Tax and Small Business

Last week the Small Business Council issued its report to Government. I am sure there are many wizard things in there maybe even some tax recs.

Also last week I had a friend to stay who is helping some workers that have lost thousands of dollars of wages and holiday pay when their employer went into receivership. Her expression was Wage Theft. It is a crime in Australia but not in New Zealand. Unlike theft as a servant which totally is.

Talking to her it was obvious that there was considerable overlap between what she is seeing and the issues considered by the TWG of closely held companies where the directors have an ownership interest not paying PAYE and GST (1).

And yes my friend’s friends are worried about their PAYE and KiwiSaver deductions. So really hope tightening up on this stuff is in the Small Business report along with the expected recs on compliance cost reduction.

I am also personally very interested in what the Group comes up with as the Productivity Commission noted that NZ has a lot of small low productivity firms without an up or out dynamic (2). That is firms tieing up capital that should be released for more productive purposes with the associated benefit of not staying on too long and dragging their workers and the tax base with them.

Now ever since I found that reference I have been concerned that there may be aspects of the tax system that may be driving that. Benefits or ‘opportunities’ that don’t arise for employees subject to PAYE or owners of widely held businesses subject to audits and outside shareholder scrutiny.

And it is true that there is nothing particularly special in a tax sense here to New Zealand. However given that New Zealand rates as number one in the ease of doing business index there may be more people going into business than would be the case in other countries.

Some of these aspects can be reduced through stricter enforcement by Inland Revenue but are otherwise largely structural in a self assessment tax system where the department doesn’t audit every taxpayer. One is a policy choice possibly because the alternative would add significant complexity to the tax system and the final example is a combination of the need for stronger enforcement and/or policy changes needed now that the company and top personal rate are destined to be permanently misaligned.

So what are these ‘aspects’?

Concealing income or deducting private expenses

Recent work by Norman Gemmell and Ana Cabal found that the self employed had 20% higher consumption than the PAYE employed at the same levels of taxable income.

Now it could be that for some reason the extra consumption of the self employed comes from inheritances or untaxed capital gains or taking loans from their business – more on that later – more so than those in the PAYE system or owners of widely held businesses. It might not be tax evasion at all.

But we just don’t know.

All we know is the 20% extra consumption and that there is a greater opportunity and fewer checks with closely held businesses to conceal income or deduct personal expenses. And Inland Revenue says such levels are comparable with other countries.

While things like greater withholding taxes and/or reporting can help, I am also concerned that with greater automation it also becomes much easier to have those personal expenses effortlessly charged against the business rather than recorded as personal drawings.

Interest Deductions

The second aspect is my specialist subject of interest deductions. Unlike concealing income or deducting personal expenditure – this one is totes legit.

Interest is fully deductible to a company and for everyone else it is deductible if it can be linked to a taxable income earning purpose or income stream aka tracing.

What that means is if a business person has a house of $2 million and a business of $1 million and has debt of $1 million – all the interest deductions on the debt can be tax deductible – if the debt can be linked to the business. This can be compared to a house of $2 million and debt of $1 million – and no business – where none of it is deductible.

To make this fairer with taxpayers who don’t have the opportunity to structure their debt there would need to be some form of apportionment over all assets – business and personal. So in the above example interest on only $330,000 should be allowed.

But yes – that would require a form of valuation of personal and business assets. And yes valuing goodwill brings up all the same – valid – concerns raised with taxing more capital gains.

So I guess we can say that under the status quo fairness – and possibly capital allocation – have been traded off against compliance costs.

Income Splitting

The third is the ability to income split with partners to take advantage of the progressive tax scale. Now this is only actually allowed if the partner is doing work for the business. But verifying the scale and degree of this work – even with burden of proof on Commissioner – is a big if not impossible task for the Commissioner.

Other mechanisms include loans from the partner to help max out the lower income tax bands.

And the statistics would support an argument that there is a degree of maxing out the lower bands just not that there necessarily is a lot of income splitting.

Interestingly both Canada and Australia have rules for personal services companies where these types of deductions are not allowed.

But this is ok if this is the amount of value going to the shareholders. Maybe our firms are so unproductive that they can only support shareholder salaries of $70k and below.

If that were the case though we wouldn’t be seeing the final aspect which is taking loans from companies you control instead of taxable dividends.

