Goodbye again

Hello everyone

I realise I just disappeared on here so I thought I’d update you on my new whereabouts and then sign out.

I am currently the Policy Director and Economist for the NZ Council of Trade Unions. So blogging is off the agenda for the foreseeable future.

However I am still writing about things and publish a monthly economic bulletin. To date I have published one in January and February for the CTU. It comes out on the last day of the month.

I have published a tax piece for interest.co.nz, been interviewed by the NBR and was on the telly on Q and A.

I still have lots of reckons. Some of which include tax and can be found on Twitter @andreataxyoga and LinkedIn https://www.linkedin.com/in/andrea-black-0b2490123/

But for anyone who would like to obtain an emailed version of my monthly views for the CTU – options include:

1) Leave your email address in the comments section. I am moderating all comments so it won’t be public or

2) Email me on andreab@nzctu.org.nz.

Either way I’ll add you to the distribution list.

But you’ve been a great audience and I have appreciated all the engagement. It has all been such a pleasure.

Kia kaha

Andrea

Guest Writing

Hello lovely readers.

After almost three years of this blog being a solo gig I am now trying something a bit different.

Following the example of Mick Jagger and why he performs with super talented back up singers:

‘Otherwise it would be a bit boring – it would just be me, me, me and a bit of Keith’. (1)

I have decided to open the blog up to guest writing. Well one writer at the moment. I have approached another but she hasn’t got back to me. You know who you are!

As of tomorrow Guest Writer number 1 is Alison Pavlovich. Alison teaches tax at Massey as did the OG of progressive tax thought Deborah Russell. Alison used to be important in the UK and now – for reasons that are beyond me – is doing a PhD.

More importantly she is cool, has views and agreed to a cameo appearance. So – dear readers – give her lots of clicks to make her feel loved and maybe she’ll come back.

If these tentative steps prove successful, I’d like to open the blog up more widely to viewpoints and authors that wouldn’t normally be heard. An ability to write and not take it all too seriously will be key. I would also be open to anonymous or pseudonym writing in particular cases. Tax knowledge is a given.

Yes that is all code – work with it.

As for me – I’ll still be here – doing my thing as often as I have to date. But now – I hope – you also get to hear other voices.

Hope you enjoy it.

Andrea

(1) This comes from one of my truly favourite films in the whole entire world 20 Feet from Stardom. It is on Netflix. Team watch it now!

Sparking Joy

Hello. How’s it going?

Thought I’d come back for a wee while.

Am currently on my hols. Tax Working Group gig appears to be over and have – I hope – put in my last bill. Contract got extended to June for any residual stuff but as there isn’t any residual stuff – I have effectively tagged out.

Have various ideas about what next but have decided for the next [insert time period here] I would Marie Kondo my energy.

And what is it that sparks joy in the life of your correspondent? International Tax and learning French.

No really.

The latter I haven’t done since 2016 and the former not since issues like ‘death as a rollover event’ dominated my tax brain.

And because I am a deeply relational individual you can all come with me. For international tax that is. French, probs, will be a more private pursuit.

So the blog is reopening for une période indéterminée.

The plan is mostly international tax but you might get other stuff.

Tax Working Group stuff is unlikely – see reference to contract – although there are some cinderella bits like Charities or the Tax Advocate or the Crown debt agency that have got lost in the CGT noise I might discuss further.

What you won’t get dear readers any more is the cartoons. At times sourcing those took as much time as writing the fricken blog post. Not a joy spark and so out.

And comments will still be moderated. Soz.

But otherwise. I’m back.

Andrea

The last post

Well dear readers this is it. Our time together is coming to an end. I now have a grown up job.

Sir Michael Cullen has asked me to become the independent advisor on the Tax Working Group. And I have accepted.

Through a combination of no longer having the time and not really feeling comfortable publicly commenting on stuff that may also be under review; I am closing the blog for the duration. I will still pay the princely sum of USD 30 or so to WordPress to keep it all in existence. But new stuff – soz.

