Let’s talk about tax.

Or more particularly let’s talk about small business owners not paying the top marginal tax rate.

Well this has all taken much long than I expected.

Getting back to you dear readers. What else could I be taking about? Post election I was ready to go again but then had some family stuff to do. But I am here now.

Election night every part of my body hurt. And that was nothing to do with the result. After 24 years in Wellington – and as an ex runner – I thought I knew about hills. But after a couple of weeks of (almost) daily door knocking when (almost) every door in Wellington was up a vertical incline – I was spent. I was ready for it to be over. Win, lose or draw.

Except it still isn’t over.

But focussing on what is really important – my body has recovered and family stuff is sorted. So I can think about real tax again. Not what passes for tax in an election campaign.

Now while I was out destroying my aging body a very interesting paper was delivered at the Law Society’s annual tax conference entitled Dividend Avoidance. In that paper five ways were outlined for owners of closely held companies to get dosh out of their companies tax free. Aka not triggering the dividend rules.

Now this is very interesting for a number of reasons:

- The rhetoric that small businesses are ‘paying their fair share’ just might not be true;

- The 5 ways will only be used when have shareholders that earn more than $70k – ie not poor people;

- Only became an issue when company tax rate became 28% and

- James Shaw inadvertently outed this early this year and was told by the Minister of Revenue – and to an extent me – that there was nothing to see.

Now before we go through one of the clever – and possibly too clever – ways the top marginal tax rate isn’t being paid; a few building blocks.

BB 1

The imputation/dividend interface should mean that when value shifts from the company to the shareholder; tax not paid at the company level is paid by the shareholders. Aka #doubletaxationisgross. This includes use of losses. It doesn’t matter how tax is not paid. When it goes to the shareholder he or she should make up the difference.

BB 2

Dividends paid between companies with the same ultimate shareholders are taxfree. Coz same economic ownership so no actual value passing.

BB 3

Capital gains earned by a company can only be passed on to shareholders tax free if the company is liquidated. And liquidation should be kinda big deal. Otherwise a capital gain is simply untaxed income that will get taxed when goes to the shareholders.

BB 4

The actual market value of the company – goodwill – can only come on to the the company’s books on sale. Accounting standards quite correctly stop companies increasing their accounts for their market value. Too easy to be abused.

BB 5

Shareholders can take money out of their companies at any time. This is done through the shareholder current account. When they take out more money than they have earned it becomes negative or overdrawn. If the shareholder is also an employee they need to pay non-deductible interest on this loan.

But – in theory – this whole drawing more from your company than you actually earn should stop at some point. And then the extra 5c should be paid. Well at some stage.

The other thing to put into the mix is that following the Penny and Hooper case there will be lots of structures where a trust owned the business. You know the last time small business didn’t pay the top marginal tax rate.

The Law Society paper outlined five ways for small business to not pay the top tax rate. But I am just going to take you through one that neatly springs from the Penny and Hooper structures.

So here we are: a small business owner or professional person with what they thought was a totes legit way of progressive tax scale not applying to them. They’ve paid the back taxes to IRD and yelled at their accountant. What to do now?

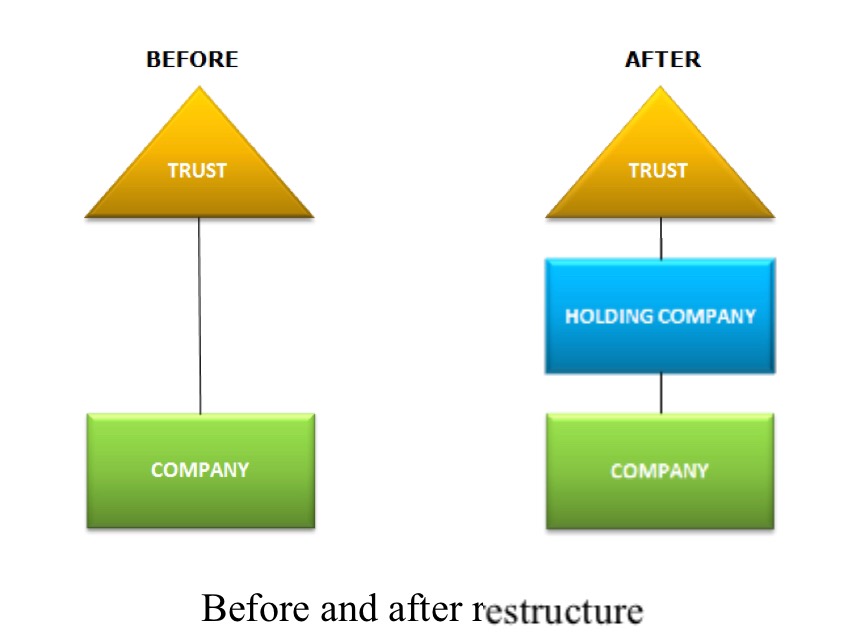

Step one Trust sets up a new company – Holding Company

Step two Trust sells its shares in company – Company – wot earns money to Holding Company for its market value. This is likely to be significantly above the value shown on Company’s accounts as Goodwill is not allowed in them.

Step three Trust lends money to Holding Company for purchase. For the accountants reading this is Dr Loan to Holding Company Cr Investment in Company.

Step four Company now pays dividends to Holding Company. And who would have thought -they are now tax free and an intercompany dividend.

Step five Holding Company makes loan repayments to Trust.

Step six Trust distributes to beneficiaries tax free.

Voila! Tax is only paid at the company tax rate. No more risk of extra 5c. And even more beautifully – if tax is not paid at the company level; nothing is paid at all. So good.

Now to be fair this isn’t a permanent tax scheme as only works until loan is repaid. But then maybe the company has further increased in value and can be done again?

But arguably as the ultimate capital gain could be paid out on liquidation – it is simply timing and I should calm the F down? Nah I don’t buy that either. It is structuring into a concession. And what is that called? Yes dear readers tax avoidance.

Now there are a few other things that are kinda interesting here too:

- Really only became an issue in 2010 when the company tax rate dropped to 28%. By the same government that reduced the top tax rate to 33% because they were concerned about avoidance of the top tax rate. You can’t make these things up.

- Discovered on Investigation. And given how hard this stuff is – taking a wild guess here – by people that Inland Revenue are currently cutting the pay of or making reapply for their jobs. Again can’t make this stuff up.

I can only hope that if we ever get more than a caretaker Minister of Revenue – whomever he or she is – they get onto this stat. Because what is now really clear is that for small businesses earning more than 70k – the top tax rate is optional.

James – you were right.

Andrea