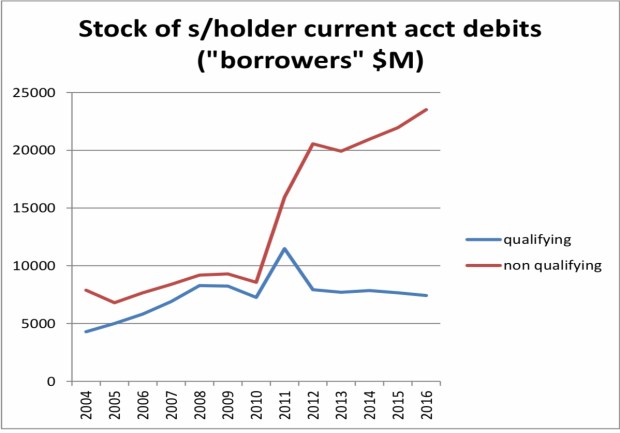

Overdrawn shareholder current accounts

Now to be fair for this to occur there should also be interest paid by the shareholder to the company on loans from the company to the shareholder. And unlike the interest in point 2 – none of this should be tax deductible to shareholder if it is funding personal expenditure while the interest received will be taxable. This on its own should be enough to not do it and receive taxable dividends instead.

Unfortunately the facts also don’t seem to back this up. Imputation credit account balances – meaning tax has been paid but not distributed- have been climbing. Now this could be like totally awesome if it meant all the money was being retained in the company to grow.

Except that overdrawn current account balances – loans from the company to the shareholders- have been similarly growing too. Now sitting at about $25 billion.

And yes this all started from about 2010. And what happened in 2010? Why dear readers the company tax rate was cut to 28% while the trust rate remained at 33%.

Ironically the associated cut in top marginal rate was to stop the income shifting that went on between personal income and the trust rate.

Now one level it shouldn’t matter at all if these balances continue to climb so long as non- deductible assessable interest is paid on the debt. However an overdrawn current account is – imho – the gateway drug to dividend avoidance.

And yes that can be tax avoidance but much like the tax evasion opportunities, income splitting and interest on overdrawn current accounts – all of this requires enforcement by Inland Revenue. And as they can’t audit everyone there will always be a degree that is structural in a self assessment tax system.

But the underlying driver of people wanting to take loans from their company rather than imputed dividends is that our top personal tax rate and company tax rate are not the same. Paying a dividend would require another 5% tax to be paid.

Possible options

Now other countries have always had a gap between the top rate and either the company or trust rate so this shouldn’t be the end of the world. But those countries have buttressing rules that we don’t have in New Zealand. The personal services company rules discussed above or the accumulated earnings tax in the US (3) or the Australian rule that deems such loans to be dividends.

Until recently I had been a fan of making the look through company rules compulsory for any company that was currently eligible. (4) I couldn’t see the downside. The closely held business really is an extension of its shareholder so why not stop pretending and tax them correctly.

However some very kind friends have been in my ear and pointed out the difficulties of taxing the shareholder when all the income and cash to pay the tax was in the company. It works ok when it is just losses being passed through. So maybe I am less bullish now.

An alternative approach could be to apply a weighted average of the shareholders tax rates on the basis that all the income would be distributed. Similar to PIEs. The tax liability is with the entity but the rate is based on the shareholders. I guess you then do a mock distribution to the shareholders which can then be distributed to them tax free. And yes only to closely held companies. Wider would be a nightmare.

Kind of a PIE meets LTC.

Or you could just old school it and raise the company tax rate to 33% for all companies. Shareholders with tax rates below that could use the LTC rules and make the assessment of whether the compliance of the rules was greater or less than the extra tax.

It would require an adjustment to the thin capitalisation rules by increasing the deductible debt levels to ensure foreign investment didn’t pay more tax. But for some of you dear readers increased taxation on foreign investment might even be a plus.

But all in all I don’t think the status quo with small business is a goer. Whether it is for fairness reasons, or capital allocation reasons or simply stopping me worrying – doing something is a really good idea.

Because I would hate to think any of this was enabling behaviours that kept people in business longer than they should. And even with the most whizziest of new IRD computers – there will always be limits on enforcement.

Andrea

(1) Page 116 Paragraph 68

(2) Page 19

(3) Although it would make more sense to only apply this to the extend that the income hasn’t been retained in the business and distributed in non- dividend form.

(4) Yes there is the issue that companies could start adding an extra class of share to get around this. But I don’t believe this is insurmountable with de minimis levels of additional categories and the odd antiavoidance rule for good measure. It is even the advice of KPMG so clearly not that wacky.

The other Boleyn girl

Since coming back from hols your correspondent has been struggling with an annoying cold. That bad side is that my yoga practice has suffered. Good side is that I have had greater opportunity to sample the ever expanding Netflix menu.

So for comedy I can recommend Santa Clarita Diet, Huge in France and Derry Girls. For documentaries I can recommend Bobby Sands 66 Days, Black Panthers and Period. End of sentence. Oh and Knock Down The House of course. Obvi.

Now for reasons that are beyond me – although constant checking for the next season of The Crown may have had a minor effect – Netflix is recommending The Other Boleyn Girl to me. A book I read many years ago while stuck in an airport but not one I want to watch immediately after a documentary on IRA hunger strikers.

