tax.

So with $2 billion a year to spend – what are the efficiency gains/reduction in deadweight losses? Turning to the – focus group named – line item Consequential Adjustments. Page 26. Nothing. There is a discussion of an increase in consumption and higher business profits coz people get more money to spend. But no actual mention of any increase to labour supply as a result.

But looking at the RIS though page 28 – there is expected to be a 0.28% increase in labour supply aka reduction in deadweight cost from the package chosen.

Yep. 0.28%. Aka 0.0028. Not quite sure my aging focal length can pick up something so small.

But then that makes sense. The deadweight loss thing operates on the marginal rate and there wasn’t much of a change in all of this.

Now let’s all take a moment to think about what they could have done. Smooth out the tax and transfer interface. Here the effective marginal tax rates are pretty nasty.

And with $2 billion a year to spend it wouldn’t have been too hard to have created quite meaningful efficiency gains from focussing on those.

Then that really would have been a budget for low and middle income families.

Andrea

Two bills one week

Let’s talk about tax.

Or more particularly let’s talk about the two tax bills that were introduced this week.

Some time last century dear readers your correspondent was a junior accountant for an oil company in the UK. And in that company was a low cost petrol retailer. Now one day in the early nineties all staff – yes even the accountants – were called into some marketing meeting. Purpose of meeting was to explain some new wizard marketing strategy that we could all sing and dance around.

But before that particular experience some faceless but well dressed consultant treated us to some research. It was on customer behaviour and why customers chose one petrol station over another. Riveting stuff. And have to say the monthly accounts I would normally be doing at this time were starting to look pretty good.

Now pretty much like every consultant presentation I have sat through before or since – the insights were off the scale. People chose our petrol stations because of: location; retail stuff and coz we were cheap. Genius. Worth every penny. So glad they got the specialists in for that.

But then they dropped an actual knowledge bomb on my 25 year old self. As well as the blindingly obvious stuff – there was an actual true story group of customers that used our stations just because we said we were low cost. And for this group it didn’t actually matter whether we were low cost or not. Saying it was enough. Twenty five year old mind blown. The facts didn’t matter.

Now all of this came back to me this week with the Budget and the Family Incomes tax bill that was introduced and passed this week. A Budget that was for low and middle income families. Or as some commentators are dubbing it – a left wing budget.

Wow. Just wow. The facts still don’t matter.

Now it was Hon Steven’s big day out. Tax cuts for everyone!!! Just under 2 bill per year on tax cuts alone. And while there was other stuff. Vast bulk of the cost comes from tax cuts. Not entirely sure that this was what JustSpeak had in mind with its #billionbetterthings strap line but I guess tax cuts is preferable to any more bloody prisons.

And of course anything involving tax – even adjusting thresholds rather than rates – means more money goes to higher earners. It just does. It’s just what happens when you play around with tax stuff rather than transfer stuff. Coz higher income earners are the people who pay are the people who pay most of the income tax for individuals. So any cuts in income tax go to those who pay the income tax.

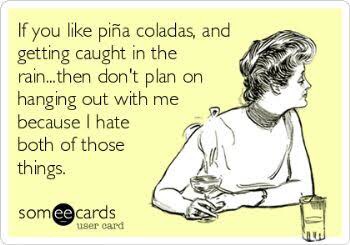

Oh and tax stuff applies to individuals not families. But I guess the clever Treasury people were able to turn this into a family costing below.

But then taking these lovely numbers and annualising them you get this:

Soooo families with incomes over $84k get half the dosh. Very progressive.

Even if those families didn’t actually want the princely sum of $35 per week and might have preferred it to go to mental health, or more state houses or more refugees. But at least it was only one new prison not three! #smallmercies.

But hey this is the party that has been elected. They can kinda do what they like. But a raid into Labour’s territory? Really? I guess if you say it often enough it must be true.

And then for comic relief was the political equivalent of a wardrobe malfunction. Hon Steven said that only one third of those eligible for IETC claimed it in a year rationalising its repeal. But then following questioning from the Michael Wood, Tim McIndoe kindly clarified that yes it was more 30% during the tax year and another 50% at the end of the year. Right ok. 80% not 30%.

And to be fair in the like actual Budget speech Hon Steven did say ‘during the tax year’. So not like actually lying. And in reality more likely a mix up in the bureaucracy than any intention to mislead.

