Two bills one week

Let’s talk about tax.

Or more particularly let’s talk about the two tax bills that were introduced this week.

Some time last century dear readers your correspondent was a junior accountant for an oil company in the UK. And in that company was a low cost petrol retailer. Now one day in the early nineties all staff – yes even the accountants – were called into some marketing meeting. Purpose of meeting was to explain some new wizard marketing strategy that we could all sing and dance around.

But before that particular experience some faceless but well dressed consultant treated us to some research. It was on customer behaviour and why customers chose one petrol station over another. Riveting stuff. And have to say the monthly accounts I would normally be doing at this time were starting to look pretty good.

Now pretty much like every consultant presentation I have sat through before or since – the insights were off the scale. People chose our petrol stations because of: location; retail stuff and coz we were cheap. Genius. Worth every penny. So glad they got the specialists in for that.

But then they dropped an actual knowledge bomb on my 25 year old self. As well as the blindingly obvious stuff – there was an actual true story group of customers that used our stations just because we said we were low cost. And for this group it didn’t actually matter whether we were low cost or not. Saying it was enough. Twenty five year old mind blown. The facts didn’t matter.

Now all of this came back to me this week with the Budget and the Family Incomes tax bill that was introduced and passed this week. A Budget that was for low and middle income families. Or as some commentators are dubbing it – a left wing budget.

Wow. Just wow. The facts still don’t matter.

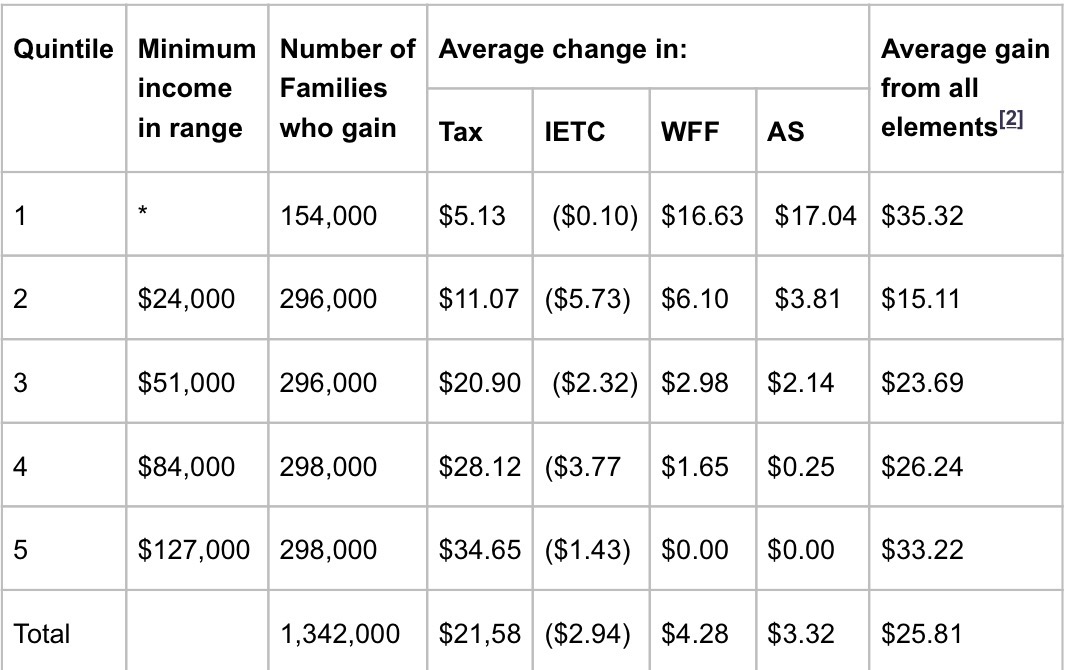

Now it was Hon Steven’s big day out. Tax cuts for everyone!!! Just under 2 bill per year on tax cuts alone. And while there was other stuff. Vast bulk of the cost comes from tax cuts. Not entirely sure that this was what JustSpeak had in mind with its #billionbetterthings strap line but I guess tax cuts is preferable to any more bloody prisons.

