Taxing multinationals (3) – Digital Services Tax

I had thought this might be a good post for my young friends to sub in on. But quite quickly into the conversation it became clear there would need to be too many ‘but Andrea says’ interjections to make it technically right. So we decided that I should go it alone.

Background

Now first of all the whole making multinationals pay tax thing is a bit of a comms mess so I thought I’d have a go at unpicking it.

The underlying public concern was, and is, based around large – often multinational – companies not paying enough tax. A recent article on my Twitter feed on Amazon earning $11.2 billion but paying no tax is pretty representative of the underlying concern.

Technically there were/are two reasons for this:

1) The ability to earn income without physically being in the country you earn the money from. This is primarily the digital issue.

2) Arbitraging and finding their way through different countries rules to overall lower tax paid worldwide. This is primarily an issue with foreign investment as such techniques really only worked with locally resident companies or branches.

In terms of the OECD work while it was 1) that kicked off the work – most of their action points have previously related to 2). That is – the base erosion part of base erosion and profit shifting.

In New Zealand there was a 2017 discussion document that was advanced by Judith Collins and Steven Joyce on the New Zealand specific bits of 2) which was then picked up and implemented by Stuart Nash and Grant Robertson.

And while the speech read by Michael Wood after Speaker Trevor got upset with Stuart for sitting down opens with a discussion of ‘the digital issue’, the bill was about increasing the taxation of foreign investment – ie 2) – not the tech giants. (1)

Current NZ proposal

Now Ministers Robertson and Nash have issued a discussion document proposing – maybe – a digital services tax if the OECD doesn’t get its act together.

Before we go any further one very key aspect here is the potential revenue to be raised. $30- $80 million dollars a year.

Now that may seem like a lot of money – and of course it is – but not really in tax terms. As a comparison $30 million was the projected revenue from a change to the employee shares schemes. Only insiders and my dedicated readers would even have been aware of this.

Now given the public concern and the size of the tech giants – with $30 million projected revenue – I would say either there really isn’t a problem or the base is wrong.

So what is the base? What is it that this tax will apply to?

Much like the Michael Wood/Stuart Nash speech, the problem is set out to be broad – digital economy including ecommerce (2) but then the proposed solution is narrow – digital services which rely on the participation of their user base (3).

This tax will apply to situations where the user is seen to be creating value for the company but this value is not taxed. The examples given are the content provided for YouTube and Facebook , the network effects of Google or the intermediation platforms of Uber and AirBnB.

And because of this, the base for the tax is the advertising revenue and fees charged for the intermediation services. Contrary to what the Prime Minister indicated it will not be taxing the underlying goods or services (4). It will tax the service fee of the Air BnB but not the AirBnB itself. That is already subject to tax. Well legislatively anyway.

There are some clever things in the design as, to ensure it doesn’t fall foul of WTO obligations, it applies to both foreign and New Zealand providers of such services. But then sets a de minimis such that only foreign providers are caught (5).

Officials – respect.

But then it takes this base and applies a 2-3% charge and gets $30 million. Right. Hardly seems worth it for all the anguish, compliance cost and risk of outsider status.

The other issue that seems to be missing is recognition of the value being provided to the user with the provision of a free search engine, networking sites, or email. In such cases while the user does provide value to the business in the form of their data, the user gets value back in the form of a free service.

For the business it is largely a wash. They get the value of the data but bear the cost of providing the service. That is there is no net value obtained by the business. (6)

For the individual the way the tax system works is that private costs are non deductible but private income is taxable. Yep that is assymetric but without assymetries there isn’t a tax base.

In some ways this free service is analogous to the free rent that home owners with no mortgage get – aka an imputed rent and the associated arguments for taxing it. That is the paying of rent is not deductible but the receipt of rent should be taxable.

Under this argument it is the user that should be paying tax on the value that has been transferred to them via the free service not the business. While I think the correct way to conceptualise digital businesses, taxing users is as likely as imputed rents becoming taxable.

But key thing is that the tax base is quite narrow and doesn’t pick up income from the sale or provision of goods and services from suppliers such as Apple, Amazon and Netflix. None of this is necessarily wrong as there has never been taxation on the simple sale of goods but it is a stretch to say this will meet the publics demand for the multinationals to pay more tax.

And it is true such sales are subject to GST but last time I looked GST was paid by the consumer not the business.

Technically there are also a number of issues.

