Taxing multinationals (3) – Digital Services Tax

I had thought this might be a good post for my young friends to sub in on. But quite quickly into the conversation it became clear there would need to be too many ‘but Andrea says’ interjections to make it technically right. So we decided that I should go it alone.

Background

Now first of all the whole making multinationals pay tax thing is a bit of a comms mess so I thought I’d have a go at unpicking it.

The underlying public concern was, and is, based around large – often multinational – companies not paying enough tax. A recent article on my Twitter feed on Amazon earning $11.2 billion but paying no tax is pretty representative of the underlying concern.

Technically there were/are two reasons for this:

1) The ability to earn income without physically being in the country you earn the money from. This is primarily the digital issue.

2) Arbitraging and finding their way through different countries rules to overall lower tax paid worldwide. This is primarily an issue with foreign investment as such techniques really only worked with locally resident companies or branches.

In terms of the OECD work while it was 1) that kicked off the work – most of their action points have previously related to 2). That is – the base erosion part of base erosion and profit shifting.

In New Zealand there was a 2017 discussion document that was advanced by Judith Collins and Steven Joyce on the New Zealand specific bits of 2) which was then picked up and implemented by Stuart Nash and Grant Robertson.

And while the speech read by Michael Wood after Speaker Trevor got upset with Stuart for sitting down opens with a discussion of ‘the digital issue’, the bill was about increasing the taxation of foreign investment – ie 2) – not the tech giants. (1)

Current NZ proposal

Now Ministers Robertson and Nash have issued a discussion document proposing – maybe – a digital services tax if the OECD doesn’t get its act together.

Before we go any further one very key aspect here is the potential revenue to be raised. $30- $80 million dollars a year.

Now that may seem like a lot of money – and of course it is – but not really in tax terms. As a comparison $30 million was the projected revenue from a change to the employee shares schemes. Only insiders and my dedicated readers would even have been aware of this.

Now given the public concern and the size of the tech giants – with $30 million projected revenue – I would say either there really isn’t a problem or the base is wrong.

So what is the base? What is it that this tax will apply to?

Much like the Michael Wood/Stuart Nash speech, the problem is set out to be broad – digital economy including ecommerce (2) but then the proposed solution is narrow – digital services which rely on the participation of their user base (3).

This tax will apply to situations where the user is seen to be creating value for the company but this value is not taxed. The examples given are the content provided for YouTube and Facebook , the network effects of Google or the intermediation platforms of Uber and AirBnB.

And because of this, the base for the tax is the advertising revenue and fees charged for the intermediation services. Contrary to what the Prime Minister indicated it will not be taxing the underlying goods or services (4). It will tax the service fee of the Air BnB but not the AirBnB itself. That is already subject to tax. Well legislatively anyway.

There are some clever things in the design as, to ensure it doesn’t fall foul of WTO obligations, it applies to both foreign and New Zealand providers of such services. But then sets a de minimis such that only foreign providers are caught (5).

Officials – respect.

But then it takes this base and applies a 2-3% charge and gets $30 million. Right. Hardly seems worth it for all the anguish, compliance cost and risk of outsider status.

The other issue that seems to be missing is recognition of the value being provided to the user with the provision of a free search engine, networking sites, or email. In such cases while the user does provide value to the business in the form of their data, the user gets value back in the form of a free service.

For the business it is largely a wash. They get the value of the data but bear the cost of providing the service. That is there is no net value obtained by the business. (6)

For the individual the way the tax system works is that private costs are non deductible but private income is taxable. Yep that is assymetric but without assymetries there isn’t a tax base.

In some ways this free service is analogous to the free rent that home owners with no mortgage get – aka an imputed rent and the associated arguments for taxing it. That is the paying of rent is not deductible but the receipt of rent should be taxable.

Under this argument it is the user that should be paying tax on the value that has been transferred to them via the free service not the business. While I think the correct way to conceptualise digital businesses, taxing users is as likely as imputed rents becoming taxable.

But key thing is that the tax base is quite narrow and doesn’t pick up income from the sale or provision of goods and services from suppliers such as Apple, Amazon and Netflix. None of this is necessarily wrong as there has never been taxation on the simple sale of goods but it is a stretch to say this will meet the publics demand for the multinationals to pay more tax.

And it is true such sales are subject to GST but last time I looked GST was paid by the consumer not the business.

Technically there are also a number of issues.

The tax won’t be creditable in the residence country because it is more of a tariff than an income tax hence the concern with the WTO. It is also a poster child for high trust tax collecting as the company liable for the tax by definition has no presence in New Zealand and it is also reliant on the ultimate parent’s financial accounts for information.

This is all before you get to other countries seeing the tax as inherently illegitimate and risking retaliation.

OECD proposals

The alternative to this is what is going on at the OECD.

They have divided their work into 2 pillars.

Pillar one

Pillar one is about extending the traditional ideas of nexus or permanent establishment to include other forms of value creation.

The first proposal in this pillar is to use user contribution as a taxing right. It is similar to the base used for the digital services tax and faces the same conceptual difficulty – imho – with the value provided to users.

However unlike the DST it would be knitted into the international framework, be reciprocal and there would/should be no risk of retaliation or double taxation.

The second proposal is to extend a taxing right based on the marketing intangibles created in the user or market country. The whole concept of a marketing intangible is one I struggle with. Broadly it seems to be the value created for the company – such as customer lists or contribution to the international vibe of the product – from marketing done in the source/user/market jurisdiction.

This is a whole lot broader than the user contribution idea and has nothing really to do with the digital economy – other than it includes the digital economy.

Some commentators have suggested it is a negotiating position of the US. Robin Oliver has suggested that the US seems to be saying – if you tax Google we’ll tax BMW. In NZ what this would mean is that if we could tax Google more then China could tax Fonterra more based on marketing in China that supported the Anchor brand.

Both options explicitly exclude taxation on the basis of sales of goods or services (7).

There is a third option under this option pithily known as the significant economic presence proposal. The Ministers discussion document describes it essentially as a form of formulary apportionment that could be an equal weighting of sales, assets and employees. (8) Now that sounds quite cool.

I do wonder whether it would also be reasonable to include capital in such an equation as no business can survive without an equity base.

In the OECD discussion document they state that while revenue is a key factor it also needs one or more other things like after sales service in the market jurisdiction, volume of digital content, responsibility for final delivery or goods (9). Such tests should catch Apple and Amazon in Australia as they have a warehouse there but they are likely to be caught already with the extension of the permanent establishment rules.

It is less clear whether this would mean New Zealand could tax a portion of their profits but if that is what is wanted – this seems the best option as it is getting much closer to a form of formulary apportionment.

Pillar two

The other pillar – Pillar 2 – sets up a form of minimum taxation either for a parent when a subsidiary company has a low effective tax rate or when payments are made to associated companies with low effective tax rates. Again much broader than just the digital economy and similar to what I suggested a million years ago as an alternative to complaining about tax havens.

For high tax parents with low tax subsidiaries this is effectively an extension of the controlled foreign company rules and would bring in something like a blacklist where there could be full accrual taxation or just taxation up to the ordained minimum rate.

For high tax subsidiaries making payments to low tax sister or holding companies, they have the option of either denying a tax deduction for the payment or imposing a withholding tax. This could be useful in cases where royalties and the like are going to companies with low effective tax rates. On the face of it, it could also apply to payments for goods and services made by subsidiary companies.