I have really enjoyed the opportunity to write as I would like and not as a policy official or a disputant. I have also enjoyed all the new people I have met as well as the polite and intelligent- albeit limited- engagement on the blog itself. But I get to be a grownup again which I am looking forward to. Even if that does mean womens work shoes and writing in complete sentences.

Looking into my future compliance, I am very pleasantly surprised with the new tax landscape for contractors. GST registration and filing can be done online. Even registration for ACC seems to be automatic with GST registration. And provisional tax largely avoided through withholding taxes if the payer agrees. Which I am hoping the Treasury will. The tax system has clearly benefited from my absence.

I do still have some partially written posts that I never finalised. Including alternative minimum taxes and GST on online shopping. Even had a cartoon ready for the latter.

But what I can do is encourage you all to engage with the Working Group processes particularly if you aren’t a tax person. The tax system belongs to us all. As independent advisor I will have a role – if they want – in helping community groups and NGOs frame their submissions. So they are able to fully engage with a system that can – at times – seem oblique and arcane. Even after reading the blog.

So I hope I am able to engage with a number of you through the Working Group processes. But otherwise I would like to thank you all for your attention and wish you a very Happy Christmas – no recipes this year – and New Year. In the immortal words of Douglas Adams:

So long, and thanks for all the fish.

Andrea

My fair tax review

So the details of this government’s tax review is out.

Depending on who you read it will either be revolutionary or not radical.

Now even though this blog has come as a response to the Left’s – and fairness’s – relatively recent introduction into the tax debate – I couldn’t see anything I could competently add to the random number generator that is the current public discussion. That was until I read one commentator – who actually understands tax – talk about the last Labour government’s tax review – the McLeod Report.

He referred to that report as having analysis that stood up 16 years later. And with the underlying analysis found in the issues report I would wholeheartedly agree. But in terms of the recommendations in the final report I would say, however, that it was very much of its time.

And by that I mean that while the issues report fully discussed all issues of fairness/equity as well as efficiency – when it came to the final report efficiency was clearly queen.

Now by efficiency I am meaning ‘limiting the effects tax has on economic behaviour’. And fairness as meaning all additions to wealth – aka income – are treated the same way.

The tax review kicked off in 2000 at about the same time I arrived at Inland Revenue Policy. In early 2000 there was:

- No working for families

- No Kiwisaver

- Top personal tax rate was about to increase to 39% but with no change to company or trust tax rate

- Interest was about to come off student loans while people studied.

That is the settings generally were the ones that had come from the Roger Douglas Ruth Richardson years.

Also in tax land the Commissioner was having a seriously hard time as the Courts were taking a very legalistic attitude to tax structuring. High water mark was a major loss in 2001. And unsurprisingly in such an environment the banks had started structuring out of the tax base. But it would be a while before that became obvious.

Housing was affordable. Families such as mine could be supported on one senior analyst salary – and live walking distance to town.

The tax review was headed by a leading practitioner Rob McLeod; and had two economists, a tax lawyer and a small business accountant. One woman. Because that is what progressive looked like 2000.

And so what were their recommendations/suggestions?

No capital gains tax but an imputed taxable return on capital This one is both efficient and fair. And did materialise in some form with the Fair Dividend rate changes to small offshore investment. It is the basis of TOP tax proposal. At the issues paper stage it was proposed to include imputed rents but the public (over) reaction caused it to be dropped. Interestingly it is explicitly out of scope with the Cullen review.

Flow through tax treatment for closely held businesses and separate tax treatment for large business

What this is about is saying entities that are really just extensions of the individuals concerned should be taxed like individuals not the entity chosen. This is effectively the basis of the Look Through Company rules – although they are optional. It means the top tax rate will always be paid. But it also means that capital gains and losses can be accessed immediately.

Now this is definitely efficient as the tax treatment will not be dependent on the entity chosen. And it is also arguably fair for the same reason.

It does mean though that if a company structure is chosen and the business gets into trouble: the tax losses can be accessed as it is effectively the loss of the shareholder but the creditors not paid because it is a separate legal entity. Which probably wouldn’t exactly feel fair to any creditor.

But all this is unreconciled public policy rather than the McLeod report.

Personal tax scale to be 18% up to $29,500 and 33% thereafter.