The tax won’t be creditable in the residence country because it is more of a tariff than an income tax hence the concern with the WTO. It is also a poster child for high trust tax collecting as the company liable for the tax by definition has no presence in New Zealand and it is also reliant on the ultimate parent’s financial accounts for information.

This is all before you get to other countries seeing the tax as inherently illegitimate and risking retaliation.

OECD proposals

The alternative to this is what is going on at the OECD.

They have divided their work into 2 pillars.

Pillar one

Pillar one is about extending the traditional ideas of nexus or permanent establishment to include other forms of value creation.

The first proposal in this pillar is to use user contribution as a taxing right. It is similar to the base used for the digital services tax and faces the same conceptual difficulty – imho – with the value provided to users.

However unlike the DST it would be knitted into the international framework, be reciprocal and there would/should be no risk of retaliation or double taxation.

The second proposal is to extend a taxing right based on the marketing intangibles created in the user or market country. The whole concept of a marketing intangible is one I struggle with. Broadly it seems to be the value created for the company – such as customer lists or contribution to the international vibe of the product – from marketing done in the source/user/market jurisdiction.

This is a whole lot broader than the user contribution idea and has nothing really to do with the digital economy – other than it includes the digital economy.

Some commentators have suggested it is a negotiating position of the US. Robin Oliver has suggested that the US seems to be saying – if you tax Google we’ll tax BMW. In NZ what this would mean is that if we could tax Google more then China could tax Fonterra more based on marketing in China that supported the Anchor brand.

Both options explicitly exclude taxation on the basis of sales of goods or services (7).

There is a third option under this option pithily known as the significant economic presence proposal. The Ministers discussion document describes it essentially as a form of formulary apportionment that could be an equal weighting of sales, assets and employees. (8) Now that sounds quite cool.

I do wonder whether it would also be reasonable to include capital in such an equation as no business can survive without an equity base.

In the OECD discussion document they state that while revenue is a key factor it also needs one or more other things like after sales service in the market jurisdiction, volume of digital content, responsibility for final delivery or goods (9). Such tests should catch Apple and Amazon in Australia as they have a warehouse there but they are likely to be caught already with the extension of the permanent establishment rules.

It is less clear whether this would mean New Zealand could tax a portion of their profits but if that is what is wanted – this seems the best option as it is getting much closer to a form of formulary apportionment.

Pillar two

The other pillar – Pillar 2 – sets up a form of minimum taxation either for a parent when a subsidiary company has a low effective tax rate or when payments are made to associated companies with low effective tax rates. Again much broader than just the digital economy and similar to what I suggested a million years ago as an alternative to complaining about tax havens.

For high tax parents with low tax subsidiaries this is effectively an extension of the controlled foreign company rules and would bring in something like a blacklist where there could be full accrual taxation or just taxation up to the ordained minimum rate.

For high tax subsidiaries making payments to low tax sister or holding companies, they have the option of either denying a tax deduction for the payment or imposing a withholding tax. This could be useful in cases where royalties and the like are going to companies with low effective tax rates. On the face of it, it could also apply to payments for goods and services made by subsidiary companies.

It might also be effective against stories of Amazon not paying any tax – as zero is a pretty low effective tax rate.

The underlying technology seems to be based on the hybrid mismatch rules which also had an income inclusion and a deduction denial rule. Such rules were ultimately aimed at changing tax behaviour rather than explicitly collecting revenue.

Pillar 2 seems similar. If there will be clawing back of under taxation it is better to have no under taxation in the first place. So it may mean the US starts taxing more rather than subsidiary companies paying more tax.

Pillar 2 by being based around payments within a group will have no effect when there is no branch or subsidiary as is often the case with the cross border sale of goods and services to individuals .

My plea

Now the reason for all this work – both the DST and the OECD – is the issue of tax fairness and the public’s perception of fairness.

DST – imho – is really not worth it. All that risk for $30 million per year. No thank you.

But it has come about because even after the BEPS changes they still aren’t catching the underlying concern of the public – the lack of tax paid by the tech giants.

And there is no subtlety to that concern. In all my discussions no one is separating Apple, Amazon and Netflix from Google, Facebook and YouTube.

But it is time to be honest.

There are good reasons for that distinction. NZ is a small vulnerable net exporting country. Our exporters may also find themselves on the sharp end of any broader extension of taxation.

So policy makers please stop asserting the problem is the entire digital economy and then move straight to a technical discussion of a narrow solution without explaining why.

