SUPERCommissioner

OVER 2,000 hack attempts and I finally broke into Andrea’s blog. (1) I should have known straight away her password would be CGT4eva. So here I am. Another rare left-leaning socially progressive tax expert.

This may be why Michael Wood, chair of the Finance and Expenditure Select Committee – politely and somewhat bemusedly – said to me: “you realise you are the only submission against this aspect of the bill….this should be interesting”.

The bill is now an Act of Parliament, the Taxation (Annual Rates for 2019–20, GST Offshore Supplier Registration, and Remedial Matters) Act 2019.

I was not the only submitter on the bill.

There were 268 submitters who opposed the ring-fencing of rental losses. Of course there were – some people might have to pay more tax. But, only one submitter (me), was opposing a tiny amendment that was also a blatant disregard for democracy and the rule of law.

And that tiny amendment created the Commissioner’s new superpower.

While Spiderman has quite an extraordinary power to climb, and Magneto has the power to control magnetic fields, much more useful than all that, the Commissioner of Inland Revenue has acquired the power to exempt taxpayers from tax law.

Totally wicked.

This power can be used to make a wide-reaching exemption for all taxpayers affected by the law, or limited to specific circumstances. You know – just special people.

The Commissioner may use her power to correct ‘obvious errors’ in the law. Or to give effect to the law’s intended purpose – as determined by the Commissioner – to resolve an ambiguity in the law, to reconcile inconsistencies between two laws or between the law and an ‘administrative practice’.

The last one is my personal favourite.

The Commissioner may grant the exemption where a tax law is inconsistent with the IRD practice on the issue. Wonderful. So unelected bureaucrats trump Parliament? Although yeah I get that Parliament has given the Commissioner this power. And this quite extrordinary superpower has been granted with little public interest.

There are two reasons for this.

First tax is apparently boring and doesn’t attract great public interest unless one’s own wallet is impacted. The usual submitters (tax geeks) generally represent business interests. The other reason is that the power is likely to operate only in a taxpayer’s interest, not against.

The provisions state that a taxpayer is not required to follow the Commissioner’s edict to exempt a law. Aha not so powerful after all. Taxpayers can choose to follow the strict letter of the law. In other words, this exemption will only be applied for the benefit of the taxpayer, not to their detriment.

So what’s my problem? My concerns are two-fold.

First, I am not comfortable with administrative functions being granted superpowers to circumvent law made by the democratically elected representatives. Second, I am concerned with who will benefit from these provisions.

Segregation of the duties of our government is one of the foundations of New Zealand’s (unwritten) constitution. Law making power is granted to the elected body – parliament – made up of members chosen by the people and crossing all spectrums of society.

Administration of the law is taken up by unelected employees of government. Granting law making (or breaking) powers to an official appointed by the State Services Commissioner crosses the segregation boundaries and undermines the process of law making.

Granting the Commissioner the ability to exempt a law because it is inconsistent with an administrative practice moves into the sphere of law making.

The third branch of government, sitting alongside parliament and the executive, is the judiciary – those who interpret and enforce law.

Granting the Commissioner the power to exempt taxpayers from a law because it is inconsistent with parliament’s intention steps on the toes of the judiciary. It is the judiciary’s role to determine what the intention of parliament might be.

My second concern is somewhat more pragmatic. Who is this superpower designed to benefit?

Most New Zealanders receive all their income from salary and wages and pay their tax through the PAYE system. Most New Zealanders have no need for an accountant and do not even file tax returns.

But if you have more complex financial affairs, you may need an accountant. And if you have lots of money, you might have a very expensive accountant with a great deal of expertise in money matters – including tax. You might have a very expensive lawyer as well. This is good news and has kept me in gainful employment through my working years.

Now, I have spoken with a few of my friends (who have accountants but not the expensive sort), and they tell me they are not aware of the Commissioner’s new superpower. They tell me they are unlikely to be requesting the Commissioner to use her new power in their favour due to – well – ignorance. I have an inkling who may be inclined to use the new provisions, however.

Perhaps those with more complex tax affairs. Perhaps those who use expensive accountants and lawyers. Perhaps those with access to tax knowledge and expertise.

Now the Inland Revenue officials who have reviewed my submission have said, “don’t worry” Alison. The Commissioner’s new superpower is “intended to only be used for minor or administrative matter where there are no, or negligible fiscal implications”. Which would be fine except that’s not what the legislation says.

The superpower is not at all limited to ‘minor or administrative’ matters. It is far broader than that. And as for ‘no or negligible fiscal impact’… what would be the point of exempting a law if there was no or negligible fiscal implications?

And once again, this is not exactly what the law says. It says the Commissioner may only use her power if there are no or negligible fiscal implications for the Crown. Now the last financial year produced over $80bn of tax revenue for the Crown. So I ask, what is negligible in the context of $80bn? Is $20m negligible?

This is up to the Commissioner to determine.

Now I do not mean to suggest any corruption on the part of our tax administration or our current Commissioner. But the law must protect the people from the potential for corruption. And this law steps well over that line.

The use of this superpower will be one to watch. But who will be watching? That is a conversation for another day.

Alison

————————————————————————————————————

(1) I note though that Andrea prefers ‘unauthorised access’ to ‘hack’. But as she invited me in – albeit not through a search bar – she can get over herself.

When Harry met FATCA

Let’s talk about tax.

Or more particularly let’s talk about the taxation of US citizens living abroad.

I just love the Royal Family. Yeah I know it goes against any and every possible progressive and egalitarian ideal I hold but phish.

I grew up reading my grandmother’s Women’s Weekly and their coverage of Princess Anne’s (first) wedding and the Silver Jubilee. Over time this progressed to Diana, Fergie and their babies. And the Womens Weekly became the Hello magazine. Complete with Princess Beatrice aged two at a society wedding. So good.

And season two of The Crown has landed. Brilliant. I mean seriously- what about Philip?

Of course season one was dominated by the spectre of the abdication of a King who wanted to marry a divorced American woman. As well as the sister of the Queen who wanted to marry a divorced man.

So it was with every sense of delighted irony that I watched the recent engagement of Prince Harry to a divorced older mixed race American woman. Whose father might be catholic. ROFLMAO.

