Other capital taxes – what are the options?

Last Thursday I had the very great pleasure of talking about tax to smart young people – here and here – at the Social Change Collective alongside Marjan van den Belt and Max Rashbrooke.

One of the questions was if not CGT and we wanted to tax capital more – what are the options? Answered it on the night but as the sharing individual I am I thought I’d do it for you all too.

This version might even be more coherent. Fingers crossed.

To me the options seem to be:

- Net equity tax or risk free rate of return method (rfrm)

- Wealth tax

- Alternative minimum tax

- Land tax

Net equity tax / risk free rate of return method

Susan St John is proposing the net equity tax – or risk free rate of return method for residential property.

This means a notional rate comparable to that a risk free rate of return – say 5 year bank term deposit – is applied to the equity held in residential property. This amount then becomes the income that is subject to tax.

For example if a property has a value of $1million – land $800k building $200k – but has a mortgage of $600k – it has net equity of $400k.

If a rate of return of say 3% is applied to the equity of $400k this will generate taxable income of $12,000. This $12k would then be taxed at the tax rate that applies to that particular taxpayer. Say 33% if top rate individual or trust. 28% if a company.

This $12k would replace any existing taxable income from that asset. That is rent would no longer be taxable and so there would be no associated deductions allowed.

As Susan is only proposing that it apply to residential property there would be no particular problems with getting a valuation to work out ‘net equity’ as land is regularly valued.

There could be issues if the debt that is attached to a property funded other investments and not the property itself. However there are lots of issues with debt and how it is allocated generally – I don’t think that is a deal breaker here.

There are also the issues that I raised in my comments on the officials note. For landlords who are currently charging below market rent this may incentivise rent increases. It may also further disincentivise landlords maintaining their properties as there is no tax benefit for doing so.

However that is more the place of regulation rather than tax.

Interim conclusion: Some technical issues with debt allocation and possible adverse behavioural effects by landlords but quite doable. No issues with valuation.

Wealth tax

Max Rashbrooke is proposing a wealth tax on all wealth.

An annual tax of a small percentage of the value of wealth held. As per the previous example – assuming no other wealth was held by the taxpayer – a small percentage – say 1/2% would apply to the $400k and an extra $2000 wealth tax would be payable on top of any other existing taxation.

Unlike net equity tax, this is not a proxy or an alternative calculation of taxable income for income tax to apply to. It is an additional tax on a different base in the same way GST is.

And just like GST it is a form of double tax. Consumption – and GST – is made from tax paid income. That is the same income is taxed twice. It is a feature. The beauty of GST is can also ensure one level of tax is paid when income wasn’t taxed in first place. Say if an untaxed capital gain.

Wealth taxes are similar. If tax has been paid at every level we would get:

For some asset classes such as bank deposits – or possibly foreign shares – this is absolutely the deal as there is no part of the income that is untaxed. In those cases wealth tax seems a bit like over kill/taxation.

For other classes such as shares, investment in small businesses and unleveraged residential rental property where some part of the return is taxed but there is still an element of untaxed capital gain – depending on the rate of tax – a wealth tax absolutely has merit.

For serial entrepreneurship or land banking where the whole return is a capital gain – in a world without the capital gain taxed – this is an absolutely bang on approach.

Assuming this can be got through – maybe with different rates for different types of wealth although that will then bring in issues of debt allocation – the most significant issue will be that of valuation.

This is particularly the case with valuing goodwill in unlisted businesses. To have to value every year would make the valuation industry very rich.

Now I know it is possible for the tax administration to come up with some rules of thumb but having been upclose and personal in the Michael Cullen/Troy Bowker spat on exactly this issue – it is definitely a practical thing that will slow this option down.

Interim conclusion: Need to clarify conceptual basis for including asset classes already fully taxed. Valuation issues likely to be a significant hurdle in practice. But could work.

Alternative minimum tax

Geoff Simmons and TOP are proposing an alternative minimum tax on all wealth. A bit like Susan’s proposal but instead of the rate being applied to residential property it would apply to all the wealth of a taxpayer.

But unlike Susan’s option, instead of the rfrm number becoming the taxable income figure it would be compared to the taxable income that arises under the current tax rules. Tax would then be payable on the higher of the two numbers.

So in our example above if the property was the only source of wealth and currently returned no taxable income, then the $12,000 would be taxed at whatever the appropriate tax scale is.

However by including all wealth this option suffers from the same valuation issues as a wealth tax.

But because it calculates an alternative minimum income level, rather than an additional or alternative tax, there is no issue of double or triple taxation. Its aim is to simply ensure the income that level of wealth should (or is on an imputed basis) be generating is subject to tax at normal rates.

Interim conclusion: Conceptually the most coherent of all the options but significant issues with valuation. Could work though.

Land tax

This would involve an annual tax of a small percentage of the value of land held. Like a wealth tax it would be a separate and additional tax but unlike a wealth tax it is levied on the value of the land – in this case $800k – with no reference to the debt borrowed to purchase it.

By focussing on land it doesn’t have the valuation issues that a wealth tax or an alternative minimum tax does. Also there are no issues with allocating debt.

It does, however, seem arbitrary to pick on one asset class only. But as this is the asset class that is currently undertaxed by reference to the level of capital gains earned (1)- such an argument doesn’t stress me.

It is, though, the current tax base of local authorities so if central government were to move into their tax base, local authorities’ arguments for a portion of GST could become more compelling.

Interim conclusion: Conceptually the least coherent of all the options. Minimal practical issues. Could definitely work.

The key difference between all these options is that a land or wealth tax is an additional tax separate to income tax. Net equity or alternative minimum taxes, however, are still within the income tax system but trying to get a better measure of taxable income than the status quo.

But they have many more things in common.

Similarities between the options

Thresholds

I think all options will need some form of threshold before they apply. No one – thank goodness – is keen on a family home exclusion. But all have additional complexity and compliance cost so something like $500k threshold for an individual could take out personal assets including a home (and maybe KiwiSaver) for most people. This would then mean the taxes could focus on the top end of the income and/or wealth scale.

May not have cash to pay the tax

None of these options are realisation based. That is they apply irrespective of whether any cash – or income other than imputed income – has been generated from the assets or wealth. Now I know that Susan St John explicitly doesn’t care about that as she feels then the property should be sold if that is a problem for the owner. I am guessing that is also the view of TOP as it is only cash poor pensioners that can get any deferral.