The tax scale at the time ranged from 9.5% to 39% at $60,000. The proposal would have had the effect of increasing the incentive to earn income over $60,000 as so would have been more efficient than the then 39% tax rate. As the company and trust rate were also 33% it would have returned the tax nirvana where the structure didn’t matter.

However it would have increased taxes on lower incomes and decreased taxes on higher incomes. So while efficient – not actually fair according to the vibe of the Cullen review terms of reference.

New migrants seven years tax free on foreign income

At this time our small foreign investment – aka foreign investment fund – rules were quite different to other countries. While we didn’t have a realised capital gains tax – for portfolio foreign investment we could have an accrued capital gains tax in some situations. This was considered off putting to potential high skilled high wealth migrants. So to stop tax preventing migration that would otherwise happen; the review proposed such migrants get seven years tax free on foreign income.

This proposal was the other one that was enacted with a four year tax free window – transitional migrants rules.

And again a policy that is efficient but arguably not fair. As the foreign income of New Zealanders in subject to full tax. However Australia and the United Kingdom also have these rules that New Zealanders can access.

The logical consequence though is that no one with capital lives in their countries of birth anymore. And not sure that is ultimately efficient.

New foreign investment to have company tax rate of 18%

Again this is the foreign investment – good – argument. But it ultimately comes from a place where foreign capital doesn’t pay tax because it is from a pension fund, sovereign wealth fund or charity. Or if it is tax paying that tax paid in New Zealand doesnt provide any form of benefit in its home or residence country. So by reducing the tax rate by definition this reduces the effect of tax on decision making.

However doesn’t factor in the loss of revenue if there are location specific rentswhich aren’tsensitive to tax. And not exactly fair that domestic capital pays tax at almost twice the tax rate. Unsurprisingly didn’t go ahead.

Tax to be capped at $1 million for individuals

This again comes from the place of removing a tax disincentive from investing and earning income. Yeah not fair and also didn’t go ahead.

Restricting borrowing costs against exempt foreign income

This was the basis of the banks tax avoidance schemes that ended up costing $2 billion. It is only briefly mentioned in the final report with no submissions. It is to the review team’s – probably most likely Rob McLeod – credit that it is there at all. This proposal was both efficient and fair. Stopping the incentive to earn foreign income as well as making sure tax was paid on New Zealand income.

It will be very interesting to see where this review comes out with the balance between efficiency and fairness. Because both matter. Without fairness we don’t get voluntary compliance and without efficiency we get misallocated capital and an underperforming economy. But the public reaction to the taxation of multinationals and ‘property speculators’ would indicate a bit more fairness is needed to preserve voluntary compliance.

And as indicated 16 years ago – taxation of capital is a good place to start.

Andrea

Right From The Start

Let’s talk about tax.

Or more particularly let’s continue to talk about the IRD restructure.

There are so many things I would rather talk about: how charities don’t have to distribute; exactly what was Roger Douglas going on about; and Labour Party’s family package.

But last week’s post was really a rant. And I don’t like ranting. So I thought this week I’d take a more considered look. In large part to work through how exactly had I got Business Transformation just so wrong?