But to your correspondent Budget 2017 – whole thing – deeply underwhelming. Just hope they didn’t also waste money on consultants as well.

Now ironically there was another tax bill that was also introduced last week that actually was a raid into Labour’s territory. Making everyone pay their fair share and all that. For top earners anyway. The Taxation (Annual Rates for 2017–18, Employment and Investment Income, and Remedial Matters) Bill. Just trips off the tongue. And on the whole it is a standard dull but worthy tax bill. Except for Employee Share Schemes. A well buried piece of social justice aka base maintenance.

Now the commentary and the previous discussion document are eye wateringly technical. Even your correspondent struggled. But buried in the RIS – para 54 – is the comment that it will raise $30 million a year. Now tiny in comparison to Steven’s big day out but quite a bit for a base maintenance item that deals with the taxation of remuneration. Especially since this is a net amount and there is an extension of a tax expenditure promoting widely offered share schemes. #workerparticipation.

Coz while yeah there are holes in the taxbase generally – all the remuneration stuff tends to be pretty water tight.

It all seems to have started life with a Revenue Alert that the department issued in late 2015. There they set out two wheezes that quite honestly could really only be used by important and well remunerated employees. People for whom the top tax rate is pretty much their average top rate. Coz honestly what employer could be bothered going to this amount of effort for ordinary employees.

Now currently the law pretty much says that if employees get shares then the difference between their value and what they pay for them is income. Makes sense.

But the Revenue Alert talks of a situation where:

- An employee buys shares on day one for market value. Awesome no taxable income there. No transfer of value. Alg.

- But they buy them with an interest free loan. Nah still cool. The value is in the interest free part and that is catered for by the Fringe Benefit Tax rules.

- Now there is a specific exclusion for interest free loans for employee share purchases. Mmm. Nah still ok. This is a specific concession and while it is an interest free loan – it is still a loan and needing repaying even if the shares go down. So yep still alg.

Except the wheeze is that the loan can be fully repaid by just handing the shares back. Ahh wot?

So if the shares go up – the difference is an untaxed capital gain but if they go down – nowt. Mmm no. Now the lovely Commissioner has quite correctly said – yeah nah – tax avoidance. And coz this is all connected to employment is looking to tax the gain as remuneration. Yep with you there Mrs Commissioner.

Now applying the tax avoidance provision all over the place is no way to run a tax system. So Hon Judith’s bill applies if you buy shares from your employer but you aren’t subject to the risk of them declining in value – aka not held ‘at risk’. In those situations when you get actual value from the transaction – that value is taxable. You know kinda like how when you are on a promise for a bonus – when that bonus actually materialises it is taxable? Yeah just like that here too.

Now yeah what ‘at risk’ means might not be super clear but tax avoidance audits aren’t super fun either. And as my late dear friend Tim Edgar would have said – just stay away from the edge. Everyone else pays tax on gains from their employer – so should the employees whose employers can be bothered to do clever stuff for them.

And this is what a socially progressive tax bill actually looks like. Hope it survives select committee.

Andrea

Cry me a river

Let’s talk about tax. Yes dear readers – tax. No prison reform no yoga stuff. Just nice emotionally simple tax.

Or more particularly let’s talk about the recent Australian Budget announcement of a levy on banks aka the Great Australian Bank Robbery.

Your correspondent has now completed her yoga teacher training and so is available for weddings, funerals and bar/bat mischvahs. Highlights of the course included injuring herself while dancing and getting zero on the first attempt on the final exam.

It’s not like I haven’t failed things before but when the question was – reminiscent of the Peter Cook coal miners sketch – ‘who am I?‘ to fail – mmm – more than a little surreal. Now even the first time thought I had answered in a sufficiently right brained way – lots of introspective emotion involving personal power and connection with others – aahhh no.

But your correspondent is a resilient adaptive individual – even before the course – so regrouped with – ‘complete‘.

90%.

I couldn’t make this up. Subsequently found other correct answers included: me; enough – and my particular favourite – light. Ok right. Thanks for sharing.