I get why economists might not care about this and/or see it as a design feature to encourage more efficient use of assets but not sure that is how the general public would see it. Even with a threshold.

As an example the Tax Working Group only considered rfrm on residential rental properties as it was only that group that would have the cash to pay it.

Impact on Māori collectively owned assets

Māori currently own a tiny fraction of the land they did at the time of the signing of Te Tiriti. And the settlements they have received were only 2% or so of the value they lost through crown action. (2)

Now the deal with the settlements was that they were to be full and final and that there are no special tax rules. But any tax isn’t linked to cash income earned and targets their assets or wealth, even if not the basis of a potential contemporary Waitangi Tribunal case, will be considered more bad faith action from the Crown.

As a woke Wellington snowflake I would have no problem exempting assets held collectively under a Māori Authority. Not for tax policy reasons but as a way of preventing further injustice. But as the equivalent noise showed with capital gains, this would not be a universal view.

Would raise shed loads of money

Rfrm on residential rental property only was found to raise a $1 billion (3) a year more than the current taxation of residential rental property. This was even when the extension of the brightline test to 5 years and loss ringfencing was allowed for. That was with a rate of 3.5% which was the 5 year bank term deposit rate at the time of the report.

$1 billion. Every year.

Let that sink in.

Final conclusion on all options

So all options even with quite modest rates could raise seriously useful dosh for the Government.

But this money wouldn’t come from thin air. Like capital gains it comes from people of means. A section of whom – much like with capital gains – are well organised, connected and resourced.

So I am not holding my breath for any of these being adopted by a major party any time soon. No matter their merit.

Andrea

(1) Paragraph 60.

(2) For readers interested in more background. Here is the officials paper on the subject for TWG and here is mine as I didn’t feel officials went far enough.

(3) Paragraph 41

The other Boleyn girl

Since coming back from hols your correspondent has been struggling with an annoying cold. That bad side is that my yoga practice has suffered. Good side is that I have had greater opportunity to sample the ever expanding Netflix menu.

So for comedy I can recommend Santa Clarita Diet, Huge in France and Derry Girls. For documentaries I can recommend Bobby Sands 66 Days, Black Panthers and Period. End of sentence. Oh and Knock Down The House of course. Obvi.

Now for reasons that are beyond me – although constant checking for the next season of The Crown may have had a minor effect – Netflix is recommending The Other Boleyn Girl to me. A book I read many years ago while stuck in an airport but not one I want to watch immediately after a documentary on IRA hunger strikers.

AI still has a way to go.

Anyway the story is that there was apparently an older Boleyn sister that Henry was keen on before he was keen on Anne. And she was probably better coz she loved him much more but is now like super obscure – or possibly completely fictional – and so like it all could have been so different.

Now in CGT land there is also another Boleyn girl. Leading up to the finalisation of the report one of the members – Robin Oliver – put together a sketch of an alternative way of taxing more capital gains.

It has the pithy title of Robin Oliver: Taxing Share Gains but not Gains Made by Companies: Member Note for Session 24 of the Tax Working Group. It also got the slightly more pithy title in the media of CGT Light.

And yes I know there won’t be anymore taxation of capital gains but acceptance is a process and, as a relational being , I am (over) sharing.

So off we go!

Now I am sure you all know dear readers the final design was one of:

- Gains taxed from valuation day

- Loss ringfencing in ‘transition’ period but limited constraints thereafter

- Applying to most – currently untaxed – assets

- Limited rollover relief when buying other assets

- No change to existing rules for debt or foreign shares

And the associated issues with this were:

- Difficulties with valuing hard to value assets like goodwill particularly when only part of a business is sold off

- Revenue risk in downturns

- Incentivising ownership of foreign shares over New Zealand shares

- Lock in

- Complex rules to prevent double deductions within corporate groups

- Troy Bowker getting upset a lot.

Now there were possible ways of reducing all those issues – except maybe the last one. But Robin had a go at looking at it all a bit differently while still ultimately taxing more capital gains on a realised basis.

In particular he suggested:

- Taxation of gains on residential property – valuation method as per final report

- Possible taxation of other land but with extensive rollover provisions

- Inclusion of depreciable property – although in practice this just means losses and/or depreciation would return for buildings that fall in value with gains taxed if rise in value. Maybe software would also be affected but most depreciable assets already get deductions for their decline in value.

So far not that much different to the final report. However there were four key differences:

- No increased taxation of capital gains – other than above – at company level

- Shareholder of listed companies taxed on gains on sale from a valuation day

- Shareholder of unlisted widely held companies taxed on gains on sale. Existing holdings grandparented

- Shareholder of closely held company taxed on gains on assets sold by company. Existing goodwill of companies grandparented.

In some ways this option was lighter than that of the final report:

- Existing holdings of widely held unlisted companies would be outside the tax but they would also be outside the complexities of valuation, the median rule and loss ringfencing.

- Existing goodwill of closely held companies would also be outside the tax but also outside the complexities of valuation, and the median rule.

Now while the grandparenting thing seems like a big gift, it would have been less than Australia did coz they grandparented – didn’t apply the tax to – all existing assets and now 30 years later Australia collect lots of money (1). And yeah it would have been less money to play with in the immediate period but a whole lot more money than is the case now.

The non-taxation of assets in widely held companies would give a timing advantage to shareholders as tax wouldn’t be paid until the shareholders sold their shares. But it would mean that such groups wouldn’t have the compliance cost of the double deduction rules. And the Government wouldn’t have the risk that those rules didn’t actually work all that well and lose lots of money in the process. Coz it’s not like that has never happened before.

But in other ways Robin’s option was actually tougher. Shareholders of closely held companies would be paying tax on any capital gain earned by the company – at their marginal tax rate. So if that was 33% they would pay tax at 33% not the company rate of 28%.

Robin prepared all this as a possible option for Ministers and the Working Group made it very clear that the choices were not binary and the hard stuff was in the active business area. So it could have been worked up by officials as an option in any discussion document – even if they weren’t wild about it at the time. (3)

The Government might even have grandparented all existing assets as Australia did and take away all the noise. And yeah it would take a while to build up but after 10 years or so (4) – serious money.