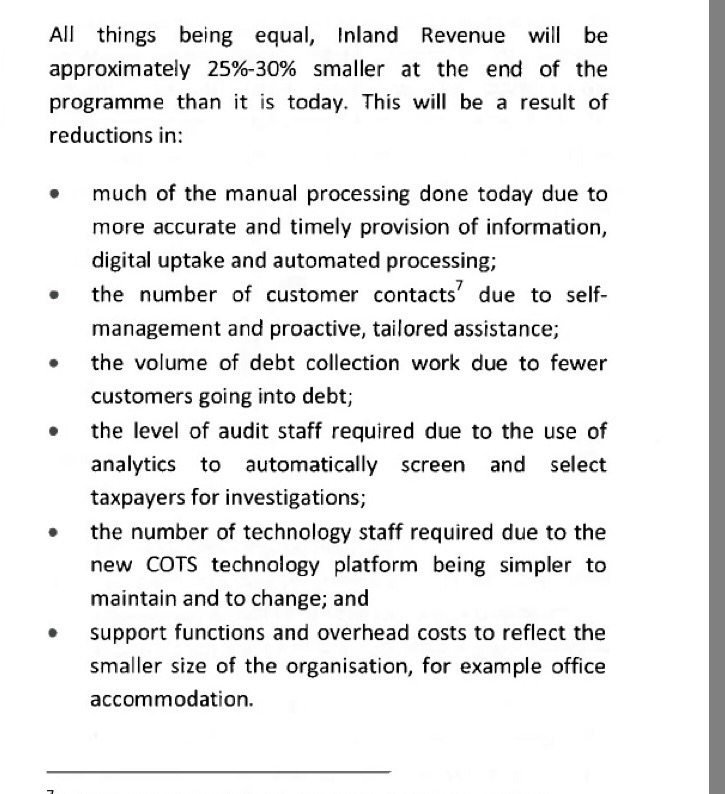

The Business Case signed off by Cabinet was a reasonable place to start. Except didn’t that simply say in the brave new world there would be fewer errors, less manual processing, and fewer IT staff? And aren’t these customer facing people the ones being confirmed in their jobs?

And yes it did talk about a reduction in audit staff because there would be better screening. But that always seemed reasonable. Less low end work consistent with a more knowledge based department.

But then I had a look at what actually said:

Now with the dot point on audit staff, I had thought that level was simply a synonym for number or volume. You know – the words that had been used in the other dot points. Using level makes the language less repetitive as any good editor will do.

But looking and thinking again – level is also a synonym for grade or capability. And this is exactly what is happening. A reduction in the pay bands of the senior people is due to a reduction in the capability required across the audit cohort.

HR 101.

So right from the start – the information was always there. Hiding in plain sight. Just as well I am no longer employed for my ability to do detail.

One thing though that is very clear in the restructure is just how important data analytics people will be in the department. So important that in the specialist group only about a quarter of the positions are for tax technical people. So important that it appears the additional technical people referred to in the Commissioner’s press statement are data intelligence people.

Ok. Fair enough. But while these people and the flash new computer could be very helpful in identifying issues; resolving them – not so much.

So why is the department tilting its focus in this way? Over the last week I have been (over) thinking about this and this is what I have come up with. It’s not great but it is the best I can do.

Everything is ok – and if it’s not – service will fix it

When I rejoined the department in 2015 there was a theme of Right from the Start. This came from OECD work in 2012 of the same name. The gig was simply – for small and medium businesses – it is better for revenue authorities to help them get it right from the start rather than audit non or poor compliance. In large part – stating the flaming obvious but it was a good way to think about allocating resources. I was – and still am – very supportive of this approach.

From time to time I would hear that RFTS could ultimately mean – no audits – for anybody large or small. But as that was just silly I didn’t pay much attention to it. The OECD work after all was all about small businesses for whom the tax law can get a bit overwhelming. It didn’t apply to the types of big business that actively structure into the tax law.

Or so I thought until last December when the Large Enterprises Update came out using RFTS language. Largely harmless I thought and mostly a rebadging of the long standing direct compliance work undertaken by Senior Investigators in the Large Enterprises section. I then clicked through to the Multinationals Compliance Document. Again largely a standard breakdown of the issues worked on by the section.

What did catch my eye was the foreword from the Commissioner. In it she said:

The 600 largest taxpayer groups, whose tax affairs we review every year, contribute more than $6 billion tax to NZ annually.

But this is no time to rest on our laurels. Internationally there are serious challenges in collecting tax from multinationals. New Zealand needs to play our part in addressing that. And while I am confident that most are paying the tax they should in New Zealand, the public appears less convinced. We each need to conduct ourselves in a way to correct that misperception.

Mmm $6 billion. Possibly includes a large slice of PAYE and GST which is more collected than contributed. But I digress.

Oh right. So everything is ok. Good to know.

Not exactly sure why then there are at least three discussion documents on the problems with international taxation. And even with all that the Leader of the Opposition is writing to companies telling them to get their tax act together.

Of course who were the people that uncovered the issues in the first place? Yes you guessed it. The audit staff whose level is being reduced.

