Tax and small business (2) – company tax rate

Last week was a big week for your correspondent.

On Wednesday I got to upgrade my CA certificate to a FCA one at a posh dinner at Te Papa. As a third generation accountant I was absolutely tickled pink by that.

Interestingly of the 12 Wellington people there were 5 tax people: Me, Mike Shaw, Suzy Morrissey, Stewart Donaldson and Lara Ariel. All except Lara I have had the great pleasure to work with personally and professionally over the years.

I got to give a wee talk and so thanked my Wakefield (mother’s accountant line) genes; the balance sheet for being able to distinguish between the concept of capital as an asset or net equity – a framework other professions lack; and Inland Revenue Investigations as both the employer of my proposers and the place of some of the highlights of my personal and professional life.

I gave a slightly longer talk on the Tuesday. Twelve minutes instead of two.

The theme of that seminar was options to improve fairness now that extending the taxation of capital gains was off the table. The punchline of my talk was that the company tax rate should be raised.

I had come to that point following lots of feedback on my tax and small business post.

Very experienced tax people were sympathetic to my concerns but the ideas of mandating the LTCs rules or restricting interest deductions or even a weighted average small company tax rate sent them over the edge with the compliance costs involved. Their preference was that it was just simpler all round to increase the company tax rate with adjustments such as allowing the amount of deductible debt for non-residents.

And so on Tuesday I had a go at putting that argument.

Clearly not well as Michael Reddell described the argument as cavalier given NZ’s productivity issues.

Regular readers will know I am concerned about whether the tax system is a factor in New Zealand’s long tail of unproductive firms without an up or out dynamic. And that is before we get to any well meaning – but not always hitting the mark – collection of small companies tax debts inadvertently providing working capital for failing firms.

Although I had twelve minutes to talk on Tuesday, the company tax punchline really only got a minute or two to expand. So I’ll try and have a better go at it here. (1)

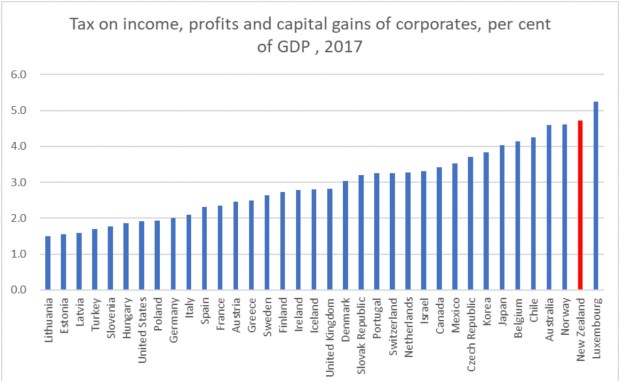

Now before we get to the arguments in favour of a company tax increase, Michael referred to this table as prima facie indicating that business income is not overtaxed.

Yep.

This table absolutely shows that second to – that other well known high tax country – Luxembourg, New Zealand’s company tax take is the highest in the OECD as a percentage of GDP.

My difficulty is that – in a New Zealand context – I struggle to call the company tax collected – a tax on business income.

Absolutely it includes business income.

But it also includes tax paid by NZ super fund – the country’s largest taxpayer and Portfolio Investment Entities which are savings entities. In other countries such income would be exempt or heavily tax preferred. And yes I know there are arguments about whether they are the correct settings or not but all that tax is currently collected as company tax.

Also, for all the vaunted advantages of imputation, the byproduct of entity neutrality is the potential blurring of returns from labour and capital for closely held companies. So – and particularly with a lower company than top personal rate – there will always be income from personal exertion taxed at the company rate.

And business income is also earned in unincorporated forms such as sole trader or partnership. All subject to the personal progressive tax scale rather than the flat company rate.

Australia’s company tax is also high but less so. Possibly a function of their lower taxation on superannuation than New Zealand or even that such income is classified according to its legal form of a trust.

And all that is before we get to issues like classical taxation in other countries encouraging small businesses to choose flow through options to avoid double taxation. An example is S Corp in the US. Tax paid under such structures will not be shown in the above numbers as the income is taxed in the hands of the shareholders.

It is true that we have a similar vehicle here in the look through company. But unsurprisingly, under imputation, this is used primarily for taxable incomes of under $10k. It is quite compliance heavy and does require tax to be paid by the shareholder while it is the company that has the underlying income and cash. But it is elective and seems to be predominantly currently used as a means of accessing corporate losses.

But back to tax fairness and company taxation.

The argument put to me by my friends – with more practical experience than I have – was: if you want to increase the level of taxation paid by the people with wealth – increase the company tax rate as that is the tax rich people pay. The logical tax rate would be the trust and top personal rate – currently 33%.

That company tax is the tax rich people pay is absolutely true. The 2016 IR work on the HWI population shows exactly that:

It would also mean that the rules that other countries have like personal services companies or accumulated earnings – that we absolutely need with a mismatch in rates – no longer become necessary.

But what about foreign investment through companies?

If the focus was New Zealanders owning closely held New Zealand businesses, an adjustment could be made either by increasing the thin capitalisation debt percentage or making a portion – most likely 5/33 – of the imputation credit refundable on distribution.

However there is also an argument not to do this. The relatively recent cut in the company tax rate has not particularly affected the level of foreign investment in New Zealand. (2)

Personally I am agnostic.

Listed companies?

Based on officials advice to the TWG (3) this group fully distributes its taxable income. So if the company tax rate increased all this would mean was that resident shareholders received a full imputation credit at 33% rather than one at 28% and withholding tax at 5%.

What happened to non-resident shareholders would depend on the decision above on non-resident investors. Either they would pay more tax on income from NZ listed companies or there could be a partially refundable imputation credit to get back to 28c.

The top PIR rate for PIEs could now also be increased to the top marginal tax rate for individuals as I keep being told the 28c rate is not a concession – more to align it with the unit trust or company tax rate. Or maybe KiwiSavers stay at 28% alongside an equivalent reduction for lower rates.

Start ups already have access to the look through company rules and so some more may access those rules if the shareholders marginal rates were below an increased company tax rate.

So an increase in the company tax rate need not have a material impact on foreign investment, listed companies and start ups.

Which then brings us to profitable closely held companies. Ones where the directors have an economic ownership of the company. A lower tax rate should, on the face of it, have allowed retained earnings and capital to grow faster. And therefore allow greater investment.

And on the face of it that is what has seemed to happen with this group. Imputation credit balances have climbed since the 28% tax rate meaning that tax paid income has not been distributed to shareholders.

However loans from such companies to their shareholders have also climbed indicating that value is still being passed on to shareholders – just not in taxable dividend form.

Now yes shareholders should be paying non-deductible – to them – interest to the company for these loans but it is more than coincidental that this increase should happen when there is a gap between the company rate and that of the trust and top personal tax rate.

And alongside this was an increase in dividend stripping as a means of clearing such loans.

So an increase in the company tax rate would reduce those avoidance opportunities and align the tax paid by incorporated and unincorporated businesses.

And with more tax collected from this sector, Business would have a strong argument for more tax spending on the things they care about. Things like tax deductions in some form for seismic strengthening, setting up a Tax Advocate, or the laundry list of business friendly initiatives that get trotted out such as removing rwt on interest paid within closely held groups.

Some of which might even be productivity enhancing.

For the next few months, I am returning to gainful – albeit non-tax – employment. As it is non-tax there should be no conflicts with this blog except for my energy and – possibly – inclination.