And it all really did make me crave balance. Which in my world after eight full days on yoga is the left-brained world of tax. I had planned to write about the Australian transfer pricing case Chevron but this week has been the Australian Budget with a big new tax on their banks. And as I have had a few questions on this and I am trying to be more topical – here we go:

Now the bank tax thing seems to be part of a package of the Australian government responding to the Australian banks bad – but probs more likely monopolistic – behaviour. Also potentially a political response to appointing a popular Labour Premier – and good god a woman – to be head of the Bankers Association. And my word the banks must have been bad as they only found out about it on Budget Day and it starts on 1 July without – as far as I can see – any grandfathering.

Wow. Just wow.

So what is it?

It is a levy on big banks liabilities that aren’t:

- customer deposits or

- (tier 1) equity that doesn’t generate a tax deduction.

It targets commercial bonds, hybrid instruments (tier 2 capital) and other instruments that smaller banks can’t access coz they are small. And as it will form part of the cost of this borrowing- under normal tax principles – the levy would be tax deductible. But even allowing for this tax deduction it is supposed to raise AUD 6.2 billion over four years. So not chump change.

What is its effect?

Now there can be no argument that the levy will effectively make such instruments more expensive to use. And here the public arguments get really sophisticated:

- Malcolm Turnbull says that ‘other countries have them’ and it would be ‘unwise’ for banks to pass it on to borrowers; and

- the Treasurer Scott Morrison (ScoMo) is telling banks to ‘cry me a river’ when they have expressed a degree of displeasure.

Awesome. Thanks for playing.

Corrective taxation

Now while this is predicted to raise revenue; it is by no means clear that this is its primary objective or even if it will occur. The reason being it only applies to big banks and to certain types of liabilities. To me this looks like a form of corrective tax like cigarette excise rather than a revenue raiser like an income or consumption tax like GST.

And much like a tax on cigarettes; pollution or congestion; this tax is 100% avoidable – legitimate tax avoidance even – by funding lending with an untaxed option like customer deposits. In theory anyway. It is likely that banks will have maxxed out how much they can borrow from the public at existing interest rates.

But with this extra tax; the relativities will change. Meaning there is now scope to pay more for the untaxed deposits but less than the tax if Banks want to maintain the same level of lending. Bank costs will still go up but through marginally higher deposit rates incentivised through the tax – rather than the tax itself.

In this scenario the Australian government still gets the costs of the higher interest deduction but not the revenue. But Australian savers win.

As the big banks are the dominant players in the market – this increase in interest rates for depositors will also impact the smaller banks as they will need to pay the higher rates to continue to attract depositors too. So no actual competitive pressure from the small banks and possibly less actual tax. Genius.

An alternative equally revenue enhancing scenario is that banks wind down assets – lending – and become smaller. Less lending but higher cost of borrowing if demand stays the same.

Who bears the cost?

As they do in New Zealand anytime extra taxes are mooted; the Australian banks are arguing that these extra costs will be borne by borrowers. Now in a fully competitive market without barriers to entry the more price dependent – or elastic – the demand for loans is the more it will fall on the shareholders. But lending overall will fall with the imposition of a tax which in turn will have housing market impacts if fewer people can get a mortgage.

With barriers to entry – like hypothetically say banking regulation – they are already pricing to maximise their profit so I would be inclined to say it will also hit shareholders. And the fall in price of banking shares would indicate that is what shareholders think too.

Except that if deposit rates go up instead; the cost structure of the entire banking industry will go up. And if no tax is actually being paid but the cost is being transferred through higher deposit rates then the banking industry will have political cover to pass the cost on to borrowers.

Alternatives

Now if this schmoozle is all about the banks paying more tax then either a higher company tax rate on big banks or increasing the requirements for non- interest bearing capital would have been far simpler. While the former is pretty transparent that it is a blatant tax grab from the banks; the latter less so. They both have the advantage though of ensuring tax can’t be opted out of as well as keeping the competitive pressure from the smaller banks.

But both would form part of the banks cost structure and so – depending on the pressure from the small banks and how elastic demand is – be passed on in some form to borrowers. However if the government really wanted only the shareholders to pay then a one- off windfall tax would be the way to do it.

Whether or not the banks – and their shareholders – should actually be treated like this is another story. But Cry me a river ScoMo: at least be transparent and do it properly!

Other stuff

It goes without saying that this is truly cr@p process. All the detail seems to be in ScoMo’s press statement. Although – legislation by press statement – is an unfortunate feature of Australian tax policy.

And as for the Malcolm Turnbull ‘other countries have it too’ argument. From what I can see this was to pay back the government for the bail outs they gave the banks over the GFC. While Australia does have deposit insurance I wasn’t aware of any like actual bailouts.