It might also be effective against stories of Amazon not paying any tax – as zero is a pretty low effective tax rate.

The underlying technology seems to be based on the hybrid mismatch rules which also had an income inclusion and a deduction denial rule. Such rules were ultimately aimed at changing tax behaviour rather than explicitly collecting revenue.

Pillar 2 seems similar. If there will be clawing back of under taxation it is better to have no under taxation in the first place. So it may mean the US starts taxing more rather than subsidiary companies paying more tax.

Pillar 2 by being based around payments within a group will have no effect when there is no branch or subsidiary as is often the case with the cross border sale of goods and services to individuals .

My plea

Now the reason for all this work – both the DST and the OECD – is the issue of tax fairness and the public’s perception of fairness.

DST – imho – is really not worth it. All that risk for $30 million per year. No thank you.

But it has come about because even after the BEPS changes they still aren’t catching the underlying concern of the public – the lack of tax paid by the tech giants.

And there is no subtlety to that concern. In all my discussions no one is separating Apple, Amazon and Netflix from Google, Facebook and YouTube.

But it is time to be honest.

There are good reasons for that distinction. NZ is a small vulnerable net exporting country. Our exporters may also find themselves on the sharp end of any broader extension of taxation.

So policy makers please stop asserting the problem is the entire digital economy and then move straight to a technical discussion of a narrow solution without explaining why.

It gives the impression that more is being done than actually is. And quite frankly this will bite you on the bum when people realise what is actually going on.

And front footing an issue is Comms 101 after all.

Andrea

(1) To be fair that bill did also include a diverted profits tax light which was directed at the likes of Facebook who just do ‘sales support’ in New Zealand rather than full on sales. But that was a very minor part of the bill.

(2) Paragraphs 1.2-1.4

(3) Paragraphs 1.5 onwards

(4) I had a link for her press conference but it has been taken down. She suggested that it was only fair that if motels in NZ paid tax so should AirBnBs. I completely agree but the AirBnBs are already in the tax base and if they aren’t currently paying tax that is an enforcement issue not a DST issue.

(5) Paragraph 3.24

(6) Paragraph 60 of the OECD interim report also notes this issue.

(7) Paragraph 67

(8) Paragraph 4.47

(9) Paragraph 51

PIEs, timebar and tax fairness

My lovely young friends had a great time with their guest post last week and were delighted with the reception they received. Including getting picked up by interest.co.nz – something they like to point out I have never managed.

They were really keen to post this week on the digital services tax discussion document which they think is awesome. But I need to have a little chat to them before they do.

We also had a chat about whether the Andrea Tax Party is really a goer. Much like Alfred Ngaro we have concluded it all seems a bit hard. Also the move from thinking about things to politics hasn’t been the smoothest for TOP. So as the evidence led people that we are, we have decided to conserve our emotional energy and not fall out over boring constitutional issues.

I’ll stay as your correspondent and my young friends will come back from time to time when they can fit it in between their three jobs and studying. They are also checking out Organise Aotearoa who recently put up this sign in Auckland and seem to be to the left of Tax Justice Aotearoa.

As well as the digital services tax proposal – which I’ll save for my (briefed) young friends – the other tax story this week was how thanks to the Department upgrading its computer system it has found a number of people – 450,000 – haven’t been paying enough tax on their PIE investments. And while that is the case the Department has said that it won’t chase this tax on any past years.

Behind this story are two interesting – to me anyway – tax concepts.

Portfolio investment entities (PIEs)

These are a Michael Cullen special and came in at the same time as KiwiSaver. Before their introduction all managed funds were taxed at the trust rate of 33% and were taxed on any gains they made on shares sales – because they were in business.

Alongside all this was passive investment or index funds who had managed to convince Inland Revenue that because they only sold because they had to, those gains weren’t taxable.

Individual investors weren’t taxed on their capital gains and otherwise they were taxed at less than 33% if they had taxable income below the 33% threshold. This was particularly the case for retired investors.

The status quo did though give a minor tax benefit to high income people who were otherwise paying tax at 39%.

So it was all a bit of a hot mess.

Added into the equation was that, unlike now, the Department’s computer wasn’t up to much so all policy was based on ‘keeping people out of the system’.

So where the PIE stuff landed was income of the fund would be broken up in terms of who owned it and taxed at the rate of the owners. Except for the high earners – as their alternative was a unit trust taxed at the company rate – the top rate was capped at the company rate.

Low income people were now taxed at their own rate rather than the trust rate and high income people kept their low level tax benefit.

Happiness all round.

But it all depended on the individual investor telling the fund what the correct rate was and boy did the funds send out lots of reminders. I got totally sick of them.

Particularly when not filling them out meant you got taxed at 28% which was the top rate anyway.

So the people getting caught out this week would have once told the fund to tax them at a lower rate. It wouldn’t have happened by accident.

Although it is entirely possible they were on a lower rate at the time – because they had losses or something – and then ‘forgot’ to update it. Such people though would probably had a tax agent who would normally pick this stuff up. So not these people,

The caught people I would suggest are people, without tax agents, who accidentally or intentionally chose the wrong rate at the time or are PAYE earners whose income has increased over time and didn’t think to tell their fund.

But really only a tax audit would tell the difference between the two groups even if the effect is the same.

Time Bar

The other thing this week has shone light on is something known in the tax community as timebar (2).

It is a balance between the Government’s right to the correct amount of revenue and taxpayer’s ability to live their lives not worrying about a future tax audit. The deal is that if you have filed your tax return and provided all the necessary information – but you are wrong in the Government’s favour – Inland Revenue can only go back and increase your tax for four years.

If you haven’t filed and/or provided the necessary information – usually in cases of tax evasion – game on. The Department has no time constraints.

But the thing is none of this is an obligation on Inland Revenue. It is a right but not an obligation.

Under the Care and Management provisions (1) – the Commissioner must only collect the highest net revenue over time factoring in compliance costs and the resources available to her.

And so on that basis – I must presume – she has decided to not go back and collect tax for the last three years underpaid PIE income. In the same way he – as it was then – decided to only pursue two years of tax avoidance that arose from the Penny and Hooper tax avoidance cases.

Now I am sure this is completely above board legally in much the same way as the use of current accounts or the non-taxation of capital gains.

But with a tax fairness lens, it makes discussions with my young friends quite tricky.

They only have their personal labour which, to them, is taxed higher than I was at the same age. They don’t have capital and see this recent story as another way the tax system is slanted against them.

So I am not sure we have seen the last of the motorway signs.

Andrea

(1) Section 6A(3)

(2) Section 108

Tax and politics (2)

Kia ora koutou

Andrea has handed over to us on the youth wing of the Andrea Tax Party for this week’s blog post so we can set out our views on tax.

What she proposed is ok but we can’t help feeling it was more than a little influenced by her Gen X, neoliberal, tax free capital gain and imputed rent earning privilege. A bit like the recent Budget – more foundational than transformational.

But we have also worked out that – by definition – any capital gains tax that applied from a valuation day or worse still grandparenting would have hit any gains our generation would have earned rather than the gains that have arisen to date.

And don’t get us started about the exemption for a family home. The only members of our generation who will buy a house – with exorbitant mortgages – are those whose parents can help financially. Again more revealed Gen X privilege.