AI still has a way to go.

Anyway the story is that there was apparently an older Boleyn sister that Henry was keen on before he was keen on Anne. And she was probably better coz she loved him much more but is now like super obscure – or possibly completely fictional – and so like it all could have been so different.

Now in CGT land there is also another Boleyn girl. Leading up to the finalisation of the report one of the members – Robin Oliver – put together a sketch of an alternative way of taxing more capital gains.

It has the pithy title of Robin Oliver: Taxing Share Gains but not Gains Made by Companies: Member Note for Session 24 of the Tax Working Group. It also got the slightly more pithy title in the media of CGT Light.

And yes I know there won’t be anymore taxation of capital gains but acceptance is a process and, as a relational being , I am (over) sharing.

So off we go!

Now I am sure you all know dear readers the final design was one of:

- Gains taxed from valuation day

- Loss ringfencing in ‘transition’ period but limited constraints thereafter

- Applying to most – currently untaxed – assets

- Limited rollover relief when buying other assets

- No change to existing rules for debt or foreign shares

And the associated issues with this were:

- Difficulties with valuing hard to value assets like goodwill particularly when only part of a business is sold off

- Revenue risk in downturns

- Incentivising ownership of foreign shares over New Zealand shares

- Lock in

- Complex rules to prevent double deductions within corporate groups

- Troy Bowker getting upset a lot.

Now there were possible ways of reducing all those issues – except maybe the last one. But Robin had a go at looking at it all a bit differently while still ultimately taxing more capital gains on a realised basis.

In particular he suggested:

- Taxation of gains on residential property – valuation method as per final report

- Possible taxation of other land but with extensive rollover provisions

- Inclusion of depreciable property – although in practice this just means losses and/or depreciation would return for buildings that fall in value with gains taxed if rise in value. Maybe software would also be affected but most depreciable assets already get deductions for their decline in value.

So far not that much different to the final report. However there were four key differences:

- No increased taxation of capital gains – other than above – at company level

- Shareholder of listed companies taxed on gains on sale from a valuation day

- Shareholder of unlisted widely held companies taxed on gains on sale. Existing holdings grandparented

- Shareholder of closely held company taxed on gains on assets sold by company. Existing goodwill of companies grandparented.

In some ways this option was lighter than that of the final report:

- Existing holdings of widely held unlisted companies would be outside the tax but they would also be outside the complexities of valuation, the median rule and loss ringfencing.

- Existing goodwill of closely held companies would also be outside the tax but also outside the complexities of valuation, and the median rule.

Now while the grandparenting thing seems like a big gift, it would have been less than Australia did coz they grandparented – didn’t apply the tax to – all existing assets and now 30 years later Australia collect lots of money (1). And yeah it would have been less money to play with in the immediate period but a whole lot more money than is the case now.

The non-taxation of assets in widely held companies would give a timing advantage to shareholders as tax wouldn’t be paid until the shareholders sold their shares. But it would mean that such groups wouldn’t have the compliance cost of the double deduction rules. And the Government wouldn’t have the risk that those rules didn’t actually work all that well and lose lots of money in the process. Coz it’s not like that has never happened before.

But in other ways Robin’s option was actually tougher. Shareholders of closely held companies would be paying tax on any capital gain earned by the company – at their marginal tax rate. So if that was 33% they would pay tax at 33% not the company rate of 28%.

Robin prepared all this as a possible option for Ministers and the Working Group made it very clear that the choices were not binary and the hard stuff was in the active business area. So it could have been worked up by officials as an option in any discussion document – even if they weren’t wild about it at the time. (3)

The Government might even have grandparented all existing assets as Australia did and take away all the noise. And yeah it would take a while to build up but after 10 years or so (4) – serious money.

But it was not to be. And in the end all possibilities went the way of the real Boleyn girls.

Thanks for listening.

Andrea

(1) Page 28

(2) Paragraphs 11-13

(3) Robin’s response to officials comments

(4) Figure 3.10

Alignment again

Let’s tax about tax.

Or more particularly let’s talk about Australia’s proposal for a reduced tax rate for small business.

Ok yes I am excited. A new government. A Labour led government. And a young woman as a Prime Minister. Mostly what I hoped for as I climbed the millions of steps to door knock in Wellington. My left leg is almost recovered too. Thanks for asking.

And as if all of this wasn’t exciting enough two of my young friends Talia Smart and Matt Woolley won the Robin Oliver tax competition. Talia on Charities and Business and Matt on the integration of the company and personal tax. I hope to cover their papers once they become public.

Oh and Stuart Nash has won the pools and become Minister of Revenue.

So big congrats to Talia, Matt and Hon Stu. Expecting great things from you all.

