Let’s talk about (the recent Greens’ press statement on) tax.

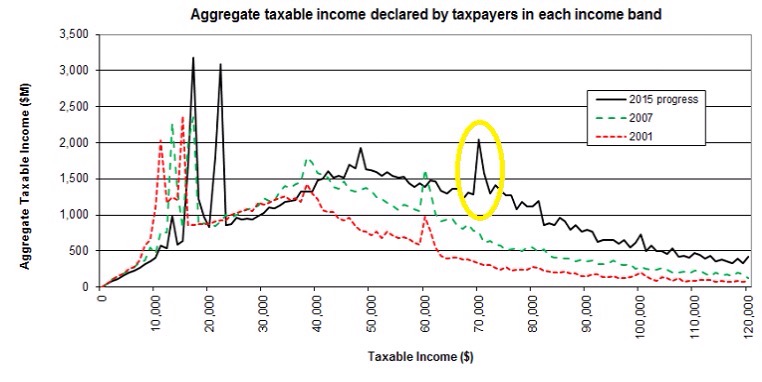

Recent data has shown there is a spike around $70,000 of reported taxable income for individuals – convienently the point where the top marginal tax rate of 33% starts. And according to the Greens this shows evidence of tax avoidance by rich people which can be fixed by – among other things – increasing Inland Revenue’s investigation budget. Mmm maybe.

Before I go on, I am working on the assumption that when the Greens talk about tax avoidance it is in the colloquial ‘not paying as much tax as I think you should’ kinda way rather than tax avoidance according to the actual law. All cool but unfortunately (or fortunately) the department is constrained by what Parliament has enacted and how the Courts have interpreted it.

Now in the mid 2000s – it is true – similar spikes were evidence of widespread tax avoidance among self-employed professionals. The wheeze was that they were employed by trusts which were taxed at 33% on the income the individuals earned – not the top individual’s rate of 39%. And then the trust paid the individuals a below market salary for their services to the trust.

Only the below market salary was taxed at 39% and the rest of the income at the lower trust rate. And then any tax paid income of the trust could then be distributed tax free to beneficiaries. Too easy and too good to be true. Hence tax avoidance according to the actual law.

Moving to 2017. The trust and top personal rate are the same so that particular wheeze won’t work. But now we just have misalignment between the company rate at 28% and the top personal rate of 33%.

Except that under a misalignment with the company rate there is no distributing the income tax free. When income is distributed from the company to the shareholder – a dividend – it is subject to another 5% tax. Now any ‘tax avoidance’ – in theory anyway – is just timing until the shareholder needs the money. There should be no ultimate reduction in tax. Although timing advantages can be a big deal and can also make something tax avoidance under the actual law.

But the only way I can see of moving this from tax avoidance – not paying as much tax as I think you should – to tax avoidance under the actual law is if the department can show that the $70k is not a market salary – as they did with the self employed professionals.

And while that wasn’t simple for the department last time – now all tax advisors know about the need for a market salary – possibly from painful personal experience. So anyone giving advice that $70k is an acceptable salary – when the market rate is higher – does so knowing it could be attacked by the department and will have all the supporting arguments ready.

But the Greens are right the spike is still there. Last time the spike was widespread tax avoidance according to the actual law – so why wouldn’t it be this time too? Not the first time I have lacked imagination.

Just in case tho I am right – I am also all about the solutions. And there is at least one way of getting rid of the spike without increasing anyone’s budget. Think of all that extra money Greens you could spend on cleaning up the rivers instead of tax inspectors.

One way is to increase the company tax rate to the top marginal rate.

Another way is to make the look-through company (LTC) rules compulsory.

Currently any company with five or fewer shareholders can choose not to be taxed as a company. Instead income and losses are taxed as if the shareholders had earned the money themselves. Except currently those rules are optional. Make them compulsory and the spike goes. No more income in more lowly taxed closely held companies as no more closely held companies for tax purposes. Simple.

And the really good news for the Greens is that there is currently a bill in the House making changes to the LTC rules; so a Supplementary Order Paper doing just that would be totes in scope. Oh and it is an ‘annual rates’ bill too so they could also have a go at the company tax rate at the same time. Awesome.

Now lots of people who haven’t made an LTC election may not like that and say so quite loudly. Coz that’s what you get when you are strong on policing tax avoidance – lots of upset people all with lots of incentive to write to you and come and tell you how upset they are.

But unless the current law with closely held companies – or company tax rate – changes I can’t see any level of increased funding will get rid of that nasty spike.

Namaste.

Hi Andrea

I reckon a different explanation for the spike could be income spitting.

That is, say a businessperson or retiree who has income from business or investments in their family trust and allocates out this income to beneficiaries (themselves, their spouse, their kids etc.) to use up any available lower tax rates rather than paying tax at 33% in the trust.

It might just be topping the spouse’s income up from say, a $55k salary by $15k to get to $70k. This is not reliant on (or able to be attacked using) market salary arguments.

It is also perceived tax avoidance rather than legal and will not be addressed by the LTC changes or company tax rate alignment you suggest.

I’d suggest that this is responsible for some of the spike at $48k too given that’s where most of the benefit is.

What do you think?

Cheers

Cam

LikeLiked by 1 person

Thanks Cam that is quite likely. And while there are ‘excessive remuneration’ provisions in the Act it is unlikely that a $55k to $70k increase would trigger them.

I still think though even with this there is still potential exposure to market salary arguments but as with Penny and Hooper it has to be quite a gap for it to have traction as a tax avoidance argument.

I guess it all comes down to how much money is being left in the company – because if it is bugger all – then there really isn’t much of an issue generally.

I guess also even if the LTC rules were made compulsory they attribute – I think – on the basis of shareholding ( or decision making powers maybe getting them confused with CfCs) so that could be squeued to low income shareholders.

Contrary to my tone in the article – there is something that isn’t right about that peak and it would be good if the Minister or IRD could come out and say they have looked into it and it is ok. Partic since the points you raise were the case in the mid 2000s and there was wide scale tax avoidance.

LikeLike

Andrea

what about the PIE regime? salary earners can salary sacrifice into super schemes to bring their incomes under $70,000. Those who earn income from investments that are PIE taxed at source don’t even have to declare the gross income. We a ctually don’t know what peoples true gross incomes are. I think that the PIE regime is highly distortionary. Why should saving by the rich be subsidized ( 28%v33%) when lower income people pay a PIE rate that reflects their actual marginal tax rate ?

LikeLiked by 1 person

You are right this will exclude any PIE income. I thought though that the worst excesses of salary sacrifice were shut down a while ago. I’ll go and look that up.

LikeLiked by 1 person

Susan this is all I could find.

http://www.ird.govt.nz/payroll-employers/make-deductions/deductions/super-contributions/esct.html

It is from 2014 but shows a superannuation tax of 33% of contributions where the contributions and salary exceed $84k.

To me this means if someone salary sacrifices – cool – but their employer pays tax at 33% on the amount of ‘sacrifice’.

But yes ongoing income on those savings will be taxed only at 28% which is concessionary.

LikeLiked by 1 person

Useful commentary thanks. But isn’t it still a bit puzzling that even after the trust and maximum personal rates were aligned the spike is almost as almost as big as it ever was? Does that lead to a reassessment of how important the trust channel actually was in 01 and 07?

LikeLiked by 1 person

No I think there needs to be some assurances that the avoidance hasn’t morphed and that the 5 cents is being paid on distribution. Albeit a bit delayed.

Because to be blunt my view that everything should be market now doesn’t tie in that well to the facts.

But I just can’t go straight to tax avoidance the way the Greens have.

LikeLike