Fringe Benefit Tax – Reply from Inland Revenue

There is nothing much more humbling than motherhood. No matter how competent you are in your day job, one’s darling offspring have the ability to test every part of you.

For that reason I have rarely met arrogant mothers. Sure most of us have views about the right way of handling things but that is really a function of values and how your particular child works.

Because children’s superpower is their ability to ensure that we are only ever one meal or one exam or one party away from fully questioning our ability to raise the next generation.

Tax is much like that too. Tax people can be confident but we all know that we are only ever one opinion – missing a section or a case – away from falling completely on our faces.

And so it is for me on my recent post on Fringe Benefit Tax and double cab utes. Inland Revenue have kindly reached out to me to point out I overlooked a subsection – not the first time that has happened – and so office workers could not get the work related exemption if they had a sign written double cab ute.

I accept their analysis and accept that there is nothing in the law or its interpretation by Inland Revenue – as they have outlined it – that is driving the double cab ute phenomenon.

However it would be good to know how much FBT – or personal use adjustments – actually arises from personal use of the double cab utes. Because the ones I see aren’t even sign written.

Andrea

Reply from Inland Revenue

Hi Andrea

We have read your recent blog “Emissions, Feebates and Fringe Benefit Tax”(12 July 2019) and have a couple of comments regarding double cab utes and the work related vehicle exemption.

You have suggested that a sign-written double cab ute would be exempt from FBT under the work-related vehicle exemption. However, the work-related vehicle exemption is actually far narrower than that. Section CX 38 defines work-related vehicle:

CX 38 Meaning of work-related vehicle

Meaning

(1) Work-related vehicle, for an employer, means a motor vehicle that prominently and permanently displays on its exterior,—

(a) if the employer owns the vehicle, the form of identification that the employer regularly uses in carrying on their undertaking or activity; or

(b) if the employer rents the vehicle, the form of identification—

(i) that the employer regularly uses in carrying on their undertaking or activity; or

(ii) that the person from whom it is rented regularly uses in carrying on their undertaking or activity.

Exclusion: car

(2) Subsection (1) does not apply to a car.

Exclusion: private use

(3) A motor vehicle is not a work-related vehicle on any day on which the vehicle is available for the employee’s private use, except for private use that is— (a) travel to and from their home that is necessary in, and a condition of, their employment; or (b) other travel in the course of their employment during which the travel arises incidentally to the business use.

Paragraph (3) of s CX 28 is often overlooked. It states that if the vehicle is available for private use (other than for travel from home to work or incidental travel) then it is not a work-related vehicle and it will be subject to FBT. The exemption is actually quite narrow.

Inland Revenue interprets s CX 28(3)(a) to mean an employee cannot use a vehicle for private use except for travel to and from their home where that travel has a direct or needed relationship with the employee’s employment; and is a requirement of that employee’s terms of employment. So in your scenario, the shareholder-employee that runs the office would not be entitled to the work-related vehicle exemption. We make this point explicitly at para [107] of Interpretation Statement IS 17/07 “FBT and Motor Vehicles”:

For example, if a receptionist is given a vehicle to travel between home and work, the employer would not be entitled to the benefit of the private use exclusion in s CX 38(3)(a), because the travel to and from home is not necessary to the receptionist’s role.

We have tried to clarify this aspect of the work-related vehicle exemption for taxpayers and their advisors. Our Interpretation Statement IS 17/07 “FBT and Motor Vehicles” https://www.classic.ird.govt.nz/technical-tax/interpretations/2017/ explains the exemption in detail from para [66] onwards. We have also made a video on the work-related vehicle exemption: https://www.classic.ird.govt.nz/help/demo/fbt-videos/

Hope this helps and happy to discuss this with you if you’d like.