And of course anything involving tax – even adjusting thresholds rather than rates – means more money goes to higher earners. It just does. It’s just what happens when you play around with tax stuff rather than transfer stuff. Coz higher income earners are the people who pay are the people who pay most of the income tax for individuals. So any cuts in income tax go to those who pay the income tax.

Oh and tax stuff applies to individuals not families. But I guess the clever Treasury people were able to turn this into a family costing below.

But then taking these lovely numbers and annualising them you get this:

Soooo families with incomes over $84k get half the dosh. Very progressive.

Even if those families didn’t actually want the princely sum of $35 per week and might have preferred it to go to mental health, or more state houses or more refugees. But at least it was only one new prison not three! #smallmercies.

But hey this is the party that has been elected. They can kinda do what they like. But a raid into Labour’s territory? Really? I guess if you say it often enough it must be true.

And then for comic relief was the political equivalent of a wardrobe malfunction. Hon Steven said that only one third of those eligible for IETC claimed it in a year rationalising its repeal. But then following questioning from the Michael Wood, Tim McIndoe kindly clarified that yes it was more 30% during the tax year and another 50% at the end of the year. Right ok. 80% not 30%.

And to be fair in the like actual Budget speech Hon Steven did say ‘during the tax year’. So not like actually lying. And in reality more likely a mix up in the bureaucracy than any intention to mislead.

But to your correspondent Budget 2017 – whole thing – deeply underwhelming. Just hope they didn’t also waste money on consultants as well.

Now ironically there was another tax bill that was also introduced last week that actually was a raid into Labour’s territory. Making everyone pay their fair share and all that. For top earners anyway. The Taxation (Annual Rates for 2017–18, Employment and Investment Income, and Remedial Matters) Bill. Just trips off the tongue. And on the whole it is a standard dull but worthy tax bill. Except for Employee Share Schemes. A well buried piece of social justice aka base maintenance.

Now the commentary and the previous discussion document are eye wateringly technical. Even your correspondent struggled. But buried in the RIS – para 54 – is the comment that it will raise $30 million a year. Now tiny in comparison to Steven’s big day out but quite a bit for a base maintenance item that deals with the taxation of remuneration. Especially since this is a net amount and there is an extension of a tax expenditure promoting widely offered share schemes. #workerparticipation.

Coz while yeah there are holes in the taxbase generally – all the remuneration stuff tends to be pretty water tight.

It all seems to have started life with a Revenue Alert that the department issued in late 2015. There they set out two wheezes that quite honestly could really only be used by important and well remunerated employees. People for whom the top tax rate is pretty much their average top rate. Coz honestly what employer could be bothered going to this amount of effort for ordinary employees.

Now currently the law pretty much says that if employees get shares then the difference between their value and what they pay for them is income. Makes sense.

But the Revenue Alert talks of a situation where:

- An employee buys shares on day one for market value. Awesome no taxable income there. No transfer of value. Alg.

- But they buy them with an interest free loan. Nah still cool. The value is in the interest free part and that is catered for by the Fringe Benefit Tax rules.

- Now there is a specific exclusion for interest free loans for employee share purchases. Mmm. Nah still ok. This is a specific concession and while it is an interest free loan – it is still a loan and needing repaying even if the shares go down. So yep still alg.

Except the wheeze is that the loan can be fully repaid by just handing the shares back. Ahh wot?

So if the shares go up – the difference is an untaxed capital gain but if they go down – nowt. Mmm no. Now the lovely Commissioner has quite correctly said – yeah nah – tax avoidance. And coz this is all connected to employment is looking to tax the gain as remuneration. Yep with you there Mrs Commissioner.

Now applying the tax avoidance provision all over the place is no way to run a tax system. So Hon Judith’s bill applies if you buy shares from your employer but you aren’t subject to the risk of them declining in value – aka not held ‘at risk’. In those situations when you get actual value from the transaction – that value is taxable. You know kinda like how when you are on a promise for a bonus – when that bonus actually materialises it is taxable? Yeah just like that here too.