So we aren’t super sad it is off the table.

TOP are still promoting an alternative minimum tax and CPAG want to tax a risk free return on residential property. Both reasonable and we may yet move over to them but it the meantime we are seeing if we can do better.

This is what we are thinking:

Land tax on holdings over $500,000. Limited targetted exemptions.

This was a proposal under National’s tax working group (1) in 2009/10 that was also then ignored by the Government at the time.

The deal is that there would be a tax on the value of land. That’s pretty much it. There could be exemptions for conservation land, maybe land locked up for ecological services and Maori freehold land.

The last one might be controversial but we are completely over the race baiting that goes on anytime different treatment for Maori assets comes up. Settlement assets were a fraction of that taken by the Crown and until such time as Maori indicators – not the least the prison population – gets anywhere near non-Maori, we are open to different treatment to improve outcomes.

As this tax is certain what tends to happen is that the price of land falls by an NPV of the tax. The effect therefore is the same as a one off tax on existing landowners. And to be honest – we’d be open to that. Seems much lower compliance cost something Andrea and her friends get so excited about.

Now we know there is an argument that because of the effect on existing land owners – this is unfair.

However to a generation locked out of land ownership in any form due to the high prices – we are deeply underwhelmed by that argument. It was equally unfair that existing owners got the unearned gains over the last 10 years or so. And yes they might not be the same people who are affected – but again – underwhelmed.

So all holdings of land over $500,000 – other than those mentioned above – will be subject to a land tax. And honestly maybe we have the threshold too low.

GST – no change

This one causes us pain.

We really want to drop the rate as poor people spend so such more of their income than rich people. But rich people who might be living off tax free capital gains still have to buy food – and they spend more on food than poor people. So a cut in GST is – in absolute terms – a greater tax cut for the rich.

However the prevailing wisdom that increases in GST don’t matter if you increase benefits is also BS. This is for a couple of reasons:

Benefits – until this Budget kicks in – are increased by CPI but low income households have higher inflation than high income households.

Benefit increases do not survive National Governments. The associated rise in benefits from the GST introduction were unwound by the benefit cuts in 1992 and more recently benefits were eroded through changes to the administration by WINZ.

And even Andrea witnessed the changed behaviour of WINZ as she was in receipt of the Child Disability Allowance from 2007 to 2012. She went from having a super helpful empathetic case manager to having the allowance stopped when they lost her paperwork.

If anyone wants to argue instead that the last government increased benefits – bring it on – because if that is how Andrea was treated by them just imagine how WINZ behaved to people who weren’t senior public servants.

So we are recommending no change here unless there was some way of making it progressive.

Inheritance tax on all estates over $500,000

Andrea might be fixated with taxing people when they are alive but all this means is that the huge untaxed gains that have been earned get to be passed on to the next generation. And yes that might be some of us but anything to reduce the wealth inequality in New Zealand has to be considered.

We take Andrea’s point about this also applying to death of settlors (and maybe beneficiaries) but all estates over $500,000 will be taxed at the GST rate as it is inherently deferred consumption.

Make the personal tax scale more progressive

When Andrea started work in 1985 – as an almost grad – she earned $15,000 and paid $5,000 of that in tax. That is an average tax rate of 33% and probably a marginal tax rate of something like 45%.

She had no student loan because University was free. In fact she also got a bursary of about $700 three times a year. There was no GST.

Grads in 2019 start on about $50,000. Income tax is about $9,000. This is an average tax rate of about 18% and a marginal tax rate of 30%. Student loan repayments are 12% and GST is probably about 10% allowing for rent and savings. This gives a marginal tax rate of 52% which will then climb to 55% if they ever get a well paying job. So 10% higher tax than 1985 on pretty middling incomes.

We get that including student loans might upset Andrea’s tax friends but we are also guessing none of those people have 12% of their earnings going to Inland Revenue every pay day.

Team if it looks like a duck and quakes like a duck….

In fairness we also know her father in 1985 had a marginal tax rate of 66% although he got deductions for life insurance and ‘work related’ expenses. Now parents top out at 33% plus say 10% for GST – 43%.

We guess then parents should pay more but 1) not everyone has middle class parents 2) declining labour share of GDP and 3) the ones who can are already helping us and that is a recipe for entrenched privilege.

So our policy proposal is:

1) Make the changes Andrea suggests to stop all the tax avoidance and tax evasion.

2) Extend the bottom tax rate of 10.5% to $40,000

3) Increase the next tax rate to 25% from $40,000 to $70,000

4) Bring in a new threshold of 40% at $100,000

Or something like that.

The bottom threshold needs extending to include anyone who can still receive any sort of welfare benefit while also earning income. That reduction in tax then needs to be clawed back for higher earners and really high earners just need to pay more.

Emissions trading scheme

And please if there isn’t going to be any sensible carbon tax or any environmental taxes could we at least put a proper price on carbon in the Emissions Trading Scheme.

It is only human life on this planet we are talking about.

We think that is it for us. Andrea and her Gen X biases will be back next week.

Ngā mihi

Young friends of Andrea

(1) Page 50

Tax and politics

Your correspondent is back from Sydney. Had a great time because – well – Sydney.

Managed to score a gig on a panel at the TP Minds conference talking about international policy developments for transfer pricing. An interesting experience as I am pretty strong in most tax areas except GST – and you guessed it – transfer pricing.

But it was ok as I did a bit of prep and all those years of working with the TP people paid off. And of course I do know a little bit about international tax and BEPS so alg.

Even a techo tax conference again reminded me just how different – socially and culturally – Australia is to New Zealand. Examples include: the expression man in the pub being used without any sense of irony or embarrassment and one of the presenters – a senior cool woman from the ATO – wearing a hijab.

Can’t imagine either in tax circles in NZ.

My particular favourite though was watching the telly which showed a clip of Bill Shorten describing franking (imputation) credits as something you haven’t earned and a gift from the government. Now Australia does cash out franking credits but – wow – seriously just wow. Kinda puts any gripes I might have about Jacinda talking about a capital gains tax into perspective.

And in the short time I have been away yet another minor party has formed as well as the continuation of the utter dismay from progressives over the CGT announcement.

In the latter case I am fielding more than a few queries as to what the alternatives actually are to tax fairness is a world where a CGT has been ruled out pretty much for my lifetime.

Now while I have previously had a bit of a riff as to what the options could be, I have been having a think about what I would do if I were ever the ‘in charge person’ – as my kids used to say – for tax.

To become this ‘in charge person’ I guess I’d also have to set up a minor party although minor parties and tax policies are both historically pretty inimical to gaining parliamentary power.

But in for a penny – in for a pound what would be the policies of an Andrea Tax Party be?

Here goes:

Policy 1: All income of closely held companies will be taxed in the hands of its shareholders

First I’d look to getting the existing small company/shareholder tax base tidied up.

On one hand we have the whole corporate veil – companies are legally separate from their shareholders – thing. But then as the closely held shareholders control the company they can take loans from the company – which they may or may not pay interest on depending on how well IRD is enforcing the law – and take salaries from the company below the top marginal tax rate.

On the other hand we have look through company rules – which say the company and the shareholder are economically the same and so income of the company can be taxed in the hands of the shareholder instead. But because these rules are optional they will only be used if the company has losses or low levels of taxable income.