And my delight became complete when the Washington Post pointed out Meghan and Harry’s children will be subject to FATCA and US residence taxation. Oh and I have been meaning to write about the joys of US citizen taxation since like forever. So finally here was my angle.

The British Royal family – the gift that keeps on giving.

First key thing is that all people born in the United States or born to at least one US parent – like Harry’s children will be – are US citizens. And at this point such people who don’t live in America can get a little over excited. I can work in America woohoo. No green card or resident alien stuff for me! Transiting through LAX will be a breeze.

All true. But much like the British Royal Family – US citizenship is also the gift that keeps on giving.

Now dear readers we have covered tax residence of individuals before. The tests that determine whether a country can tax on the foreign income of its inhabitants. And most countries have some version of the being here or owning stuff rule to work out whether someone is tax resident.

But thanks to American exceptionalism they go one step further. The US applies residence taxation to its citizens even the ones who don’t live there. So with foreign income and US citizens it is now possible to have the country of the source of the income, the country of ‘main’ residence and the US in the mix. So for Harry’s kids: with that Bermuda dosh: there could be Bermuda; United Kingdom and the United States all with their hand out. Just as well Bermuda not big on taxation. Such a relief. That is if Hazza pays tax in the first place.

Now for lesser New Zealand mortals who might be born in the US or have a Meghan Markle equivalent mum or dad: the US/NZ tax treaty is kinda important. And if they have income from any other country that country’s US treaty will also be your friend.

Because in all those treaties is a nifty little clause called Relief of Double Taxation. Aka such a relief – no double taxation. So let’s look a a situation where a New Zealand tax resident with a US born mum – NZUSM – earns $100 Australian interest income. Australia will deduct 10% tax or $10. New Zealand will also tax that income and another $23 ($33-$10) tax will be paid in New Zealand.

Then – because who doesn’t love a party – so will the United States. Giving an Australian tax credit of $10 and a New Zealand tax credit of $23. Depending on the US tax rate for the NZUSM – they will have to pay more tax; pay no more tax; or get surplus credits to carry forward.

Now for something like interest or any other income source New Zealand taxes; this is just annoying. Maybe a bit more tax to pay but not the end of the world.

The full horror comes when NZUSM has types of income that the US taxes but NZ doesn’t. You know like capital gains? Taxable in the US. And the horror becomes squared when NZUSM realises that the US uses its – not NZ’s – tax rules and classifications to calculate the income. Who would have thought?

So that look through company or loss attributing qualifying company where income has been taxed in hands of shareholders – treated as company the US – maybe not so clever after all. Coz what about a LTC loss that was offset against the taxable income of NZUSM – coz it is all like the same economic owner? US – no loss offset allowed – full tax now due. In the US the LTC is discrete NZ company. Nothing to do with NZUSM.

And then of course there is FATCA. For like ever the US has a requirement that its foreign based citizens report their balances with foreign banks. Now quelle surprise – compliance wasn’t great. So the US then said they would collect the information from the foreign banks directly and if they didn’t comply they’d impose a 30% tax on fund flows from the US. Did concentrate the mind somewhat.

Now the US is using this information to enforce compliance. And the NZUSMs of the world are not best pleased. Finding out there was a dark side – albeit one pretty well known – to the whole I can work in the US thing. Unsurprisingly there is a wave of people seeking to renounce their citizenship. Alg except the tax thing goes on for ten years after such renunciation. And such renunciation can’t be done by parents for their children.

So while Harry may have finally found his bride; he has also found the US tax system. What could possibly go wrong?

Andrea

No accounting for tax

Let’s talk about tax.

Or more particularly let’s talk about accounting tax expense.

Now dear readers the most unlikely thing has happened. A tax free week in the media. No Matt Nippert on charities – just for the moment I hope – no Greens on foreign trusts. No negative gearing and – thankfully – no R&D tax credits. So with nothing topical atm – we can return to actually useful and non-reactive posts. And yes I am the arbiter of this. Although the whole Roger Douglas and his #taxesaregross does warrant a chat. Need to psyche into that a bit first though.

So I am now returning to my guilt list. Things I have been asked to write about but haven’t . That list includes land tax; estate duties; some GST things; raising company tax rate; minimum taxes; and accounting tax expense.

And so today picking from the random number generator that is my inclination – you get accounting tax expense.

At the Revenue when reviewing accounts one of the things that gets looked at is the actual tax paid compared to the accounting income. This percentage gives what is known as the effective tax rate or ETR. And yes there are differences in income and expense recognition between accounting and tax but for vanilla businesses – in practice – not as many as you would think.

Now it is true that a low ETR can at times be easily explained through untaxed foreign income or unrealised capital profits. But it is also true that for potential audits it can be a reasonable first step in working out if something is ‘wrong’. Coz like it was how the Banks tax avoidance was found. They had ETRs of like 6% or so when the statutory rate was 33%.

So when I ran into a May EY report that said foreign multinationals operating in New Zealand had ETRs around the statutory rate – I was intrigued.

Looking at it a bit more – it was clear that it was a comparison of the accounting tax expense and the accounting income. Not the actual tax paid and accounting income. Now nothing actually wrong with that comparison but possibly also not super clear cut that all is well in tax land.

And I have been promising/threatening to do a post on the difference between these two. So with nothing actually topical – aka interesting – happening this week; now looks good.

Now the first thing to note is that the tax expense in the accounts is a function of the accounting profit. So if like Facebook NZ income is arguably booked in Ireland – then as it isn’t in the revenues; it won’t be in the profits and so won’t be in the tax expense.

Second thing to note is that the purpose of the accounts is to show how the performance of the company in a year; what assets are owned and how they are funded. One key section of the accounts called Equity or Shareholders funds which shows how much of the company’s assets belong to the shareholders.

And the accounts are primarily prepared for the shareholders so they know how much of the company’s assets belong to them. Yeah banks and other peeps – such as nosey commentators – can be interested too but the accounts are still framed around analysing how the company/shareholders have made their money.

And it is in this context that the tax expense is calculated. It aims to deduct from the profit – that would otherwise increase the amount belonging to shareholders – any amount of value that will go to the consolidated fund at some stage. Worth repeating – at some stage.