It is though kinda reminiscent of the diverted profits tax which is also a targetted tax on a group of bad people. Except that might have a non-negative tax effect. Here we have – to extent it is passed on in higher deposit rates – higher costs industry wide causing less, not more, tax paid by this industry. Let’s just hope for Australia’s sake the savers are not all in the tax free threshold.

So nicely done ScoMo and Big Malc. Possibly more Lavender Hill mob than Ronnie Biggs. But much like the Australian fruit fly; keep it on your side on the Tasman. It makes even this revenue protective commentator blanch and our banking tax base can so do without it.

Andrea

Update

A commentator on the blog’s facebook page has suggested that this levy makes sense in terms of addressing the huge implicit subsidy that is the Australian deposit guarantee scheme. I have absolutely no issue with this being charged for in the form of a levy on the banks. Naively I would have thought that such a levy would then be based on the deposits covered by the guarantee not the liabilities that aren’t. Apparently that’s not how Australian politics works!

The discussion can be found in the Facebook comments section for this post.

I am into champagne

Let’s (not) talk about tax.

Let’s talk about yoga stuff.

As part of her assessment for yoga teacher training your correspondent has had to read B K S Iyengar’s Light on Life and write 500 words on something that ‘spoke to me’. As 500 words is blog length and we have now all handed in our essays I thought I’d post it as a bit of ‘light’ relief after all the tax stuff.

Think of it – dear readers – as the blog equivalent of alternate nostril breathing which is supposed to balance out the hemispheres of your brain. Although that exercise after a couple of rounds doesn’t so much balance out your left brained correspondent as make her want to run screaming from the room. So like all yoga; work with your comfort levels and rest or stop when you need to. Listen to your body.

But first a bit of background. Yoga is not actually what non-yogis think it is. Non-yogis think of it in terms of contortionist poses – that they are like far too stiff or inflexible to do. And this isn’t helped by the whole instayogi thing. Beautiful fit young people doing postures average people can’t do on beaches or tropical islands that average people can’t afford to go to.

There are 8 limbs of yoga: the postures or asanas are but one of them. And that not to under rate them. As an ex runner I would say: come for the flexibility; stay for the brain calming and inner peace.

I had hoped to work in the ideas of Marianne Elliott social activist and yoga teacher. In particular her framework for progressive social change which I have paraphrased (and adjusted slightly) as involving:

- The official rules laws and structures we live by;

- How we treat each other; and

- How we treat ourselves.

And it is in the latter that yoga is referenced. But the essay I have to write is very short and I didn’t start soon enough to do a decent job with both Marianne’s and Iyengar’s ideas. For people who are interested in this combination I would suggest reading direct from Marianne’s work and skipping the rest of this post.

And yes this will be the last non-tax post for a while. Yes it is a tax blog and I will return to tax stuff in a couple of weeks after my teacher training is over.

Andrea

“We have been asked to read Iyengar’s Light on Life and write about what spoke to us. It is fair to say that yoga has changed my life. But not in a way that is particularly obvious from the outside.

My family has REALLY BAD GENES meaning living as long as I would like may not be possible. So I have organised my life to ‘do something different’ when I turned 50. That ‘something different’ broadly is working for progressive social change.

So this was in my head reading Light of Life. To be fair while I struggled with the book; there were a few things that really did resonate with me:

Role of asana

Iyengar says that asana is the physical process that relaxes the mind which in turn allows pranayama – breathing – to unlock the prana – energy – blockages in the body. Which in turn calms and focuses the mind.(Page 14)

This is absolutely my experience. In the time leading up to my fiftieth birthday I had many competing ideas and emotions. Normally would rush to decisions that may or may not be the right ones for me and those around me.

Now it was my physical yoga practice that I kept coming back to. It might have sorted out my posture but more importantly it kept my mind clear and proceeding with calmness and focus.

I am a little nervous though of his concept of right pain as a tool for growth (page 49). As what I had thought to be ‘right pain’ in chaturanga has lead to a shoulder I am still trying to fix a year later.

Asteya and Aparigahaha

Non-stealing and non-covetousness like non-violence ahimsa, are tenets that are blindingly obvious ones for any philosophy. Iyengar, however, takes them further than I have seen before.