Kind regards

Emissions, Feebates and Fringe Benefit Tax

This week the Government released a discussion document on a form of emissions pricing for new and imported vehicles. Pretty much on cue the opponents were railing against this ‘tax’ thereby bringing it into scope for this blog.(1)

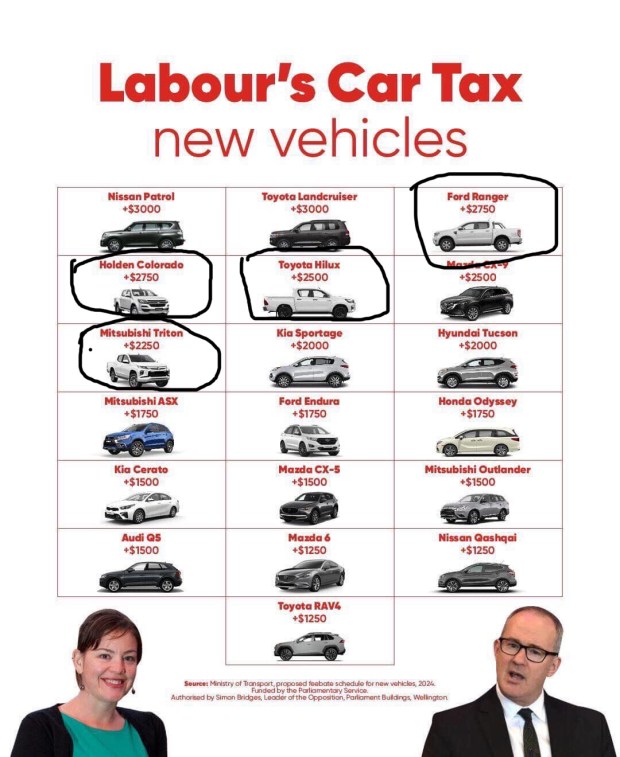

[The reason for the badly drawn boxes will become clear in a bit. I can assure the Leader of the Opposition that they have nothing to do with poor graphic design on the part of the National Party Research Unit.]

The idea is that heavy emitting vehicles would pay a charge and low emitting vehicles would get a subsidy. While they were aimed to broadly net off there is likely to be a net cost which the Government will need to appropriate as a reserve fund to keep it all moving (2).

As an aside my former tax policy self can’t help feeling what is proposed in the discussion document is all a bit technically perfect and could possibly be simplified without losing too many of the behavioural benefits. (3)

But implicit in all of this is that there is some sort of market failure or unpriced externality as New Zealanders, more than other countries, seemed to value a low capital cost highly even if it involved higher running costs.

I guess then in a ‘if you can’t beat them join them approach’ the deal is that the government will marginally bring down the capital cost of low emitting, low running cost vehicles. Giving net benefits of between $111 and $821 million being largely a reduction in fuel costs from people driving more fuel efficient cars.

I haven’t fully nailed this yet as conceptually on an npv basis if low emitting cars have lower running costs the net benefits should stand on their own without government intervention. So I am wondering if there is something in a lack of personal savings to fund the higher capital cost or a bias against potential loss of value v operating costs that is influencing these decisions. (4)

Regardless it seems to be a microcosm of the environmental tax proposals in the Tax Working Group. There the proposals were that any money raised from additional taxation was used to fund the transition to greater environmental sustainability. (5)

As here it was a bit loose. Revenue recycling was the term used rather than hypothecation as it gave the Government the ability to also put money into any transition programme and so not be constrained by the funds actually raised.

And much like most of the environmental proposals in the TWG report – behavioural benefits are the name of the game. Rather than revenue raising.

And much like all behavioural taxation and subsidies – whether they have any actual effect will depend on the elasticity of demand for such vehicles (6). Because if demand is:

- Very elastic – price sensitive – the $8000 benefit v $3000 cost will see a massive swing away from high emitting to low emitting vehicles. There will be no revenue raised and it will cost the Government a packet.

- Elastic ish – it will have an effect but there will still be high emitting cars purchased. This is useful if the Government wants minimise it’s contribution to the overall cost.