First a disclaimer. When IFRS came in mid 2000s the tax accounting rules moved from really quite difficult to insanely hard and at times quite nuts. Silly is another technical term. That is they moved from an income statement to a balance sheet approach. Now because I am quite kind the rest of the post will describe the income statement approach which should give you the guts of the idea as to why they are different. Don’t try passing any exams on it though.

Now the way it is calculated is to first apply the statutory rate to the accounting profit. And it is the statutory rate of the country concerned. That is why it was a dead give away with Apple – note 16 – that they weren’t paying tax here even though they were a NZ incorporated company. The statutory rate they used was Australia’s.

Then the next step is to look for things called ‘permanent differences’. That is bits of the profit calculation that are completely outside the income tax calculation. Active foreign income from subsidiaries; capital gains and now building depreciation are but three examples. So then the tax effect of that is then deducted (or added) from the original calculation.

For Ryman – note 4 – adjusting for non-taxable income takes their tax expense from from $309 million to $3.9 million. That number then becomes the tax expense for accounting.

But there is still a bunch of stuff where the tax treatment is different:

- Interest is fully tax deductible for a company. But – if that cost is part of an asset – it is added to the cost of the asset and then depreciated for accounting. And the depreciation will cause a reduction in the profits over say – if a building – 40-50 years. So for tax interest reduces taxable profit immediately while for accounting 1/50th of it reduces accounting profits over the next 50 years.

- Replacements to parts of buildings that aren’t depreciable for tax can – like interest – receive an immediate tax deduction. But for accounting a new roof or hot water tank are added to the depreciable cost of the building and written off over the life of the asset.

- Dodgy debts from customers work the other way. Accounting takes an expense when they are merely doubtful. But for tax they have to actually be bad before they can be a tax deduction.

These things used to be known as timing differences as it was just timing between when tax and accounting recognised the expense.

And then the difference between the actual cash tax and the tax expense becomes a deferred tax asset or liability. It is an asset where more tax has been paid than the accounting expense and a liability where less tax has been paid than the expense.

And the fact that these two numbers are different does not mean anyone is being deceptive. They just have different raisons d’etre. Now if anyone wants to know how much actual tax is paid – the best places to look are the imputation account or the cash flow statement. The actual cash tax lurks in those places.

But yeah it does look like actual tax. I mean it is called tax expense.

Your correspondent has memories of the public comment when the banking cases started to leak out. I still remember one morning making breakfasts and school lunches when on Morning Report some very important banking commentator was talking. He was saying that the cases seemed surprising coz looking at the accounts the tax expense ratio seemed to be 30%. [33% stat rate at the time]. But that 3% of the accounting profits was still a large number and so possibly worthy of IRD activity.

Dude – no one would have been going after a 3% difference.

In those cases conduit tax relief on foreign income was being claimed on which NRWT was theoretically due if that foreign income were ever paid out. So because of this the tax relief being claimed never showed up in the accounts as it was like always just timing.

Except that the wheeze was there was no actual foreign income. It was all just rebadged NZ income. And yeah that income might be paid out sometime while the bank was a going concern. So it stayed as part of the tax expense. Serindipitously giving a 30% accounting effective tax rate while the actual tax effective tax rate was 6%.

And a lot of these issues are acknowledged by EY on page 13 of under ‘pitfalls’.

So yeah foreign multinationals – like their domestic counterparts – may well have accounting tax expense ratios of 28%. But whether anyone is paying their fair share though – only Inland Revenue will know.

Andrea

‘Taxes are gross’

Let’s talk about tax.

Or more particularly let’s talk about the deadweight costs of taxation.

For those of you who have liked this blog’s Facebook page you will know that your correspondent was recently a little over excited at getting a credit for tech checking White Man Behind a Desk‘s video on Tax Avoidance.

For those who have yet to watch it. Do it now! Like immediately. The rest of this post can wait.

There are a number of videos in their stable including indigenous rights; prisons and now Tax. My world is complete.

Particular favourite is the one on Social Bonds. ‘That’s friendly Pierce Brosnan and friendly Daniel Craig’. Again its like they made it specially for me. It has tax and prisons. Including a brilliant discussion of contracting out and Serco’s role. Who are now apparently also bidding for: ‘the nighttime; the colour Magenta; and the feeling of hope.’

If I could just like teach Robbie some more tax – he could so take over this blog.

Anyway no more spoilers – go and watch this one too. Please come back though. You can like us both. Wellington peeps WMBAD is live at Circa. Go and see him!

Now in Social Bonds is a quite inspired discussion of tax economics – aka taxes are gross. And also a pretty good imitation of tax economists. Robbie – if you are reading this change ‘incentives’ to ‘distortions’ and you will have totally nailed it.

For the rest of you as a bit of a public service I thought I might unpack the ‘nya, you know ahh, mnew, gross’ discussion at 1 minute 30. Coz in that Robbie is talking about the deadweight cost of taxation.

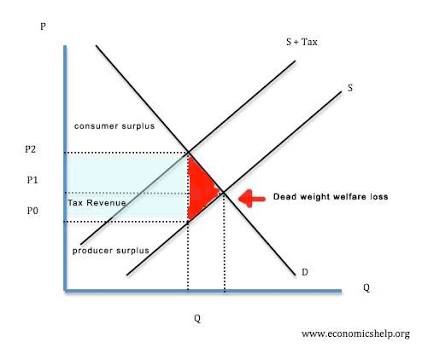

Now we all know about the compliance cost aspect of taxation. And should we ever doze off on that one the Business lobby groups will be more than happy to remind us. And we all also know about the administrative costs of taxation – aka the great public service that is Inland Revenue. But the cost of taxation through behavioural changes is often hidden or not acknowledged.

And these behavioural changes are called deadweight losses or excess burden or efficiency losses. They relate to the activity or production or purchase that won’t happen simply because there is a tax on it. The other costs – compliance and administration – are still real ones but in these diagrams they are assumed away to explicitly show the economic costs.

This is to be contrasted with the loss of income or wealth that has simply been transferred to the government in the form of taxation. In our diagram the deadweight cost is in red and the tax collected in blue. Interesting colours politically. Possibly an American diagram.