I am hopeful that at least two guest posts will land over this period and you may still get me in some form.

But otherwise I will be maintaining the blog’s Facebook page, and am on Twitter @andreataxyoga. I can also recommend Terry Baucher’s podcasts – the Friday Terry – when he isn’t swanning around the Northern Hemisphere.

Andrea

(1) Officials wrote a very good paper for the TWG on company tax rate issues. It can be found here: https://taxworkinggroup.govt.nz/sites/default/files/2018-09/twg-bg-appendix-2–company-tax-rate-issues.pd

(2) Paragraph 33 for a discussion of this graphs limitations. These include a reduction in the amount of deductible debt and depreciation allowances at the time of the reduction to 28% which would have worked in the opposite direction to the tax cut.

(3) Paragraph 11

Tax and Small Business

Last week the Small Business Council issued its report to Government. I am sure there are many wizard things in there maybe even some tax recs.

Also last week I had a friend to stay who is helping some workers that have lost thousands of dollars of wages and holiday pay when their employer went into receivership. Her expression was Wage Theft. It is a crime in Australia but not in New Zealand. Unlike theft as a servant which totally is.

Talking to her it was obvious that there was considerable overlap between what she is seeing and the issues considered by the TWG of closely held companies where the directors have an ownership interest not paying PAYE and GST (1).

And yes my friend’s friends are worried about their PAYE and KiwiSaver deductions. So really hope tightening up on this stuff is in the Small Business report along with the expected recs on compliance cost reduction.

I am also personally very interested in what the Group comes up with as the Productivity Commission noted that NZ has a lot of small low productivity firms without an up or out dynamic (2). That is firms tieing up capital that should be released for more productive purposes with the associated benefit of not staying on too long and dragging their workers and the tax base with them.

Now ever since I found that reference I have been concerned that there may be aspects of the tax system that may be driving that. Benefits or ‘opportunities’ that don’t arise for employees subject to PAYE or owners of widely held businesses subject to audits and outside shareholder scrutiny.

And it is true that there is nothing particularly special in a tax sense here to New Zealand. However given that New Zealand rates as number one in the ease of doing business index there may be more people going into business than would be the case in other countries.

Some of these aspects can be reduced through stricter enforcement by Inland Revenue but are otherwise largely structural in a self assessment tax system where the department doesn’t audit every taxpayer. One is a policy choice possibly because the alternative would add significant complexity to the tax system and the final example is a combination of the need for stronger enforcement and/or policy changes needed now that the company and top personal rate are destined to be permanently misaligned.

So what are these ‘aspects’?

Concealing income or deducting private expenses

Recent work by Norman Gemmell and Ana Cabal found that the self employed had 20% higher consumption than the PAYE employed at the same levels of taxable income.

Now it could be that for some reason the extra consumption of the self employed comes from inheritances or untaxed capital gains or taking loans from their business – more on that later – more so than those in the PAYE system or owners of widely held businesses. It might not be tax evasion at all.

But we just don’t know.

All we know is the 20% extra consumption and that there is a greater opportunity and fewer checks with closely held businesses to conceal income or deduct personal expenses. And Inland Revenue says such levels are comparable with other countries.

While things like greater withholding taxes and/or reporting can help, I am also concerned that with greater automation it also becomes much easier to have those personal expenses effortlessly charged against the business rather than recorded as personal drawings.

Interest Deductions

The second aspect is my specialist subject of interest deductions. Unlike concealing income or deducting personal expenditure – this one is totes legit.

Interest is fully deductible to a company and for everyone else it is deductible if it can be linked to a taxable income earning purpose or income stream aka tracing.

What that means is if a business person has a house of $2 million and a business of $1 million and has debt of $1 million – all the interest deductions on the debt can be tax deductible – if the debt can be linked to the business. This can be compared to a house of $2 million and debt of $1 million – and no business – where none of it is deductible.

To make this fairer with taxpayers who don’t have the opportunity to structure their debt there would need to be some form of apportionment over all assets – business and personal. So in the above example interest on only $330,000 should be allowed.

But yes – that would require a form of valuation of personal and business assets. And yes valuing goodwill brings up all the same – valid – concerns raised with taxing more capital gains.

So I guess we can say that under the status quo fairness – and possibly capital allocation – have been traded off against compliance costs.

Income Splitting

The third is the ability to income split with partners to take advantage of the progressive tax scale. Now this is only actually allowed if the partner is doing work for the business. But verifying the scale and degree of this work – even with burden of proof on Commissioner – is a big if not impossible task for the Commissioner.

Other mechanisms include loans from the partner to help max out the lower income tax bands.

And the statistics would support an argument that there is a degree of maxing out the lower bands just not that there necessarily is a lot of income splitting.

Interestingly both Canada and Australia have rules for personal services companies where these types of deductions are not allowed.

But this is ok if this is the amount of value going to the shareholders. Maybe our firms are so unproductive that they can only support shareholder salaries of $70k and below.

If that were the case though we wouldn’t be seeing the final aspect which is taking loans from companies you control instead of taxable dividends.

Overdrawn shareholder current accounts

Now to be fair for this to occur there should also be interest paid by the shareholder to the company on loans from the company to the shareholder. And unlike the interest in point 2 – none of this should be tax deductible to shareholder if it is funding personal expenditure while the interest received will be taxable. This on its own should be enough to not do it and receive taxable dividends instead.

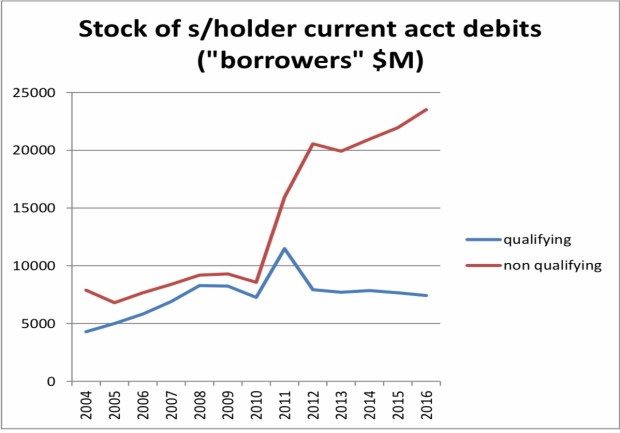

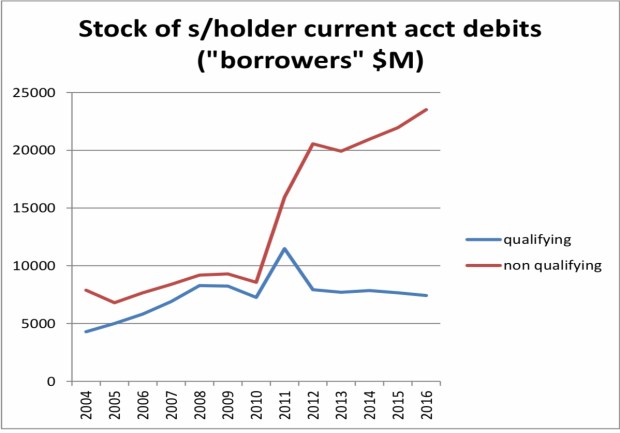

Unfortunately the facts also don’t seem to back this up. Imputation credit account balances – meaning tax has been paid but not distributed- have been climbing. Now this could be like totally awesome if it meant all the money was being retained in the company to grow.