- Inelastic – price insensitive – there will be little or no change as people love their big emitting cars. On that basis it would start to become more like tobacco excise and become a good little earner for the Government. For the planet – not so much.

Now in the cabinet paper there is a list of other complementary things the government is doing (7). But curiously there is nothing on tax other than the RIS correctly ruling out a GST exemption for electric cars. Maybe it was because the Ministry didn’t consult with Inland Revenue (8) as I would have hoped the Department could have explained to them how environmentally unneutral fringe benefit tax (FBT) is.

Fringe benefit tax and the environment

The deal with fringe benefit tax is it taxes fringe benefits – such as ‘free’ cars or cheap loans – given to employees. The idea is that then there will be a tax level playing field to receiving cash wages and non-cash fringe benefits such as cars. FBT is an OG promoter of tax fairness as non-cash benefits are more likely to be given to higher income people.

However for completely unintentional reasons, in two ways, this tax could be incentivising the wrong things from an environmental perspective.

Carparks v public transport

The first is there is effectively no fringe benefit tax on the employer provision of car parks. This arises initially through an explicit exemption for any benefits provided on the employer’s premises.

The employer’s premises exemption make sense for compliance cost reasons as how do you work out the value of a benefit that is all part of the employer’s cost of running the business. So seems fair enough.

But when this meets car parks, the Department’s interpretation is that any leased land forms part of an employer’s premises.

And guess what – carparks are now all leased. Who would have thought!

There have been at least two attempts – one under Michael Cullen and another under Bill English – to legislatively remove this exemption. Both failed.

So rather than get on that horse again – as part of its environmental work – the TWG recommended that the government consider also removing FBT from the provision of public transport (9). To level the environmental – if not the tax – playing field.

Double cab utes and the work related vehicle

The second relates to double cab utes and the work related vehicle exclusion. See I told you my vandalising of the National Party’s work would become relevant.

[TL:DR The vandalised pictures would all meet definition of a work related vehicle – if signwritten – and be exempt from fringe benefit tax.]

A bit like the on premises exemption for car parks, there is also an exemption for work related vehicles. Again that makes sense for compliance cost reasons as there is not much private value from getting to take a work ute home.

In the late 80’s when I worked for a Chartered Accountant, the rules around work related vehicle were that it needed to be signwritten and it needed to have the back seats taken out of any vehicle that had more than two seats. I have very strong memories of the partner I worked for arguing with clients about how non negotiable both requirements were.

Now the rules seem to be that the vehicle is not ‘designed mainly to carry people’. (10)

I have been told that some time in the early 90’s the Department’s interpretation of this went from ‘take out the back seats’ to ‘double cab utes ok’.

Now for a sole operator tradie the need for the back seats may be a bit of a stretch as a requirement for a work related vehicle but is arguably ok. However I seriously struggle with a shareholder employee that runs the office and does the books having an FBT exempt dual cab ute. And yet that is exactly what is possible and completely legal.

All costs of the vehicle are tax deductible if the employer is a company and no FBT is payable.

So until there is a change to this I would suggest that the $3000 will simply be paid as it is less than the possible FBT that would otherwise be paid (11). In fact assuming no actual work related use or employee related expenditure any double cab ute that costs more than $31,000 it would make sense to just pay the $3,000. (12)

So may be this is revenue raising after all?

Andrea

Update (25/7/19)

Inland Revenue have kindly reached out to me to point out I overlooked a subsection – not the first time that has happened – and so office workers could not get the work related exemption if they had a sign written double cab ute.

I accept their analysis and accept that there is nothing in the law or its interpretation by Inland Revenue – as they have outlined it – that is driving the double cab ute phenomenon.

However it would be good to know how much FBT – or personal use adjustments – actually arises from personal use of the double cab utes. Because the ones I see aren’t even sign written.

(1) Long term readers will know this is nonsense as I will write on anything that spins my wheels.

(2) Paragraph 141 of Cabinet Paper.