But the computer is like really smart

Now the other thing I haven’t really factored in is just how useful a super smart computer will be for finding risks and doing stuff. And maybe if the lawyers aren’t messed around too much, maybe they with the lower level Investigators – or Customer Compliance Specialists as they will become – can do the job. Particularly if the computer is like totally wicked.

Maybe.

But computers can’t work without material. And what they currently have for large business is the Basic Compliance package which includes financial statements. This is cool but financial accounts are prepared for their shareholders and it is all about communicating information to them. One company’s accounts can follow a different format and structure to another company.

So some person at IRD will still need to do something to turn this into comparable information.

In all the BT stuff that has come out – I haven’t seen anything that requires/mandates business information to be provided in a particular format. And in terms of public stuff remember now even Facebook doesn’t have to file accounts. So for big companies IRD has the most information. And that is currently financial accounts following a non-standard format.

But maybe – you know – machine learning or Artificial Intelligence can sort this out. HMRC is apparently getting into it. In areas that include case work – ‘to enhance decision making’. Great. Good to know.

A tax accountant, however, commenting in that article is less convinced. Because facts and circumstances.

But then dear readers – much like this tax accountant – let’s just hope it is her lack of imagination. And it is all part of a well thought out plan. Fingers crossed.

Andrea

Nothing much at stake

I try to have a policy of not writing when I am angry. And I am currently red hot angry.

I also try to write in a way which joins dots with public stuff so that bigger more powerful people – which is pretty much everyone – can’t have a go. So that was the approach I took when I last wrote about the IRD restructure. And at that stage it was a proposal with staff consultation.

Included in the proposal was that the job I previously did and those of the transfer pricing specialists would be disestablished. There were similar jobs that could be applied for – but with up to 30% pay cuts. Now yeah we weren’t badly paid in #IamMetiria terms. But given we were the technical leaders for most of the big cases in the last decade and compared to the people we were up against – the taxpayer got serious value for money. Same for the senior lawyers we worked with and the senior investigators. Their jobs also either disestablished or reconfigured for much less money.

But now it is finalised. And pretty much as bad as proposed.

Now everyone has ‘equalisation clauses’ in their contracts. This means that if a job with a lower salary is taken following a restructure a payment equal to the difference in salary for two years is made. The structure of this also means they can leave the month after the payment is made and be better off. Great for them. For the taxpayer – not so much.

All because why? Because Business Transformation. What? A new computer system? Seriously a new computer means kicking or managing out the people who have delivered the returns over the last ten plus years?

All in a week where Oxfam outed Reckitt for a restructure involving profit stripping. One which looking at their accounts seems to be a transfer pricing wheeze. The same week where the Greens announced a higher top rate with no mention of the trust rate. No need for any high end tax enforcement there.

So where is the oversight of this? Is this so operational that Ministers aren’t concerned? Will they be concerned if any new BEPS rules become irrelevant as the capability to enforce them won’t be there? Or is it simply my lack of imagination? The new computer will be so flash it will be able to review accounts; conduct interviews; and analyse several countries tax laws. Digital disruption indeed.

What I do know is that my former colleagues will be just fine. They may have a truly shite period coming up. But they are all talented resourceful individuals. Whether they are still at the department in a year – is another thing entirely.

So that new computer really has to be something. Because whether it is tax cuts or increased public spending – the money needs to keep coming in.

Andrea

I am into champagne

Let’s (not) talk about tax.

Let’s talk about yoga stuff.

As part of her assessment for yoga teacher training your correspondent has had to read B K S Iyengar’s Light on Life and write 500 words on something that ‘spoke to me’. As 500 words is blog length and we have now all handed in our essays I thought I’d post it as a bit of ‘light’ relief after all the tax stuff.

Think of it – dear readers – as the blog equivalent of alternate nostril breathing which is supposed to balance out the hemispheres of your brain. Although that exercise after a couple of rounds doesn’t so much balance out your left brained correspondent as make her want to run screaming from the room. So like all yoga; work with your comfort levels and rest or stop when you need to. Listen to your body.