Except that overdrawn current account balances – loans from the company to the shareholders- have been similarly growing too. Now sitting at about $25 billion.

And yes this all started from about 2010. And what happened in 2010? Why dear readers the company tax rate was cut to 28% while the trust rate remained at 33%.

Ironically the associated cut in top marginal rate was to stop the income shifting that went on between personal income and the trust rate.

Now one level it shouldn’t matter at all if these balances continue to climb so long as non- deductible assessable interest is paid on the debt. However an overdrawn current account is – imho – the gateway drug to dividend avoidance.

And yes that can be tax avoidance but much like the tax evasion opportunities, income splitting and interest on overdrawn current accounts – all of this requires enforcement by Inland Revenue. And as they can’t audit everyone there will always be a degree that is structural in a self assessment tax system.

But the underlying driver of people wanting to take loans from their company rather than imputed dividends is that our top personal tax rate and company tax rate are not the same. Paying a dividend would require another 5% tax to be paid.

Possible options

Now other countries have always had a gap between the top rate and either the company or trust rate so this shouldn’t be the end of the world. But those countries have buttressing rules that we don’t have in New Zealand. The personal services company rules discussed above or the accumulated earnings tax in the US (3) or the Australian rule that deems such loans to be dividends.

Until recently I had been a fan of making the look through company rules compulsory for any company that was currently eligible. (4) I couldn’t see the downside. The closely held business really is an extension of its shareholder so why not stop pretending and tax them correctly.

However some very kind friends have been in my ear and pointed out the difficulties of taxing the shareholder when all the income and cash to pay the tax was in the company. It works ok when it is just losses being passed through. So maybe I am less bullish now.

An alternative approach could be to apply a weighted average of the shareholders tax rates on the basis that all the income would be distributed. Similar to PIEs. The tax liability is with the entity but the rate is based on the shareholders. I guess you then do a mock distribution to the shareholders which can then be distributed to them tax free. And yes only to closely held companies. Wider would be a nightmare.

Kind of a PIE meets LTC.

Or you could just old school it and raise the company tax rate to 33% for all companies. Shareholders with tax rates below that could use the LTC rules and make the assessment of whether the compliance of the rules was greater or less than the extra tax.

It would require an adjustment to the thin capitalisation rules by increasing the deductible debt levels to ensure foreign investment didn’t pay more tax. But for some of you dear readers increased taxation on foreign investment might even be a plus.

But all in all I don’t think the status quo with small business is a goer. Whether it is for fairness reasons, or capital allocation reasons or simply stopping me worrying – doing something is a really good idea.

Because I would hate to think any of this was enabling behaviours that kept people in business longer than they should. And even with the most whizziest of new IRD computers – there will always be limits on enforcement.

Andrea

(1) Page 116 Paragraph 68

(2) Page 19

(3) Although it would make more sense to only apply this to the extend that the income hasn’t been retained in the business and distributed in non- dividend form.

(4) Yes there is the issue that companies could start adding an extra class of share to get around this. But I don’t believe this is insurmountable with de minimis levels of additional categories and the odd antiavoidance rule for good measure. It is even the advice of KPMG so clearly not that wacky.

Alignment again

Let’s tax about tax.

Or more particularly let’s talk about Australia’s proposal for a reduced tax rate for small business.

Ok yes I am excited. A new government. A Labour led government. And a young woman as a Prime Minister. Mostly what I hoped for as I climbed the millions of steps to door knock in Wellington. My left leg is almost recovered too. Thanks for asking.

And as if all of this wasn’t exciting enough two of my young friends Talia Smart and Matt Woolley won the Robin Oliver tax competition. Talia on Charities and Business and Matt on the integration of the company and personal tax. I hope to cover their papers once they become public.

Oh and Stuart Nash has won the pools and become Minister of Revenue.

So big congrats to Talia, Matt and Hon Stu. Expecting great things from you all.

We should hear about the tax working group soon. A group that as well as looking as the fairness thing for tax is also looking at housing affordability. And as of today is now looking at whether small businesses should have a lower tax rate. Like wot Australia has.

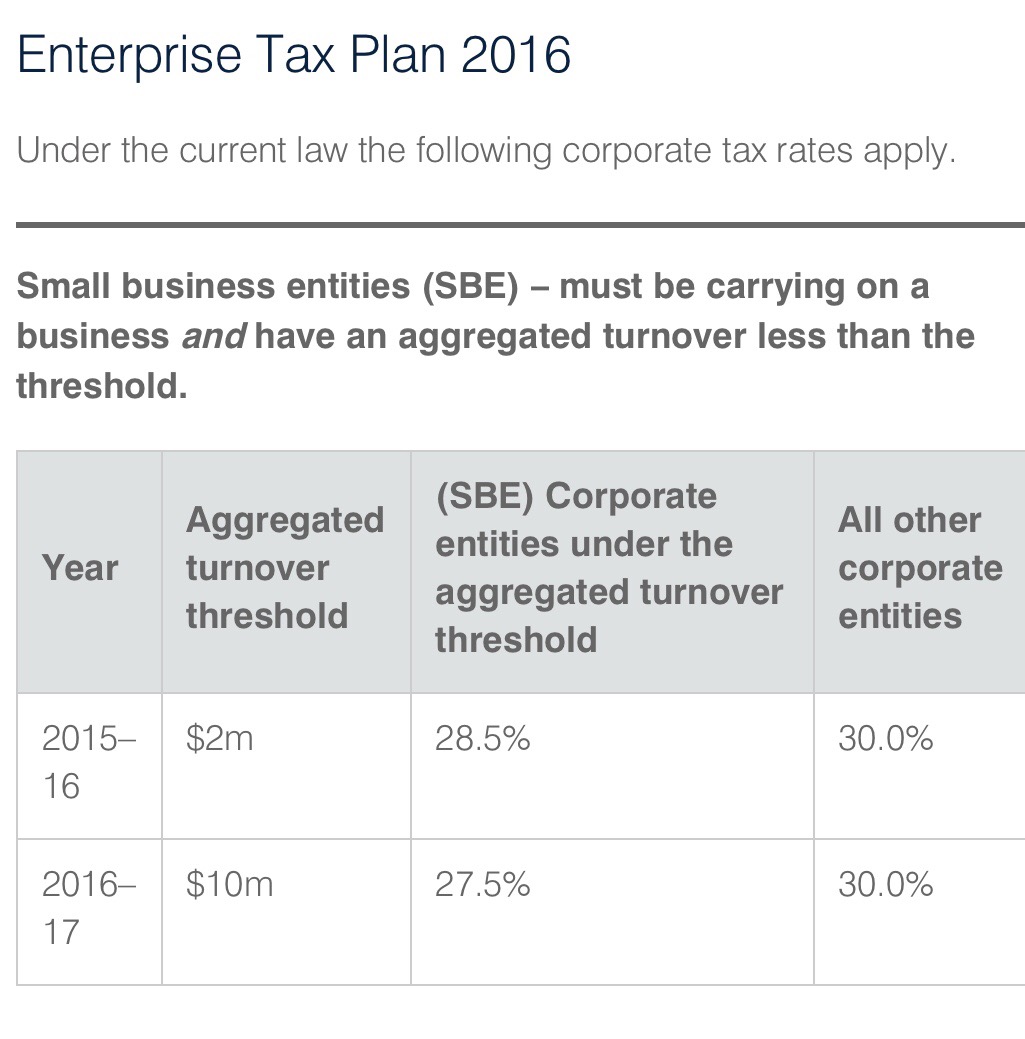

Now as hadn’t really paid any attention to this dear readers now seems like an opportune time to have a look. Apparently in 2016 the Australian government reduced the tax rate on companies with a low turnover who were in business like this:

Then they said in future years the threshold for what is small will go up and the tax rate will go down:

And then just to be fun, they introduced but didn’t pass another bill which would have reduced rates for everyone ultimately. At this point I just thank the tax gods I live in New Zealand.

