Tax, debt and wage theft

Last week I went to a cocktail bar with young and interesting people (1). Had the best lime and soda of my life. #winningatlife. Apparently they serve other drinks too but decided to quit while I was ahead.

The young people were the workers that had been left out of pocket following Wagamama going into receivership. (2) With this as an example they, alongside Raise the Bar, are currently waging a campaign against wage theft in the hospitality industry.

I went along to their public meeting in case anyone needed a hand with their tax – because when payroll goes wrong – tax isn’t that far behind. The lime and soda was just a bonus.

Gave them a bit of a blurb about how the law allowed Inland Revenue to claim unpaid tax from employees in cases where it hadn’t been taken out of your pay in the first place. Proving that could be a bit difficult in cases where the records were cr@p – so it might be a case of talking to IR nicely and explaining the situation and going from there.

Now these wonderful young people were well ahead of me. August last year was when info stopped turning up on their myIR. And August last year was when they started talking to the department.

Experience was broadly positive. The deal seems to be IR will update your info if you can show your payslip and bank account as to what was deducted and the amount you actually received. For these workers PAYE seems to be (largely) fixed but not student loan deductions. So there might be some follow up secure mail messages for that.

Their personal KiwiSaver deductions are also ok but the employer contribution has vaporised.

Managers of the firm – also out of pocket not just the workers – talk of receiving lots of letters from IRD with lots of penalties on them. They forwarded them on and were told it was being fixed and/or a mistake.

So all of this went on from August last year until July this year when the firm went into receivership. 11 months of workers contacting IRD over their own personal tax and IRD sending letters with penalties to the company.

And I am like – Inland Revenue knew about this for 11 months? Is this what was supposed to happen?

So I went back to the paper Officials provided for the TWG in July 2018 – a month before things started going weird for the lovely young people.

It says that 85% of taxpayers file and pay on time. Now on one level that sounds good in a 98.5% of Māori children are not in care sort of way.

But taxpayer is an odd metric when talking about filing and paying. I am one taxpayer but last year I filed 12 GST returns, 1 IR 3 and 1 Donations tax credit form. Now they were all on time and fully paid – because old habits die hard – but I would have thought compliance should be measured on a returns basis rather than a taxpayer basis?

Oh and it is. Trawling through the Department’s 2018 annual return the notes at the end show that they are actually talking about returns not taxpayers (3).

Right.

And again 85% could be awesome or it could be so so depending on how PAYE earners are treated.

From the info below it looks like there were about 9 million returns filed in any one year. If 3.5 million PAYE people are excluded before the 85% is calculated – alg. But if they are included this means that the on time rate for everything else is more like 75% (4).

Still not bad.

But whether it is 15% or 25%; whether 9 million is actual or potentially filed; whether or not any of this is weighted for value of debt; the absolute numbers of not filing and paying on time are not small.

But back to the officials paper (5).

That paper sets out that Inland Revenue triages its debt non-compliance into three groups:

Disorganised This is where the taxpayer has the funds but has rubbish systems and their brain is full. Here reminders from IR tend to do the trick.

Can’t pay Business either temporarily or permanently failing and so doesn’t have the dosh to pay tax. Early conversations with the taxpayer about whether their business is viable are the thing here. (6) Financial penalties aren’t very useful as the taxpayer can’t pay the original debt.

Won’t pay Taxpayer has the funds but choses not to pay tax. Behaviours include not passing on ’employee’s PAYE deductions’. Here insolvency proceedings, taking security and criminal prosecution are the thing.

Ok so my new cool friends’ employer looks like a can’t pay with a soupçon of won’t pay. And maybe there was lots of lovely engagement and installment arrangements behind the scenes?

Regardless the compliance and admin costs of every worker having to prove every tax deduction for 11 months, the follow up conversations on student loans and the loss of employer KiwiSaver contributions – just maybe Inland Revenue could have moved a little faster?

If not for the ProdComm’s concern about the long tail of unproductive firms, other suppliers and these young people’s lives – then maybe for the Crown account? Because while IR – I am sure – will ultimately sort out the individuals tax; as these lovely young people pointed out last week:

Not passing on PAYE hurts everyone in New Zealand

The Tax Working Group recommended making directors who have an economic ownership in the company personally liable for arrears on GST and PAYE obligations where there has been deliberate or persistent non-compliance. (7) And most of this is about concentrating the mind of the actors concerned and shortening the pain for everyone rather than necessarily a bunch of corporate veil lifting.