It gives the impression that more is being done than actually is. And quite frankly this will bite you on the bum when people realise what is actually going on.

And front footing an issue is Comms 101 after all.

Andrea

(1) To be fair that bill did also include a diverted profits tax light which was directed at the likes of Facebook who just do ‘sales support’ in New Zealand rather than full on sales. But that was a very minor part of the bill.

(2) Paragraphs 1.2-1.4

(3) Paragraphs 1.5 onwards

(4) I had a link for her press conference but it has been taken down. She suggested that it was only fair that if motels in NZ paid tax so should AirBnBs. I completely agree but the AirBnBs are already in the tax base and if they aren’t currently paying tax that is an enforcement issue not a DST issue.

(5) Paragraph 3.24

(6) Paragraph 60 of the OECD interim report also notes this issue.

(7) Paragraph 67

(8) Paragraph 4.47

(9) Paragraph 51

Stripped for action

Let’s talk about tax.

Or more particularly let’s talk about small business owners not paying the top marginal tax rate.

Well this has all taken much long than I expected.

Getting back to you dear readers. What else could I be taking about? Post election I was ready to go again but then had some family stuff to do. But I am here now.

Election night every part of my body hurt. And that was nothing to do with the result. After 24 years in Wellington – and as an ex runner – I thought I knew about hills. But after a couple of weeks of (almost) daily door knocking when (almost) every door in Wellington was up a vertical incline – I was spent. I was ready for it to be over. Win, lose or draw.

Except it still isn’t over.

But focussing on what is really important – my body has recovered and family stuff is sorted. So I can think about real tax again. Not what passes for tax in an election campaign.

Now while I was out destroying my aging body a very interesting paper was delivered at the Law Society’s annual tax conference entitled Dividend Avoidance. In that paper five ways were outlined for owners of closely held companies to get dosh out of their companies tax free. Aka not triggering the dividend rules.

Now this is very interesting for a number of reasons:

- The rhetoric that small businesses are ‘paying their fair share’ just might not be true;

- The 5 ways will only be used when have shareholders that earn more than $70k – ie not poor people;

- Only became an issue when company tax rate became 28% and

- James Shaw inadvertently outed this early this year and was told by the Minister of Revenue – and to an extent me – that there was nothing to see.

Now before we go through one of the clever – and possibly too clever – ways the top marginal tax rate isn’t being paid; a few building blocks.

BB 1

The imputation/dividend interface should mean that when value shifts from the company to the shareholder; tax not paid at the company level is paid by the shareholders. Aka #doubletaxationisgross. This includes use of losses. It doesn’t matter how tax is not paid. When it goes to the shareholder he or she should make up the difference.

BB 2

Dividends paid between companies with the same ultimate shareholders are taxfree. Coz same economic ownership so no actual value passing.

BB 3

Capital gains earned by a company can only be passed on to shareholders tax free if the company is liquidated. And liquidation should be kinda big deal. Otherwise a capital gain is simply untaxed income that will get taxed when goes to the shareholders.

BB 4

The actual market value of the company – goodwill – can only come on to the the company’s books on sale. Accounting standards quite correctly stop companies increasing their accounts for their market value. Too easy to be abused.

BB 5

Shareholders can take money out of their companies at any time. This is done through the shareholder current account. When they take out more money than they have earned it becomes negative or overdrawn. If the shareholder is also an employee they need to pay non-deductible interest on this loan.

But – in theory – this whole drawing more from your company than you actually earn should stop at some point. And then the extra 5c should be paid. Well at some stage.

The other thing to put into the mix is that following the Penny and Hooper case there will be lots of structures where a trust owned the business. You know the last time small business didn’t pay the top marginal tax rate.

The Law Society paper outlined five ways for small business to not pay the top tax rate. But I am just going to take you through one that neatly springs from the Penny and Hooper structures.

So here we are: a small business owner or professional person with what they thought was a totes legit way of progressive tax scale not applying to them. They’ve paid the back taxes to IRD and yelled at their accountant. What to do now?