But first a bit of background. Yoga is not actually what non-yogis think it is. Non-yogis think of it in terms of contortionist poses – that they are like far too stiff or inflexible to do. And this isn’t helped by the whole instayogi thing. Beautiful fit young people doing postures average people can’t do on beaches or tropical islands that average people can’t afford to go to.

There are 8 limbs of yoga: the postures or asanas are but one of them. And that not to under rate them. As an ex runner I would say: come for the flexibility; stay for the brain calming and inner peace.

I had hoped to work in the ideas of Marianne Elliott social activist and yoga teacher. In particular her framework for progressive social change which I have paraphrased (and adjusted slightly) as involving:

- The official rules laws and structures we live by;

- How we treat each other; and

- How we treat ourselves.

And it is in the latter that yoga is referenced. But the essay I have to write is very short and I didn’t start soon enough to do a decent job with both Marianne’s and Iyengar’s ideas. For people who are interested in this combination I would suggest reading direct from Marianne’s work and skipping the rest of this post.

And yes this will be the last non-tax post for a while. Yes it is a tax blog and I will return to tax stuff in a couple of weeks after my teacher training is over.

Andrea

“We have been asked to read Iyengar’s Light on Life and write about what spoke to us. It is fair to say that yoga has changed my life. But not in a way that is particularly obvious from the outside.

My family has REALLY BAD GENES meaning living as long as I would like may not be possible. So I have organised my life to ‘do something different’ when I turned 50. That ‘something different’ broadly is working for progressive social change.

So this was in my head reading Light of Life. To be fair while I struggled with the book; there were a few things that really did resonate with me:

Role of asana

Iyengar says that asana is the physical process that relaxes the mind which in turn allows pranayama – breathing – to unlock the prana – energy – blockages in the body. Which in turn calms and focuses the mind.(Page 14)

This is absolutely my experience. In the time leading up to my fiftieth birthday I had many competing ideas and emotions. Normally would rush to decisions that may or may not be the right ones for me and those around me.

Now it was my physical yoga practice that I kept coming back to. It might have sorted out my posture but more importantly it kept my mind clear and proceeding with calmness and focus.

I am a little nervous though of his concept of right pain as a tool for growth (page 49). As what I had thought to be ‘right pain’ in chaturanga has lead to a shoulder I am still trying to fix a year later.

Asteya and Aparigahaha

Non-stealing and non-covetousness like non-violence ahimsa, are tenets that are blindingly obvious ones for any philosophy. Iyengar, however, takes them further than I have seen before.

Non-stealing includes not taking more than you need. When combined with non-covetousness this means that taking more than you need could mean deprivation for others. And to Iyengar wealth being tied up in a few hands is also theft or covetousness.

To be faithful to these yamas wealth – as energy – must circulate otherwise ‘it will stagnate and poison us’. ‘Energy needs to flow or its source withers.’ (Page 245) This particularly resonated with me given according to Oxfam 8 men have as much wealth as half the world.

What I am increasingly seeing in New Zealand – through our out-of-whack property market – is wealth being captured through those that own property from those that don’t. And so by capturing all the wealth we are poisoning our children’s potential to live the lives we have lead.

But here’s the thing. Those who have the most won’t let that happen to their children. So opportunity and material comfort will only be available to the children of families that already have it. The exact social ill that families such as mine were escaping 100 years ago by coming to New Zealand.

So although Iyengar’s primary message was of one of inner freedom – embedded in that was the other eternal truth – that the personal is political.”

Much ado

Let’s talk about tax.

Or more particularly let’s talk about non-residents buying property in New Zealand.

Your correspondent has never understood the expression the devil is in the detail. Coz as someone who has spent her career in detail – I have always found the truth or the clarity to be in the detail. Because surely it is only from the detail that the high level stuff can come? Otherwise how do you trust that the principles or concepts are right?

All of this came back to me – as I mentioned last week – when a reader asked about the non- resident stats on property purchases. And how they kinda get touted as being both evidence and not evidence of low levels of foreign ownership in New Zealand.

As it all just very confused with claim and counterclaim – it is worth starting at the beginning. And in the beginning was Budget 2015. The government wanted a demand side measure or measures to help cool the housing market aka something to reduce the number or value of buyers in the market. And yeah that is me in the early stuff.