Non-stealing includes not taking more than you need. When combined with non-covetousness this means that taking more than you need could mean deprivation for others. And to Iyengar wealth being tied up in a few hands is also theft or covetousness.

To be faithful to these yamas wealth – as energy – must circulate otherwise ‘it will stagnate and poison us’. ‘Energy needs to flow or its source withers.’ (Page 245) This particularly resonated with me given according to Oxfam 8 men have as much wealth as half the world.

What I am increasingly seeing in New Zealand – through our out-of-whack property market – is wealth being captured through those that own property from those that don’t. And so by capturing all the wealth we are poisoning our children’s potential to live the lives we have lead.

But here’s the thing. Those who have the most won’t let that happen to their children. So opportunity and material comfort will only be available to the children of families that already have it. The exact social ill that families such as mine were escaping 100 years ago by coming to New Zealand.

So although Iyengar’s primary message was of one of inner freedom – embedded in that was the other eternal truth – that the personal is political.”

Being there

Let’s talk about tax.

Or more particularly let’s talk about tax residence.

There is currently is a big to do about Peter Thiel both here and in the foreign press about exactly how did a US billionaire become a New Zealand citizen. Soz can’t help with that. But on my Facebook feed this morning is coming the question – so is this guy tax resident? Now that I can do off the public stuff and is pretty much probs yeah/nah. But citizenship – scmitzerzenship – really not relevant much at all.

There are many concepts of residence used in the bureaucracy. The main one is permanent residence – an immigration concept – which pretty much gives the recipient the rights of a citizen except maybe you can’t stand for Parliament.

Tax residence however – who would have thought – is a completely different concept. While in practice most New Zealand permanent residents and citizens will be tax residents. It is by no means a dead cert.

Now why tax residence matters is that residents are taxed on any foreign income earned and fully taxed on New Zealand income. Tax non-residents are not taxed on foreign income and have concessionary rules on how New Zealand income is taxed. Think Google.

For an individual there are two ways – you can become tax resident and a number of ways you effectively lose it.

The two ways are:

- Being here – an individual who is physically in New Zealand for 6 months in ANY 12 month period becomes New Zealand tax resident.

- Connections to New Zealand – even if you are here less than 6 months in any twelve month period if you have a house you live or have lived in while you are here AND you have other connections you will become subject to tax in New Zealand on your foreign income.

So looking at Mr Thiel. According to reports the dude has two houses in New Zealand. Combined with his New Zealand citizenship and the stuff wot he did to demonstrate commitment to NZ – not free from doubt but – I would say there was a pretty high chance he would hit the connections to New Zealand test. And yes tax friends I am talking about a permanent place of abode but there are non tax people who read this and we’d all agree as terms go it is not the most intuitive.

Now you might be thinking dear readers – woohoo – New Zealand can tax his foreign income. Hello mega surplus and Scandinavian levels of public services.

Ah but not so fast there is now the small matter of the US/NZ tax treaty.

On the basis that he is a ‘naturalised American’ he is also tax resident of the US and they will also claim taxing rights on his foreign income. And here the treaty will sort that out:

- First question is which is the country where he has a home available to him? Ah probs both. Next question.

- Second question which country is where his personal and economic ties are stronger? Mmm tough. A late forties ‘naturalised American’ with business interests there and a confidante of the President v really likes NZ and invests in tech companies. Tricky but I think we can call it for the US.

Now is this tax dodging or tax avoidance? Should we feel aggrieved as New Zealanders that he is a citizen but unlikely to be a tax resident?

Me nope.

I defo don’t think this is tax dodging or tax avoidance as there is nothing cute or clever or structured in being taxed where your stuff is and where your links are stronger. Given the NZ diaspora who are NZ citizens – not all of them will be residents under the two tests and even if they are they will also have the benefit of their treaty. And in theory anyway he should be paying tax on his foreign income in the US.

But I can only hope that when the ‘exceptional circumstances’ were being weighed in Mr Thiel’s application the Minister knew that while we were getting a citizen – given how international tax works – it was unlikely we were getting a taxpayer.

Andrea

Two men one press release

Let’s talk about tax.

Or more particularly let’s talk about Oxfam’s recent press release on inequality and tax.

Now dear readers when I moved to weekly – hah – posting it was because this blog was supposed to be my methadone programme. Getting me off tax and on to other issues. So when I posted last night – after having posted 3 times last week – I gave myself a good talking to. This had to stop. One post a week was quite enough to keep the cravings at bay. To continue in this vein would risk a relapse.