(3) My former tax policy self also couldn’t help noticing options that looked awfully like tax pooling. The firms who offer that must currently be creaming it given the recent use of money interest rates. But that is a story for another day.

(4) Strictly speaking income tax also shouldn’t be a thing here as operating costs are tax deductible as is any interest expense and the capital cost is depreciable over time. It might conceptually be possible that the tax depreciation understates the actual depreciation but at 30% DV/21% straight line it doesn’t feel material or likely.

(5) Page 53 Paragraph 127

(6) Elasticity of supply will also feature in the final outcomes. If there is any form of constrained or monopolistic supply then the benefits could be absorbed by the supplier but with the costs passed on to consumer.

(7) Paragraph 35

(8) Paragraph 126

(9) Recommendation 18

(10) Section CX 38 of Income Tax Act 2007 and definition of car.

(11) 49.25% of 20% of cost price at say $45000 is FBT foregone of about $4.5k.

(12) Working backwards to a FBT cost of $3000, gives about $30,500.

Let’s tax this!

Let’s talk about tax.

Or more particularly let’s talk about sugar tax and Jacinda’s announcement about a regional fuel tax.

As of last week my gap year officially ended. Really keen now to go back to being a grownup. Trouble is still don’t know what that looks like. So as a bit of a transition path; decided tutoring tax to lovely young people at Victoria would be a good idea. Had no idea it would require seven hours of training – don’t ask – before I could get in front of them though. But all over now and three weeks of actual tutoring has now taken place. Hence the transmission silence.

Now the first week of classes included a question on legal v economic incidence of taxation aka who bears the tax aka taxes are gross.

And since I last posted the Sugar tax people have done some work and the lovely Jacinda – who may or may not have a baby as PM – has announced a regional fuel tax to fix Auckland. Well transport anyway.

So as this is what passes as topical these days for tax; today I’ll look at sugar and petrol taxes. More similar than you’d think. And both come down to who pays the tax is different to who bears the tax. TAXN 201.

Now while a sugar tax is but a dream of public health professionals; petrol tax is currently in existence. And unlike GST which cascades; petrol tax is an excise simply applied either at the border or at the refinery. Same applies to alcohol and cigarettes – except for the refinery bit. One off charge to producers or importers which then flows through – or not – to the final consumer.

Now there is the whole ‘paying for roads’ thing with a petrol tax but fundamentally it is a tax because we can. Petrol – almost like insulin – has a relatively inelastic demand. No or minimal dead weight loss. No triangles. What’s not to love?

And because of this no deadweight loss/inelastic demand, the tax that is paid by the oil company feeds through to the price paid by the car driver. And so my aversion to driving and cars makes it a form of legitimate tax avoidance. Sweet. But otherwise tax is raised with little change in behaviour.

Now a regional fuel tax is interesting. I guess the vibe is that petrol that is consumed in Greater Auckland gets the tax and petrol that isn’t – doesn’t. It could be that the destination can be broadly worked out once it leaves the refinery on its way to the Wiri tank farm. Auckland pipeline or something. In which case it will be a matter of the oil companies adding another set of codes to their computer system. I’m sure that they accept that without comment. Even then there’ll probs need to be a crediting system for fuel delivered outside the taxable region.

Alternatively if it can’t be worked out – then it will have to be charged by the individual petrol station. Possibly by the oil companies when they deliver to them. They’ll enjoy that too.

But one way or another because of our carbon economy, serious money will be raised. Perhaps more buses will be taken but broadly Auckland car drivers will have less money to spend on other things.

On the other hand – the Sugar Tax people’s gig is not that they want revenue raised per se. Although they do have a laundry list of stuff they want the money spent on. More that they want an increased price so that less of it is consumed. Because health reasons. And as someone who has a tricky relationship with the white stuff – am sympathetic. But whether it ends up being a corrective tax with some revenue raised – like cigarettes – or just a tax grab all depends on the elasticity of demand for it.