Now yeah what ‘at risk’ means might not be super clear but tax avoidance audits aren’t super fun either. And as my late dear friend Tim Edgar would have said – just stay away from the edge. Everyone else pays tax on gains from their employer – so should the employees whose employers can be bothered to do clever stuff for them.

And this is what a socially progressive tax bill actually looks like. Hope it survives select committee.

Andrea

R&D again

I haven’t forgotten you dear readers. Normal transmission will return in mid May promise. But this morning when I opened my Herald app I see R&D tax incentives are being discussed again. Sigh.

But then your correspondent has friends in the big firms – all lovely people. All have mortgages and families that need feeding. And with IR Business Transformation their jobs could be at risk. Nice to know they could have something to fall back on.

Anyway dear readers I wrote about it all here. Have a read while you are waiting.

Andrea

Fairness – Take two!

Let’s talk about tax.

Or more particularly let’s talk about tax and fairness.

On leaving the bureaucracy last year there were two issues that drove me absolutely mental and I wanted to put my energies into. The first was the rising prison population at a time of falling crime rates and the second was homelessness. Since then with the former I have become the policy coordinator for JustSpeak and a trustee for Yoga Education in Prisons Trust. For the latter – zip.

So with that in mind I went to a recent Labour Party thing on Housing stuff. But about mid way Phil Twyford said that the Labour Party in its first term of office was going to do a comprehensive review of the tax system to improve its fairness. Now I have heard them talk about this before – but comprehensive review. Wow.

Since then Andrew Little has said they aren’t putting up taxes. So maybe this means this working group will be ‘tax neutral’ in the way Bill English’s was?

Now on the basis that this isn’t simply code for a capital gains tax, I thought I’d do a bit of a scan as to what this could mean in practice. My focus will be on the revenue positive items as the tax community will have their own laundry list of revenue negative ‘unfairnesses’ they will want fixing.

But first I am going to get over myself. Yes fairness could mean a poll tax but when the Left talks about tax and fairness it is implicitly a combination of horizonal and vertical equity. Horizontal equity where all income is taxed the same way and Vertical equity where tax rises in proportion to income.

Alternatively tax and fairness to the Left can also mean using the tax system to remove or reduce structural inequities in the economy and not just in the tax system itself. So here we go:

Untaxed income

Capital income

Now the most obvi unfair thing is the way capital income is taxed more lightly than labour income. Always loved Andrew Little’s comment about the average Auckland house earning more than the average Auckland worker. Dunno why he doesn’t use it more.

Now the lighter taxation might be there for some good reasons including:

- Long periods before it is realised. Is it fair to tax people when don’t have cash to pay the tax?

- Valuation issues. Although this goes once move to realisation based taxes.

- International norm. Soz unfortunately everyone taxes capital more lightly – sigh.

- Lock in effect. If have to pay tax would you ever sell?

- Incentive for entrepreneurship which is a good thing apparently.

Oh and not being able to get elected.

Options include a realised capital gains tax or Gareth’s wealth taxation thing. Both have issues but both would be an improvement if fairness or horizontal equity is your thing.

Imputed rents

Alongside the not taxing capital gains is that we don’t tax imputed rents. Remember how owning your own home is effectively paying non-deductible rent to yourself and earning taxable rent? Except the value of the rent is not taxed? Awesome. But its non-taxation also offends the horizontal equity thing – even if it is your house – and so is unfair.

Active income of controlled foreign companies

New Zealand companies that earn foreign business income in their own names are taxed. New Zealand companies that earn foreign income through a foreign company aren’t. Why? International norm. Not fair but everyone else does that too. Also brought in by Michael Cullen. Nuff said.

Capital or wealth taxation

While Gareth’s thing is potentially wealth taxation it really is taxation of an imputed or deemed return on wealth rather than a tax on wealth per se. Actually taxing capital or wealth is where inheritance or gift duties come in.

Now neither of them are actually income taxes. They are outright taxes on capital. And if that capital arose from taxed income then would be very unfair to tax. However not entirely sure that is the case and these taxes are relatively painless as they tax windfalls; don’t effect behaviour and only apply to the well off. So they potentially promote fairness from a ‘reducing inequality’ sense rather than a horizontal or vertical equity sense.