Such a good idea – on so many levels.

And this might be what is included as compliance and enforcement issues in the Business possibles on the tax work programme?

Hope so.

And hope it is an issue in the Small Business Council’s report. As it all needs action stat.

Andrea

(1) Consequently post written to the earworm of Don’t you want me. Gen Xers will understand. Millennials it was the OG Someone that I used to know.

(2) In recent news Wagamama UK have decided to give them an out of pocket settlement. Great news and a great relief to me as Wagamama is a regular for my UK family. I can continue to eat there with a clear conscience when I visit.

(3) Page 118

(4) Assuming 9 million returns, 85% is 7.65m returns. If we excluded 3.5m PAYE returns as being broadly right this gives 4.15 m returns on a base of (9m – 3.5m) 5.5 m. 4.15/5.5 is a 75% filed and paid on non- PAYE earners.

(5) Section 3

(6) Footnote 6 is worth a look. ‘Interventions could include writing off some or all of the tax debt’. That is definitely for another day.

(7) As long as there has been an appropriate warning system. Rec 64(a)

Where have all the audits gone?

Blogging this time around is quite a different experience to last time. Then I was still relatively unknown and didn’t have the wide circle of cool progressive friends that I do now.

I tried out various types of subjects and – much like now – went broadly where my interest and the topics of the day were trending. The post that got me noticed was the review of TOP’s tax policy – including getting noticed by Gareth Morgan and the one that went the widest was my push for Deborah Russell.

The one that got most hits on the day – and it is still the number one – was when I got upset about the Inland Revenue restructure of the investigation function. My friends were hurting and so I was hurting too.

Since then my LinkedIn feed has shown a steady stream of talented people leaving Inland Revenue for other opportunities. I have heard it said that the people who left were change resistant and/or deadwood. The fact that they left would put lie to the change resistant angle. And given they have all moved on to senior positions in government, the Big 4, international organisations or their own successful practices – I think deadwood is a stretch too.

The Commissioner recently told the Finance and Expenditure committee that there had been no drop in technical expertise (1). And I think that is probably right. While there has been a net loss of talent, there are still lots of very capable competent people there. A number of people who were senior team leaders have gone back to doing the work. They were kick arse before they became team leaders and will be kick arse now. The tax system is safe with them.

Similarly the managers who were ultimately appointed. All very sane, experienced and competent. Yes some took redundancy but they are now doing different cool things with their lives.

So for these reasons I haven’t felt any need to reopen this topic. My friends who were affected have now either moved on and happy in their new roles or accepted the pay cut – after equalisation wears off – given the other benefits working for the Revenue entails. And there are quite a number. Flexibility, intellectual interest, and socially productive work – to name but three.

Yes there is still the matter of a 27% engagement score (2) but that is between the Commissioner, the Minister and the State Services Commissioner. Nothing I can add to that. There should still be the capability and capacity to run a decent audit programme even after the restructure.

Like most of the tax community, I had heard that this year people were being moved out of investigating into correspondence or the phones to help the BT transition. But they were only mumurings – there was no proof of that.

Until now.

Andrew Bayly Opposition spokesman for Revenue has put in a number of written parliamentary questions – it appears – looking to get to the bottom of the mumurings.