We should hear about the tax working group soon. A group that as well as looking as the fairness thing for tax is also looking at housing affordability. And as of today is now looking at whether small businesses should have a lower tax rate. Like wot Australia has.

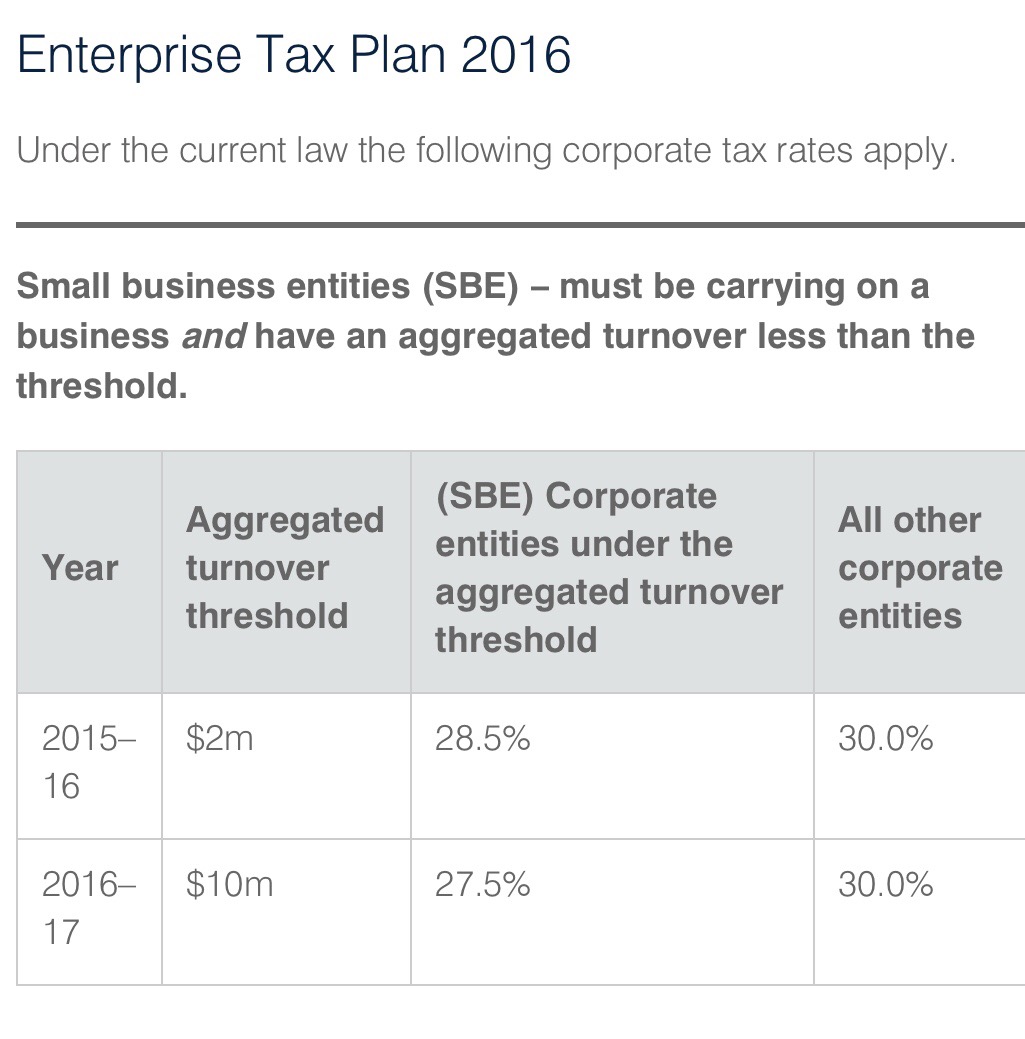

Now as hadn’t really paid any attention to this dear readers now seems like an opportune time to have a look. Apparently in 2016 the Australian government reduced the tax rate on companies with a low turnover who were in business like this:

Then they said in future years the threshold for what is small will go up and the tax rate will go down:

And then just to be fun, they introduced but didn’t pass another bill which would have reduced rates for everyone ultimately. At this point I just thank the tax gods I live in New Zealand.

Now there is a thing that if the turnover is more than 80% passive income – dividends and the like – the lower rate doesn’t apply. But 75% alg. And the turnover thing seems to have a group concept in it – so that is something. No splitting up companies – in theory anyway.

Tbh it looks like a fiscal thing. Reducing the company tax rate but it a way that doesn’t all go to the nasty big companies. Some of whom will be foreign. So will cost less than a simple company tax reduction.

Conceptually a tax cut for small business – not nasty big business – what’s not to love? The tax equivalent of free doctors visits. It does have a few downsides:

- At the margin may inhibit growth. Coz who wants to grow and get a higher tax rate?

- Incentivise passive holding companies. 80% is still pretty and

- (You guessed it) incentivise recharacterisation of other higher taxed forms of income. Aka alignment issues.