If we turn our minds back to taxes are gross. Wage income has an elasticity of 0.414; non- wage income of 0.909 – source Treasury. While cigarettes have an elasticity of 0.5 – source my aging brain.

Now working on the assumption that sugar is less addictive than cigarettes and less embedded than Auckland car driving; all things being equal there should be less of it consumed. So although it would have a similar structure to a petrol tax it would be a corrective tax rather than a revenue raiser per se. Although with cigarettes it does a good job at being both. But as is seen with cigarettes the tax has to get to eye watering levels to actually have a significant impact.

The complexities with a sugar tax all come with:

- What is taxed? Sugar or soft drink

- What is the level of the tax? Ultimately a political decision like all taxation.

- Who collects it? Probably the importers.

Personally I am an agnostic. For people who are really interested in this stuff I’d recommend the recent book co written by Lisa Marriott on this. After reading it: still agnostic. With all taxes the compliance and administration is far more than proponents ever realise. So I’d prefer far tougher regulation on advertising to children before moving to tax. But as part of a package like cigarettes – maybe.

And no removing GST from healthy food is so not the answer. Because rich people spend far more in absolute terms on healthy food than poor people do. And like the whole tax free threshold thing – ends up being a bigger tax cut to the rich than the poor.

Now dear readers you may have noticed that my weekly postings are no longer happening. I am still fairly active on the blog’s facebook page https://www.facebook.com/Letstalkabouttaxnz/ but full blog posts – not so much. Because busy.

Coming up to the election; I have views. And as I am no longer a bureaucrat; will be doing some partisan foot soldier stuff. So maybe a transmission silence until then.

I am however fascinated by what is happening and am seeing parallels to the 1984 election. If I get time I will share that with you.

But otherwise see you all on the other side – of the election.

Andrea

#shelterisforpeople

Let’s talk about tax.

Or more particularly let’s talk about the proposed Australian tax on under-utilised properties.

Now in New Zealand the big tax story is how Labour is planning to remove tax breaks from ‘speculators’. Including the best headline ever – ‘Shelter is for people – not for tax‘. Great strap line. I can see the #shelterisforpeople hashtags and possible memes. And all because they are only planning to remove negative gearing.

Now negative gearing is a term used when losses – usually from interest – from renting out a property are deducted from other taxable income. Usually income from a day job. And this kinda is a standard feature of our tax system. All income is added together and then all deductions are offset and tax is paid on the balance.

However with property a major form of income – capital gains – is not included in the calculation. So this does give a degree of tax preference – or shelter – that ordinary businesses don’t get. Is it a loophole? Dunno. Not including capital gain definitely is a loophole. But really the only way interest should actually be allowed even with including capital gains – is if they were taxed every year on an unrealised accrued basis. Now that would really be #shelterisforpeople.

And until that ever happens – no breath holding here – all that second order stuff like removing tax depreciation and negative gearing has a place. Such restrictions also probs still have merit with a realised capital gains tax as can be massive deferral benefits with that. Remember how the retirement villages don’t ever sell?

And of course in all this #shelterisforpeople stuff around negative gearing there is no mention of the other real tax breaks of:

And given the cr@p Labour is getting over this relatively mild proposal – which will only move the tax system towards fairness a tiny bit – I can’t say I blame them. Working group I guess.

And into this mix comes the recent Australian proposals to tax ‘under-utilised’ housing of foreigners. The rhetoric behind it is to free up housing for Australians. And I guess it comes off the reports of large scale empty properties in Sydney. Now recently I watched – with increasing horror – my son and his girlfriend both with incomes and references trying to find a flat in Manly. So I am totes in support of that objective – so long as ‘Australians’ can be also read as bludging Kiwi students. Not entirely sure why it is targetted at foreigners though. Coz exactly why is the nationality of the landlord relevant when the problem is that a house is empty?