But it was not to be. And in the end all possibilities went the way of the real Boleyn girls.

Thanks for listening.

Andrea

(1) Page 28

(2) Paragraphs 11-13

(3) Robin’s response to officials comments

(4) Figure 3.10

An alternative progressive tax policy

Your correspondent is having a lovely Friday. Thanks for asking.

Started the day chatting to Terry Baucher on tax stuff and then Wellington is having one of its beautiful days.

Had lunch with a friend setting the world to rights which included me riffing on what a progressive tax policy could look like that was a bit radical but not completely nuts.

I have very tolerant friends.

Anyway given the relational being that I am – I thought I’d share it with you.

It starts from a place of Jacinda saying that while a CGT is off the table – nothing else is. And having spent the last 16 months or so thinking about tax stuff from a heavily constrained perspective – it is all a bit exciting to get off the leash.

So it goes!

Inheritance tax

This would apply to all estates over a (tbd) threshold. It has the advantage of involving one of life’s certainties so wouldn’t be affecting behaviour at all. Now it might mean people pass on assets before they die and they might use trusts to avoid it.

The former strikes me as a collateral benefit of the tax and the latter would need to involve rules involving death of settlors and/or beneficiaries. Next.

Closely held companies

They would become taxed at the top marginal tax rate to stop all the $70k and overdrawn current account stuff. There would be the option though of the look through company rules applying when incomes of shareholders are actually below $70k.

Very small companies

Consistent with a submission from Chartered Accountants of Australia and New Zealand (1) very small companies – tbd – would be taxed on turnover. Yes there are issues with it but it would reduce compliance costs for them and stop the revenue risk of oh gosh how did that personal expenditure get into my tax return.

Property ownership

The CPAG submission of a net equity tax would apply here. Yes it is similar to the TOP proposal but has the advantage of only applying to property so none of the valuation issues. Also I am not too stressed about partial family home exemptions so the types thresholds Susan St John proposes seem very pragmatic.

Personal tax thresholds

Any money collected – and quite frankly there may not be any when your focus is fairness rather than revenue raising – would go into raising the bottom threshold as per the TWG proposal.

Then either this could flow through to everyone or get clawed back by raising the tax rate for the next threshold. Also a possibility raised by the TWG.

Options not considered

Raising the top personal tax rate

Now I know this is a darling of the left and I accept I could be heavily coloured by having paid the higher rate for many years. But here’s the thing:

It is taxing the top income earners who are already in the tax system paying tax on their income. It doesn’t touch income that isn’t taxed already in a way a number of the measures above do.

Also the mismatch thing between different entities is a nightmare and to do properly would involve also an increase in the trust rate or face the use of trusts that were prolific previously.

There is already an issue with a mismatch between the company rate and top personal rate which I am hoping the proposal for closely held companies would fix.

Lowering the GST rate

Now I get that GST is regressive. Totes. No argument. But as rich people spend more in absolute terms, they pay more GST in absolute terms. And if they are not paying income tax for whatever reason – if they want to eat they have to pay GST.

So can’t recommend this I’m afraid.

However also not a fan of raising it either. See comment on regressivity.

Anyway that’s enough from me.

So would this all make the tax system fairer. Totes. Could anyone get elected on this? No idea. Well beyond my skill set.

Enjoy your weekend.

Andrea

(1) Pages 28-29

Taxing more capital gains

Now your correspondent loves a good paraphrase as much as the next socially progressive tax commentator. And so she had been largely unstressed about the use of the term capital gains tax by Jacinda on Wednesday or in any of the previous or subsequent discussion.

A comms device. Alg. Important to focus on the substance of the announcement rather than any technical nit picking.

But now I am not so sure.

Indulge me a minute. Call it background if you will.

Now what the Tax Working Group actually recommended was that more capital gains should be taxed. The majority – and me – thought a more comprehensive approach was best while the minority thought only gains on sales of residential rental should be taxed.

And the reason it was framed like that was because the tax system already taxes a number of capital gains: financial arrangements, certain types of land sales, leasehold improvements, employee share options and (sort of) returns from foreign shares.

It is true that by value lots are either excluded or administratively unenforceable. Looking at you assets purchased with the intention of resale.

But all the discussion was on extending income taxation to different asset classes that generated untaxed capital gains – rather a capital gains tax per se.

And here is why it matters.

While we don’t have a capital gains tax – over time, or incrementally as the minority put it, – successive governments have deemed specific capital gains to be taxable income when it is clear that untaxed gains are being substituted for taxable income. It has been the safety valve for the lack of a formal capital gains tax. And all done without any fanfare.

So it was with a degree of surprise upon watching Jenée Tibshraeny’s excellent interview of the Minister of Finance, I heard him say that an extension of the bright line test was unlikely because it would be too much like a capital gains tax.

Sorry?

Now I am really hoping that what he meant was: it is unlikely because there isn’t much substituting taxable income for capital gain with residential property. Rather than it is unlikely because any capital gain that is now untaxed will not be taxed while Jacinda is PM.

Because that would be a step backwards in terms of tax policy and make me properly sad.

So now really looking forward to that new tax work programme.

Andrea

The next day

Ok yes I am disappointed.

But probably no more or less than the members of the 2001 and 2008 tax reviews who also recommended greater taxation of capital. So it was always on the cards.

And to be fair the New Zealand tax system has never had a formal capital gains tax but has been taxing capital gains since whenever. All by deeming them to be taxable income.

IMHO this really hasn’t been the end of the world from a social cohesion point of view until that is – land prices went insane and somehow my generation extracted value from our children.

Now yes it would be awesome to tax that value extract – but what would be more awesome would be land prices falling. Coz something has gone gobsmackingly wrong when yopros need government intervention to buy their first home.

But back to tax.

Personally though I am surprised there wasn’t something. After all even the minority felt their was a very strong case to tax gains from residential rental and for those who were worried about valuation issues there was always the CGT lite option aka grandparenting.

But this is not to be.

So what is happening? Possible vacant land tax, cracking down of speculators and tax dodgers.

The former I am quite comfortable with as I think it has merit as a corrective tax. Needs to be better than Australia though. And yes local government is the best placed for that. Maybe a targetted rate or something.

Cracking down on speculators. Right.

Now there is the small matter of the brightline test which taxes sales within 5 years which – I would have thought – well included any speculation period.