Now there is a thing that if the turnover is more than 80% passive income – dividends and the like – the lower rate doesn’t apply. But 75% alg. And the turnover thing seems to have a group concept in it – so that is something. No splitting up companies – in theory anyway.

Tbh it looks like a fiscal thing. Reducing the company tax rate but it a way that doesn’t all go to the nasty big companies. Some of whom will be foreign. So will cost less than a simple company tax reduction.

Conceptually a tax cut for small business – not nasty big business – what’s not to love? The tax equivalent of free doctors visits. It does have a few downsides:

- At the margin may inhibit growth. Coz who wants to grow and get a higher tax rate?

- Incentivise passive holding companies. 80% is still pretty and

- (You guessed it) incentivise recharacterisation of other higher taxed forms of income. Aka alignment issues.

As we have discussed before dear readers – alignment matters. Whether it is misalignment of the trust and top rate or the company and the top rate. Income will gravitate to its lowest taxed form. Now if that income stays in the company and helps it grow. Alg. Effectively a tax subsidy for small business who might use this money to – say – help offset the higher minimum wage.

But it also might further incentivise the whole ‘salary at $70k’ thing; an overdrawn current account; and dodgy as dividend stripping. Because with small business the corporate veil in practice is pretty thin. The shareholders, the company and the senior employees are all the same people. And as we saw last week, small business isn’t as tax pure as maybe first thought.

The tax avoidance provision will help but is no way to run a tax system. Maybe we’ll need some tighter rules on getting money out of a company. That has merit regardless.

Will be interesting to see what the working group thinks about it.

Andrea

Stripped for action

Let’s talk about tax.

Or more particularly let’s talk about small business owners not paying the top marginal tax rate.

Well this has all taken much long than I expected.

Getting back to you dear readers. What else could I be taking about? Post election I was ready to go again but then had some family stuff to do. But I am here now.

Election night every part of my body hurt. And that was nothing to do with the result. After 24 years in Wellington – and as an ex runner – I thought I knew about hills. But after a couple of weeks of (almost) daily door knocking when (almost) every door in Wellington was up a vertical incline – I was spent. I was ready for it to be over. Win, lose or draw.

Except it still isn’t over.

But focussing on what is really important – my body has recovered and family stuff is sorted. So I can think about real tax again. Not what passes for tax in an election campaign.

Now while I was out destroying my aging body a very interesting paper was delivered at the Law Society’s annual tax conference entitled Dividend Avoidance. In that paper five ways were outlined for owners of closely held companies to get dosh out of their companies tax free. Aka not triggering the dividend rules.

Now this is very interesting for a number of reasons:

- The rhetoric that small businesses are ‘paying their fair share’ just might not be true;

- The 5 ways will only be used when have shareholders that earn more than $70k – ie not poor people;

- Only became an issue when company tax rate became 28% and

- James Shaw inadvertently outed this early this year and was told by the Minister of Revenue – and to an extent me – that there was nothing to see.

Now before we go through one of the clever – and possibly too clever – ways the top marginal tax rate isn’t being paid; a few building blocks.

BB 1

The imputation/dividend interface should mean that when value shifts from the company to the shareholder; tax not paid at the company level is paid by the shareholders. Aka #doubletaxationisgross. This includes use of losses. It doesn’t matter how tax is not paid. When it goes to the shareholder he or she should make up the difference.

BB 2

Dividends paid between companies with the same ultimate shareholders are taxfree. Coz same economic ownership so no actual value passing.

BB 3

Capital gains earned by a company can only be passed on to shareholders tax free if the company is liquidated. And liquidation should be kinda big deal. Otherwise a capital gain is simply untaxed income that will get taxed when goes to the shareholders.

BB 4

The actual market value of the company – goodwill – can only come on to the the company’s books on sale. Accounting standards quite correctly stop companies increasing their accounts for their market value. Too easy to be abused.

BB 5

Shareholders can take money out of their companies at any time. This is done through the shareholder current account. When they take out more money than they have earned it becomes negative or overdrawn. If the shareholder is also an employee they need to pay non-deductible interest on this loan.

But – in theory – this whole drawing more from your company than you actually earn should stop at some point. And then the extra 5c should be paid. Well at some stage.

The other thing to put into the mix is that following the Penny and Hooper case there will be lots of structures where a trust owned the business. You know the last time small business didn’t pay the top marginal tax rate.

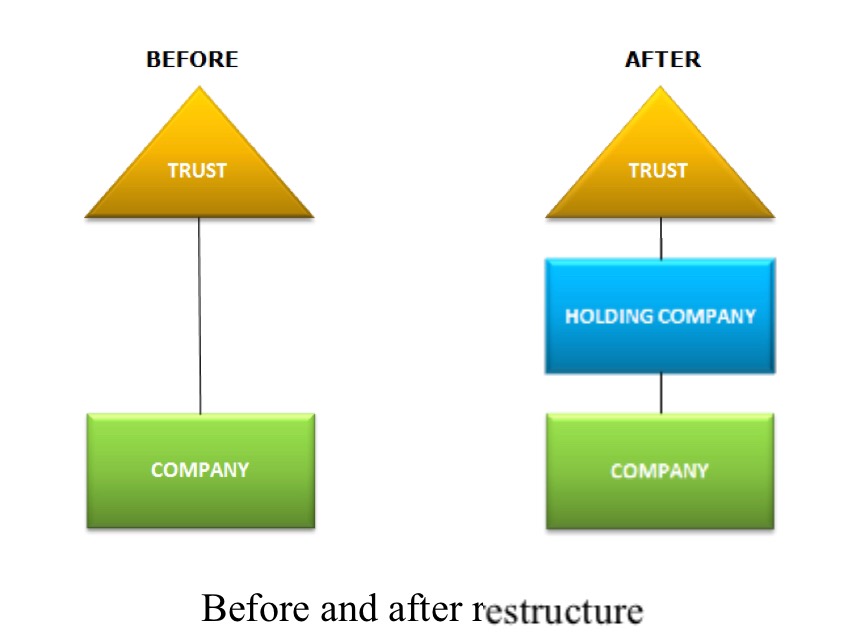

The Law Society paper outlined five ways for small business to not pay the top tax rate. But I am just going to take you through one that neatly springs from the Penny and Hooper structures.

So here we are: a small business owner or professional person with what they thought was a totes legit way of progressive tax scale not applying to them. They’ve paid the back taxes to IRD and yelled at their accountant. What to do now?

Step one Trust sets up a new company – Holding Company

Step two Trust sells its shares in company – Company – wot earns money to Holding Company for its market value. This is likely to be significantly above the value shown on Company’s accounts as Goodwill is not allowed in them.

Step three Trust lends money to Holding Company for purchase. For the accountants reading this is Dr Loan to Holding Company Cr Investment in Company.