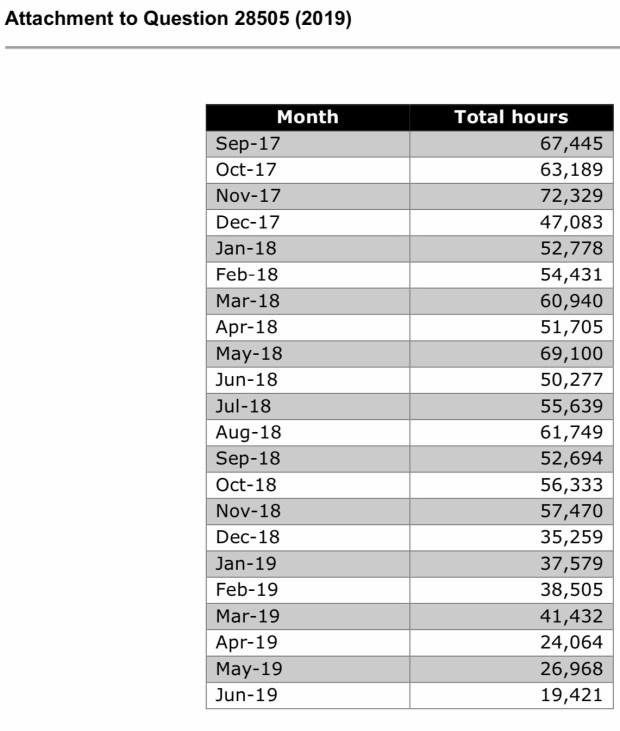

He asked quite a number of questions but the one I homed in on was audit hours. (3) Dear readers they have plumeted. June 19 is a third of June 18 – yes a third. To be fair that is probably the worst month. At best they are 2/3 of the previous year.

So the murmurings were true.

Ok so during an important stage the Commissioner moved her resources around. Fair enough.

What I don’t understand is if they were to fall like that why not come clean? Front foot it to the tax community. Say yeah audit activity will drop over this period because [insert reasons here] but – much like Arnie – we’ll be back baby. Don’t get complacent.

But it does mean that if this level of resources are being shifted from BAU to BT, BT is costing more than originally forecast. And these extra costs should be booked against BT. Or if they are being booked against BT – then the BAU money should be given back. It’s not like the Government doesn’t have uses for it.

Now none of this, as far as I can tell, is being mentioned in the monthly reporting to Joint ministers. This focus is solely on the BT programme and no mention, that I can see, on the affect on BAU.

There is, however, a mention in the paper Minister Nash took to Cabinet in November

The department’s service performance may dip while these changes are embedded. I will be kept regularly informed of any issues that arise. (4)

So I can only assume there has been parallel reporting on BAU to the Minister of Revenue on this and he and Treasury are happy with the reallocation of resources.

Of course if I have any of this wrong Inland Revenue – as I know you read the blog – please let me know and I’ll retract accordingly. But otherwise – Andrew Bayly is doing his job.

Andrew, our politics may not be the same, but dude – respect. I now have your wpq link on speed dial. Thank you for your service.

Andrea

(1) Second paragraph page 4

(2) Page 12 question from Dan Bidois

(3) The answer to audit commencements about not having information that predates START is odd. We all used to put our time into eCase. Clumsy and annoying. But it was all there. I can’t believe that Inland Revenue would be in breach of the Public Records Act and not have that information anymore. Would be a really back look too given taxpayers have to hold records for 7 years. Must be a mistake.

(4) Paragraph 32

SUPERCommissioner

OVER 2,000 hack attempts and I finally broke into Andrea’s blog. (1) I should have known straight away her password would be CGT4eva. So here I am. Another rare left-leaning socially progressive tax expert.

This may be why Michael Wood, chair of the Finance and Expenditure Select Committee – politely and somewhat bemusedly – said to me: “you realise you are the only submission against this aspect of the bill….this should be interesting”.

The bill is now an Act of Parliament, the Taxation (Annual Rates for 2019–20, GST Offshore Supplier Registration, and Remedial Matters) Act 2019.

I was not the only submitter on the bill.

There were 268 submitters who opposed the ring-fencing of rental losses. Of course there were – some people might have to pay more tax. But, only one submitter (me), was opposing a tiny amendment that was also a blatant disregard for democracy and the rule of law.

And that tiny amendment created the Commissioner’s new superpower.

While Spiderman has quite an extraordinary power to climb, and Magneto has the power to control magnetic fields, much more useful than all that, the Commissioner of Inland Revenue has acquired the power to exempt taxpayers from tax law.

Totally wicked.

This power can be used to make a wide-reaching exemption for all taxpayers affected by the law, or limited to specific circumstances. You know – just special people.