Now the actual plan is to impose the charge that is levied when foreigners get permission to buy property in the first place. AUD 5,000 for a property of less than AUD 1 mill and equivalently more thereafter. And much like the Inland Revenue restructure cleverer people than me will have come up with it; but here’s what I don’t get:

- One. If someone is rich enough to own property and not need to rent it out then don’t ya think they can cope with an extra 5-10k expenditure?

- Two. Collectability. Now I get that people will pay if it is the price of getting what they want. But how exactly is this going to be collected from people who have already got the right to buy a new property? And from foreigners who by definition don’t live in Australia much? How is this going to work exactly? There are collection clauses in some treaties but this won’t be a tax covered by them.

- Three. AUD 16.5 m over next three years collected. Really? All this for just $16.5 mill?

Now if this is a big problem such a corrective tax could be put into the mix. But then it needs to be:

- A tax that is penal. So people look to change their behaviour;

- Applied to all under-utilised properties. Coz foreigners only is nuts; and

- Deemed income tax so collection clauses in treaties can be used.

Now there is no mention of an equivalent policy in the Labour stuff. Maybe under-utilised property isn’t a big problem in New Zealand? Even if Gareth does have six. But much like the Bank Levy – let’s not blindly follow the Australians. If we want one let’s make it work.

Andrea

Cry me a river

Let’s talk about tax. Yes dear readers – tax. No prison reform no yoga stuff. Just nice emotionally simple tax.

Or more particularly let’s talk about the recent Australian Budget announcement of a levy on banks aka the Great Australian Bank Robbery.

Your correspondent has now completed her yoga teacher training and so is available for weddings, funerals and bar/bat mischvahs. Highlights of the course included injuring herself while dancing and getting zero on the first attempt on the final exam.

It’s not like I haven’t failed things before but when the question was – reminiscent of the Peter Cook coal miners sketch – ‘who am I?‘ to fail – mmm – more than a little surreal. Now even the first time thought I had answered in a sufficiently right brained way – lots of introspective emotion involving personal power and connection with others – aahhh no.

But your correspondent is a resilient adaptive individual – even before the course – so regrouped with – ‘complete‘.

90%.

I couldn’t make this up. Subsequently found other correct answers included: me; enough – and my particular favourite – light. Ok right. Thanks for sharing.

And it all really did make me crave balance. Which in my world after eight full days on yoga is the left-brained world of tax. I had planned to write about the Australian transfer pricing case Chevron but this week has been the Australian Budget with a big new tax on their banks. And as I have had a few questions on this and I am trying to be more topical – here we go:

Now the bank tax thing seems to be part of a package of the Australian government responding to the Australian banks bad – but probs more likely monopolistic – behaviour. Also potentially a political response to appointing a popular Labour Premier – and good god a woman – to be head of the Bankers Association. And my word the banks must have been bad as they only found out about it on Budget Day and it starts on 1 July without – as far as I can see – any grandfathering.

Wow. Just wow.

So what is it?

It is a levy on big banks liabilities that aren’t:

- customer deposits or

- (tier 1) equity that doesn’t generate a tax deduction.

It targets commercial bonds, hybrid instruments (tier 2 capital) and other instruments that smaller banks can’t access coz they are small. And as it will form part of the cost of this borrowing- under normal tax principles – the levy would be tax deductible. But even allowing for this tax deduction it is supposed to raise AUD 6.2 billion over four years. So not chump change.

What is its effect?

Now there can be no argument that the levy will effectively make such instruments more expensive to use. And here the public arguments get really sophisticated:

- Malcolm Turnbull says that ‘other countries have them’ and it would be ‘unwise’ for banks to pass it on to borrowers; and

- the Treasurer Scott Morrison (ScoMo) is telling banks to ‘cry me a river’ when they have expressed a degree of displeasure.

Awesome. Thanks for playing.

Corrective taxation

Now while this is predicted to raise revenue; it is by no means clear that this is its primary objective or even if it will occur. The reason being it only applies to big banks and to certain types of liabilities. To me this looks like a form of corrective tax like cigarette excise rather than a revenue raiser like an income or consumption tax like GST.