Deductions

There are a few things here. There are all the issues with interest and capital gains but they reduce if you ever tax capital gains or do Gareth’s thing. Others include:

- Borrowing for PIE investment can get deductions at 33% while PIE income is taxed at 28%

Donations tax credit

Now this isn’t an obvious one as everyone can get a third back of their donations up to their total taxable income. So that is pretty fair. But the more taxable income you have the more subsidy you get. And it can go to a decile 10 school; your own personal charity or a church with an interesting back story. But dude – seriously – who can afford to give away all their taxable income? Perhaps worth a little look.

Labour income

Withholding taxes

Labour income that is earned as an employee is subject to PAYE and no deductions are allowed. Labour income that is earned as a contractor is only sometimes subject to withholding taxes and deductions are allowed. Aside from deductions which are likely to be pretty minimal with most employee type jobs – there is an evasion risk when people become responsible for their own tax. Spesh when such people are on very low incomes. Whole bunch of other ‘fairness’ issues too like access to employment law; but this is just a tax post.

Personal companies

Labour – and any income – can also be earned through a company. And a company is only taxed at 28% while the top rate is 33%. So if you don’t need all that income to live off you can decide how much stays in the company and how much you pay yourself. Is that fair?

Other things

Now of course there is always the old staple – increasing the top marginal tax rate. And yes that does enhance vertical equity but it also causes other problems elsewhere. So if you are going to make the system more misaligned please make sure that it doesn’t become the backdrop for widespread income shifting as it did last time.

Oh and secondary tax. Now there are many things that are unfair including precarious work and over taxation. Not sure secondary tax is one of them. While you have a progressive tax scale and multiple income sources – you get secondary tax. It appears that under BT – page 22 – the edges can be taken off getting a special tax code which should help but secondary tax in some form is structurely here to stay.

Look forward to it all playing out.

Andrea

All The Right Moves

Let’s talk about tax.

Or more particularly let’s talk about the charitable tax exemption given to Scientology.

For reasons that are beyond me I have seen very few of Tom Cruise’s movies. Even in the mid/late eighties when he and I were in our respective heydays. Whether it was my twice weekly Rocky Horror attendance that crowded them out or the current boyfriend didn’t want the competition – couldn’t tell you. And it wasn’t as though I was super geeky or anything. Both The Breakfast Club and Merry Christmas Mr Lawrence ‘spoke to me’ – I was young what can I say – so defo the target audience for Mr Cruise. Also have never seen An Officer and a Gentleman but I think that’s Richard Gere.

I did see All The Right Moves an early film that wasn’t too bad. And I did see one of the Mission Impossible films with my boys. Truly excreable but it was clear my offspring not me were the target audience there.

Apart from his films and rotating cast of wives, Tom Cruise is also famous for being a member of the Scientology church which became newsworthy last week. Now again for reasons that are beyond me I had always thought that the Scientology Church wasn’t a registered charity in New Zealand. But recently a former colleague told me that I was wrong. Perhaps I was thinking of the Jedi? Coz they aren’t a registered charity.

Yeah that must be it. I was thinking of the Jedi.

But just in case I am not the only one confusing them with the Jedi, I thought I might look at what is public on the Charities Register and how they could have got registered.

Mr CharityWatchNZ and Society for the Promotion of Community Standards – name which is a blast from the past Patricia Bartlett who didn’t like swearing or nudity – have both done more fulsome discussions on Mr Cruise’s religion in New Zealand which are worth a read.

Now I am sure you remember from A Plague on all your Houses that there are two ways Scientology could become registered. One through the advancement of religion where the benefit to the community is just assumed or through the catch all option of other matters beneficial to the community where there is also a public benefit test that needs to be met.

It appears to have been registered as a religious charity but its purpose statement seems to cover all bases. Arts and culture; social services; human rights as well as emergency disaster relief . All for the general public and not just members of Scientology. Lucky us. A degree of divinity is defo needed to do all that.

And from the news reports that is what they say they are doing too. Refurbed a heritage building complete with dolls and help disenfranchised youth. Your correspondent is big on help for disenfranchised youth and am sufficiently twee to enjoy a nice heritage building. So go them.