The Commissioner may use her power to correct ‘obvious errors’ in the law. Or to give effect to the law’s intended purpose – as determined by the Commissioner – to resolve an ambiguity in the law, to reconcile inconsistencies between two laws or between the law and an ‘administrative practice’.

The last one is my personal favourite.

The Commissioner may grant the exemption where a tax law is inconsistent with the IRD practice on the issue. Wonderful. So unelected bureaucrats trump Parliament? Although yeah I get that Parliament has given the Commissioner this power. And this quite extrordinary superpower has been granted with little public interest.

There are two reasons for this.

First tax is apparently boring and doesn’t attract great public interest unless one’s own wallet is impacted. The usual submitters (tax geeks) generally represent business interests. The other reason is that the power is likely to operate only in a taxpayer’s interest, not against.

The provisions state that a taxpayer is not required to follow the Commissioner’s edict to exempt a law. Aha not so powerful after all. Taxpayers can choose to follow the strict letter of the law. In other words, this exemption will only be applied for the benefit of the taxpayer, not to their detriment.

So what’s my problem? My concerns are two-fold.

First, I am not comfortable with administrative functions being granted superpowers to circumvent law made by the democratically elected representatives. Second, I am concerned with who will benefit from these provisions.

Segregation of the duties of our government is one of the foundations of New Zealand’s (unwritten) constitution. Law making power is granted to the elected body – parliament – made up of members chosen by the people and crossing all spectrums of society.

Administration of the law is taken up by unelected employees of government. Granting law making (or breaking) powers to an official appointed by the State Services Commissioner crosses the segregation boundaries and undermines the process of law making.

Granting the Commissioner the ability to exempt a law because it is inconsistent with an administrative practice moves into the sphere of law making.

The third branch of government, sitting alongside parliament and the executive, is the judiciary – those who interpret and enforce law.

Granting the Commissioner the power to exempt taxpayers from a law because it is inconsistent with parliament’s intention steps on the toes of the judiciary. It is the judiciary’s role to determine what the intention of parliament might be.

My second concern is somewhat more pragmatic. Who is this superpower designed to benefit?

Most New Zealanders receive all their income from salary and wages and pay their tax through the PAYE system. Most New Zealanders have no need for an accountant and do not even file tax returns.

But if you have more complex financial affairs, you may need an accountant. And if you have lots of money, you might have a very expensive accountant with a great deal of expertise in money matters – including tax. You might have a very expensive lawyer as well. This is good news and has kept me in gainful employment through my working years.

Now, I have spoken with a few of my friends (who have accountants but not the expensive sort), and they tell me they are not aware of the Commissioner’s new superpower. They tell me they are unlikely to be requesting the Commissioner to use her new power in their favour due to – well – ignorance. I have an inkling who may be inclined to use the new provisions, however.

Perhaps those with more complex tax affairs. Perhaps those who use expensive accountants and lawyers. Perhaps those with access to tax knowledge and expertise.

Now the Inland Revenue officials who have reviewed my submission have said, “don’t worry” Alison. The Commissioner’s new superpower is “intended to only be used for minor or administrative matter where there are no, or negligible fiscal implications”. Which would be fine except that’s not what the legislation says.

The superpower is not at all limited to ‘minor or administrative’ matters. It is far broader than that. And as for ‘no or negligible fiscal impact’… what would be the point of exempting a law if there was no or negligible fiscal implications?

And once again, this is not exactly what the law says. It says the Commissioner may only use her power if there are no or negligible fiscal implications for the Crown. Now the last financial year produced over $80bn of tax revenue for the Crown. So I ask, what is negligible in the context of $80bn? Is $20m negligible?

This is up to the Commissioner to determine.

Now I do not mean to suggest any corruption on the part of our tax administration or our current Commissioner. But the law must protect the people from the potential for corruption. And this law steps well over that line.

The use of this superpower will be one to watch. But who will be watching? That is a conversation for another day.

Alison

————————————————————————————————————

(1) I note though that Andrea prefers ‘unauthorised access’ to ‘hack’. But as she invited me in – albeit not through a search bar – she can get over herself.

PIEs, timebar and tax fairness

My lovely young friends had a great time with their guest post last week and were delighted with the reception they received. Including getting picked up by interest.co.nz – something they like to point out I have never managed.