And then there is the existing provision since whenever – bought with the intention of resale – which didn’t work very well so the Nats brought in the brightline test.

Unfortunately though compliance with these rules is a bit average and enforcement is a bit hard. (1)

Mmm

And there will also be cracking down on tax dodgers. Not quite sure I know what that means.

There are our friends the closely held companies and dividend stripping . Which is essentially winding up to extract an untaxed capital gain and setting up a new company. Rather than just getting a taxable dividend from the original company.

Taxing these capital gains would have helped the issue.

And so instead strengthening enforcement for closely held companies (2) will be considered a high priority area for the next work programme.

Except enforcement is operational and the work programme is policy so not quite sure how that will work. But maybe I should get over myself, go with the vibe and wait for the actual new work programme.

But the Charities (3) stuff is all looking good.

The things I am most saddest about though are some of the more innovative obscure issues that aren’t being even considered for inclusion on the work programme. Which really only means – ‘will get to it if have time’.

They are the :

- Tax Advocate service (4) which would have helped small business and given an additional source of advice to the Minister;

- Overarching purpose clause (5) to say what the point of taxation is;

These are all potential neutral unpolitical improvements to the tax system. But didn’t hear Jacinda ruling them out – so maybe still hope.

So I might write some more about these. Oh and the OECD work on digital services. But once I have processed all this.

Andrea

(1) Annex on compliance.

(1) Paragraph 17 Executive Summary

(2) Recommendation 66

(3) Recommendation 78-82

(4) Recommendation 73

(5) Recommendation 77b

(6) Recommendation 66. Although to be fair there is a suggestion this could be handled differently.

#Doubletaxationisgross

Let’s talk about tax.

Or more particularly let’s talk about tax and companies.

Well dear readers what a week it has been in the Beltway. Secret recordings down south and secret payouts from Wellington. All the more bizarre as – Mike Williams confirmed – MPs staffers pretty much have sack at will contracts. If your MP doesn’t like you – that’s it you’re out. No lengthy performance management for them. Facepalm. So maybe this factoid could get added to new MPs induction?

But as always the key issue gets missed. Exactly who under 40 years old knows what a dictaphone is?

And into this maelstom Inland Revenue released a paper on taxation of individuals and some stuff on debt. Both worthy topics of discussion. But then Ryman released its results. And their CEO said like tax is paid – just not like income tax and just like not by them.

So after last week’s post I thought I’d have a look.

Oh yes the real tax is very easily found in the Income Tax Note. Tax losses of $28.9 million in the 2017 year. Up from last year when they were only $15 million of losses. They are a growth stock after all. Quite different from the tax expense which was $6m tax payable.

To your correspondent this looks awfully like her specialist subject of interest deductions for capital profits. All mixed up in a world where interest expense isn’t in the P&L but instead added to the asset value. Complying with both accounting and tax. And yeah totes a tax loophole but one from like whenever.

And again in Ryman’s accounts the rent equivalent from the time value of money of the occupancy advances is in neither the accounting nor the tax profit. Because reasons.

Now expecting controversy the CEO front footed the issue saying that the shareholders paid tax and that Ryman had actually paid GST. He then also referred to the PAYE deducted as they were employers. Kinda going to ignore that bit tho coz the whole claiming credit for other people’s tax really gets on my nerves.

And I’ll take his word on the GST angle coz I am cr@p at GST. But with his shareholders paid the tax comment – he is talking about imputation. And as I haven’t covered that before dear readers – today you get imputation. Oh and other random thoughts on tax and companies.

Now the official gig about imputation is how – notwithstanding that they are separate legal peeps – the company is merely a vehicle for their shareholders to do stuff. So for tax purposes the company structure should – sort of – get looked through to its shareholders. And this means dividends are in substance the same income as company profits and so should get a credit for tax paid by the company.

And as a tax person this stuff is considered to be in the stating the flaming obvious category.

But as I am no longer an insider – I am increasingly finding it interesting just how public policy on companies manages to talk out of both sides of its mouth. And how – much like the sack at will contracts or milliennials using dictaphones – no one has noticed.

On one hand we have the Companies Act which sets up companies with separate legal personalities from its shareholders. Meaning that if you transact with a company and it doesn’t pay you. Bad luck bucko. Nothing to do with the shareholders. Limited liability; corporate veil and all that.

But for tax if you only have a few shareholders those losses can flow through to the shareholders and be offset against against other income. The negative gearing thing but using a company. Coz in substance the company and shareholders are like the same.

And a similar thing happens with the Trust rules. Trust law says that it is trustees that own the assets. And once you have handed stuff over to them as settlor – that’s it – that stuff isn’t yours anymore. So if that settlor owes you money – also bad luck bucko. Don’t for a second think you can approach the trustees – coz whoa – settlor nothing to do with them.

But then tax says – for trusts – as settlors call the shots; it’s the residence of the settlor that is important. Mmmm. This means that a trust with a New Zealand resident trustee and a foreigner wot gave the stuff to the trustee – foreign trust – isn’t taxed on foreign income. Coz that would be like wrong. Even though the assets are owned by a New Zealand resident. And New Zealand residents normally pay tax on foreign income.

Right. Awesome. Thanks for playing.

Anyway back to imputation.

Now put any thoughts of separate legal personalities outside your pretty heads dear readers and think substance. Think companies are vehicles for shareholders. Don’t think about small shareholders having no say or liability if anything goes wrong. Just think one economic unit.

And then you will have no problem seeing potential double taxation if profit and dividends are both taxed. Coz #doubletaxationisgross.

So as part of the uber tax reforms in the late eighties imputation was brought in. Tax paid by the company can be magically turned into a tax credit called – imaginatively – an imputation credit which then travels with a dividend. Creating light and laughter in the capital markets. Or as I have put to me – increased inequality. As when imputation came in it gave dividend recipients – aka well off people – an income boost courtesy of the tax system. Probs also a tax free boost in the share price too.

Now putting aside such inconvenient facts – your correspondent has always defended imputation. Because in order to get the light and laughter or increased inequality – companies actually have to pay tax. And of that – big fan.

But all of this is only useful if shareholders are resident. Coz the credits only have value to New Zealand residents. And this is kind of why foreign companies may not care about paying tax here. And did I mention tax has to actually be paid?