My view is that given the reality of how small companies operate – company and shareholders are in effect the same – taking down the wall for tax is the most intellectual honest thing to do. Might even raise revenue. Would defo stop the spike of income at $70,000 and most likely the escalating overdrawn current account balances.

So look through company rules – or equivalent – for all closely held companies. FWIW was pretty much the rec of the OG Tax Review 2001 (1).

Now that the tax base is sorted out – if someone wants to add another higher rate to the progressive tax scale – fill your boots. But my GenX and tbh past relatively high income earning instincts aren’t feeling it.

Policy 2: Extensive use of withholding taxes

The self employed consume 20% more at the same levels of taxable income as the employed employed. Sit with that for a minute.

20% more.

Now the self employed could have greater levels of inherited wealth, untaxed capital gains or like really awesome vegetable gardens.

Mmm yes.

Or its tax evasion. Cash jobs, not declaring income, income splitting or claiming personal expenses against taxable income.

Now in the past I have got a bit precious about the use of the term tax evasion or tax avoidance but I am happy to use the term here. This is tax evasion.

IRD says that puts New Zealand at internationally comparable levels (2). Gosh well that’s ok then.

Not putting income on a tax return needs to be hit with withholding taxes. Any payment to a provider of labour – who doesn’t employ others – needs to have withholding taxes deducted.

Cash jobs need hit by legally limiting the level of payments allowed. Australia is moving to $10,000 but why not – say $200? I mean who other than drug dealers carries that much cash anyway?

Claiming personal expenses is much harder. This we will have to rely on enforcement for.

Policy 3: Apportion interest deductions between private and business

Currently all interest deductions are allowable for companies – because compliance costs. Otherwise interest is allowed as a deduction if the funding is directly connected to a business thing.

Seems ok.

What it means though is that for someone with a small business and personal assets such as a house, all borrowing can go against the business and be fully deductible.

Options include some form of limitation like thin capitalisation or debt stacking rules. I’d be keen though on apportionment. If you have $2 million in total assets and $1 million of debt – then only 50% of the interest payable is deductible.

Policy 4: Clawback deductions where capital gains are earned

Currently so long as expenditure is connected with earning taxable income it is tax deductible. It doesn’t matter how much taxable income is actually earned or if other non-taxable income is earned as well.

Most obvious example is interest and rental income. So long as the interest is connected with the rent it is deductible even if a non-taxable capital gain is also earned.

One way of limiting this effect is the loss ringfencing rules being introduced by the government. Another way would be – when an asset or business is sold for a profit – clawback any loss offsets arising from that business or asset. Yes you would need grouping rules but the last government brought in exactly the necessary technology with its R&D cashing out losses (4).

Policy 5: Publication of tax positions

And finally just to make sure my party is never elected – taxable income and tax paid of all taxpayers – just like in Scandinavia will be published. Because if everyone is paying what they ought. Nothing to hide. And would actually give public information as to what is going on.

Options not included

What’s not there is any form of taxation of imputed income like rfrm. It isn’t a bad policy but taxing something completely independent of what has actually happened – up or down – doesn’t sit well with me.

Also no mention of inheritance tax. Again not a bad policy I’d just prefer to tax people when they are alive.

And for international tax I think keep the pressure on via the OECD because the current proposals plus what has already been enacted in New Zealand is already pretty comprehensive.

Now I know none of this is exactly exciting and so I’ll get the youth wing to do the next post.

Andrea

(1) Overview IX

(2) Paragraph 6

(3) Treatment of interest when asset held in a corporate structure

(4) Page 11 onward

Taxing multinationals (2) – the early responses

Ok. So the story so far.

The international consensus on taxing business income when there is a foreign taxpayer is: physical presence – go nuts; otherwise – back off.

And all this was totally fine when a physical presence was needed to earn business income. After the internet – not so much. And with it went source countries rights to tax such income.

Tax deductions

However none of this is say that if there is a physical presence, or investment through a New Zealand resident company, the foreign taxpayer necessarily is showering the crown accounts in gold.

As just because income is subject to tax, does not necessarily mean tax is paid.

And the difference dear readers is tax deductions. Also credits but they can stand down for this post.

Now the entry level tax deduction is interest. Intermediate and advanced include royalties, management fees and depreciation, but they can also stand down for this post.

The total wheeze about interest deductions – cross border – is that the deduction reduces tax at the company rate while the associated interest income is taxed at most at 10%. [And in my day, that didn’t always happen. So tax deduction for the payment and no tax on the income. Wizard.]

Now the Government is not a complete eejit and so in the mid 90’s thin capitalisation rules were brought in. Their gig is to limit the amount of interest deduction with reference to the financial arrangements or deductible debt compared to the assets of the company.

Originally 75% was ok but then Bill English brought that down to 60% at the same time he increased GST while decreasing the top personal rate and the company tax rate. And yes a bunch of other stuff too.

But as always there are details that don’t work out too well. And between Judith and Stuart – most got fixed. Michael Woodhouse also fixed the ‘not paying taxing on interest to foreigners’ wheeze.

There was also the most sublime way of not paying tax but in a way that had the potential for individual countries to smugly think they were ok and it was the counterparty country that was being ripped off. So good.

That is – my personal favourite – hybrids.

Until countries worked out that this meant that cross border investment paid less tax than domestic investment. Mmmm maybe not so good. So the OECD then came up with some eyewatering responses most of which were legislated for here. All quite hard. So I guess they won’t get used so much anymore. Trying not to have an adverse emotional reaction to that.

Now all of this stuff applies to foreign investment rather than multinationals per se. It most certainly affects investment from Australia to New Zealand which may be simply binational rather than multinational.

Diverted profits tax

As nature abhors a vacuum while this was being worked through at the OECD, the UK came up with its own innovation – the diverted profits tax. And at the time it galvanised the Left in a way that perplexed me. Now I see it was more of a rallying cry borne of frustration. But current Andrea is always so much smarter than past Andrea.

At the time I would often ask its advocates what that thought it was. The response I tended to get was a version of:

Inland Revenue can look at a multinational operating here and if they haven’t paid enough tax, they can work out how much income has been diverted away from New Zealand and impose the tax on that.

Ok – past Andrea would say – what you have described is a version of the general anti avoidance rule we have already – but that isn’t. What it actually is is a form of specific anti avoidance rule targetted at situations where companies are doing clever things to avoid having a physical taxable presence. [Or in the UK’s case profits to a tax haven. But dude seriously that is what CFC rules are for]

It is a pretty hard core anti avoidance rule as it imposes a tax – outside the scope of the tax treaties – far in excess of normal taxation.

And this ‘outside the scope of the tax treaties’ thing should not be underplayed. It is saying that the deals struck with other countries on taxing exactly this sort of income can be walked around. And while it is currently having a go at the US tech companies, this type of technology can easily become pointed at small vulnerable countries. All why trying for an new international consensus – and quickly – is so important.

In the end I decided explaining is losing and that I should just treat the campaign for a diverted profits tax as merely an expression of the tax fairness concern. Which in turn puts pressure on the OECD countries to do something more real.

Aka I got over myself.

In NZ we got a DPT lite. A specific anti avoidance rule inside the income tax system. I am still not sure why the general anti avoidance rule wouldn’t have picked up the clever stuff. But I am getting over myself.