They were really keen to post this week on the digital services tax discussion document which they think is awesome. But I need to have a little chat to them before they do.

We also had a chat about whether the Andrea Tax Party is really a goer. Much like Alfred Ngaro we have concluded it all seems a bit hard. Also the move from thinking about things to politics hasn’t been the smoothest for TOP. So as the evidence led people that we are, we have decided to conserve our emotional energy and not fall out over boring constitutional issues.

I’ll stay as your correspondent and my young friends will come back from time to time when they can fit it in between their three jobs and studying. They are also checking out Organise Aotearoa who recently put up this sign in Auckland and seem to be to the left of Tax Justice Aotearoa.

As well as the digital services tax proposal – which I’ll save for my (briefed) young friends – the other tax story this week was how thanks to the Department upgrading its computer system it has found a number of people – 450,000 – haven’t been paying enough tax on their PIE investments. And while that is the case the Department has said that it won’t chase this tax on any past years.

Behind this story are two interesting – to me anyway – tax concepts.

Portfolio investment entities (PIEs)

These are a Michael Cullen special and came in at the same time as KiwiSaver. Before their introduction all managed funds were taxed at the trust rate of 33% and were taxed on any gains they made on shares sales – because they were in business.

Alongside all this was passive investment or index funds who had managed to convince Inland Revenue that because they only sold because they had to, those gains weren’t taxable.

Individual investors weren’t taxed on their capital gains and otherwise they were taxed at less than 33% if they had taxable income below the 33% threshold. This was particularly the case for retired investors.

The status quo did though give a minor tax benefit to high income people who were otherwise paying tax at 39%.

So it was all a bit of a hot mess.

Added into the equation was that, unlike now, the Department’s computer wasn’t up to much so all policy was based on ‘keeping people out of the system’.

So where the PIE stuff landed was income of the fund would be broken up in terms of who owned it and taxed at the rate of the owners. Except for the high earners – as their alternative was a unit trust taxed at the company rate – the top rate was capped at the company rate.

Low income people were now taxed at their own rate rather than the trust rate and high income people kept their low level tax benefit.

Happiness all round.

But it all depended on the individual investor telling the fund what the correct rate was and boy did the funds send out lots of reminders. I got totally sick of them.

Particularly when not filling them out meant you got taxed at 28% which was the top rate anyway.

So the people getting caught out this week would have once told the fund to tax them at a lower rate. It wouldn’t have happened by accident.

Although it is entirely possible they were on a lower rate at the time – because they had losses or something – and then ‘forgot’ to update it. Such people though would probably had a tax agent who would normally pick this stuff up. So not these people,

The caught people I would suggest are people, without tax agents, who accidentally or intentionally chose the wrong rate at the time or are PAYE earners whose income has increased over time and didn’t think to tell their fund.

But really only a tax audit would tell the difference between the two groups even if the effect is the same.

Time Bar

The other thing this week has shone light on is something known in the tax community as timebar (2).

It is a balance between the Government’s right to the correct amount of revenue and taxpayer’s ability to live their lives not worrying about a future tax audit. The deal is that if you have filed your tax return and provided all the necessary information – but you are wrong in the Government’s favour – Inland Revenue can only go back and increase your tax for four years.

If you haven’t filed and/or provided the necessary information – usually in cases of tax evasion – game on. The Department has no time constraints.

But the thing is none of this is an obligation on Inland Revenue. It is a right but not an obligation.

Under the Care and Management provisions (1) – the Commissioner must only collect the highest net revenue over time factoring in compliance costs and the resources available to her.

And so on that basis – I must presume – she has decided to not go back and collect tax for the last three years underpaid PIE income. In the same way he – as it was then – decided to only pursue two years of tax avoidance that arose from the Penny and Hooper tax avoidance cases.

Now I am sure this is completely above board legally in much the same way as the use of current accounts or the non-taxation of capital gains.

But with a tax fairness lens, it makes discussions with my young friends quite tricky.

They only have their personal labour which, to them, is taxed higher than I was at the same age. They don’t have capital and see this recent story as another way the tax system is slanted against them.

So I am not sure we have seen the last of the motorway signs.

Andrea

(1) Section 6A(3)

(2) Section 108