And this last point that brings me back to Ryman’s chairman. He is right. If the company doesn’t pay tax – then the shareholders do when a dividend is paid. So honestly what are we all getting excited about?

Well – profits have to be like actually distributed before that happens and shareholders have to be taxpayers. And Ryman distributes less than 25% of their accounting profit.

And the residence of shareholders? Who knows. Lots of nominee companies listed which could mean KiwiSavers or non-residents. Oh and Ngai Tahu. Who seems to be a charity.

So yeah maybe. Some tax will be paid by some shareholders. That is true. Let’s hope it exceeds the tax losses Ryman is producing.

Andrea

PS. This will be the last post – except if it isn’t – for the next couple of weeks. Your correspondent is getting all her chickens back for a while. And much as I love you all dear readers – I love them more. Until Mid July. Xx

Two bills one week

Let’s talk about tax.

Or more particularly let’s talk about the two tax bills that were introduced this week.

Some time last century dear readers your correspondent was a junior accountant for an oil company in the UK. And in that company was a low cost petrol retailer. Now one day in the early nineties all staff – yes even the accountants – were called into some marketing meeting. Purpose of meeting was to explain some new wizard marketing strategy that we could all sing and dance around.

But before that particular experience some faceless but well dressed consultant treated us to some research. It was on customer behaviour and why customers chose one petrol station over another. Riveting stuff. And have to say the monthly accounts I would normally be doing at this time were starting to look pretty good.

Now pretty much like every consultant presentation I have sat through before or since – the insights were off the scale. People chose our petrol stations because of: location; retail stuff and coz we were cheap. Genius. Worth every penny. So glad they got the specialists in for that.

But then they dropped an actual knowledge bomb on my 25 year old self. As well as the blindingly obvious stuff – there was an actual true story group of customers that used our stations just because we said we were low cost. And for this group it didn’t actually matter whether we were low cost or not. Saying it was enough. Twenty five year old mind blown. The facts didn’t matter.

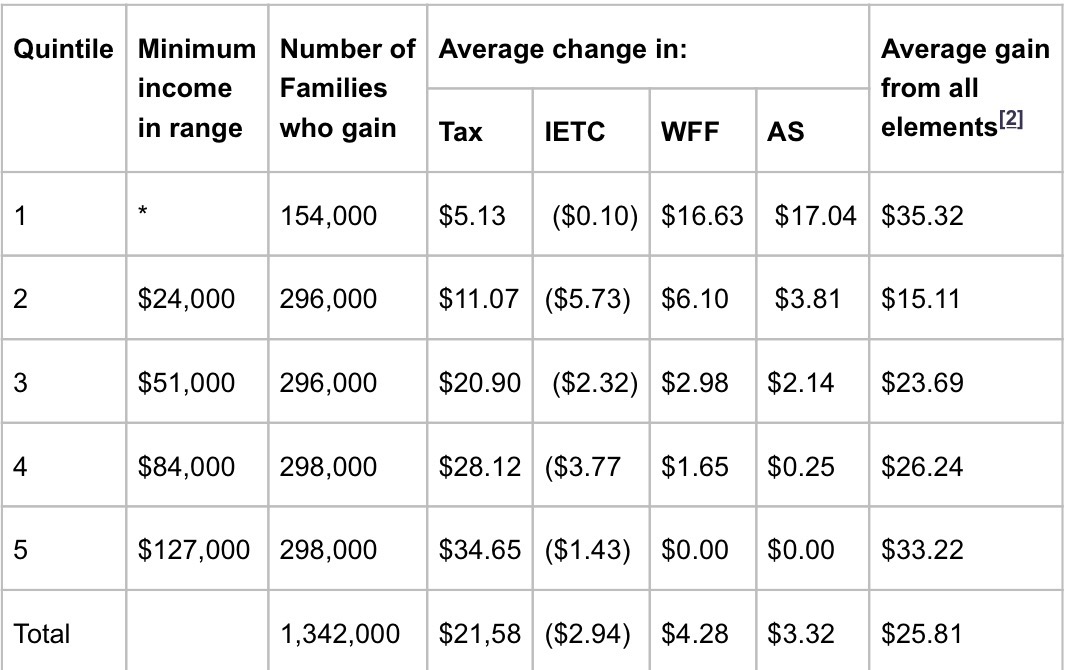

Now all of this came back to me this week with the Budget and the Family Incomes tax bill that was introduced and passed this week. A Budget that was for low and middle income families. Or as some commentators are dubbing it – a left wing budget.

Wow. Just wow. The facts still don’t matter.

Now it was Hon Steven’s big day out. Tax cuts for everyone!!! Just under 2 bill per year on tax cuts alone. And while there was other stuff. Vast bulk of the cost comes from tax cuts. Not entirely sure that this was what JustSpeak had in mind with its #billionbetterthings strap line but I guess tax cuts is preferable to any more bloody prisons.

And of course anything involving tax – even adjusting thresholds rather than rates – means more money goes to higher earners. It just does. It’s just what happens when you play around with tax stuff rather than transfer stuff. Coz higher income earners are the people who pay are the people who pay most of the income tax for individuals. So any cuts in income tax go to those who pay the income tax.

Oh and tax stuff applies to individuals not families. But I guess the clever Treasury people were able to turn this into a family costing below.

But then taking these lovely numbers and annualising them you get this:

Soooo families with incomes over $84k get half the dosh. Very progressive.

Even if those families didn’t actually want the princely sum of $35 per week and might have preferred it to go to mental health, or more state houses or more refugees. But at least it was only one new prison not three! #smallmercies.

But hey this is the party that has been elected. They can kinda do what they like. But a raid into Labour’s territory? Really? I guess if you say it often enough it must be true.

And then for comic relief was the political equivalent of a wardrobe malfunction. Hon Steven said that only one third of those eligible for IETC claimed it in a year rationalising its repeal. But then following questioning from the Michael Wood, Tim McIndoe kindly clarified that yes it was more 30% during the tax year and another 50% at the end of the year. Right ok. 80% not 30%.

And to be fair in the like actual Budget speech Hon Steven did say ‘during the tax year’. So not like actually lying. And in reality more likely a mix up in the bureaucracy than any intention to mislead.

But to your correspondent Budget 2017 – whole thing – deeply underwhelming. Just hope they didn’t also waste money on consultants as well.