Of course no form of diverted profits tax is of any use when there is no form of cleverness. It doesn’t work where there is a physical presence or when business income can be earned – totes legit – without a physical presence.

And isn’t this the real issue?

Andrea

Alignment again

Let’s tax about tax.

Or more particularly let’s talk about Australia’s proposal for a reduced tax rate for small business.

Ok yes I am excited. A new government. A Labour led government. And a young woman as a Prime Minister. Mostly what I hoped for as I climbed the millions of steps to door knock in Wellington. My left leg is almost recovered too. Thanks for asking.

And as if all of this wasn’t exciting enough two of my young friends Talia Smart and Matt Woolley won the Robin Oliver tax competition. Talia on Charities and Business and Matt on the integration of the company and personal tax. I hope to cover their papers once they become public.

Oh and Stuart Nash has won the pools and become Minister of Revenue.

So big congrats to Talia, Matt and Hon Stu. Expecting great things from you all.

We should hear about the tax working group soon. A group that as well as looking as the fairness thing for tax is also looking at housing affordability. And as of today is now looking at whether small businesses should have a lower tax rate. Like wot Australia has.

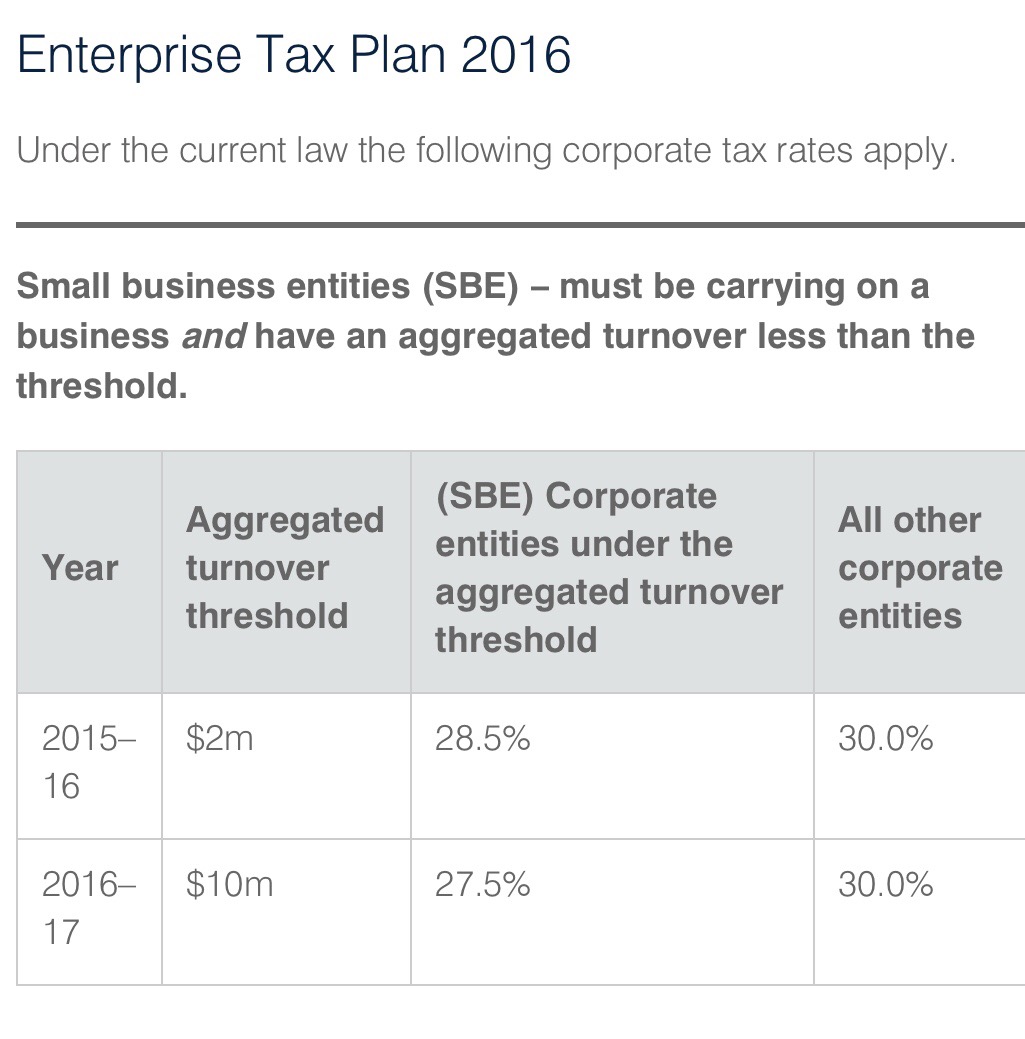

Now as hadn’t really paid any attention to this dear readers now seems like an opportune time to have a look. Apparently in 2016 the Australian government reduced the tax rate on companies with a low turnover who were in business like this:

Then they said in future years the threshold for what is small will go up and the tax rate will go down:

And then just to be fun, they introduced but didn’t pass another bill which would have reduced rates for everyone ultimately. At this point I just thank the tax gods I live in New Zealand.

Now there is a thing that if the turnover is more than 80% passive income – dividends and the like – the lower rate doesn’t apply. But 75% alg. And the turnover thing seems to have a group concept in it – so that is something. No splitting up companies – in theory anyway.

Tbh it looks like a fiscal thing. Reducing the company tax rate but it a way that doesn’t all go to the nasty big companies. Some of whom will be foreign. So will cost less than a simple company tax reduction.

Conceptually a tax cut for small business – not nasty big business – what’s not to love? The tax equivalent of free doctors visits. It does have a few downsides:

- At the margin may inhibit growth. Coz who wants to grow and get a higher tax rate?

- Incentivise passive holding companies. 80% is still pretty and

- (You guessed it) incentivise recharacterisation of other higher taxed forms of income. Aka alignment issues.

As we have discussed before dear readers – alignment matters. Whether it is misalignment of the trust and top rate or the company and the top rate. Income will gravitate to its lowest taxed form. Now if that income stays in the company and helps it grow. Alg. Effectively a tax subsidy for small business who might use this money to – say – help offset the higher minimum wage.

But it also might further incentivise the whole ‘salary at $70k’ thing; an overdrawn current account; and dodgy as dividend stripping. Because with small business the corporate veil in practice is pretty thin. The shareholders, the company and the senior employees are all the same people. And as we saw last week, small business isn’t as tax pure as maybe first thought.

The tax avoidance provision will help but is no way to run a tax system. Maybe we’ll need some tighter rules on getting money out of a company. That has merit regardless.

Will be interesting to see what the working group thinks about it.

Andrea

Stripped for action

Let’s talk about tax.

Or more particularly let’s talk about small business owners not paying the top marginal tax rate.

Well this has all taken much long than I expected.

Getting back to you dear readers. What else could I be taking about? Post election I was ready to go again but then had some family stuff to do. But I am here now.

Election night every part of my body hurt. And that was nothing to do with the result. After 24 years in Wellington – and as an ex runner – I thought I knew about hills. But after a couple of weeks of (almost) daily door knocking when (almost) every door in Wellington was up a vertical incline – I was spent. I was ready for it to be over. Win, lose or draw.

Except it still isn’t over.

But focussing on what is really important – my body has recovered and family stuff is sorted. So I can think about real tax again. Not what passes for tax in an election campaign.