Now the degree to which this happens is a function of the ‘elasticity’ of whomever or whatever is subject to the tax. Aka the slope of the demand or supply curve.

And the textbook example of a product that is highly inelastic is insulin for diabetics. The demand for it will occur irrespective of its price. Taxing it will be a one for one transfer from the diabetic to the consolidated fund. This is the theory. And as the mother of a Type 1 diabetic can confirm it is also totes the practice. In this case the demand curve will be completely vertical meaning no deadweight cost. Woohoo or total tax grab – up to you which one.

All blue now no nasty red.

Cigarettes from memory has an elasticity of .5 meaning it isn’t a total tax grab as there will be a reduction in actual demand with a tax increase. But still fairly inelastic.

Income tax is much harder. I do know in the early 2000s when I returned to work and still had young children, the 39% tax rate actually made my decision to cut my hours easier.

And Treasury looked at this for the natural experiment that was the 39% tax rate. They found for wage income the elasticity was 0.414 – so more elastic than insulin but less than cigarettes. And for non-wage income it was 0.909. Although with non-wage income the genius decision not to lift the trust rate at the same time means it could be recharacterisation of the income rather than no longer earning it.

And yeah I know I have mixed up demand and supply in the chat above but the guts is all the same. More inelastic the whatever is – if you impose a tax on it the lesser the behavioral change and the lower the deadweight cost.

Now the decision to talk about all this stuff dear readers isn’t just a mind w@nk on my part. Last week as you may remember the lovely Hon Steven announced that his benevolent government was planning to cut taxes through the increase in thresholds. Well only if you like vote them back in. Coz its not like the red team will give it to you even if the green team voted for it …? Too hard for me. Think I’ll stick to tax.

So with $2 billion a year to spend – what are the efficiency gains/reduction in deadweight losses? Turning to the – focus group named – line item Consequential Adjustments. Page 26. Nothing. There is a discussion of an increase in consumption and higher business profits coz people get more money to spend. But no actual mention of any increase to labour supply as a result.

But looking at the RIS though page 28 – there is expected to be a 0.28% increase in labour supply aka reduction in deadweight cost from the package chosen.

Yep. 0.28%. Aka 0.0028. Not quite sure my aging focal length can pick up something so small.

But then that makes sense. The deadweight loss thing operates on the marginal rate and there wasn’t much of a change in all of this.

Now let’s all take a moment to think about what they could have done. Smooth out the tax and transfer interface. Here the effective marginal tax rates are pretty nasty.

And with $2 billion a year to spend it wouldn’t have been too hard to have created quite meaningful efficiency gains from focussing on those.

Then that really would have been a budget for low and middle income families.

Andrea

Do ron ron

Let’s talk about tax.

Or more particularly let’s talk about the recent Australian transfer pricing case Chevron.

In a week when Inland Revenue announced a major restructure which will involve staff now needing ‘broad skill ranges’; it made me think of the type of work I used to do there – international tax.

It was true that my job needed skills other than technical ones:

- keeping your cool when being verbally attacked by the other side;

- being able to explain technical stuff to people ‘who don’t know anything about tax’ – aka anyone at Inland Revenue not in a direct tax technical function;

- ensuring the bright young ones got opportunities and didn’t get lost in the system; and

- generally ‘leveraging’ my networks to support those who were doing cutting edge stuff but not getting cut through doing things the ‘right’ way.

But otherwise what I did required a quite narrow specialised technical skill range. And that was good as it allowed me and my colleagues to focus on one particular area so we could be credible and effective. You know kinda like professional firms do?

As an aside I am not sure how this broad skill ranges thing ties in with the original business case – page 36 – which alluded to the workforce becoming more knowledge based. Coz knowledge-based work is kinda specialised not broad. But then the proposals are coming from a Commissioner who has a legal obligation to protect both the integrity of the tax system as well as the medium to long term sustainability of the department so I am sure she knows what she is doing.

Wonder what the penalties are for breaching those provisions? But I digress.

Back to me. The international tax I did though was actually quite broad compared to the work my colleagues did in transfer pricing. That was eye wateringly specialised and quite rightly so. These were the girls and boys who were on the frontline with the real multinationals like Apple, Google, Uber and the like.

And I was thinking of them recently when an appeal from an Australian transfer pricing case Chevron came out. Two wins to the Australian Commissioner and the Australian TP people – woop woo! Go them.

The guts of the case is that Chevron Australia set up a subsidiary in the US which borrowed money from third parties for – let us say – not very much and on lent it to Chevron Australia for – let us say – loads. And it was with a facility of 2.5 billion US dollars. Now you can kinda imagine the difference between not very much and loads on that was a f$cktonne of interest deductions – see why I get obsessed with interest – and therefore profit shifting from Australia to the US.

Now even though it was a subsidiary of Chevron Australia; the Australian CFC rules don’t seem to apply to the US. Coz comparatively taxed country – thank god we don’t have those rules anymore. And the judgment says it wasn’t taxed in the US either. Didn’t spell out why but I am guessing as the Australian companies are Pty ones – check the box stuff – they get grouped in the US somehow. No biggie for US but bucket loads less tax than they would otherwise pay in Australia.

And according to Chevron it was like totes legit. Coz loads is the market price for lots of really risky unsecured debt. I mean seriously dude like look up finance theory.

To which the seriously unbroad people in the Australian Tax Office said – yeah nah. Theory is like only part of it. The test is what would happen with an independent party in that situation.

- Option one – the seriously risky party ponies up with guarantees from those who aren’t seriously risky. You know how those millennials who buy houses and don’t eat smashed avocado do when their parents guarantee their loans? It is the same with big multinationals.

- Option two – banks don’t lend. So just like for all the milennials who don’t own houses but who do eat smashed avocado and don’t have rich parents.

And the Australian court thought about it all – pointed at the unbroad public servants – and said:

“What they said. Chevron you are talking b%llcocks. The arms length price is one an independent party like millennials would actually pay. This includes guarantees and you price on those facts. Not the fantasy nonsense you are spouting.”

Well broadly. Actual wording may vary. Read the judgments.

Now these are seriously useful judgments – internationally – for the whole multinationals paying their fair share thing. Let’s just hope New Zealand keeps the people who can apply them.