Step four Company now pays dividends to Holding Company. And who would have thought -they are now tax free and an intercompany dividend.

Step five Holding Company makes loan repayments to Trust.

Step six Trust distributes to beneficiaries tax free.

Voila! Tax is only paid at the company tax rate. No more risk of extra 5c. And even more beautifully – if tax is not paid at the company level; nothing is paid at all. So good.

Now to be fair this isn’t a permanent tax scheme as only works until loan is repaid. But then maybe the company has further increased in value and can be done again?

But arguably as the ultimate capital gain could be paid out on liquidation – it is simply timing and I should calm the F down? Nah I don’t buy that either. It is structuring into a concession. And what is that called? Yes dear readers tax avoidance.

Now there are a few other things that are kinda interesting here too:

- Really only became an issue in 2010 when the company tax rate dropped to 28%. By the same government that reduced the top tax rate to 33% because they were concerned about avoidance of the top tax rate. You can’t make these things up.

- Discovered on Investigation. And given how hard this stuff is – taking a wild guess here – by people that Inland Revenue are currently cutting the pay of or making reapply for their jobs. Again can’t make this stuff up.

I can only hope that if we ever get more than a caretaker Minister of Revenue – whomever he or she is – they get onto this stat. Because what is now really clear is that for small businesses earning more than 70k – the top tax rate is optional.

James – you were right.

Andrea

Two bills one week

Let’s talk about tax.

Or more particularly let’s talk about the two tax bills that were introduced this week.

Some time last century dear readers your correspondent was a junior accountant for an oil company in the UK. And in that company was a low cost petrol retailer. Now one day in the early nineties all staff – yes even the accountants – were called into some marketing meeting. Purpose of meeting was to explain some new wizard marketing strategy that we could all sing and dance around.

But before that particular experience some faceless but well dressed consultant treated us to some research. It was on customer behaviour and why customers chose one petrol station over another. Riveting stuff. And have to say the monthly accounts I would normally be doing at this time were starting to look pretty good.

Now pretty much like every consultant presentation I have sat through before or since – the insights were off the scale. People chose our petrol stations because of: location; retail stuff and coz we were cheap. Genius. Worth every penny. So glad they got the specialists in for that.

But then they dropped an actual knowledge bomb on my 25 year old self. As well as the blindingly obvious stuff – there was an actual true story group of customers that used our stations just because we said we were low cost. And for this group it didn’t actually matter whether we were low cost or not. Saying it was enough. Twenty five year old mind blown. The facts didn’t matter.

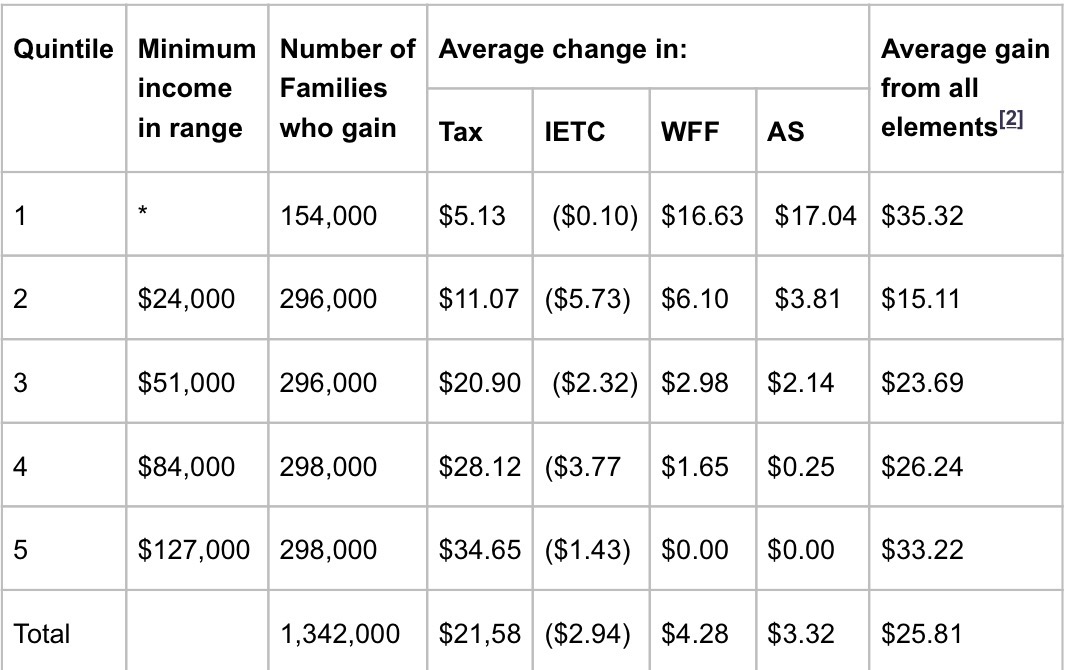

Now all of this came back to me this week with the Budget and the Family Incomes tax bill that was introduced and passed this week. A Budget that was for low and middle income families. Or as some commentators are dubbing it – a left wing budget.

Wow. Just wow. The facts still don’t matter.

Now it was Hon Steven’s big day out. Tax cuts for everyone!!! Just under 2 bill per year on tax cuts alone. And while there was other stuff. Vast bulk of the cost comes from tax cuts. Not entirely sure that this was what JustSpeak had in mind with its #billionbetterthings strap line but I guess tax cuts is preferable to any more bloody prisons.

And of course anything involving tax – even adjusting thresholds rather than rates – means more money goes to higher earners. It just does. It’s just what happens when you play around with tax stuff rather than transfer stuff. Coz higher income earners are the people who pay are the people who pay most of the income tax for individuals. So any cuts in income tax go to those who pay the income tax.

Oh and tax stuff applies to individuals not families. But I guess the clever Treasury people were able to turn this into a family costing below.

But then taking these lovely numbers and annualising them you get this:

Soooo families with incomes over $84k get half the dosh. Very progressive.

Even if those families didn’t actually want the princely sum of $35 per week and might have preferred it to go to mental health, or more state houses or more refugees. But at least it was only one new prison not three! #smallmercies.

But hey this is the party that has been elected. They can kinda do what they like. But a raid into Labour’s territory? Really? I guess if you say it often enough it must be true.

And then for comic relief was the political equivalent of a wardrobe malfunction. Hon Steven said that only one third of those eligible for IETC claimed it in a year rationalising its repeal. But then following questioning from the Michael Wood, Tim McIndoe kindly clarified that yes it was more 30% during the tax year and another 50% at the end of the year. Right ok. 80% not 30%.

And to be fair in the like actual Budget speech Hon Steven did say ‘during the tax year’. So not like actually lying. And in reality more likely a mix up in the bureaucracy than any intention to mislead.

But to your correspondent Budget 2017 – whole thing – deeply underwhelming. Just hope they didn’t also waste money on consultants as well.

Now ironically there was another tax bill that was also introduced last week that actually was a raid into Labour’s territory. Making everyone pay their fair share and all that. For top earners anyway. The Taxation (Annual Rates for 2017–18, Employment and Investment Income, and Remedial Matters) Bill. Just trips off the tongue. And on the whole it is a standard dull but worthy tax bill. Except for Employee Share Schemes. A well buried piece of social justice aka base maintenance.