Now while I was out destroying my aging body a very interesting paper was delivered at the Law Society’s annual tax conference entitled Dividend Avoidance. In that paper five ways were outlined for owners of closely held companies to get dosh out of their companies tax free. Aka not triggering the dividend rules.

Now this is very interesting for a number of reasons:

- The rhetoric that small businesses are ‘paying their fair share’ just might not be true;

- The 5 ways will only be used when have shareholders that earn more than $70k – ie not poor people;

- Only became an issue when company tax rate became 28% and

- James Shaw inadvertently outed this early this year and was told by the Minister of Revenue – and to an extent me – that there was nothing to see.

Now before we go through one of the clever – and possibly too clever – ways the top marginal tax rate isn’t being paid; a few building blocks.

BB 1

The imputation/dividend interface should mean that when value shifts from the company to the shareholder; tax not paid at the company level is paid by the shareholders. Aka #doubletaxationisgross. This includes use of losses. It doesn’t matter how tax is not paid. When it goes to the shareholder he or she should make up the difference.

BB 2

Dividends paid between companies with the same ultimate shareholders are taxfree. Coz same economic ownership so no actual value passing.

BB 3

Capital gains earned by a company can only be passed on to shareholders tax free if the company is liquidated. And liquidation should be kinda big deal. Otherwise a capital gain is simply untaxed income that will get taxed when goes to the shareholders.

BB 4

The actual market value of the company – goodwill – can only come on to the the company’s books on sale. Accounting standards quite correctly stop companies increasing their accounts for their market value. Too easy to be abused.

BB 5

Shareholders can take money out of their companies at any time. This is done through the shareholder current account. When they take out more money than they have earned it becomes negative or overdrawn. If the shareholder is also an employee they need to pay non-deductible interest on this loan.

But – in theory – this whole drawing more from your company than you actually earn should stop at some point. And then the extra 5c should be paid. Well at some stage.

The other thing to put into the mix is that following the Penny and Hooper case there will be lots of structures where a trust owned the business. You know the last time small business didn’t pay the top marginal tax rate.

The Law Society paper outlined five ways for small business to not pay the top tax rate. But I am just going to take you through one that neatly springs from the Penny and Hooper structures.

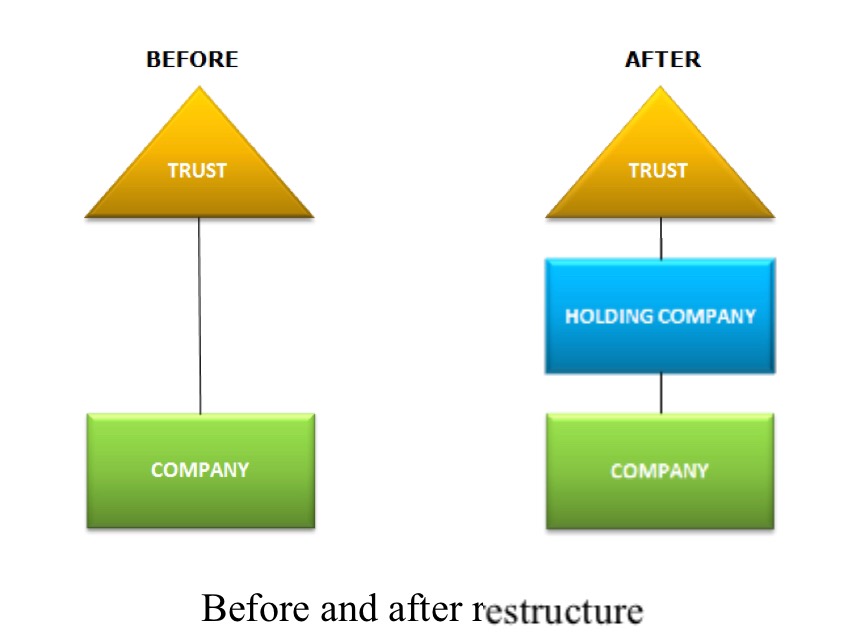

So here we are: a small business owner or professional person with what they thought was a totes legit way of progressive tax scale not applying to them. They’ve paid the back taxes to IRD and yelled at their accountant. What to do now?

Step one Trust sets up a new company – Holding Company

Step two Trust sells its shares in company – Company – wot earns money to Holding Company for its market value. This is likely to be significantly above the value shown on Company’s accounts as Goodwill is not allowed in them.

Step three Trust lends money to Holding Company for purchase. For the accountants reading this is Dr Loan to Holding Company Cr Investment in Company.

Step four Company now pays dividends to Holding Company. And who would have thought -they are now tax free and an intercompany dividend.

Step five Holding Company makes loan repayments to Trust.

Step six Trust distributes to beneficiaries tax free.

Voila! Tax is only paid at the company tax rate. No more risk of extra 5c. And even more beautifully – if tax is not paid at the company level; nothing is paid at all. So good.

Now to be fair this isn’t a permanent tax scheme as only works until loan is repaid. But then maybe the company has further increased in value and can be done again?

But arguably as the ultimate capital gain could be paid out on liquidation – it is simply timing and I should calm the F down? Nah I don’t buy that either. It is structuring into a concession. And what is that called? Yes dear readers tax avoidance.

Now there are a few other things that are kinda interesting here too:

- Really only became an issue in 2010 when the company tax rate dropped to 28%. By the same government that reduced the top tax rate to 33% because they were concerned about avoidance of the top tax rate. You can’t make these things up.

- Discovered on Investigation. And given how hard this stuff is – taking a wild guess here – by people that Inland Revenue are currently cutting the pay of or making reapply for their jobs. Again can’t make this stuff up.

I can only hope that if we ever get more than a caretaker Minister of Revenue – whomever he or she is – they get onto this stat. Because what is now really clear is that for small businesses earning more than 70k – the top tax rate is optional.

James – you were right.

Andrea

No accounting for tax

Let’s talk about tax.

Or more particularly let’s talk about accounting tax expense.

Now dear readers the most unlikely thing has happened. A tax free week in the media. No Matt Nippert on charities – just for the moment I hope – no Greens on foreign trusts. No negative gearing and – thankfully – no R&D tax credits. So with nothing topical atm – we can return to actually useful and non-reactive posts. And yes I am the arbiter of this. Although the whole Roger Douglas and his #taxesaregross does warrant a chat. Need to psyche into that a bit first though.

So I am now returning to my guilt list. Things I have been asked to write about but haven’t . That list includes land tax; estate duties; some GST things; raising company tax rate; minimum taxes; and accounting tax expense.

And so today picking from the random number generator that is my inclination – you get accounting tax expense.

At the Revenue when reviewing accounts one of the things that gets looked at is the actual tax paid compared to the accounting income. This percentage gives what is known as the effective tax rate or ETR. And yes there are differences in income and expense recognition between accounting and tax but for vanilla businesses – in practice – not as many as you would think.

Now it is true that a low ETR can at times be easily explained through untaxed foreign income or unrealised capital profits. But it is also true that for potential audits it can be a reasonable first step in working out if something is ‘wrong’. Coz like it was how the Banks tax avoidance was found. They had ETRs of like 6% or so when the statutory rate was 33%.

So when I ran into a May EY report that said foreign multinationals operating in New Zealand had ETRs around the statutory rate – I was intrigued.