Andrea

Shy and retiring

Let’s talk about tax.

Or more particularly let’s talk about how retirement villages don’t pay much tax.

Your correspondent has just returned from Auckland having: topped up her CPD hours; seen old friends and talked with tax peeps. And in that short period while I was away another industry was outed as being non-taxpaying. Now it is retirement villages and they aren’t even foreign.

But don’t panic. Steven Joyce says Inland Revenue is reviewing sectors of the economy which has low tax to accounting profits. And if there is a policy problem it can be put on the policy work programme. Phew.

Now as I have 5 days to complete 3 major pieces of assessment from my yoga course I have had two months to do – the sensible thing would be to put this issue down and pick it up after I have done my assessment. Coz it is not like they about to start taxpaying anytime soon.

But the issue is really interesting.

I am sure 4 days is enough to do all that other work. And I do need breaks from all that right brained stuff. I mean isn’t yoga all about balance?

So let’s have a look at the public stuff dear readers and see if we can’t unpick why these lovely people – much like our multinational friends – aren’t major contributors to the fisc. Now I know there are a few different operators but I thought I’d have a look at Ryman. Who may or may not be representative of the rest of them.

Tax actually paid

Now their tax stuff is interesting. Accounting tax expense of $3.9 million on an accounting profit of $305 million. But accounting tax expense is a total distraction if you want to know how much tax is actually paid. Why? Different rules. Future post I think.

Next place to look – imputation account which increased by $37,000. That can be real tax but can also include imputation credits from dividends received. So close but no cigar.

And then there is the oblique reference in note 4 to their tax losses in New Zealand having increased from $2.5 million in 2015 to $17.9 million in 2016. Bingo! That looks like they made a tax loss of $15 million in 2016 when they made an accounting profit of $305 million. Nice work if you can get it.

Ok now before we get into some exciting detail let’s have a think about what these retirement villages actually do. They can provide hospital services; some provide cafeterias; and they generally keep the place maintained. But mostly they ‘sell’ lifetime rights to apartments and flats on their premises.

Forgone rent

And it is this lifetime rights/apartment thing that is – in your correspondents view – the most interesting.

Looking at Ryman’s accounts and marketing material the deal seems to be residents provide an occupancy advance and get to have undisturbed use of an apartment until they ‘leave’. On ‘departure’ the right will be ‘resold’ and the former resident gets back wot they paid less some fees.

So the retirement village gets the benefit of any capital gain on the apartment as well as the benefit of forgone interest payable on the advance. All comparable to a ‘normal’ landlord who would receive the benefit of rent and capital gain on their property.

And like a ‘normal’ landlord they don’t really know how long the resident or tenant will want to stay. It could be one day or 30 years. But economically this doesn’t matter as the longer the resident stays the less in NPV terms the retirement village has to pay back. So whether landlord gets rent or repayable occupancy advance they both give the same outcome pretax and pre accounting rules. That is with rent over a long period you get lots of rent; with interest free occupancy advances over a long period you get lots of not having to pay interest.

However this isn’t how it pans out for accounting or tax.

For accounting the advances are carried at full value because they could be called immediately – occupancy advances in section j of Significant Accounting Policies. And because of this there is no time value of money benefit ever turning up in the Profit and Loss account – or what ever it is called now. Unlike rent which would get booked to the P&L when it was earned.

And tax is equally interesting. The Ryman gig seems to be that for the occupancy advance the resident gets title under the Unit Titles Act and a first mortgage for the period they are in the property. Fabulous.

Unfortunately your correspondent is about as far away from a property lawyer as it comes. But according to my property law advisor Wikipedia; a leasehold estate is where a person holds a temporary right to occupy land. Kinda looks like what is happening here. So that would be taxable under the land provisons. And even if it isn’t taxable there – to your correspondent – it looks pretty taxable as business income.

But in either case that involves taxing the entire advance and not just the interest benefit. Seems a bit mean.

Deductions

True. But let’s look at deductions before we call meanness.

Tax deductions are allowed when expenses are incurred or legally committed to. Not when actually paid. So if you are a yoga teacher and you commit to a Tiffany Cruikshank course in Cadiz in May 2017 – she is here in Wellington ATM so exciting – paying the USD 500 deposit in April 2016 you can take a deduction for the full amount of USD 2790 in the 2016/17 tax year. Even though you don’t pay it until closer to the actual course. Tax geeks yeah I am talking about Mitsubshi.

So for our retirement village friends as they are committed to repaying the occupancy advance in the future on the day they receive it. Immediate deductibility which cancels any taxable income. Mmm.

Tbf though the tax act isn’t big on the whole time value of money thing.

Financial arrangement rules

The exception is the financial arrangement rules where embedded interest can be spread over the term of the loan. And there is even a specific determination that deals with retirement villages. Now that seems to have more bells and whistles than is obvious from Ryman’s accounts so not entirely sure it relates to them. But there is one bit that could apply as the determination does say that the repayable occupancy advance is considered to be a loan.

Except even this gives no taxable income. This is because value coming in is compared to expected value going out. And of course THEY ARE THE SAME AMOUNT! So nowt to bring in as income.

Fixing it

Fixing this gap it would involve imputing some form of interest benefit that was in lieu of rent. But what interest rate to use? What is the term? And then there is the whole thing that no one actually sees it as a lease agreement. Everyone sees it as ‘ownership’ with a guaranteed sale price back.

Also entirely possible that what I consider to be blindingly obvious; cleverer people than me may consider to be – well – wrong.

Interest deductions

Then we get to much more old school techniques interest deductions to earn capital gains. And here Ryman seems to capitalise interest into new builds – section e of Significant Accounting Policies – rather than expense it for accounting. So there will be whole bunch of interest expense that isn’t in the P&L that will be on the tax return.

Unrealised capital gains

And finally thanks to NZ IRFS 13 – really does roll off the tongue doesn’t it – their accounting profits note 7 include a bunch of revaluations on their investment properties which I am guessing is the apartments. Bugg€r with this is that even a realised capital gains tax wouldn’t touch this and doesn’t look like these guys sell. Gareth’s thing though would work a treat as all the unrealised gains are on the balance sheet.