As we have discussed before dear readers – alignment matters. Whether it is misalignment of the trust and top rate or the company and the top rate. Income will gravitate to its lowest taxed form. Now if that income stays in the company and helps it grow. Alg. Effectively a tax subsidy for small business who might use this money to – say – help offset the higher minimum wage.

But it also might further incentivise the whole ‘salary at $70k’ thing; an overdrawn current account; and dodgy as dividend stripping. Because with small business the corporate veil in practice is pretty thin. The shareholders, the company and the senior employees are all the same people. And as we saw last week, small business isn’t as tax pure as maybe first thought.

The tax avoidance provision will help but is no way to run a tax system. Maybe we’ll need some tighter rules on getting money out of a company. That has merit regardless.

Will be interesting to see what the working group thinks about it.

Andrea

#shelterisforpeople

Let’s talk about tax.

Or more particularly let’s talk about the proposed Australian tax on under-utilised properties.

Now in New Zealand the big tax story is how Labour is planning to remove tax breaks from ‘speculators’. Including the best headline ever – ‘Shelter is for people – not for tax‘. Great strap line. I can see the #shelterisforpeople hashtags and possible memes. And all because they are only planning to remove negative gearing.

Now negative gearing is a term used when losses – usually from interest – from renting out a property are deducted from other taxable income. Usually income from a day job. And this kinda is a standard feature of our tax system. All income is added together and then all deductions are offset and tax is paid on the balance.

However with property a major form of income – capital gains – is not included in the calculation. So this does give a degree of tax preference – or shelter – that ordinary businesses don’t get. Is it a loophole? Dunno. Not including capital gain definitely is a loophole. But really the only way interest should actually be allowed even with including capital gains – is if they were taxed every year on an unrealised accrued basis. Now that would really be #shelterisforpeople.

And until that ever happens – no breath holding here – all that second order stuff like removing tax depreciation and negative gearing has a place. Such restrictions also probs still have merit with a realised capital gains tax as can be massive deferral benefits with that. Remember how the retirement villages don’t ever sell?

And of course in all this #shelterisforpeople stuff around negative gearing there is no mention of the other real tax breaks of:

And given the cr@p Labour is getting over this relatively mild proposal – which will only move the tax system towards fairness a tiny bit – I can’t say I blame them. Working group I guess.

And into this mix comes the recent Australian proposals to tax ‘under-utilised’ housing of foreigners. The rhetoric behind it is to free up housing for Australians. And I guess it comes off the reports of large scale empty properties in Sydney. Now recently I watched – with increasing horror – my son and his girlfriend both with incomes and references trying to find a flat in Manly. So I am totes in support of that objective – so long as ‘Australians’ can be also read as bludging Kiwi students. Not entirely sure why it is targetted at foreigners though. Coz exactly why is the nationality of the landlord relevant when the problem is that a house is empty?

Now the actual plan is to impose the charge that is levied when foreigners get permission to buy property in the first place. AUD 5,000 for a property of less than AUD 1 mill and equivalently more thereafter. And much like the Inland Revenue restructure cleverer people than me will have come up with it; but here’s what I don’t get:

- One. If someone is rich enough to own property and not need to rent it out then don’t ya think they can cope with an extra 5-10k expenditure?

- Two. Collectability. Now I get that people will pay if it is the price of getting what they want. But how exactly is this going to be collected from people who have already got the right to buy a new property? And from foreigners who by definition don’t live in Australia much? How is this going to work exactly? There are collection clauses in some treaties but this won’t be a tax covered by them.

- Three. AUD 16.5 m over next three years collected. Really? All this for just $16.5 mill?

Now if this is a big problem such a corrective tax could be put into the mix. But then it needs to be:

- A tax that is penal. So people look to change their behaviour;

- Applied to all under-utilised properties. Coz foreigners only is nuts; and

- Deemed income tax so collection clauses in treaties can be used.

Now there is no mention of an equivalent policy in the Labour stuff. Maybe under-utilised property isn’t a big problem in New Zealand? Even if Gareth does have six. But much like the Bank Levy – let’s not blindly follow the Australians. If we want one let’s make it work.

Andrea

Do ron ron

Let’s talk about tax.

Or more particularly let’s talk about the recent Australian transfer pricing case Chevron.

In a week when Inland Revenue announced a major restructure which will involve staff now needing ‘broad skill ranges’; it made me think of the type of work I used to do there – international tax.

It was true that my job needed skills other than technical ones:

- keeping your cool when being verbally attacked by the other side;

- being able to explain technical stuff to people ‘who don’t know anything about tax’ – aka anyone at Inland Revenue not in a direct tax technical function;

- ensuring the bright young ones got opportunities and didn’t get lost in the system; and

- generally ‘leveraging’ my networks to support those who were doing cutting edge stuff but not getting cut through doing things the ‘right’ way.