Looking at it a bit more – it was clear that it was a comparison of the accounting tax expense and the accounting income. Not the actual tax paid and accounting income. Now nothing actually wrong with that comparison but possibly also not super clear cut that all is well in tax land.

And I have been promising/threatening to do a post on the difference between these two. So with nothing actually topical – aka interesting – happening this week; now looks good.

Now the first thing to note is that the tax expense in the accounts is a function of the accounting profit. So if like Facebook NZ income is arguably booked in Ireland – then as it isn’t in the revenues; it won’t be in the profits and so won’t be in the tax expense.

Second thing to note is that the purpose of the accounts is to show how the performance of the company in a year; what assets are owned and how they are funded. One key section of the accounts called Equity or Shareholders funds which shows how much of the company’s assets belong to the shareholders.

And the accounts are primarily prepared for the shareholders so they know how much of the company’s assets belong to them. Yeah banks and other peeps – such as nosey commentators – can be interested too but the accounts are still framed around analysing how the company/shareholders have made their money.

And it is in this context that the tax expense is calculated. It aims to deduct from the profit – that would otherwise increase the amount belonging to shareholders – any amount of value that will go to the consolidated fund at some stage. Worth repeating – at some stage.

First a disclaimer. When IFRS came in mid 2000s the tax accounting rules moved from really quite difficult to insanely hard and at times quite nuts. Silly is another technical term. That is they moved from an income statement to a balance sheet approach. Now because I am quite kind the rest of the post will describe the income statement approach which should give you the guts of the idea as to why they are different. Don’t try passing any exams on it though.

Now the way it is calculated is to first apply the statutory rate to the accounting profit. And it is the statutory rate of the country concerned. That is why it was a dead give away with Apple – note 16 – that they weren’t paying tax here even though they were a NZ incorporated company. The statutory rate they used was Australia’s.

Then the next step is to look for things called ‘permanent differences’. That is bits of the profit calculation that are completely outside the income tax calculation. Active foreign income from subsidiaries; capital gains and now building depreciation are but three examples. So then the tax effect of that is then deducted (or added) from the original calculation.

For Ryman – note 4 – adjusting for non-taxable income takes their tax expense from from $309 million to $3.9 million. That number then becomes the tax expense for accounting.

But there is still a bunch of stuff where the tax treatment is different:

- Interest is fully tax deductible for a company. But – if that cost is part of an asset – it is added to the cost of the asset and then depreciated for accounting. And the depreciation will cause a reduction in the profits over say – if a building – 40-50 years. So for tax interest reduces taxable profit immediately while for accounting 1/50th of it reduces accounting profits over the next 50 years.

- Replacements to parts of buildings that aren’t depreciable for tax can – like interest – receive an immediate tax deduction. But for accounting a new roof or hot water tank are added to the depreciable cost of the building and written off over the life of the asset.

- Dodgy debts from customers work the other way. Accounting takes an expense when they are merely doubtful. But for tax they have to actually be bad before they can be a tax deduction.

These things used to be known as timing differences as it was just timing between when tax and accounting recognised the expense.

And then the difference between the actual cash tax and the tax expense becomes a deferred tax asset or liability. It is an asset where more tax has been paid than the accounting expense and a liability where less tax has been paid than the expense.

And the fact that these two numbers are different does not mean anyone is being deceptive. They just have different raisons d’etre. Now if anyone wants to know how much actual tax is paid – the best places to look are the imputation account or the cash flow statement. The actual cash tax lurks in those places.

But yeah it does look like actual tax. I mean it is called tax expense.

Your correspondent has memories of the public comment when the banking cases started to leak out. I still remember one morning making breakfasts and school lunches when on Morning Report some very important banking commentator was talking. He was saying that the cases seemed surprising coz looking at the accounts the tax expense ratio seemed to be 30%. [33% stat rate at the time]. But that 3% of the accounting profits was still a large number and so possibly worthy of IRD activity.

Dude – no one would have been going after a 3% difference.

In those cases conduit tax relief on foreign income was being claimed on which NRWT was theoretically due if that foreign income were ever paid out. So because of this the tax relief being claimed never showed up in the accounts as it was like always just timing.

Except that the wheeze was there was no actual foreign income. It was all just rebadged NZ income. And yeah that income might be paid out sometime while the bank was a going concern. So it stayed as part of the tax expense. Serindipitously giving a 30% accounting effective tax rate while the actual tax effective tax rate was 6%.

And a lot of these issues are acknowledged by EY on page 13 of under ‘pitfalls’.

So yeah foreign multinationals – like their domestic counterparts – may well have accounting tax expense ratios of 28%. But whether anyone is paying their fair share though – only Inland Revenue will know.

Andrea

Roses by any other names

Let’s talk about tax.

Or more particularly let’s talk about the release of the recent government discussion documents on taxing the nasty multinationals.

You correspondent had spent the week before last on stage two of her yoga teacher training. No inner child this time but lots of describing poses in anatomical language. ‘The spine is flexed at the pelvis’ aka you bent over. Same lovely people though. Unfortunately my time on the course was punctuated by a day trip to Sydney – yes day trip – for a family funeral. I did however spend both legs watching a documentary on Oasis. So not entirely wasted. Also brought home number 2 son for a week’s visit.

So after all that I was seriously contemplating giving this week a pass too from posting. Coz like: ‘I am enough; I have enough; I do enough’ and other such lessons from the training. I was even looking for a cartoon to stand in its place:

Either:

Or possibly – as it is in colour:

But then Friday morning when I was working thru the details for a big family dinner for number 2 son and girlfriend – on comes the lovely Hon Judith Collins announcing the release of the discussion documents on taxing multinationals. Right. Ok. Mmm perhaps the cartoons won’t really cut it for Monday. But channelling my inner bureaucrat – where March counts as ‘early next year’ – Tuesday can count as Monday. Well broadly.

And the proposals are pretty good. Proper thin cap rules for finance companies are still missing but then a seven year time bar for transfer pricing! Whoa tiger. Even at my most revenue protective I’d never have thought of that. Lots of quite detailed techy stuff all which looks pretty effective to your correspondent.

On interest I am also pretty happy. No earning stripping rules but putting a cap on the interest rate should remove the structural flaw discussed previously and levelling the field by removing non- debt liabilities alg.

There is of course the small matter that with the House rising in July(?) and a Budget in May – there is no hope in hell it will even make a bill before this government finishes. Still no sign of any decisions on the Hybrids stuff that was released in September. And that is just as hard.

But if there is change in government this work will give Grant, Mike, James and Deborah an early taste of implementing fairness in the tax system. Coz there is nothing large well advised companies enjoy more than tax base protection. And they hardly ever lobby Ministers; harangue officials; brief journalists or turn up to select committees to advise them of the damage such tax measures will do to the New Zealand economy. So quite a good warm up for their fairness working group.

But I digress.

There are many and varied ways for non-residents to not pay tax with many and varied solutions. Most of which are in the discussion documents. But the one potential solution that gets all the airtime is the diverted profits tax. Which is a pretty narrow solution to a pretty narrow problem. But hey much like the iPhone 7 – irony intentional – even if our tax environment is different or our iPhone 5 is still fine – the UK and Australia have one so we want one too.

What is being proposed is the diverted profits tax equivalent of the iPhone SE – a 6 in a 5’s body. But when your existing phone really isn’t that bad.