So here we have a property business that gets interest deductions; doesn’t pay tax on its capital gains or its imputed rent. Gains go on the P&L but not the interest expense. All while being totally compliant with tax and accounting.

No wonder they are share market darlings.

Andrea

Update

Thinking about the occupancy advances some more – depending on the counterfactual – maybe the value is in the tax system already as a reduced interest deduction.

The properties need funding somehow. Usually the options are debt which generates a deductible interest payment; equity which is subject to imputation or a combination of both. Here the assets are partially funded by the interest free occupancy advance. If the residents just paid rent – the assets would then need more capital. This could be completely debt funded which would mostly offset the rental income. May even exceed it if there was an expectation of a large capital gain. So while the occupancy advance is not in the tax system; neither is the extra interest deduction.

So maybe it is all an old school interest deduction for untaxed capital gain thing. But one for which a realised CGT would be useless as they don’t sell.

May need to look at Gareth’s thing again.

Apple turnover

Let’s talk about tax.

Or more particularly let’s talk about Apple and their taxes.

Your correspondent is currently in Sydney – family stuff nothing glamorous or exciting – and had started to put together a post on Donald Trump and his 2005 tax return. Coz the Sydney Morning Herald had actually explained some stuff behind it and there were some issues that I thought – dear readers – you would find interesting.

But Saturday morning I opened my Herald app to find the latest on multinationals and tax. Apple this time. And yeah that is me. Apparently they have paid no tax in New Zealand. Whether that is 100% true only the Department would know but from looking at the accounts and how it has organised itself – looks pretty damn likely.

So how did they do? Now dear readers – you are ready for this – you know about:

So let’s go!

Tax residence

Apple appears to sell products to New Zealand through a New Zealand incorporated company called Apple Sales New Zealand. Note no Ltd at the end. It is owned by an Australian company Apple Pty Ltd.

Now normally a New Zealand incorporated company means New Zealand has full taxing rights on all its income. No need to consider whether income has a NZ source or not . If it has earned income it is taxable. Well that is unless a tax treaty would take away some of those rights. And how could that happen dear readers? Yes that’s right – if it is managed or has directors control in another country.

And is Apple Sales New Zealand (not limited) controlled offshore? Yup the directors are Australian. Ok so then not a New Zealand company for tax purposes.

Source rules

Now all the income comes from New Zealand so it should be taxed here – right? Well yeah if it has a New Zealand source. And remember that trading in v trading with thing again. Now once upon a time if you wanted to sell almost a billion dollars worth of consumer products you would kinda need to be here. But now http://www.apple.com/nz/ does the business. So thanks to the internet trading in can morph into trading with meaning bye bye income tax base.

Limits of diverted profits tax

Oh but the new things announced by Hon Judith should fix it? You know the diverted profits tax – NZ style? Well not really. The NZ diverted profits tax has some use if there really is stuff happening in New Zealand but clever things have happened to make it look like there isn’t. But here there isn’t stuff happening in NZ. Just people buying stuff from a website.

And remember how all the things a diverted profits tax would help with? Remember how trading with v trading in wasn’t one of them? Yeah this won’t save us.

Tax Avoidance

But the pretending to be a New Zealand company when it is an Australian company. That is a bit cute isn’t it and doesn’t tax avoidance stop cute stuff. Yes it does so what are the facts?

- New Zealand incorporated company

- Australian directors with Australian control

- US website

- Shipping from Australia

- GST registered

- No presence or activity in New Zealand

So taking away any clever stuff. What is actually happening?

An Australian company is selling products to New Zealand via the internet shipping from a warehouse in Australia. What is the tax consequence of this? No tax – as Apple is only trading with New Zealanders not trading in New Zealand.

Compare to current outcome – no tax. Soz nothing for tax avoidance to bite on.

Could it be fixed?

Yup.

Of course it is possible Apple will get shamed into paying tax here. Putting in New Zealand directors would do the trick. Not holding my breath though. There are also plans by the Government to strengthen our source rules – but nothing proposed tho that will bite on this issue.

What would need to happen is an extension of the ‘contracts made in New Zealand’ rule to say it is deemed to be made in the country of the purchaser for online sales.

So technically not hard.

But here’s the thing. If we do that for Apple – other countries might then do it to Fonterra; Zespri; Fisher and Paykel; Fletcher Building; and Rank when they trade without a footprint. And in this case Apple NZ seems to be paying some tax in Australia. So that will be an interesting discussion with the Australian Treasury.

And it won’t just be the nasty multinationals that get caught. Your correspondent has an extensive vintage reproduction wardrobe. All purchased online from the US and UK from relatively small companies. Risk is such suppliers would see NZ as not worth the effort and stop selling to us. But then now I live in active wear not such an issue for me.

Oh and the not limited thing? It will be a US check the box company as will the Australian Pty company meaning it is an entity hybrid and Apple Inc can choose how to treat it for tax. Cool – but don’t think it impacts on us. Phew.

Andrea

Update

Thanks to a comment below – I missed a point I really shouldn’t have.

Even if we do change our source rules every treaty we have requires there to be a permanent establishment or fixed place of business before business income can be taxed. So if our source rules were expanded to make income prima facie taxable in NZ the treaty would then allocate taxing rights to Australia.

So short of resinding our treaties – or shaming Apple into paying tax here – we have to suck it up.

There is also the issue of whether it is right to expect tax given Apple isn’t using anything that taxes have paid for. But currently that seems like an argument from another time given the public outrage.

So while taxes are inherently unilateral – this is something that has to be sorted multilaterally. Except I am not aware of any real work on it. And on that I would love to be proved wrong!

Roses by any other names

Let’s talk about tax.

Or more particularly let’s talk about the release of the recent government discussion documents on taxing the nasty multinationals.

You correspondent had spent the week before last on stage two of her yoga teacher training. No inner child this time but lots of describing poses in anatomical language. ‘The spine is flexed at the pelvis’ aka you bent over. Same lovely people though. Unfortunately my time on the course was punctuated by a day trip to Sydney – yes day trip – for a family funeral. I did however spend both legs watching a documentary on Oasis. So not entirely wasted. Also brought home number 2 son for a week’s visit.