Now the commentary and the previous discussion document are eye wateringly technical. Even your correspondent struggled. But buried in the RIS – para 54 – is the comment that it will raise $30 million a year. Now tiny in comparison to Steven’s big day out but quite a bit for a base maintenance item that deals with the taxation of remuneration. Especially since this is a net amount and there is an extension of a tax expenditure promoting widely offered share schemes. #workerparticipation.

Coz while yeah there are holes in the taxbase generally – all the remuneration stuff tends to be pretty water tight.

It all seems to have started life with a Revenue Alert that the department issued in late 2015. There they set out two wheezes that quite honestly could really only be used by important and well remunerated employees. People for whom the top tax rate is pretty much their average top rate. Coz honestly what employer could be bothered going to this amount of effort for ordinary employees.

Now currently the law pretty much says that if employees get shares then the difference between their value and what they pay for them is income. Makes sense.

But the Revenue Alert talks of a situation where:

- An employee buys shares on day one for market value. Awesome no taxable income there. No transfer of value. Alg.

- But they buy them with an interest free loan. Nah still cool. The value is in the interest free part and that is catered for by the Fringe Benefit Tax rules.

- Now there is a specific exclusion for interest free loans for employee share purchases. Mmm. Nah still ok. This is a specific concession and while it is an interest free loan – it is still a loan and needing repaying even if the shares go down. So yep still alg.

Except the wheeze is that the loan can be fully repaid by just handing the shares back. Ahh wot?

So if the shares go up – the difference is an untaxed capital gain but if they go down – nowt. Mmm no. Now the lovely Commissioner has quite correctly said – yeah nah – tax avoidance. And coz this is all connected to employment is looking to tax the gain as remuneration. Yep with you there Mrs Commissioner.

Now applying the tax avoidance provision all over the place is no way to run a tax system. So Hon Judith’s bill applies if you buy shares from your employer but you aren’t subject to the risk of them declining in value – aka not held ‘at risk’. In those situations when you get actual value from the transaction – that value is taxable. You know kinda like how when you are on a promise for a bonus – when that bonus actually materialises it is taxable? Yeah just like that here too.

Now yeah what ‘at risk’ means might not be super clear but tax avoidance audits aren’t super fun either. And as my late dear friend Tim Edgar would have said – just stay away from the edge. Everyone else pays tax on gains from their employer – so should the employees whose employers can be bothered to do clever stuff for them.

And this is what a socially progressive tax bill actually looks like. Hope it survives select committee.

Andrea

Fairness – Take two!

Let’s talk about tax.

Or more particularly let’s talk about tax and fairness.

On leaving the bureaucracy last year there were two issues that drove me absolutely mental and I wanted to put my energies into. The first was the rising prison population at a time of falling crime rates and the second was homelessness. Since then with the former I have become the policy coordinator for JustSpeak and a trustee for Yoga Education in Prisons Trust. For the latter – zip.

So with that in mind I went to a recent Labour Party thing on Housing stuff. But about mid way Phil Twyford said that the Labour Party in its first term of office was going to do a comprehensive review of the tax system to improve its fairness. Now I have heard them talk about this before – but comprehensive review. Wow.

Since then Andrew Little has said they aren’t putting up taxes. So maybe this means this working group will be ‘tax neutral’ in the way Bill English’s was?

Now on the basis that this isn’t simply code for a capital gains tax, I thought I’d do a bit of a scan as to what this could mean in practice. My focus will be on the revenue positive items as the tax community will have their own laundry list of revenue negative ‘unfairnesses’ they will want fixing.

But first I am going to get over myself. Yes fairness could mean a poll tax but when the Left talks about tax and fairness it is implicitly a combination of horizonal and vertical equity. Horizontal equity where all income is taxed the same way and Vertical equity where tax rises in proportion to income.

Alternatively tax and fairness to the Left can also mean using the tax system to remove or reduce structural inequities in the economy and not just in the tax system itself. So here we go:

Untaxed income

Capital income

Now the most obvi unfair thing is the way capital income is taxed more lightly than labour income. Always loved Andrew Little’s comment about the average Auckland house earning more than the average Auckland worker. Dunno why he doesn’t use it more.

Now the lighter taxation might be there for some good reasons including:

- Long periods before it is realised. Is it fair to tax people when don’t have cash to pay the tax?

- Valuation issues. Although this goes once move to realisation based taxes.

- International norm. Soz unfortunately everyone taxes capital more lightly – sigh.

- Lock in effect. If have to pay tax would you ever sell?

- Incentive for entrepreneurship which is a good thing apparently.

Oh and not being able to get elected.

Options include a realised capital gains tax or Gareth’s wealth taxation thing. Both have issues but both would be an improvement if fairness or horizontal equity is your thing.

Imputed rents

Alongside the not taxing capital gains is that we don’t tax imputed rents. Remember how owning your own home is effectively paying non-deductible rent to yourself and earning taxable rent? Except the value of the rent is not taxed? Awesome. But its non-taxation also offends the horizontal equity thing – even if it is your house – and so is unfair.

Active income of controlled foreign companies

New Zealand companies that earn foreign business income in their own names are taxed. New Zealand companies that earn foreign income through a foreign company aren’t. Why? International norm. Not fair but everyone else does that too. Also brought in by Michael Cullen. Nuff said.

Capital or wealth taxation

While Gareth’s thing is potentially wealth taxation it really is taxation of an imputed or deemed return on wealth rather than a tax on wealth per se. Actually taxing capital or wealth is where inheritance or gift duties come in.

Now neither of them are actually income taxes. They are outright taxes on capital. And if that capital arose from taxed income then would be very unfair to tax. However not entirely sure that is the case and these taxes are relatively painless as they tax windfalls; don’t effect behaviour and only apply to the well off. So they potentially promote fairness from a ‘reducing inequality’ sense rather than a horizontal or vertical equity sense.

Deductions

There are a few things here. There are all the issues with interest and capital gains but they reduce if you ever tax capital gains or do Gareth’s thing. Others include:

- Borrowing for PIE investment can get deductions at 33% while PIE income is taxed at 28%

Donations tax credit

Now this isn’t an obvious one as everyone can get a third back of their donations up to their total taxable income. So that is pretty fair. But the more taxable income you have the more subsidy you get. And it can go to a decile 10 school; your own personal charity or a church with an interesting back story. But dude – seriously – who can afford to give away all their taxable income? Perhaps worth a little look.

Labour income

Withholding taxes

Labour income that is earned as an employee is subject to PAYE and no deductions are allowed. Labour income that is earned as a contractor is only sometimes subject to withholding taxes and deductions are allowed. Aside from deductions which are likely to be pretty minimal with most employee type jobs – there is an evasion risk when people become responsible for their own tax. Spesh when such people are on very low incomes. Whole bunch of other ‘fairness’ issues too like access to employment law; but this is just a tax post.

Personal companies

Labour – and any income – can also be earned through a company. And a company is only taxed at 28% while the top rate is 33%. So if you don’t need all that income to live off you can decide how much stays in the company and how much you pay yourself. Is that fair?

Other things

Now of course there is always the old staple – increasing the top marginal tax rate. And yes that does enhance vertical equity but it also causes other problems elsewhere. So if you are going to make the system more misaligned please make sure that it doesn’t become the backdrop for widespread income shifting as it did last time.

Oh and secondary tax. Now there are many things that are unfair including precarious work and over taxation. Not sure secondary tax is one of them. While you have a progressive tax scale and multiple income sources – you get secondary tax. It appears that under BT – page 22 – the edges can be taken off getting a special tax code which should help but secondary tax in some form is structurely here to stay.