Now ironically there was another tax bill that was also introduced last week that actually was a raid into Labour’s territory. Making everyone pay their fair share and all that. For top earners anyway. The Taxation (Annual Rates for 2017–18, Employment and Investment Income, and Remedial Matters) Bill. Just trips off the tongue. And on the whole it is a standard dull but worthy tax bill. Except for Employee Share Schemes. A well buried piece of social justice aka base maintenance.

Now the commentary and the previous discussion document are eye wateringly technical. Even your correspondent struggled. But buried in the RIS – para 54 – is the comment that it will raise $30 million a year. Now tiny in comparison to Steven’s big day out but quite a bit for a base maintenance item that deals with the taxation of remuneration. Especially since this is a net amount and there is an extension of a tax expenditure promoting widely offered share schemes. #workerparticipation.

Coz while yeah there are holes in the taxbase generally – all the remuneration stuff tends to be pretty water tight.

It all seems to have started life with a Revenue Alert that the department issued in late 2015. There they set out two wheezes that quite honestly could really only be used by important and well remunerated employees. People for whom the top tax rate is pretty much their average top rate. Coz honestly what employer could be bothered going to this amount of effort for ordinary employees.

Now currently the law pretty much says that if employees get shares then the difference between their value and what they pay for them is income. Makes sense.

But the Revenue Alert talks of a situation where:

- An employee buys shares on day one for market value. Awesome no taxable income there. No transfer of value. Alg.

- But they buy them with an interest free loan. Nah still cool. The value is in the interest free part and that is catered for by the Fringe Benefit Tax rules.

- Now there is a specific exclusion for interest free loans for employee share purchases. Mmm. Nah still ok. This is a specific concession and while it is an interest free loan – it is still a loan and needing repaying even if the shares go down. So yep still alg.

Except the wheeze is that the loan can be fully repaid by just handing the shares back. Ahh wot?

So if the shares go up – the difference is an untaxed capital gain but if they go down – nowt. Mmm no. Now the lovely Commissioner has quite correctly said – yeah nah – tax avoidance. And coz this is all connected to employment is looking to tax the gain as remuneration. Yep with you there Mrs Commissioner.

Now applying the tax avoidance provision all over the place is no way to run a tax system. So Hon Judith’s bill applies if you buy shares from your employer but you aren’t subject to the risk of them declining in value – aka not held ‘at risk’. In those situations when you get actual value from the transaction – that value is taxable. You know kinda like how when you are on a promise for a bonus – when that bonus actually materialises it is taxable? Yeah just like that here too.

Now yeah what ‘at risk’ means might not be super clear but tax avoidance audits aren’t super fun either. And as my late dear friend Tim Edgar would have said – just stay away from the edge. Everyone else pays tax on gains from their employer – so should the employees whose employers can be bothered to do clever stuff for them.

And this is what a socially progressive tax bill actually looks like. Hope it survives select committee.

Andrea

Shy and retiring

Let’s talk about tax.

Or more particularly let’s talk about how retirement villages don’t pay much tax.

Your correspondent has just returned from Auckland having: topped up her CPD hours; seen old friends and talked with tax peeps. And in that short period while I was away another industry was outed as being non-taxpaying. Now it is retirement villages and they aren’t even foreign.

But don’t panic. Steven Joyce says Inland Revenue is reviewing sectors of the economy which has low tax to accounting profits. And if there is a policy problem it can be put on the policy work programme. Phew.

Now as I have 5 days to complete 3 major pieces of assessment from my yoga course I have had two months to do – the sensible thing would be to put this issue down and pick it up after I have done my assessment. Coz it is not like they about to start taxpaying anytime soon.

But the issue is really interesting.

I am sure 4 days is enough to do all that other work. And I do need breaks from all that right brained stuff. I mean isn’t yoga all about balance?

So let’s have a look at the public stuff dear readers and see if we can’t unpick why these lovely people – much like our multinational friends – aren’t major contributors to the fisc. Now I know there are a few different operators but I thought I’d have a look at Ryman. Who may or may not be representative of the rest of them.

Tax actually paid

Now their tax stuff is interesting. Accounting tax expense of $3.9 million on an accounting profit of $305 million. But accounting tax expense is a total distraction if you want to know how much tax is actually paid. Why? Different rules. Future post I think.

Next place to look – imputation account which increased by $37,000. That can be real tax but can also include imputation credits from dividends received. So close but no cigar.

And then there is the oblique reference in note 4 to their tax losses in New Zealand having increased from $2.5 million in 2015 to $17.9 million in 2016. Bingo! That looks like they made a tax loss of $15 million in 2016 when they made an accounting profit of $305 million. Nice work if you can get it.

Ok now before we get into some exciting detail let’s have a think about what these retirement villages actually do. They can provide hospital services; some provide cafeterias; and they generally keep the place maintained. But mostly they ‘sell’ lifetime rights to apartments and flats on their premises.

Forgone rent

And it is this lifetime rights/apartment thing that is – in your correspondents view – the most interesting.

Looking at Ryman’s accounts and marketing material the deal seems to be residents provide an occupancy advance and get to have undisturbed use of an apartment until they ‘leave’. On ‘departure’ the right will be ‘resold’ and the former resident gets back wot they paid less some fees.

So the retirement village gets the benefit of any capital gain on the apartment as well as the benefit of forgone interest payable on the advance. All comparable to a ‘normal’ landlord who would receive the benefit of rent and capital gain on their property.

And like a ‘normal’ landlord they don’t really know how long the resident or tenant will want to stay. It could be one day or 30 years. But economically this doesn’t matter as the longer the resident stays the less in NPV terms the retirement village has to pay back. So whether landlord gets rent or repayable occupancy advance they both give the same outcome pretax and pre accounting rules. That is with rent over a long period you get lots of rent; with interest free occupancy advances over a long period you get lots of not having to pay interest.

However this isn’t how it pans out for accounting or tax.

For accounting the advances are carried at full value because they could be called immediately – occupancy advances in section j of Significant Accounting Policies. And because of this there is no time value of money benefit ever turning up in the Profit and Loss account – or what ever it is called now. Unlike rent which would get booked to the P&L when it was earned.

And tax is equally interesting. The Ryman gig seems to be that for the occupancy advance the resident gets title under the Unit Titles Act and a first mortgage for the period they are in the property. Fabulous.