So after all that I was seriously contemplating giving this week a pass too from posting. Coz like: ‘I am enough; I have enough; I do enough’ and other such lessons from the training. I was even looking for a cartoon to stand in its place:

Either:

Or possibly – as it is in colour:

But then Friday morning when I was working thru the details for a big family dinner for number 2 son and girlfriend – on comes the lovely Hon Judith Collins announcing the release of the discussion documents on taxing multinationals. Right. Ok. Mmm perhaps the cartoons won’t really cut it for Monday. But channelling my inner bureaucrat – where March counts as ‘early next year’ – Tuesday can count as Monday. Well broadly.

And the proposals are pretty good. Proper thin cap rules for finance companies are still missing but then a seven year time bar for transfer pricing! Whoa tiger. Even at my most revenue protective I’d never have thought of that. Lots of quite detailed techy stuff all which looks pretty effective to your correspondent.

On interest I am also pretty happy. No earning stripping rules but putting a cap on the interest rate should remove the structural flaw discussed previously and levelling the field by removing non- debt liabilities alg.

There is of course the small matter that with the House rising in July(?) and a Budget in May – there is no hope in hell it will even make a bill before this government finishes. Still no sign of any decisions on the Hybrids stuff that was released in September. And that is just as hard.

But if there is change in government this work will give Grant, Mike, James and Deborah an early taste of implementing fairness in the tax system. Coz there is nothing large well advised companies enjoy more than tax base protection. And they hardly ever lobby Ministers; harangue officials; brief journalists or turn up to select committees to advise them of the damage such tax measures will do to the New Zealand economy. So quite a good warm up for their fairness working group.

But I digress.

There are many and varied ways for non-residents to not pay tax with many and varied solutions. Most of which are in the discussion documents. But the one potential solution that gets all the airtime is the diverted profits tax. Which is a pretty narrow solution to a pretty narrow problem. But hey much like the iPhone 7 – irony intentional – even if our tax environment is different or our iPhone 5 is still fine – the UK and Australia have one so we want one too.

What is being proposed is the diverted profits tax equivalent of the iPhone SE – a 6 in a 5’s body. But when your existing phone really isn’t that bad.

And because it all gets so much media attention – this is the one techy thing I’ll take you through dear readers. But I am very sorry there is a bit of background to go through first. Kia Kaha. You can do it.

Source rules

All taxpayers – resident and non – resident – are taxed on income with a New Zealand source. Our source rules however were devised in 1910 or so. Long before the internet and possibly even before the typewriter. Tbh tho they aren’t that bad and periodically get a wee tweak. They are broadly comparable to other countries. They include all income from a business in New Zealand which can include foreign income as well as income from contracts completed here.

Case law however has narrowed this to income from trading in New Zealand rather than trading with New Zealand. So foreign importers selling stuff to punters here are out of scope but a business here – even an internet business – game on.

Permanent Establishment

The source rules are further narrowed by any double tax agreements. Here now New Zealand business income of a non-resident is only taxable in New Zealand if it is earned by a permanent establishment aka PE. And a PE is a fixed permanentish place of business. Once upon a time it would have been pretty hard to be a real business and not to have a fixed place of business. Possibly not so much now.

So if the non-resident earns business income through a fixed place in New Zealand – taxable – otherwise not. And for historic reasons the fixed place can’t include a warehouse. Coz that is like only preparatory or auxiliary to earning the income – not like the main deal. Yeah I don’t get it either.

Tax planning Apple and Google style

So when you put together the combo of no tax when:

- contracts not entered into in New Zealand;

- income earned from trading with New Zealand;

- no fixed place of business; and

- warehouse doesn’t count.

You kinda get the most widely known of the BEPS issues. The Google and Apple thing. Tbf I think they also use treaty shopping and inflated royalties but above is also in the mix.

Diverted Profits tax UK Style

Now a diverted profits tax doesn’t deal with the ‘trading with’ thing coz that is pretty entrenched and there are limits to anyone’s powers on that. And of course this would mean our exporters who ‘trade with’ other countries would become taxable there too. But it has a go with the other bits.

In the UK their diverted profits tax pretty much deals with situations as above where there is trading in a country and a permanent establishment should arise but doesn’t. The way it works is to say : ‘oh you know the income that would have been taxable if you hadn’t done stuff to not make it taxable – well now it is taxable.’ ‘Oh and it is like taxable at a much higher rate than normal – coz like we don’t like you doing that.’

And now New Zealand

Now in New Zealand that kind of I know you have followed the letter of the law – but dude – seriously is countered by the tax avoidance provisions. And much to the chagrin of the Foreign banks; specialist doctors; and Australian owned companies it does actually work in New Zealand.

And just because the tax avoidance provisions are being successfully applied doesn’t mean that the law shoudn’t be changed. It is a bucket load of work to investigate; dispute and then prosecute successfully. And if there are lots of cases – and there do appear to be – law changes are ultimately less resource intensive.

But even given all that I am somewhat surprised that what they have proposed is very similar to the handwavy tests of the UK. A bunch of clear questions of the structure and then asks if ‘the arrangement defeats the purpose of the DTA’s PE tests.’ Ok. Not a million miles from the parliamentary contemplation test with tax avoidance. So not entirely sure what extra protection it gives us other than being a bright shiny tax thing.

But then how different was the iPhone 6 from the iPhone 5 after all? And while the iPhone 7 is newer and flasher is it actually better?

Who knows though maybe New Zealand’s version of a diverted profits tax has a signalling benefit to the Courts. And its not like it will do any harm. So long as you don’t count additional complexity as harmful.

So all in all not bad. With the earlier Hybrids and NRWT on interest – even if the diverted profits tax equivalent may not add much – all the rest of the proposals should deal to undertaxation of non- residents.

And now residents what about them – capital gains tax anyone?

Andrea

The company in residence

Let’s talk about tax.

Or more particularly let’s talk about tax residence for companies and trusts.

Following Mr Thiel’s post a reader asked about the non- resident purchaser stats that LINZ produces. And so I wrote a post on that. I really did. But as I was going through it it became clear to me that the LINZ stuff was actually super hard. Even for you dear readers. And – given I hadn’t taken yet taken you through the joys of tax residence for companies – super hard was actually super impossible.