Where they landed was a combination of the:

So the people who have to provide NZ IRD numbers are all companies, trusts and partnerships as well as individuals who have limited connections to New Zealand or are not selling a main home. So pretty much everyone except anyone who can vote and is selling their family home. This meant IRD could track buying and selling of property better and stand a better chance of enforcing the Brightline test as well as the intention test.

And the people who had to supply foreign IRD numbers were anyone – individual or entity – who a foreign country had claimed under their tax residence rules. And it was tax residence before any treaty would apply too so these people could also be tax resident in New Zealand. Think Mr Thiel. This meant IRD could let foreign tax authorities know what their tax residents were doing here . And if the foreign country had a capital gains tax – very likely – they might be interested in this information.

Now let’s have a look at the LINZ pie chart. This chart is simply a summary of those who gave foreign IRD numbers and those who didn’t. So what can it tell us about the level of ‘foreigners’ buying residential property? Well actually absolutely nothing. Coz in the 3% this could include:

- A New Zealand incorporated company with New Zealand shareholders but with directors control in either Australia, China, Canada or the UK. Coz remember from last week how shareholding was irrelevant for residence?;

- A company incorporated offshore with New Zealand shareholders but with high level control in New Zealand;

- An American citizen who lives here all the time buying an investment property;

- A trust with any of the above as a trustee.

Now in practice some scenarios are more likely than not. But the key point is that even tho 3% is small it could also include buyers – as above – that don’t exactly feel foreign.

And in the 60% green – NZ tax resident only – the reverse becomes even more pronounced. This group can include a:

- company incorporated in New Zealand with high level control in New Zealand but offshore shareholders;

- trust with a New Zealand resident company or individual as a trustee but offshore settlor and beneficiaries aka our friends the foreign trusts;

- foreign citizen on a working or student visa in New Zealand for more than 6 months.

And all of this makes complete sense when the objective is helping treaty partners enforce their tax laws. As where there is no tax claim on the individual or entity by a foreign country there is no need for a foreign IRD number. But to consider this group ‘not foreign’ – bit of a stretch really.

Now the really interesting thing tho in all this stuff is there is a defintion in the mix that is a reasonable approximation of ‘foreign’. That is the term ‘offshore person’ (pg 15). It is used for the NZ IRD number requirement and as a carve out from the main home exclusion.

In offshore person there are no tax concepts and comes pretty close to what intuitively would be considered a ‘foreigner’ or a NZ citizen with limited ties to New Zealand. For individuals an offshore person includes non-citizens; citizens who haven’t been here in 3 years or permanent residents who have been absent for a year. For companies, partnerships and trusts it is where the 25% of the beneficial ownership is by these individuals who have these limited ties to New Zealand. Peter Thiel may be an offshore person given how little he seems to be here.

So if you actually wanted a proper foreign register of buyers of residental property or wanted to assess the level of foreign ownership in NZ – that offshore person definition really isn’t bad. It would need work if you started banning these sales as it does include actual NZ citizens and the company/trust foreign threshold is a 25% ownership which is kinda low. But still a lot better than anything based on tax residence.

So is that question asked anywhere? Nah. Facepalm. I guess coz like they really really don’t want a foreign buyer register.

But if you think it through – all the Budget 2015 things were really actually only about tax. And with LINZ being the easiest place to collect the data. So it makes complete sense that this stuff is administered by LINZ – joined up government and all that.

But what doesn’t make sense is why poor old LINZ has to produce these reports. Because honestly why does anyone care what percentage of land sales might be exchanged with a foreign tax authority? Even your correspondent the international tax geek – as the Americans would say – could care less.

But though much like the:

- Bright Line test which is the infrastructure for a capital gains tax;

The offshore person’s test could be the basis of a register of foreign buyers. Thereby continuing this government’s kind provision of the springboard for the next lefty government’s policies. And who says John Key doesn’t have a legacy?

But first LINZ would have to start collecting that information.

Andrea

PS This is the last post for the next two weeks. I have part 2 of my yoga teacher training coming up. Namaste.