Unfortunately your correspondent is about as far away from a property lawyer as it comes. But according to my property law advisor Wikipedia; a leasehold estate is where a person holds a temporary right to occupy land. Kinda looks like what is happening here. So that would be taxable under the land provisons. And even if it isn’t taxable there – to your correspondent – it looks pretty taxable as business income.

But in either case that involves taxing the entire advance and not just the interest benefit. Seems a bit mean.

Deductions

True. But let’s look at deductions before we call meanness.

Tax deductions are allowed when expenses are incurred or legally committed to. Not when actually paid. So if you are a yoga teacher and you commit to a Tiffany Cruikshank course in Cadiz in May 2017 – she is here in Wellington ATM so exciting – paying the USD 500 deposit in April 2016 you can take a deduction for the full amount of USD 2790 in the 2016/17 tax year. Even though you don’t pay it until closer to the actual course. Tax geeks yeah I am talking about Mitsubshi.

So for our retirement village friends as they are committed to repaying the occupancy advance in the future on the day they receive it. Immediate deductibility which cancels any taxable income. Mmm.

Tbf though the tax act isn’t big on the whole time value of money thing.

Financial arrangement rules

The exception is the financial arrangement rules where embedded interest can be spread over the term of the loan. And there is even a specific determination that deals with retirement villages. Now that seems to have more bells and whistles than is obvious from Ryman’s accounts so not entirely sure it relates to them. But there is one bit that could apply as the determination does say that the repayable occupancy advance is considered to be a loan.

Except even this gives no taxable income. This is because value coming in is compared to expected value going out. And of course THEY ARE THE SAME AMOUNT! So nowt to bring in as income.

Fixing it

Fixing this gap it would involve imputing some form of interest benefit that was in lieu of rent. But what interest rate to use? What is the term? And then there is the whole thing that no one actually sees it as a lease agreement. Everyone sees it as ‘ownership’ with a guaranteed sale price back.

Also entirely possible that what I consider to be blindingly obvious; cleverer people than me may consider to be – well – wrong.

Interest deductions

Then we get to much more old school techniques interest deductions to earn capital gains. And here Ryman seems to capitalise interest into new builds – section e of Significant Accounting Policies – rather than expense it for accounting. So there will be whole bunch of interest expense that isn’t in the P&L that will be on the tax return.

Unrealised capital gains

And finally thanks to NZ IRFS 13 – really does roll off the tongue doesn’t it – their accounting profits note 7 include a bunch of revaluations on their investment properties which I am guessing is the apartments. Bugg€r with this is that even a realised capital gains tax wouldn’t touch this and doesn’t look like these guys sell. Gareth’s thing though would work a treat as all the unrealised gains are on the balance sheet.

So here we have a property business that gets interest deductions; doesn’t pay tax on its capital gains or its imputed rent. Gains go on the P&L but not the interest expense. All while being totally compliant with tax and accounting.

No wonder they are share market darlings.

Andrea

Update

Thinking about the occupancy advances some more – depending on the counterfactual – maybe the value is in the tax system already as a reduced interest deduction.

The properties need funding somehow. Usually the options are debt which generates a deductible interest payment; equity which is subject to imputation or a combination of both. Here the assets are partially funded by the interest free occupancy advance. If the residents just paid rent – the assets would then need more capital. This could be completely debt funded which would mostly offset the rental income. May even exceed it if there was an expectation of a large capital gain. So while the occupancy advance is not in the tax system; neither is the extra interest deduction.

So maybe it is all an old school interest deduction for untaxed capital gain thing. But one for which a realised CGT would be useless as they don’t sell.

May need to look at Gareth’s thing again.

Fairness – Take two!

Let’s talk about tax.

Or more particularly let’s talk about tax and fairness.

On leaving the bureaucracy last year there were two issues that drove me absolutely mental and I wanted to put my energies into. The first was the rising prison population at a time of falling crime rates and the second was homelessness. Since then with the former I have become the policy coordinator for JustSpeak and a trustee for Yoga Education in Prisons Trust. For the latter – zip.

So with that in mind I went to a recent Labour Party thing on Housing stuff. But about mid way Phil Twyford said that the Labour Party in its first term of office was going to do a comprehensive review of the tax system to improve its fairness. Now I have heard them talk about this before – but comprehensive review. Wow.

Since then Andrew Little has said they aren’t putting up taxes. So maybe this means this working group will be ‘tax neutral’ in the way Bill English’s was?

Now on the basis that this isn’t simply code for a capital gains tax, I thought I’d do a bit of a scan as to what this could mean in practice. My focus will be on the revenue positive items as the tax community will have their own laundry list of revenue negative ‘unfairnesses’ they will want fixing.

But first I am going to get over myself. Yes fairness could mean a poll tax but when the Left talks about tax and fairness it is implicitly a combination of horizonal and vertical equity. Horizontal equity where all income is taxed the same way and Vertical equity where tax rises in proportion to income.

Alternatively tax and fairness to the Left can also mean using the tax system to remove or reduce structural inequities in the economy and not just in the tax system itself. So here we go:

Untaxed income

Capital income

Now the most obvi unfair thing is the way capital income is taxed more lightly than labour income. Always loved Andrew Little’s comment about the average Auckland house earning more than the average Auckland worker. Dunno why he doesn’t use it more.

Now the lighter taxation might be there for some good reasons including:

- Long periods before it is realised. Is it fair to tax people when don’t have cash to pay the tax?

- Valuation issues. Although this goes once move to realisation based taxes.

- International norm. Soz unfortunately everyone taxes capital more lightly – sigh.

- Lock in effect. If have to pay tax would you ever sell?

- Incentive for entrepreneurship which is a good thing apparently.

Oh and not being able to get elected.

Options include a realised capital gains tax or Gareth’s wealth taxation thing. Both have issues but both would be an improvement if fairness or horizontal equity is your thing.

Imputed rents

Alongside the not taxing capital gains is that we don’t tax imputed rents. Remember how owning your own home is effectively paying non-deductible rent to yourself and earning taxable rent? Except the value of the rent is not taxed? Awesome. But its non-taxation also offends the horizontal equity thing – even if it is your house – and so is unfair.