But otherwise what I did required a quite narrow specialised technical skill range. And that was good as it allowed me and my colleagues to focus on one particular area so we could be credible and effective. You know kinda like professional firms do?

As an aside I am not sure how this broad skill ranges thing ties in with the original business case – page 36 – which alluded to the workforce becoming more knowledge based. Coz knowledge-based work is kinda specialised not broad. But then the proposals are coming from a Commissioner who has a legal obligation to protect both the integrity of the tax system as well as the medium to long term sustainability of the department so I am sure she knows what she is doing.

Wonder what the penalties are for breaching those provisions? But I digress.

Back to me. The international tax I did though was actually quite broad compared to the work my colleagues did in transfer pricing. That was eye wateringly specialised and quite rightly so. These were the girls and boys who were on the frontline with the real multinationals like Apple, Google, Uber and the like.

And I was thinking of them recently when an appeal from an Australian transfer pricing case Chevron came out. Two wins to the Australian Commissioner and the Australian TP people – woop woo! Go them.

The guts of the case is that Chevron Australia set up a subsidiary in the US which borrowed money from third parties for – let us say – not very much and on lent it to Chevron Australia for – let us say – loads. And it was with a facility of 2.5 billion US dollars. Now you can kinda imagine the difference between not very much and loads on that was a f$cktonne of interest deductions – see why I get obsessed with interest – and therefore profit shifting from Australia to the US.

Now even though it was a subsidiary of Chevron Australia; the Australian CFC rules don’t seem to apply to the US. Coz comparatively taxed country – thank god we don’t have those rules anymore. And the judgment says it wasn’t taxed in the US either. Didn’t spell out why but I am guessing as the Australian companies are Pty ones – check the box stuff – they get grouped in the US somehow. No biggie for US but bucket loads less tax than they would otherwise pay in Australia.

And according to Chevron it was like totes legit. Coz loads is the market price for lots of really risky unsecured debt. I mean seriously dude like look up finance theory.

To which the seriously unbroad people in the Australian Tax Office said – yeah nah. Theory is like only part of it. The test is what would happen with an independent party in that situation.

- Option one – the seriously risky party ponies up with guarantees from those who aren’t seriously risky. You know how those millennials who buy houses and don’t eat smashed avocado do when their parents guarantee their loans? It is the same with big multinationals.

- Option two – banks don’t lend. So just like for all the milennials who don’t own houses but who do eat smashed avocado and don’t have rich parents.

And the Australian court thought about it all – pointed at the unbroad public servants – and said:

“What they said. Chevron you are talking b%llcocks. The arms length price is one an independent party like millennials would actually pay. This includes guarantees and you price on those facts. Not the fantasy nonsense you are spouting.”

Well broadly. Actual wording may vary. Read the judgments.

Now these are seriously useful judgments – internationally – for the whole multinationals paying their fair share thing. Let’s just hope New Zealand keeps the people who can apply them.

Andrea

Cry me a river

Let’s talk about tax. Yes dear readers – tax. No prison reform no yoga stuff. Just nice emotionally simple tax.

Or more particularly let’s talk about the recent Australian Budget announcement of a levy on banks aka the Great Australian Bank Robbery.

Your correspondent has now completed her yoga teacher training and so is available for weddings, funerals and bar/bat mischvahs. Highlights of the course included injuring herself while dancing and getting zero on the first attempt on the final exam.

It’s not like I haven’t failed things before but when the question was – reminiscent of the Peter Cook coal miners sketch – ‘who am I?‘ to fail – mmm – more than a little surreal. Now even the first time thought I had answered in a sufficiently right brained way – lots of introspective emotion involving personal power and connection with others – aahhh no.

But your correspondent is a resilient adaptive individual – even before the course – so regrouped with – ‘complete‘.

90%.

I couldn’t make this up. Subsequently found other correct answers included: me; enough – and my particular favourite – light. Ok right. Thanks for sharing.

And it all really did make me crave balance. Which in my world after eight full days on yoga is the left-brained world of tax. I had planned to write about the Australian transfer pricing case Chevron but this week has been the Australian Budget with a big new tax on their banks. And as I have had a few questions on this and I am trying to be more topical – here we go:

Now the bank tax thing seems to be part of a package of the Australian government responding to the Australian banks bad – but probs more likely monopolistic – behaviour. Also potentially a political response to appointing a popular Labour Premier – and good god a woman – to be head of the Bankers Association. And my word the banks must have been bad as they only found out about it on Budget Day and it starts on 1 July without – as far as I can see – any grandfathering.

Wow. Just wow.

So what is it?

It is a levy on big banks liabilities that aren’t:

- customer deposits or

- (tier 1) equity that doesn’t generate a tax deduction.