And because it all gets so much media attention – this is the one techy thing I’ll take you through dear readers. But I am very sorry there is a bit of background to go through first. Kia Kaha. You can do it.

Source rules

All taxpayers – resident and non – resident – are taxed on income with a New Zealand source. Our source rules however were devised in 1910 or so. Long before the internet and possibly even before the typewriter. Tbh tho they aren’t that bad and periodically get a wee tweak. They are broadly comparable to other countries. They include all income from a business in New Zealand which can include foreign income as well as income from contracts completed here.

Case law however has narrowed this to income from trading in New Zealand rather than trading with New Zealand. So foreign importers selling stuff to punters here are out of scope but a business here – even an internet business – game on.

Permanent Establishment

The source rules are further narrowed by any double tax agreements. Here now New Zealand business income of a non-resident is only taxable in New Zealand if it is earned by a permanent establishment aka PE. And a PE is a fixed permanentish place of business. Once upon a time it would have been pretty hard to be a real business and not to have a fixed place of business. Possibly not so much now.

So if the non-resident earns business income through a fixed place in New Zealand – taxable – otherwise not. And for historic reasons the fixed place can’t include a warehouse. Coz that is like only preparatory or auxiliary to earning the income – not like the main deal. Yeah I don’t get it either.

Tax planning Apple and Google style

So when you put together the combo of no tax when:

- contracts not entered into in New Zealand;

- income earned from trading with New Zealand;

- no fixed place of business; and

- warehouse doesn’t count.

You kinda get the most widely known of the BEPS issues. The Google and Apple thing. Tbf I think they also use treaty shopping and inflated royalties but above is also in the mix.

Diverted Profits tax UK Style

Now a diverted profits tax doesn’t deal with the ‘trading with’ thing coz that is pretty entrenched and there are limits to anyone’s powers on that. And of course this would mean our exporters who ‘trade with’ other countries would become taxable there too. But it has a go with the other bits.

In the UK their diverted profits tax pretty much deals with situations as above where there is trading in a country and a permanent establishment should arise but doesn’t. The way it works is to say : ‘oh you know the income that would have been taxable if you hadn’t done stuff to not make it taxable – well now it is taxable.’ ‘Oh and it is like taxable at a much higher rate than normal – coz like we don’t like you doing that.’

And now New Zealand

Now in New Zealand that kind of I know you have followed the letter of the law – but dude – seriously is countered by the tax avoidance provisions. And much to the chagrin of the Foreign banks; specialist doctors; and Australian owned companies it does actually work in New Zealand.

And just because the tax avoidance provisions are being successfully applied doesn’t mean that the law shoudn’t be changed. It is a bucket load of work to investigate; dispute and then prosecute successfully. And if there are lots of cases – and there do appear to be – law changes are ultimately less resource intensive.

But even given all that I am somewhat surprised that what they have proposed is very similar to the handwavy tests of the UK. A bunch of clear questions of the structure and then asks if ‘the arrangement defeats the purpose of the DTA’s PE tests.’ Ok. Not a million miles from the parliamentary contemplation test with tax avoidance. So not entirely sure what extra protection it gives us other than being a bright shiny tax thing.

But then how different was the iPhone 6 from the iPhone 5 after all? And while the iPhone 7 is newer and flasher is it actually better?

Who knows though maybe New Zealand’s version of a diverted profits tax has a signalling benefit to the Courts. And its not like it will do any harm. So long as you don’t count additional complexity as harmful.

So all in all not bad. With the earlier Hybrids and NRWT on interest – even if the diverted profits tax equivalent may not add much – all the rest of the proposals should deal to undertaxation of non- residents.

And now residents what about them – capital gains tax anyone?

Andrea

Two men one press release

Let’s talk about tax.

Or more particularly let’s talk about Oxfam’s recent press release on inequality and tax.

Now dear readers when I moved to weekly – hah – posting it was because this blog was supposed to be my methadone programme. Getting me off tax and on to other issues. So when I posted last night – after having posted 3 times last week – I gave myself a good talking to. This had to stop. One post a week was quite enough to keep the cravings at bay. To continue in this vein would risk a relapse.

But this morning while I was getting dressed my husband came and turned on the radio. Rachel LeMesurier from Oxfam was talking about inequality and then she talked about tax and then Stephen Joyce came on and then he talked about tax and then he talked about BEPS.

Just one more little post won’t hurt I am sure and I’ll cut down next week honest.

Oxfam has compared the wealth of 2 New Zealand men Graham Hart and Richard Chandler to the bottom 30% of all adult New Zealanders. Now the inclusion of Richard Chandler seems to be a rhetorical device as from what I can tell he hasn’t lived here since 2006. So very unlikely to be resident for tax purposes.

In the interview Rachael Le M also made reference to the tax loopholes that support such wealth. So using what is public information about Graham Hart and what is public about the tax rules I thought I’d make a stab at setting out what these ‘loopholes’ are.

Now first dear readers please put out of your head anything you have heard about BEPS or diverted profit tax or any of the ways that the nasty multinationals don’t ‘pay their fair share of tax.’ None and I repeat none of this is relevant when dealing with our own people. It might be relevant for the countries they deal with but not for New Zealand. I am hoping that officials will also explain this to new MoF Steven Joyce as when he came on to reply to Rachael – he talked all about BEPS. Face palm.

Graham Hart is a serial business owner. Buying them sorting them out and then selling off the bits he doesn’t want all with a view to building up a Packaging empire. A Rank Group Debt google search also indicates that a substantial proportion of all this buying and selling was done through debt. And at times quite low quality debt which would indicate a proportionately higher interest rate. A number of his businesses are offshore.

So then what ‘loopholes’ – or gaps intended by Parliament – could Mr Hart be exploiting?

The first and most obvious one is that there is unlikely to be any tax on any of the gains made each time he sold an asset or business. The timeframes and lack of a particular pattern – as much as Dr Google can tell me – would indicate that the gains would not be taxable.

The second is that income from the active foreign businesses will be tax exempt and any dividends paid back to a New Zealand will also not be taxed. Trust me on this. I’ll take you all through this another day.

The third relates to debt. Even though it assists in the generation of capital gains and/or the exempt foreign income it will be fully deductible. Now because of the exempt foreign income there will potentially be interest restrictions if the debt of the NZ group exceeds 75% of the value of the assets. A restriction true but not an excessive one given exempt income is being earned.

Now also in Oxfam’s press statement is a reference to a third of HWIs not paying the top tax rate. I am guessing some version of one and three plus the ability to use losses from past business failures is the reason.

Unsurprisingly Eric Crampton of the New Zealand Institute is not sympathetic to Oxfam’s views and points to our housing market as the main driver of inequality. So then in terms of tax and housing the other tax ‘loophole’ then would be the exclusion of imputed rents from the tax base.

Now one answer could be Gareth’s proposal. That is if someone could explain to me how to tax ‘productive capital as measured in the capital account of the National Income Accounts’ in a world where tax is based on financial accounts according to NZIFRS.

The second could be a capital gains tax even on realisation and the third some form interest restriction or clawback when a capital gain is realised. Oh and taxing imputed rents.

How politically palatable is this? Not very given National, Labour, Act, New Zealand First and United Future are all opposed to a capital gains tax – at least Labour for their first term.

But then maybe it is stuff for Labour’s working group. Will be interested to see this all play out.

Andrea