Active income of controlled foreign companies

New Zealand companies that earn foreign business income in their own names are taxed. New Zealand companies that earn foreign income through a foreign company aren’t. Why? International norm. Not fair but everyone else does that too. Also brought in by Michael Cullen. Nuff said.

Capital or wealth taxation

While Gareth’s thing is potentially wealth taxation it really is taxation of an imputed or deemed return on wealth rather than a tax on wealth per se. Actually taxing capital or wealth is where inheritance or gift duties come in.

Now neither of them are actually income taxes. They are outright taxes on capital. And if that capital arose from taxed income then would be very unfair to tax. However not entirely sure that is the case and these taxes are relatively painless as they tax windfalls; don’t effect behaviour and only apply to the well off. So they potentially promote fairness from a ‘reducing inequality’ sense rather than a horizontal or vertical equity sense.

Deductions

There are a few things here. There are all the issues with interest and capital gains but they reduce if you ever tax capital gains or do Gareth’s thing. Others include:

- Borrowing for PIE investment can get deductions at 33% while PIE income is taxed at 28%

Donations tax credit

Now this isn’t an obvious one as everyone can get a third back of their donations up to their total taxable income. So that is pretty fair. But the more taxable income you have the more subsidy you get. And it can go to a decile 10 school; your own personal charity or a church with an interesting back story. But dude – seriously – who can afford to give away all their taxable income? Perhaps worth a little look.

Labour income

Withholding taxes

Labour income that is earned as an employee is subject to PAYE and no deductions are allowed. Labour income that is earned as a contractor is only sometimes subject to withholding taxes and deductions are allowed. Aside from deductions which are likely to be pretty minimal with most employee type jobs – there is an evasion risk when people become responsible for their own tax. Spesh when such people are on very low incomes. Whole bunch of other ‘fairness’ issues too like access to employment law; but this is just a tax post.

Personal companies

Labour – and any income – can also be earned through a company. And a company is only taxed at 28% while the top rate is 33%. So if you don’t need all that income to live off you can decide how much stays in the company and how much you pay yourself. Is that fair?

Other things

Now of course there is always the old staple – increasing the top marginal tax rate. And yes that does enhance vertical equity but it also causes other problems elsewhere. So if you are going to make the system more misaligned please make sure that it doesn’t become the backdrop for widespread income shifting as it did last time.

Oh and secondary tax. Now there are many things that are unfair including precarious work and over taxation. Not sure secondary tax is one of them. While you have a progressive tax scale and multiple income sources – you get secondary tax. It appears that under BT – page 22 – the edges can be taken off getting a special tax code which should help but secondary tax in some form is structurely here to stay.

Look forward to it all playing out.

Andrea

Two men one press release

Let’s talk about tax.

Or more particularly let’s talk about Oxfam’s recent press release on inequality and tax.

Now dear readers when I moved to weekly – hah – posting it was because this blog was supposed to be my methadone programme. Getting me off tax and on to other issues. So when I posted last night – after having posted 3 times last week – I gave myself a good talking to. This had to stop. One post a week was quite enough to keep the cravings at bay. To continue in this vein would risk a relapse.

But this morning while I was getting dressed my husband came and turned on the radio. Rachel LeMesurier from Oxfam was talking about inequality and then she talked about tax and then Stephen Joyce came on and then he talked about tax and then he talked about BEPS.

Just one more little post won’t hurt I am sure and I’ll cut down next week honest.

Oxfam has compared the wealth of 2 New Zealand men Graham Hart and Richard Chandler to the bottom 30% of all adult New Zealanders. Now the inclusion of Richard Chandler seems to be a rhetorical device as from what I can tell he hasn’t lived here since 2006. So very unlikely to be resident for tax purposes.

In the interview Rachael Le M also made reference to the tax loopholes that support such wealth. So using what is public information about Graham Hart and what is public about the tax rules I thought I’d make a stab at setting out what these ‘loopholes’ are.

Now first dear readers please put out of your head anything you have heard about BEPS or diverted profit tax or any of the ways that the nasty multinationals don’t ‘pay their fair share of tax.’ None and I repeat none of this is relevant when dealing with our own people. It might be relevant for the countries they deal with but not for New Zealand. I am hoping that officials will also explain this to new MoF Steven Joyce as when he came on to reply to Rachael – he talked all about BEPS. Face palm.

Graham Hart is a serial business owner. Buying them sorting them out and then selling off the bits he doesn’t want all with a view to building up a Packaging empire. A Rank Group Debt google search also indicates that a substantial proportion of all this buying and selling was done through debt. And at times quite low quality debt which would indicate a proportionately higher interest rate. A number of his businesses are offshore.

So then what ‘loopholes’ – or gaps intended by Parliament – could Mr Hart be exploiting?

The first and most obvious one is that there is unlikely to be any tax on any of the gains made each time he sold an asset or business. The timeframes and lack of a particular pattern – as much as Dr Google can tell me – would indicate that the gains would not be taxable.

The second is that income from the active foreign businesses will be tax exempt and any dividends paid back to a New Zealand will also not be taxed. Trust me on this. I’ll take you all through this another day.

The third relates to debt. Even though it assists in the generation of capital gains and/or the exempt foreign income it will be fully deductible. Now because of the exempt foreign income there will potentially be interest restrictions if the debt of the NZ group exceeds 75% of the value of the assets. A restriction true but not an excessive one given exempt income is being earned.

Now also in Oxfam’s press statement is a reference to a third of HWIs not paying the top tax rate. I am guessing some version of one and three plus the ability to use losses from past business failures is the reason.

Unsurprisingly Eric Crampton of the New Zealand Institute is not sympathetic to Oxfam’s views and points to our housing market as the main driver of inequality. So then in terms of tax and housing the other tax ‘loophole’ then would be the exclusion of imputed rents from the tax base.

Now one answer could be Gareth’s proposal. That is if someone could explain to me how to tax ‘productive capital as measured in the capital account of the National Income Accounts’ in a world where tax is based on financial accounts according to NZIFRS.

The second could be a capital gains tax even on realisation and the third some form interest restriction or clawback when a capital gain is realised. Oh and taxing imputed rents.

How politically palatable is this? Not very given National, Labour, Act, New Zealand First and United Future are all opposed to a capital gains tax – at least Labour for their first term.

But then maybe it is stuff for Labour’s working group. Will be interested to see this all play out.

Andrea