But this morning while I was getting dressed my husband came and turned on the radio. Rachel LeMesurier from Oxfam was talking about inequality and then she talked about tax and then Stephen Joyce came on and then he talked about tax and then he talked about BEPS.

Just one more little post won’t hurt I am sure and I’ll cut down next week honest.

Oxfam has compared the wealth of 2 New Zealand men Graham Hart and Richard Chandler to the bottom 30% of all adult New Zealanders. Now the inclusion of Richard Chandler seems to be a rhetorical device as from what I can tell he hasn’t lived here since 2006. So very unlikely to be resident for tax purposes.

In the interview Rachael Le M also made reference to the tax loopholes that support such wealth. So using what is public information about Graham Hart and what is public about the tax rules I thought I’d make a stab at setting out what these ‘loopholes’ are.

Now first dear readers please put out of your head anything you have heard about BEPS or diverted profit tax or any of the ways that the nasty multinationals don’t ‘pay their fair share of tax.’ None and I repeat none of this is relevant when dealing with our own people. It might be relevant for the countries they deal with but not for New Zealand. I am hoping that officials will also explain this to new MoF Steven Joyce as when he came on to reply to Rachael – he talked all about BEPS. Face palm.

Graham Hart is a serial business owner. Buying them sorting them out and then selling off the bits he doesn’t want all with a view to building up a Packaging empire. A Rank Group Debt google search also indicates that a substantial proportion of all this buying and selling was done through debt. And at times quite low quality debt which would indicate a proportionately higher interest rate. A number of his businesses are offshore.

So then what ‘loopholes’ – or gaps intended by Parliament – could Mr Hart be exploiting?

The first and most obvious one is that there is unlikely to be any tax on any of the gains made each time he sold an asset or business. The timeframes and lack of a particular pattern – as much as Dr Google can tell me – would indicate that the gains would not be taxable.

The second is that income from the active foreign businesses will be tax exempt and any dividends paid back to a New Zealand will also not be taxed. Trust me on this. I’ll take you all through this another day.

The third relates to debt. Even though it assists in the generation of capital gains and/or the exempt foreign income it will be fully deductible. Now because of the exempt foreign income there will potentially be interest restrictions if the debt of the NZ group exceeds 75% of the value of the assets. A restriction true but not an excessive one given exempt income is being earned.

Now also in Oxfam’s press statement is a reference to a third of HWIs not paying the top tax rate. I am guessing some version of one and three plus the ability to use losses from past business failures is the reason.

Unsurprisingly Eric Crampton of the New Zealand Institute is not sympathetic to Oxfam’s views and points to our housing market as the main driver of inequality. So then in terms of tax and housing the other tax ‘loophole’ then would be the exclusion of imputed rents from the tax base.

Now one answer could be Gareth’s proposal. That is if someone could explain to me how to tax ‘productive capital as measured in the capital account of the National Income Accounts’ in a world where tax is based on financial accounts according to NZIFRS.

The second could be a capital gains tax even on realisation and the third some form interest restriction or clawback when a capital gain is realised. Oh and taxing imputed rents.

How politically palatable is this? Not very given National, Labour, Act, New Zealand First and United Future are all opposed to a capital gains tax – at least Labour for their first term.

But then maybe it is stuff for Labour’s working group. Will be interested to see this all play out.

Andrea

Destination anywhere

Let’s talk about tax.

Or more particularly let’s talk about the Republican party’s recent proposal to impose ‘border adjustments’ as a reform of their corporate tax system.

To date this has passed me by. Slowly though things have percolated up to various feeds I follow. All talking about how Trump can balance the budget and punish companies that export jobs. The first I saw looked like a GST where imports are taxed and exports aren’t. Fair enough I thought if the US wants to impose import duties – ok but nothing to do with me. I do income tax not tariffs. I won’t be commenting. Good luck with the WTO on that. And our US tax treaty only covers federal income taxes not value added taxes so no issue there.

Then I saw something that said it was income tax. Sales to foreigners wouldn’t be taxed and purchases from foreigners wouldn’t get deductions. And no interest deductions coz it was a cashflow tax. Whoa I thought – that’s odd. How do you deny interest deductions as they are a cashflow? And what about restricting deductions for local purchase costs when you aren’t taxing foreign income? How’s that going to work?