But of course being charitable they not only don’t pay tax on trading income – they also get access to the donations tax credit. You know the one where the ever tolerant taxpayers of New Zealand effectively give a charity one dollar for every two donated. And looking at their annual return this means potentially $600k in 2015 and $250k or so in 2014 and 2013. So – assuming all donations claimed the credit – over $1m in 3 years. But it is a lovely building and what about all those disenfranchised youth.

Now they apparently do other stuff. Auditing or something. And if that isn’t beneficial to the community I don’t know what is. Wonder if I can get a donations tax credit for my CAANZ registration? Don’t actually know how to audit though. I wonder if investigate is close enough?

Andrea

Destination anywhere

Let’s talk about tax.

Or more particularly let’s talk about the Republican party’s recent proposal to impose ‘border adjustments’ as a reform of their corporate tax system.

To date this has passed me by. Slowly though things have percolated up to various feeds I follow. All talking about how Trump can balance the budget and punish companies that export jobs. The first I saw looked like a GST where imports are taxed and exports aren’t. Fair enough I thought if the US wants to impose import duties – ok but nothing to do with me. I do income tax not tariffs. I won’t be commenting. Good luck with the WTO on that. And our US tax treaty only covers federal income taxes not value added taxes so no issue there.

Then I saw something that said it was income tax. Sales to foreigners wouldn’t be taxed and purchases from foreigners wouldn’t get deductions. And no interest deductions coz it was a cashflow tax. Whoa I thought – that’s odd. How do you deny interest deductions as they are a cashflow? And what about restricting deductions for local purchase costs when you aren’t taxing foreign income? How’s that going to work?

But in that article Professor Alan Auerbach is talking positively about the proposals. Penny dropped.

A few years ago Prof A came to New Zealand with some other academics and gave two presentations on destination taxation that I am embarrassed to say did not understand one word of. Awesome so that is what this is about and I will have to do some actual work to comment rather than accessing my increasingly failing tax memory.

Having now done some work – that is I found the good professor’s 2010 paper and read it – I can see why I didn’t understand. It is a major change in how income tax systems work and so nothing really would have resonated.

Now let’s see if I can paraphrase the 29 pages.

Focus is on taxing cashflows that originate in the US – so:

- Foreign sales not taxed;

- Foreign purchases not deductible;

- All domestic purchases – including capital items – are deductible;

- All domestic borrowings – full amount borrowed not typo keep breathing – are taxable;

- All domestic lending is deductible; and

- Foreign borrowing and foreign lending – not respectively deductible or taxable.

Wow just wow. So wish I had followed this when Prof A came out. I would have had soooo many questions.

The advantages of this are said to be:

- Tidies up the US treatment of foreign income and removes the incentive to move US income to havens because the US would tax it even less. Yep agreed.

- Treats debt and equity equally and removes the tax preference for debt. Yep does that too as while capital items are fully deductible the full amount that is borrowed – so long as it is borrowed domestically – is taxed.

Issues with this though kinda are:

- Not only originally US income could find its way back from abroad. So could most actual foreign income actually earned overseas – as Auerbach is proposing the US become the MacDaddy of tax havens.

- No deductions for foreign purchases but deductions for the same domestic purchase. Mmm what does that sound like? Ah discrimination according to the US/NZ treaty – is what it sounds like. Article 23(4) to be precise.

- Foreign purchases not deductible but domestic sales taxable. Mmm how long will it be before foreign subs start servicing the US market? Now that can be stopped if they reform their controlled foreign company (CFC ) rules – but a CFC is by definition foreign – and isn’t foreign stuff out. It can also be stopped through a reform of the permanent establishment rules as proposed by the OECD but isn’t that a nasty pinko Obama thing?

- Domestic borrowings fully taxable but foreign borrowings not. Too easy. Bye bye local banks. Hello City of London.

There are other things like I am not at all sure that full deductibility for long lived assets is at all the right policy as it doesn’t match the decline in their economic life. So the longer lived the asset the greater the tax expenditure – because why? Is there a shortage of long lived assets in the US economy? And accelerated depreciation was the basis for the double dip leases that were all the rage around and before 2000. But maybe the requirement that the asset has to be in the US will protect them this time.