It targets commercial bonds, hybrid instruments (tier 2 capital) and other instruments that smaller banks can’t access coz they are small. And as it will form part of the cost of this borrowing- under normal tax principles – the levy would be tax deductible. But even allowing for this tax deduction it is supposed to raise AUD 6.2 billion over four years. So not chump change.

What is its effect?

Now there can be no argument that the levy will effectively make such instruments more expensive to use. And here the public arguments get really sophisticated:

- Malcolm Turnbull says that ‘other countries have them’ and it would be ‘unwise’ for banks to pass it on to borrowers; and

- the Treasurer Scott Morrison (ScoMo) is telling banks to ‘cry me a river’ when they have expressed a degree of displeasure.

Awesome. Thanks for playing.

Corrective taxation

Now while this is predicted to raise revenue; it is by no means clear that this is its primary objective or even if it will occur. The reason being it only applies to big banks and to certain types of liabilities. To me this looks like a form of corrective tax like cigarette excise rather than a revenue raiser like an income or consumption tax like GST.

And much like a tax on cigarettes; pollution or congestion; this tax is 100% avoidable – legitimate tax avoidance even – by funding lending with an untaxed option like customer deposits. In theory anyway. It is likely that banks will have maxxed out how much they can borrow from the public at existing interest rates.

But with this extra tax; the relativities will change. Meaning there is now scope to pay more for the untaxed deposits but less than the tax if Banks want to maintain the same level of lending. Bank costs will still go up but through marginally higher deposit rates incentivised through the tax – rather than the tax itself.

In this scenario the Australian government still gets the costs of the higher interest deduction but not the revenue. But Australian savers win.

As the big banks are the dominant players in the market – this increase in interest rates for depositors will also impact the smaller banks as they will need to pay the higher rates to continue to attract depositors too. So no actual competitive pressure from the small banks and possibly less actual tax. Genius.

An alternative equally revenue enhancing scenario is that banks wind down assets – lending – and become smaller. Less lending but higher cost of borrowing if demand stays the same.

Who bears the cost?

As they do in New Zealand anytime extra taxes are mooted; the Australian banks are arguing that these extra costs will be borne by borrowers. Now in a fully competitive market without barriers to entry the more price dependent – or elastic – the demand for loans is the more it will fall on the shareholders. But lending overall will fall with the imposition of a tax which in turn will have housing market impacts if fewer people can get a mortgage.

With barriers to entry – like hypothetically say banking regulation – they are already pricing to maximise their profit so I would be inclined to say it will also hit shareholders. And the fall in price of banking shares would indicate that is what shareholders think too.

Except that if deposit rates go up instead; the cost structure of the entire banking industry will go up. And if no tax is actually being paid but the cost is being transferred through higher deposit rates then the banking industry will have political cover to pass the cost on to borrowers.

Alternatives

Now if this schmoozle is all about the banks paying more tax then either a higher company tax rate on big banks or increasing the requirements for non- interest bearing capital would have been far simpler. While the former is pretty transparent that it is a blatant tax grab from the banks; the latter less so. They both have the advantage though of ensuring tax can’t be opted out of as well as keeping the competitive pressure from the smaller banks.

But both would form part of the banks cost structure and so – depending on the pressure from the small banks and how elastic demand is – be passed on in some form to borrowers. However if the government really wanted only the shareholders to pay then a one- off windfall tax would be the way to do it.

Whether or not the banks – and their shareholders – should actually be treated like this is another story. But Cry me a river ScoMo: at least be transparent and do it properly!

Other stuff

It goes without saying that this is truly cr@p process. All the detail seems to be in ScoMo’s press statement. Although – legislation by press statement – is an unfortunate feature of Australian tax policy.

And as for the Malcolm Turnbull ‘other countries have it too’ argument. From what I can see this was to pay back the government for the bail outs they gave the banks over the GFC. While Australia does have deposit insurance I wasn’t aware of any like actual bailouts.

It is though kinda reminiscent of the diverted profits tax which is also a targetted tax on a group of bad people. Except that might have a non-negative tax effect. Here we have – to extent it is passed on in higher deposit rates – higher costs industry wide causing less, not more, tax paid by this industry. Let’s just hope for Australia’s sake the savers are not all in the tax free threshold.

So nicely done ScoMo and Big Malc. Possibly more Lavender Hill mob than Ronnie Biggs. But much like the Australian fruit fly; keep it on your side on the Tasman. It makes even this revenue protective commentator blanch and our banking tax base can so do without it.

Andrea

Update

A commentator on the blog’s facebook page has suggested that this levy makes sense in terms of addressing the huge implicit subsidy that is the Australian deposit guarantee scheme. I have absolutely no issue with this being charged for in the form of a levy on the banks. Naively I would have thought that such a levy would then be based on the deposits covered by the guarantee not the liabilities that aren’t. Apparently that’s not how Australian politics works!