But in that article Professor Alan Auerbach is talking positively about the proposals. Penny dropped.

A few years ago Prof A came to New Zealand with some other academics and gave two presentations on destination taxation that I am embarrassed to say did not understand one word of. Awesome so that is what this is about and I will have to do some actual work to comment rather than accessing my increasingly failing tax memory.

Having now done some work – that is I found the good professor’s 2010 paper and read it – I can see why I didn’t understand. It is a major change in how income tax systems work and so nothing really would have resonated.

Now let’s see if I can paraphrase the 29 pages.

Focus is on taxing cashflows that originate in the US – so:

- Foreign sales not taxed;

- Foreign purchases not deductible;

- All domestic purchases – including capital items – are deductible;

- All domestic borrowings – full amount borrowed not typo keep breathing – are taxable;

- All domestic lending is deductible; and

- Foreign borrowing and foreign lending – not respectively deductible or taxable.

Wow just wow. So wish I had followed this when Prof A came out. I would have had soooo many questions.

The advantages of this are said to be:

- Tidies up the US treatment of foreign income and removes the incentive to move US income to havens because the US would tax it even less. Yep agreed.

- Treats debt and equity equally and removes the tax preference for debt. Yep does that too as while capital items are fully deductible the full amount that is borrowed – so long as it is borrowed domestically – is taxed.

Issues with this though kinda are:

- Not only originally US income could find its way back from abroad. So could most actual foreign income actually earned overseas – as Auerbach is proposing the US become the MacDaddy of tax havens.

- No deductions for foreign purchases but deductions for the same domestic purchase. Mmm what does that sound like? Ah discrimination according to the US/NZ treaty – is what it sounds like. Article 23(4) to be precise.

- Foreign purchases not deductible but domestic sales taxable. Mmm how long will it be before foreign subs start servicing the US market? Now that can be stopped if they reform their controlled foreign company (CFC ) rules – but a CFC is by definition foreign – and isn’t foreign stuff out. It can also be stopped through a reform of the permanent establishment rules as proposed by the OECD but isn’t that a nasty pinko Obama thing?

- Domestic borrowings fully taxable but foreign borrowings not. Too easy. Bye bye local banks. Hello City of London.

There are other things like I am not at all sure that full deductibility for long lived assets is at all the right policy as it doesn’t match the decline in their economic life. So the longer lived the asset the greater the tax expenditure – because why? Is there a shortage of long lived assets in the US economy? And accelerated depreciation was the basis for the double dip leases that were all the rage around and before 2000. But maybe the requirement that the asset has to be in the US will protect them this time.

Now that was 2010 and an academic paper. Let’s see what has actually proposed by policy makers – Paul Ryan nonetheless.

Paul Ryan’s 2016 tax policy allows: full deductions for capital expenditure; repatriation of foreign dividends tax free; ‘border adjustment’ aka taxing imports and exempting exports; ‘streamlining’ subpart F aka CFC rules and denying deductibility for net interest. So pretty much Professor Auerbach’s proposal with a corporate tax cut to 20c and not the foreign bank preference.

As a big interest whinger – here, here and here – I am going to be really interested to see how interest denials stay the course. The rest of the proposal looks pretty standard right wing with a bit of foreign bashing with the foreign purchase deduction denial. But denying interest – wow – that is huge. Further than I would go even with a reduced corporate tax rate. But then maybe the interest deductions will flow into foreign countries at the same time the income is flowing out. All the more reason for New Zealand to a make sure we have interest deductions for non- residents properly sorted. Next week’s post promise.

In Paul Ryan’s thing there are some spurious references to the WTO and how they are mean to the US – I think that is called doing their job – but no reference to the tax treaty breaches. But the IRS international tax counsel know all about these issues and I hope they are being funded properly – coz buckle up boys – their competent authorities are about to get really busy. Oh and it’s Article 23(3) in the US treaty with China.

And the servicing of the US from say Canada and Mexico – don’t know how far drones can fly – pretty sure though it’s higher than the average wall or fence. But that is my bet as to what will happen when imports are denied a tax deduction. Not more tax revenue and not more jobs. And lots of warning for the companies who can start looking at border real estate. Just like the GOP – so very business friendly.

Yep. Making America great again – one own goal at a time.

Andrea