The Christmas Post

Let’s (not) talk about tax.

Let’s talk about a couple of Christmas related things.

Christmas thing one – Holy Innocents Day.

Many many years ago when I was a late teenager and a Christian I went to church with my father on the Sunday after Christmas. Taking the service was one Canon John Froud. The Canon. A retired priest who took the unglamorous – 8am – or the respite services after the major festivals for the main priest.

The Canon also looked after the Servers of which I was one. Main advice for us was – particularly if something went wrong – ‘whatever you do – do it slowly’. Could be a yoga motto. He loved us young people in a fairly direct unsentimental way – all completely appropriately so sad I have to say this – and had time for us in the way the main priest who had a parish to run couldn’t possibly.

He did however like things done properly and the crewcut may have reflected a military background at one time. I still have a memory of turning up for serving duty at the 8am service – what I thought was on time and correctly presented. No idea what time I had got to bed tho. But before entering the church I was told ‘Open your eyes Andrea – they are at half mast.’ I duly opened my eyes.

Now on the Sunday after Christmas, the Canon as he was leading the service gave the sermon. And the topic he chose was Holy Innocents Day. As apparently that is the Sunday after Xmas in the Anglican calendar. What he said has stuck with me to today. And I can’t think of many other things that have had a similar impact.

Holy Innocents Day is to honour all the baby boys that were slaughtered on the orders of Herod when he heard of the birth of the King of the Jews. Now in the mid eighties there was no Wikipedia link to challenge the veracity of the Canon’s sermon. But to me it seems quite likely given what a nasty bugger Herod was – better to be his pig than his son – and would explain the whole going to Egypt thing.

At this point I could start to reference ‘trade-offs’; or make yin/yang or omelette analogies. But I won’t. All I wish to do is note that even with a festival as joyous as Christmas – there is another side that should be remembered. As that was what the Canon wanted us to do.

Christmas thing two – Pavlova

Changing the subject completely. Because dear readers you have all been so fabulous – I am going to give you my pavlova recipe. I make an absolutely state of the art top draw pavlova. And you can now too.

Background

This recipe comes from my grandmother and the proportions are one egg white to 2 ounces of caster sugar. Yes ounces soz. I have a jug that measures sugar in ounces. I don’t think it is too critical though as I have used less than that in the past and it all worked fine. I have also used this recipe for 4 egg whites and 16 and the proportions still work. I use – broadly – one egg white to one person. But then I have been feeding teenage boys up until now.

Also – key message- it needs to be made the night before.

Recipe

- Turn oven to 200 degrees Celsius. Line a tray – or even roasting dish if a big pav – with cooking paper.

- Get out cornflour and a vinegar like white or red wine. Not balsamic vinegar. Put on bench.

- Get a large bowl and make sure it is scrupulously clean and dry.

- In a measuring jug or equivalent measure out the caster sugar you need in the one egg white to two ounces proportion. Leave in jug/container until needed.

- Separate egg white from egg yolks. Use actual eggs. Tried egg whites in a packet once and could not get the proportions right. Make sure there are absolutely no specks of yoke in the white. If you crack an egg and the yolk breaks – put it all with the yolks. Much like the dry bowl. Any speck of yolk and the pavlova won’t work.

- Beat egg whites until they are so stiff that you could upend bowl and nothing would come out. Up to you if you actually want to try it.

- Beat in caster sugar.

- Add a slurp of vinegar and a teaspoon or so of cornflour. Beat again.

- Take pavlova mixture and mound as high as possible on tray.

- Put into oven at 200 degrees. Immediately turn it down to 125 degrees and cook for an hour. Possibly a bit longer for very large pavlovas.

- After an hour turn off the oven but leave the pavlova inside. Leave everything exactly as it is overnight until the pavlova and the oven are completely cold. This technique should give you a pavlova with a crunchy outside and a marshmallow inside.

- Cream and fruit immediately before eating. Not before. Otherwise the crunchy bits will go soggy.

- You’re welcome.

But otherwise dear readers – Merry Christmas and Happy New (election) Year to you and yours. Back sometime mid January.

Namaste.