Now that was 2010 and an academic paper. Let’s see what has actually proposed by policy makers – Paul Ryan nonetheless.

Paul Ryan’s 2016 tax policy allows: full deductions for capital expenditure; repatriation of foreign dividends tax free; ‘border adjustment’ aka taxing imports and exempting exports; ‘streamlining’ subpart F aka CFC rules and denying deductibility for net interest. So pretty much Professor Auerbach’s proposal with a corporate tax cut to 20c and not the foreign bank preference.

As a big interest whinger – here, here and here – I am going to be really interested to see how interest denials stay the course. The rest of the proposal looks pretty standard right wing with a bit of foreign bashing with the foreign purchase deduction denial. But denying interest – wow – that is huge. Further than I would go even with a reduced corporate tax rate. But then maybe the interest deductions will flow into foreign countries at the same time the income is flowing out. All the more reason for New Zealand to a make sure we have interest deductions for non- residents properly sorted. Next week’s post promise.

In Paul Ryan’s thing there are some spurious references to the WTO and how they are mean to the US – I think that is called doing their job – but no reference to the tax treaty breaches. But the IRS international tax counsel know all about these issues and I hope they are being funded properly – coz buckle up boys – their competent authorities are about to get really busy. Oh and it’s Article 23(3) in the US treaty with China.

And the servicing of the US from say Canada and Mexico – don’t know how far drones can fly – pretty sure though it’s higher than the average wall or fence. But that is my bet as to what will happen when imports are denied a tax deduction. Not more tax revenue and not more jobs. And lots of warning for the companies who can start looking at border real estate. Just like the GOP – so very business friendly.

Yep. Making America great again – one own goal at a time.

Andrea

Unconditional – it’s what it means

Let’s (briefly) talk about tax ( and education). Again – yes I know.

The headline of today’s Dominion Post showed that in 2015 schools collected $11 million in donations more than they had previously. Now dear readers after And another thing you all know that this means that of the extra $11 million the government subsidied this by a third.

Also interesting if you follow the embedded Stuff links you see that decile 10 schools dominate the donations stakes. By about $329 million to $2.8 million. Mega yuck given this just happens automatically and doesn’t go through Parliament every year as Education budget does.

Now this we have discussed before and promise I am not interrupting your Saturday to moan again about that.

The reason for this postette is the reference to how music lessons and school camps and the like are now being reclassified as donations.

No just no.

IRD guidance is very clear that donations need to be an ‘unconditional gift’. Nothing in return. A cash version of seva although they will probs never use that analogy.

The law is very clear and any ‘reclassification’ will be very easily overturned by the department. Please apply your brain. If you get anything in return – it ain’t a donation and so no donations tax credit.

Simple. Please carry on.

Namaste

And another thing

Let’s (briefly) talk about tax (and donations to schools).

Following Monday‘s post I got to think about the other ‘advancement’ head of charity – education.

Now there is the whole controversy about whether donations that schools seek are really for extras and their role in an education system that is supposed to be free. And there is the thing about decile funding that the government gives less to higher decile schools coz they can fund raise.

But if that ‘fund raising’ comes from ‘donations’ then the government again gives one dollar for every two actually donated. So the bigger the donation and the higher level of actual payment – the more the government gives.

None of which is recorded in the education budget coz it is an off the books tax expenditure. So the schools with richer parents get more government help. Very progressive.

Probs not actually intended. More likely to just be an interface of separate policies and never actually thought through. Shame.

Now for those of you who are properly interested in the can of worms that is tax and charity stuff I’d recommend my friend CharitywatchNZ‘s blog. Not currently being updated as he has gone back inside (the bureaucracy) for a while. But still all good stuff.

Namaste

A plague on all your houses

Let’s talk about tax.

Or more particularly let’s talk about the tax free status of religion.