Look forward to it all playing out.

Andrea

The Spike

Let’s talk about (the recent Greens’ press statement on) tax.

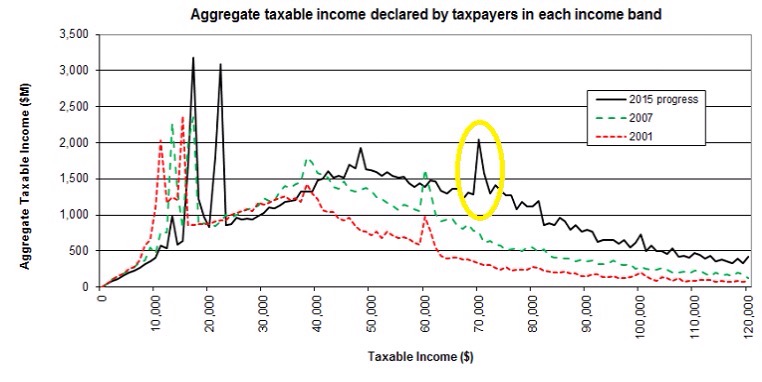

Recent data has shown there is a spike around $70,000 of reported taxable income for individuals – convienently the point where the top marginal tax rate of 33% starts. And according to the Greens this shows evidence of tax avoidance by rich people which can be fixed by – among other things – increasing Inland Revenue’s investigation budget. Mmm maybe.

Before I go on, I am working on the assumption that when the Greens talk about tax avoidance it is in the colloquial ‘not paying as much tax as I think you should’ kinda way rather than tax avoidance according to the actual law. All cool but unfortunately (or fortunately) the department is constrained by what Parliament has enacted and how the Courts have interpreted it.

Now in the mid 2000s – it is true – similar spikes were evidence of widespread tax avoidance among self-employed professionals. The wheeze was that they were employed by trusts which were taxed at 33% on the income the individuals earned – not the top individual’s rate of 39%. And then the trust paid the individuals a below market salary for their services to the trust.

Only the below market salary was taxed at 39% and the rest of the income at the lower trust rate. And then any tax paid income of the trust could then be distributed tax free to beneficiaries. Too easy and too good to be true. Hence tax avoidance according to the actual law.

Moving to 2017. The trust and top personal rate are the same so that particular wheeze won’t work. But now we just have misalignment between the company rate at 28% and the top personal rate of 33%.

Except that under a misalignment with the company rate there is no distributing the income tax free. When income is distributed from the company to the shareholder – a dividend – it is subject to another 5% tax. Now any ‘tax avoidance’ – in theory anyway – is just timing until the shareholder needs the money. There should be no ultimate reduction in tax. Although timing advantages can be a big deal and can also make something tax avoidance under the actual law.

But the only way I can see of moving this from tax avoidance – not paying as much tax as I think you should – to tax avoidance under the actual law is if the department can show that the $70k is not a market salary – as they did with the self employed professionals.

And while that wasn’t simple for the department last time – now all tax advisors know about the need for a market salary – possibly from painful personal experience. So anyone giving advice that $70k is an acceptable salary – when the market rate is higher – does so knowing it could be attacked by the department and will have all the supporting arguments ready.

But the Greens are right the spike is still there. Last time the spike was widespread tax avoidance according to the actual law – so why wouldn’t it be this time too? Not the first time I have lacked imagination.

Just in case tho I am right – I am also all about the solutions. And there is at least one way of getting rid of the spike without increasing anyone’s budget. Think of all that extra money Greens you could spend on cleaning up the rivers instead of tax inspectors.

One way is to increase the company tax rate to the top marginal rate.

Another way is to make the look-through company (LTC) rules compulsory.

Currently any company with five or fewer shareholders can choose not to be taxed as a company. Instead income and losses are taxed as if the shareholders had earned the money themselves. Except currently those rules are optional. Make them compulsory and the spike goes. No more income in more lowly taxed closely held companies as no more closely held companies for tax purposes. Simple.

And the really good news for the Greens is that there is currently a bill in the House making changes to the LTC rules; so a Supplementary Order Paper doing just that would be totes in scope. Oh and it is an ‘annual rates’ bill too so they could also have a go at the company tax rate at the same time. Awesome.

Now lots of people who haven’t made an LTC election may not like that and say so quite loudly. Coz that’s what you get when you are strong on policing tax avoidance – lots of upset people all with lots of incentive to write to you and come and tell you how upset they are.

But unless the current law with closely held companies – or company tax rate – changes I can’t see any level of increased funding will get rid of that nasty spike.

Namaste.

Extra fox

Let’s talk about tax.

Or more particularly let’s talk about secondary tax.

Early on in my mothering life as a good middle class parent your correspondent – or probs a family member as I was pretty much exhausted for the first couple of years with each baby – bought Dr Seuss’ ABC.

Aunt Abigail’s Alligator A – A – A

All the letters had rhymes with words that started with the ‘profiled’ letter. The exception – pun coming – was the letter X. Because I guess xylophone and xenophophia were outside the target range for preschoolers – the rhyme became X is very useful for words like ax (with no fricken e) and extra fox.

Now while I was still 5 plus years away from discovering tax, Mr your correpondent and I always read that as extra tax. Coz I mean what is an extra fox for goodness sake? Aunt Abigail’s Alligator now that makes sense but – Dude really – an extra fox? What’s that about?

Now amonst the Precariat secondary tax is very much considered to be an extra tax. And according to the Council of Trade Unions the Labour party has promised – as they did last election – to repeal it on coming to government.

Thing is they haven’t actually promised that. They have said in the detail of recommendation S8 that the Government as part of Inland Revenue’s business transformation should look to remove secondary tax. These are subtle but important distinctions which we will come back to. Lucky for them Labour actually has someone on their team that gets tax.

So what is secondary tax?

Well it is the tax deducted on second jobs. It is a function of having the progressive tax scale that the left loves so much.

First jobs get code M which I guess stands for main job. It takes the pay and multiplies it by the number of pay periods to get an annual amount ; calculates the tax and then divides that by the number of pay periods to get the tax for the income in the period. While it is relatively simple it does mean those with lumpy pays – overtime; seasonal workers – are overtaxed as a high pay is assumed to be a high annual income.

Second jobs however people have to choose a flat rate – secondary tax – based on how much they earn from other jobs. And there is a view – clearly shared by the CTU – that this overtaxes their income. Now it is true that it taxes second jobs more than first jobs but this is really just to reflect that extra income means higher tax.

Coz remember how progressive taxation means the more income you earn the proportionally greater tax you pay? Yeah well this is how it is implemented for those with second jobs und the current PAYE system.

Now I fully get that as it is a flat rate and if you don’t earn as much as you thought you will be over taxed. But that is a function of our PAYE system being inherently middle class. As it works beautifully for those on stable incomes ie salaries.

Everyone else with unstable incomes – even if it is only from one job – runs the risk of being overtaxed and then yes needing the claim a refund. And then yes if you go to those refund companies they’ll take a cut. There is an IRD option but they don’t have the marketing budget of the refund firms so it is less well known.

The real issue though is the changing face of employment and precarious work – something the Labour Party is at least acknowledging and trying to address. Yeah I am not sure about the training levy either – but at least they are trying.

So yeah trying to get BT to address lumpy incomes is a good idea. So good that Hon Mike may have his officials on it already.