And much like a tax on cigarettes; pollution or congestion; this tax is 100% avoidable – legitimate tax avoidance even – by funding lending with an untaxed option like customer deposits. In theory anyway. It is likely that banks will have maxxed out how much they can borrow from the public at existing interest rates.

But with this extra tax; the relativities will change. Meaning there is now scope to pay more for the untaxed deposits but less than the tax if Banks want to maintain the same level of lending. Bank costs will still go up but through marginally higher deposit rates incentivised through the tax – rather than the tax itself.

In this scenario the Australian government still gets the costs of the higher interest deduction but not the revenue. But Australian savers win.

As the big banks are the dominant players in the market – this increase in interest rates for depositors will also impact the smaller banks as they will need to pay the higher rates to continue to attract depositors too. So no actual competitive pressure from the small banks and possibly less actual tax. Genius.

An alternative equally revenue enhancing scenario is that banks wind down assets – lending – and become smaller. Less lending but higher cost of borrowing if demand stays the same.

Who bears the cost?

As they do in New Zealand anytime extra taxes are mooted; the Australian banks are arguing that these extra costs will be borne by borrowers. Now in a fully competitive market without barriers to entry the more price dependent – or elastic – the demand for loans is the more it will fall on the shareholders. But lending overall will fall with the imposition of a tax which in turn will have housing market impacts if fewer people can get a mortgage.

With barriers to entry – like hypothetically say banking regulation – they are already pricing to maximise their profit so I would be inclined to say it will also hit shareholders. And the fall in price of banking shares would indicate that is what shareholders think too.

Except that if deposit rates go up instead; the cost structure of the entire banking industry will go up. And if no tax is actually being paid but the cost is being transferred through higher deposit rates then the banking industry will have political cover to pass the cost on to borrowers.

Alternatives

Now if this schmoozle is all about the banks paying more tax then either a higher company tax rate on big banks or increasing the requirements for non- interest bearing capital would have been far simpler. While the former is pretty transparent that it is a blatant tax grab from the banks; the latter less so. They both have the advantage though of ensuring tax can’t be opted out of as well as keeping the competitive pressure from the smaller banks.

But both would form part of the banks cost structure and so – depending on the pressure from the small banks and how elastic demand is – be passed on in some form to borrowers. However if the government really wanted only the shareholders to pay then a one- off windfall tax would be the way to do it.

Whether or not the banks – and their shareholders – should actually be treated like this is another story. But Cry me a river ScoMo: at least be transparent and do it properly!

Other stuff

It goes without saying that this is truly cr@p process. All the detail seems to be in ScoMo’s press statement. Although – legislation by press statement – is an unfortunate feature of Australian tax policy.

And as for the Malcolm Turnbull ‘other countries have it too’ argument. From what I can see this was to pay back the government for the bail outs they gave the banks over the GFC. While Australia does have deposit insurance I wasn’t aware of any like actual bailouts.

It is though kinda reminiscent of the diverted profits tax which is also a targetted tax on a group of bad people. Except that might have a non-negative tax effect. Here we have – to extent it is passed on in higher deposit rates – higher costs industry wide causing less, not more, tax paid by this industry. Let’s just hope for Australia’s sake the savers are not all in the tax free threshold.

So nicely done ScoMo and Big Malc. Possibly more Lavender Hill mob than Ronnie Biggs. But much like the Australian fruit fly; keep it on your side on the Tasman. It makes even this revenue protective commentator blanch and our banking tax base can so do without it.

Andrea

Update

A commentator on the blog’s facebook page has suggested that this levy makes sense in terms of addressing the huge implicit subsidy that is the Australian deposit guarantee scheme. I have absolutely no issue with this being charged for in the form of a levy on the banks. Naively I would have thought that such a levy would then be based on the deposits covered by the guarantee not the liabilities that aren’t. Apparently that’s not how Australian politics works!

The discussion can be found in the Facebook comments section for this post.