Your correspondent has just started the first stage of yoga teacher training (YTT). Three lots of 8 11 hour days spread over 6 months. It still surprises me as I have no desire to actually teach yoga. I do have a great desire to further learn the history and philosophy of a practice that has seriously helped me get my sh!t together. But not actually teach. Oh and anyone who is reading this who is doing it too and not already a teacher – totes non-deductible as it is a capital expense.

Now because I was about to get seriously busy I was planning to invoke the ‘except when there isn’t clause’ on my Monday posting commitment. But then as if we all hadn’t suffered enough with the earthquakes, floods, and closing of non-earthquake prone buildings – we got Brian Tamaki.

It’s the gays fault.

Awesome.

Strangely that pearl of post-truth wisdom from Bishop Brian has made some people so super mad that they have launched a petition to have Destiny Church’s tax free status removed. Interesting. Because of course the fact that they are a registered charity not only means they are tax exempt on any income but also that through the donations tax credit the government effectively gives them one dollar for every two given to them.

And now on my Facebook feed are coming questions – ‘so why is religion tax exempt?’. To which I’d reply ‘historic reasons‘. Advancement of religion is one of the four heads of charity. Alongside advancement of education, relief of poverty and other matters beneficial to the community.

Historically the churches were our welfare system. And even now a lot of social services are undertaken by church based groups. But that would still fit under the ‘relief of poverty’ head.

And religion and church going is beneficial to many people. In fact there is no additional ‘public benefit’ test for the religious head coz it is just presumed to be beneficial to the community.

Now I would argue I get similar benefits from my yoga practice. So yeah it does seem a tad anachronistic given the country is increasingly secular. And the gay thing is interesting too. As although the state has said marriage is between two consenting adults – that is a step too far for our churches.

But if advancement of religion were removed; churches would then have to make their case that what they did was a matter beneficial to the community and that it had a public benefit.

Perhaps not lead with Bishop Brian.

Namaste

Trumping the tax system

Let’s (briefly) talk about tax (and Donald Trump).

Your (foreign) correspondent is very comfortably ensconced in the spare bedroom of her darling friend in Geneva. Reviewing my Facebook newsfeed – as well as giving me the most recent memory of my son and his girlfriend looking totally adorable going to a ball last year – was someone sharing this:

It discusses that Donald Trump claimed a $915 million loss in 1995 that could then be offset against any taxable income for the next 15 years.

Now the thing dear readers is – as I discussed in ‘The apple doesn’t fall far from the tree’ that is technically totes possible in New Zealand too. Putting capital into a business – spending it on business expenses – and then losing it will give you future losses to offset against other taxable income. But unlike in the US if you sell the business – rather than the company – for a capital gain the company keeps the losses and gets a capital gain that can be distributed tax free on liquidation.

And if it is done through a Look through Company the losses and the capital gains can pass through to the individual shareholders.

Now all of this could be totes fabulous as a means of encouraging entrepeneurship and innovation or simply entrencing dynastic behaviours. Couldn’t tell you.

Maybe Grant something for your ‘Fairness’ working group?

Namaste

Bright and shiny and new

Let’s talk about tax.

Or more particularly let’s talk about incentives for research and development.

Your correspondent has just arrived in Sydney for the start of what her husband delightfully refers to as her ‘retirement cruise’. That would be broadly accurate except for the fact that I am not fricken retiring – I’m on a gap year ok! and there will be no boats involved. Planes – yes – and lots of trains – yay I love trains – but nothing actually ocean going.

But with an aunt, uncle, cousin and now son and his girlfriend in Sydney I have now more family there than I do in parts of New Zealand. So it is only logical that I should come here more often than in the past and the fact that the weather is better plays no part in it. Given it is Sydney I should also reference shopping but I hate shopping – other than online shopping, probs a future GST post I think – so I won’t.

Being in Australia figured I should do a compare and contrast tax post. What to choose? What to choose? Tax free threshold?; extremely high top marginal rate?; stamp duties?; payroll taxes?; offshore banking unit?; GST exemptions?; carbon tax?; substance based approach to instrument classification? All important issues and ones I will only really ever be able to properly discuss if I am actually in Australia – so happy to take that for the team.

But today dear readers you get research and development tax credits which lots of countries – including Australia – have.