Just repealing secondary tax though is a really dumb idea.

Unless you are happy with undertaxation and people needing to file and/or becoming non-compliant with all the associated risks. Alternatively it is an argument for widening the bottom bands. But rich people will get that benefit too. So Labour Party – trying to get technology to solve it is the right direction.

Real issue though is the numbers outside the withholding systems coz they’re not employees.

Namaste

Everything is connected to everything else

Let’s talk about tax.

Or more particularly let’s talk about about a case I mentioned last week in the alignment post. It was quite controversial at the time within the tax community and did leak out a bit into the general public. As is often the ‘case’ tax is just an overlay on other interesting stuff.

Also thought of it again wot with the junior doctors strike and how the consultants would be helping over that period. I guess coz its Health that means its not strike breaking?

Anyway back to the case. Penny and Hooper (last names) were both specialist doctors earning shed loads of cash in Christchurch fixing the bung knees of those who were in denial about the length of their running careers and had yet to find yoga.

Now these gentlemen were unremarkable in that they weren’t big on paying tax according to the progressive tax scales that applied to little people and so adopted a structure recommended by their accountant. I mean everyone was doing it and what could possibly go wrong. In fact even John Shewan – of Shewan report fame – said it was bog standard behaviour.

The wheeze was that they put their businesses into a trust which at that time had a lower tax rate (33%) than the little people faced who earned over $60,000 ( threshold increased at some point but detail not relevant) 39%.

The Commissioner who was a he at the time – yes Virginia men can be senior public servants – was not best pleased. He used a bunch of words like ‘tax avoidance’,’market salary’ and ‘not’and made them pay tax like the little people. Go Team Commissioner.

The tax community also used a bunch of words like ’emmently foreseeable’; ‘lack of certainty’; and ‘chilling effect on investment’. Well maybe not the last set but that is never far away when the big people are being made to pay tax.

Anyway the Commissioner won; tax accountants lost; largely graciously ate that and everyone moved on to the next tax dept v tax community stousch.

There was some commentary at the time about how this was more than a tax case – at which point I got very excited – only to find it was about trusts could be looked through and weren’t as inviolable as people thought.

But what was never discussed was how two men who were educated at the state’s expense presumably before student loans; weren’t bonded; and whose business was almost wholly paid for by the taxpayer via ACC were earning so much money. I guess it was before the days of ‘joined up government’.

I also guess Labour’s ‘three years free’ policy will also remove what little royalty we currently get from the taxpayers’ investment in such lovely people.

All the more reason then guys to make sure misalignment works and they do actually pay the top tax rate.

Namaste

‘But I’m a director of a land-owning company!’

Let’s talk about tax.

Or more particularly let’s talk about tax; interest deductions and private expenditure in companies.

Your correspondent has returned from her ‘retirement cruise’; is recovering from jetlag and has returned to what passes for work these days. That will dear readers include a return to twice weekly posting. As a change from some of the more political posts I thought I’d return to a technical issue for a bit of light relief.

Earlier this year while I was still inside I went to a dinner party in a provincial city. At the party was a delightful gentleman I had met previously and was more than pleased to see again. The feeling appeared to be mutual and our conversation broadly went like this:

DG – Now Andrea tell me – which is better? To pay my mortgage or to pay my tax?

Me – cough, splutter, mumble – well the thing is it isn’t a choice as tax is a legal obligation.

DG- oh don’t be silly of course I know that. What I mean is it better to have a mortgage on my house get the tax deductions and then have money to invest in shares and things for capital gains or have no mortgage not get the tax deductions but have more disposable income?

Me – Ah what makes you think you get a tax deduction for the mortgage on your house?

DG- This is the country – we get tax deductions for all sorts of things and besides I’m the director of a land owning company!

Me – Is that wine over there?

Now dear readers I am sure after Zen and the art of tax compliance you all know that to get tax deductions the expenditure has to be:

- Connected to the earning of income or in the ordinary course of a business and

- not private or domestic expenditure.

So therefore if DG owns his house in his own name – or in a family trust – as neither 1) or 2) is met there is no deduction for interest expenditure.

There is the possibility that if the money were borrowed on his house and used to buy shares THAT WERE DIVIDEND PAYING then the interest would be deductible. But if the money is borrowed to construct the house for him to live in – nuh.

The complication though is the comment about being a director of a land owning company. The rules above do not apply to a company and interest deductions. From about 2000 or so the rule broadly became:

- Are you a company resident in New Zealand?

- Have you incurred an interest expense?

If yes to both, then ‘would you like interest deductions with that?’

The private and domestic test still applies to such expenditure but I have always struggled to align any concept of private and domestic to a company.

So at first pass – yep – if DG holds his house in a company – in your correspondent’s view – he will get an interest deduction.

And yeah the Mixed Use Asset rules won’t apply here because ironically it isn’t a mixed use asset – it is wholly private and domestic.

But – not so fast – the music hasn’t stopped.

While there are special rules for companies and interest deductions there are also special (dividend) rules for transactions involving companies and shareholders aka ‘are policy makers really that dumb?’

These dividend rules say where ever there has been a transfer of value from a company to a shareholder there is a taxable dividend to the shareholder to the extent of the value transfer.

Ok again in English.

If a company gives a shareholder stuff – goods or services – that is a taxable dividend for the shareholder. Here the company has given the shareholder use of a house – so the shareholder DG – gets a taxable dividend.

And by ‘taxable dividend’ yes this means you need to put that value on your tax return and pay tax on it. And yes I know you didn’t get any actual cash but that doesn’t matter. You know how when you tick the box for dividend reinvestment on your publicly listed shares – you know how the dividend is still taxable even though you didn’t get any actual cash. Consider this as the same.

So what is the value that DG has received from the ‘land owning’ company? He has received the benefit of living in that house. And what do people usually pay for the benefit of living in a house they don’t own? You’re onto it – rent.

DG is then up for tax on the value of the rent not paid to the company as a dividend. And once more with feeling – it doesn’t matter that no cash has been paid from the company to the shareholder.

So the benefit DG received – use of the house without paying rent – is taxable to DG.

Now if DG has a tax rate of 33% – as the company tax rate is 28% – there will be a net 5% tax paid on the ‘imputed’ or deemed rent. That is he pays tax at 33% on the deemed rent and the company gets a deduction at 28% on the interest expense. In other words a gift to the people of New Zealand and how tax planning can go wrong. And if he didn’t know this was the case until my former colleagues come along – it will be 33% tax plus interest at about 8% plus a penalty of between 10% and 100%.

Awesome. Can only hope he didn’t also pay an agent for this wizard advice.

If his tax rate though is lower than the company rate this is where it could get really interesting. Technically even with DG putting the value of rent on his tax return there will still be a net tax deduction that ostensibly can be offset against other income.

In this case though the structure – or ‘arrangement’ as my former colleagues may start to call it – is really putting pressure on the whole ‘companies can’t have private expenditure’ thing. And from here we move into a complete world of pain – or ‘good case’ depending on which side you are on this – known as tax avoidance. Now the entire interest deduction is at risk with tax avoidance penalties of between 50% and 100%. Fun huh.

And don’t even think of paying rent to your company and making it a look through company so you get the deductions directly against your other income. The department was very clear with look through companies – the prequel – that this was tax avoidance too.

So DG I am not sure there really is any ‘country immunity’ for interest on your personal mortgage. Pay it but step away from the tax system. There be dragons.

Namaste