The discussion can be found in the Facebook comments section for this post.

‘You’re not one of those people are you?’

Let’s talk about tax (and tax rate alignment).

Your (foreign) correspondent is finishing up her ‘retirement cruise’ and gearing up to make that execrable journey home – also known as long distance economy class travel.

The yoga is going well too – thanks for asking – even without regular access to a studio. In large part to now knowing how alignment needs to work with my skeleton rather than that of a textbook Indian man.

So I have been thinking about this, how foreign tax systems are pretty much all misaligned, and that I promised to talk about the tail chasing stuff needed to make a higher top marginal tax rate work – or at least not not work. Because like misaligned bodies in yoga; misaligned tax systems also need props to work.

So today dear readers you get top personal tax rate alignment issues.

A couple of years ago while I was still a Treasury official I was at a social engagement and found myself talking to a Greens’ supporter. We were talking about the Christchurch earthquake and the rebuild and stuff – yes I do have all the fun – and the convo went something like this:

GS: You may remember that Russel proposed an earthquake levy as a means for the whole of the country to support Christchurch.

Me: yeah I remember that and on the face of it it did have merit – the problem is that whenever you increase the gap between the personal rates and the trust and company rate – you get people moving income into different forms. You may not collect all you think you will.

GS: [eye roll] you’re not one of those people are you? Other countries cope.

Well yeah I am ‘one of those people’. I really do like alignment and again not from a ‘purity of the tax system’ thing but because – like keeping R&D tax incentives out of the tax system – it serves us. It serves us because no matter how clever people want to get with their structuring – you always get the same result.

HOWEVER

Alignment – like a capital gains tax is not a silver bullet and – doesn’t mean:

- everyone magically starts earning income in their own names or

- income that isn’t taxed magically starts becoming taxed

It just means that there is no incentive to start finding a bunch of non-tax commercial reasons that coincidently mean current taxable income is now earned in different lower taxed forms.

But next lefty government if you do want to raise the top rate for individuals – you are going to need some tax props to stop or reduce the tax injuries. That is how othe countries cope. Have a look at page 36 of IRD’s 2005 BIM.

First thing that is beyond key is the trust or trustee tax rate. This must be raised too as income taxed at the trustee rate can be then given to beneficiaries without any more tax to pay. Australia has. All the Penny and Hooper drama happened because the trustee rate wasn’t raised too.

However there are potentially some collateral damage issues from this – aka political risk:

- Will estates

- Trusts for the ‘handicapped child’ or the disabled relative

Australia deals with these respectively by taxing at the progressive tax scale and giving the Commissioner a discretion to alter the rate. In the last – and possibly both – cases face palm. Given our tax administration’s aging computer and business transformation programme – a better option would be treating them like widely held superannuation funds and giving them the company tax rate.

You could also do something like giving them a non-refundable tax credit to get the rate back down to 33%. That technology was used in cashing out R&D losses. But this is all second order design detail and nothing officials and/or your working group can’t sort out. No biggie. It might be a bit messy but nothing compared to the carnage involved with not aligning the trust rate.

Next issue is companies and that is a bit harder. I am assuming raising the company tax rate is off the agenda – yeah thought so.

Misalignment with the company rate – as we do now – is marginally less risky as distributions from companies – dividends – are taxed in the hands of the shareholders. And they use my personal favourite technology – the withholding tax. There is currently an additional withholding tax on dividends when they are paid bringing total tax up to 33%.

You could keep the additional withholding tax at 5% and make people file who need to pay more tax – as there was no withholding at all last time there was a 33% company rate and a 39% top rate. But there also wasn’t alignment with trusts and that went well.

Or you could raise the withholding tax to – say – 11c and people who need refunds would then need to file. Or possibly a progressive withholding system from say 5c to 11c. All technically possible. But all options will raise compliance costs on taxpayers and/or administration costs on IRD. And remember the aging computer thing?

The real issue is whether our dividend rules last properly looked at almost 25 years ago can stand the strain of say a 11c difference between the company rate and top personal rate. There are ultimately limits to how long people can pay themselves $70k salaries but have a $200k lifestyle. You need to make sure you get that extra 11c when they decide to sort out that gap.

Alternatively you may like to consider making the look through company rules compulsory for all closely held companies. This would mean the company wasn’t taxed and all the income went to shareholders personally.

Neither issue will need to be part of the first 100 days tax changing under urgency that is de rigeur for new governments. It can be sorted out with consulation and will be better for it. But you will need to be prepared to use these tax props if you don’t want the 2000 – 2009 mess again.

Think that’s it.

Hardest thing will be reprioritising the existing BT and BEPS work programme to get space for this and your new fairness working group stuff.

Namaste