Now other than during a brief period at the end of the last Labour government, New Zealand does not give explicit tax incentives for research and development. R&D expenditure does however get more concessional treatment than other business expenditure:

- it is deductible until it is capitalised for accounting

- Consequential losses are not lost on a change in shareholding and

- Losses can be cashed out up to a limit.

Plus as discussed on Monday gains from successful entrepreneurship in the form of serial business owning are unlikely to be taxed and there is no clawback of any residual losses if the business rather than the company is sold.

And none of this is included in the billion dollars – pg 27/28 – a year that the government already spends on innovation. And yeah it is a year – none of this ‘over the forecast period’ stuff where you multiply annual expenditure by four the way they do with other initiatives. So big money.

Furthermore (wow did I really say furthermore on a blog?) growth grants look awfully like a R&D tax credit. But as this government repealed the last government’s tax credit, by definition, New Zealand does not have R&D tax credits.

Now dear readers you may be wondering why this expenditure should be treated better than any other business expenditure. And the official answer as to why it isn’t just another form of corporate welfare goes something like this:

R&D creates these things called spillover benefits that roam free like pokemon in the wild that anyone can capture. Because anyone can capture it, businesses don’t do as such of it as they ‘should’. And because wild pokemon are good for the economy governments need to pony up with a subsidy to make sure enough of it can happen.

Whether any of this is actually true – I wouldn’t have the first clue. Work of far cleverer people than me would indicate that it isn’t wrong.

What I do have the first clue on though is delivery mechanisms.

And from that first clue I say – please next lefty government – please don’t do this stuff through the tax system. Now I know my priors were fully on display last Friday – but just please don’t. And not because it fails some ‘purity of the tax system’ thing. Please don’t do it because – as we say in yoga – it doesn’t serve you.

Yeah I know both Labour and the Greens seem to be sympathetic to using the tax system more for this stuff. And while Gareth Hughes is quoted as saying delivery through the tax system is better because it is ‘simpler and less bureaucratic‘ – it is a view I hear quite often and not just from the Left. Sigh.

Now I just don’t get simpler as both Callaghan and the Income Tax Act use the accounting defintion of R&D which is trying to get at is whether something really is bright and shiny and new and not simply improving on existing stuff. Less bureaucratic however needs a bit of unpacking.

First a bit of background. Our tax system works on a self assessment basis whereby you work out how much income you have based on your – or your agent’s – intimate detailed and expert knowledge of the minutiae and nuance of the tax laws. And then you pay tax on that number. To ensure you don’t entirely take the proverbial the Commissioner has a bunch of powers at her disposal. Her – never gets old.

Now while she – still loving it – has a bunch of powers at her disposal she – ok I’ve stopped now – also has limited audit resource and can’t review every claim. And let’s put to one side that a tax dept unlike Callaghan is not known for its scientific expertise. So because of this, all things being equal a claim for R&D that isn’t quite right is more likely to get government funding through the tax system than through a grants system. Now I totes get why business would like that – just not entirely sure why the rest of us including a Minister of Finance would.

And now here’s the thing in terms of less bureaucratic. If she does decide to use her powers to challenge a tax credit that wasn’t in her view correctly claimed – game on. Potentially a complete world of pain for the receiver of the credit – aka the disputes process. And at the end of that world of pain – they might have to pay the money back even if they have spent it.

Now there is a way of avoiding this risk generally in tax and making sure it is less likely to happen. That is through getting an upfront binding ruling which – facepalm – would be very similar to a grant process.

So instead of simpler and less bureaucratic – I would say – higher fiscal risk for government and greater uncertainty for business. Awesome – sign me up now.

And I am not just being a pain here. In Australia CBA is apparently having ‘issues’ with the ATO involving serious cash that I can only assume it has spent. I also get that Australia changed has changed its rules but please note Green Party both these links talk about the mining industry being major receivers of these benefits. Something borne out by the Mining Institute who are very clear that:

The R&D tax incentive supports the development of world-leading technology in the minerals industry.

So lefty parties please just think about this very carefully before you go this way. It’s not like you will have heaps of spare cash if you do make it to the Beehive next year.

Namaste