So dear readers today you get company residence. And hang in there coz next week you get a discussion of the LINZ data where I try to clear the smoke and mirrors that is those stats. But that is next week. So back to tax residence and companies.

Ok now companies have separate legal personalities and so they can contract and do stuff independent of its shareholders. And the total wheeze is that if the company fails shareholders are not liable for its debts if their capital is fully paid. They do lose the dosh they put in as capital and of course if that was spent on deductible expenses and it is a closely held company those losses can be offset against other taxable income. But you know that already so you won’t get any more on that from me today.

So back to residence. As a company is its ‘own person’ the concepts of prescence or connections with New Zealand used for actual people make no sense with them. They need their own bespoke tests. And in New Zealand they are:

- Incorporation

- Head Office

- Directors control

- High level management

If anyone of those is in New Zealand then game on – New Zealand resident – taxable on worldwide income. Or at least before a treaty comes in.

But looking at that list and thinking about how often in tax policy the statement ‘a company is a vehicle for its shareholders’ is used. What is not on that list?

Well done – shareholding. A company could have 100% foreign shareholders – hit one or all of those tests and still be prima facie taxable on its worldwide income in New Zealand. The opposite also applies. A company could have 100% New Zealand shareholders and meet none of those tests. It then would be non-resident and so not taxable on its worldwide income. Now because that is just too cute there are other – controlled foreign company – rules that then come in. But they are for another day.

So key message – residence does not equal shareholding or beneficial ownership. Now in practice there will be significant overlap coz NZ companies are really for NZ resident shareholders. But won’t be a complete set.

And joy of joys other countries have similar tests:

Australia – incorporation or directors control

Canada – Incorporation or directors control

China – incorporation or place of effective management

UK – incorporation or place of effective management

US – incorporation

And yes dear readers – you’ve got it – two countries could claim a company. A NZ incorporated company with effective management offshore in UK or China or Australia or Canada could be claimed by those countries too. Similarly an Australian incorporated company with NZ high level management will get claimed by both Australia and New Zealand.

And then – as with Mr Thiel – the treaty will decide who gets the rose. With companies the test in the treaty is usually the place where the high level decisions aka place of effective management is. So as with Mr Thiel there is domestic law tax residence and residence for the purpose of a treaty. And the music finally stops with the treaty.

Ok well done. Now that wasn’t too hard. Now let’s try trusts. In a trust is a settlor that puts in stuff; a trustee that legally owns the stuff and manages it on behalf of the beneficiaries.

For those of you who followed the foreign trusts thing you may have heard something like ‘ NZ has a settlor based system for taxing trusts’. Now that is almost right. New Zealand has a settlor based system for the taxation of distributions. The residence of the trustee, however, is the starting point for the taxation of trusts.

And the tax residence of the trustee is the tax residence of the company or individual that is the trustee. So again the residence of the trustee could be completely different from the residence of the settlor or the residence of the beneficiaries.

Now why I am labouring this potential disconnect will make more sense next week. Feel free to pre read the LINZ reports in the first link.

Andrea

Being there

Let’s talk about tax.

Or more particularly let’s talk about tax residence.

There is currently is a big to do about Peter Thiel both here and in the foreign press about exactly how did a US billionaire become a New Zealand citizen. Soz can’t help with that. But on my Facebook feed this morning is coming the question – so is this guy tax resident? Now that I can do off the public stuff and is pretty much probs yeah/nah. But citizenship – scmitzerzenship – really not relevant much at all.

There are many concepts of residence used in the bureaucracy. The main one is permanent residence – an immigration concept – which pretty much gives the recipient the rights of a citizen except maybe you can’t stand for Parliament.

Tax residence however – who would have thought – is a completely different concept. While in practice most New Zealand permanent residents and citizens will be tax residents. It is by no means a dead cert.

Now why tax residence matters is that residents are taxed on any foreign income earned and fully taxed on New Zealand income. Tax non-residents are not taxed on foreign income and have concessionary rules on how New Zealand income is taxed. Think Google.

For an individual there are two ways – you can become tax resident and a number of ways you effectively lose it.

The two ways are:

- Being here – an individual who is physically in New Zealand for 6 months in ANY 12 month period becomes New Zealand tax resident.

- Connections to New Zealand – even if you are here less than 6 months in any twelve month period if you have a house you live or have lived in while you are here AND you have other connections you will become subject to tax in New Zealand on your foreign income.

So looking at Mr Thiel. According to reports the dude has two houses in New Zealand. Combined with his New Zealand citizenship and the stuff wot he did to demonstrate commitment to NZ – not free from doubt but – I would say there was a pretty high chance he would hit the connections to New Zealand test. And yes tax friends I am talking about a permanent place of abode but there are non tax people who read this and we’d all agree as terms go it is not the most intuitive.

Now you might be thinking dear readers – woohoo – New Zealand can tax his foreign income. Hello mega surplus and Scandinavian levels of public services.

Ah but not so fast there is now the small matter of the US/NZ tax treaty.

On the basis that he is a ‘naturalised American’ he is also tax resident of the US and they will also claim taxing rights on his foreign income. And here the treaty will sort that out:

- First question is which is the country where he has a home available to him? Ah probs both. Next question.

- Second question which country is where his personal and economic ties are stronger? Mmm tough. A late forties ‘naturalised American’ with business interests there and a confidante of the President v really likes NZ and invests in tech companies. Tricky but I think we can call it for the US.

Now is this tax dodging or tax avoidance? Should we feel aggrieved as New Zealanders that he is a citizen but unlikely to be a tax resident?

Me nope.

I defo don’t think this is tax dodging or tax avoidance as there is nothing cute or clever or structured in being taxed where your stuff is and where your links are stronger. Given the NZ diaspora who are NZ citizens – not all of them will be residents under the two tests and even if they are they will also have the benefit of their treaty. And in theory anyway he should be paying tax on his foreign income in the US.

But I can only hope that when the ‘exceptional circumstances’ were being weighed in Mr Thiel’s application the Minister knew that while we were getting a citizen – given how international tax works – it was unlikely we were getting a taxpayer.

Andrea