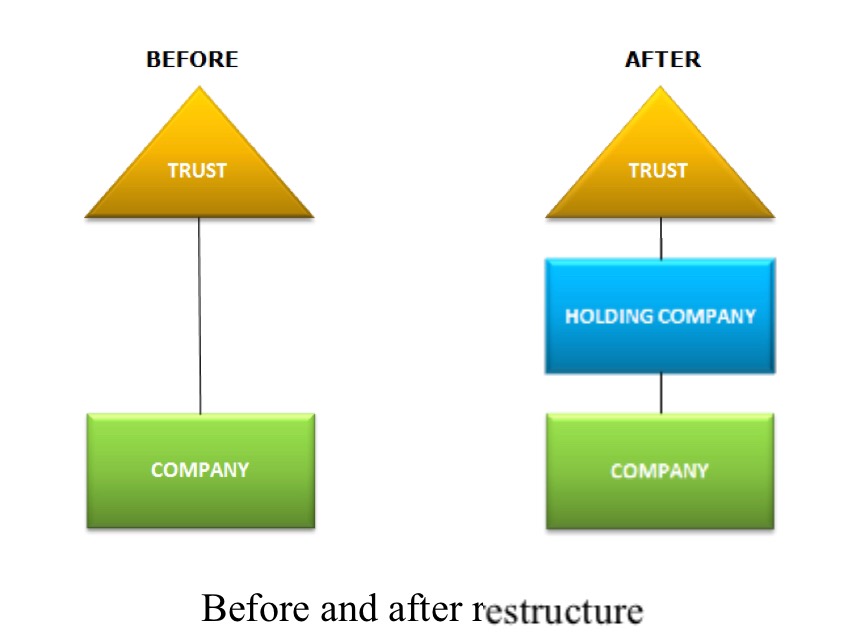

Step one Trust sets up a new company – Holding Company

Step two Trust sells its shares in company – Company – wot earns money to Holding Company for its market value. This is likely to be significantly above the value shown on Company’s accounts as Goodwill is not allowed in them.

Step three Trust lends money to Holding Company for purchase. For the accountants reading this is Dr Loan to Holding Company Cr Investment in Company.

Step four Company now pays dividends to Holding Company. And who would have thought -they are now tax free and an intercompany dividend.

Step five Holding Company makes loan repayments to Trust.

Step six Trust distributes to beneficiaries tax free.

Voila! Tax is only paid at the company tax rate. No more risk of extra 5c. And even more beautifully – if tax is not paid at the company level; nothing is paid at all. So good.

Now to be fair this isn’t a permanent tax scheme as only works until loan is repaid. But then maybe the company has further increased in value and can be done again?

But arguably as the ultimate capital gain could be paid out on liquidation – it is simply timing and I should calm the F down? Nah I don’t buy that either. It is structuring into a concession. And what is that called? Yes dear readers tax avoidance.

Now there are a few other things that are kinda interesting here too:

- Really only became an issue in 2010 when the company tax rate dropped to 28%. By the same government that reduced the top tax rate to 33% because they were concerned about avoidance of the top tax rate. You can’t make these things up.

- Discovered on Investigation. And given how hard this stuff is – taking a wild guess here – by people that Inland Revenue are currently cutting the pay of or making reapply for their jobs. Again can’t make this stuff up.

I can only hope that if we ever get more than a caretaker Minister of Revenue – whomever he or she is – they get onto this stat. Because what is now really clear is that for small businesses earning more than 70k – the top tax rate is optional.

James – you were right.

Andrea

‘I choose you – Pikachu!’

Let’s tax about tax (and hybrids).

Early in my first stint in the field I properly discovered hybrids. I was just so impressed. Impressed in a German high command discovering Enigma had been cracked kinda way – but impressed none the less. Here were instruments/entities/transfers that could render up tax benefits without tax authorities getting exercised and using words like avoidance, unacceptable or frustration. In the midst of the Structured Finance investigations to look at something so clean and so simple but so (tax) deadly was awe inspiring.

Some people may remember where they were when JFK was shot. I remember when I fully analysed my first Australian Limited Partnership – sitting at my desk at work – ticking off all the legs; finding it fully complied with Australia AND New Zealand’s law but it generated a net deduction. Like I say – completely blown away. As time went on I started to see a place for those words avoidance, unacceptable and frustration- but first love is a very special thing. Ash Ketchem may have got subsequent pokemon but Pikachu was always his first love; and the Australian Limited Partnership was my Pikachu.

And then like pokemon once you see/catch one – you start seeing them everywhere. There were your every day hybrids hiding in plain sight like the workhorse the redeemable preference share. Like Bulbasaur, solid and dependable. Deductible in Australia and imputable in New Zealand – until they weren’t. Then came blasts from the past the convertible note sisters – mandatory and optional – Squirtle and Charmander respectively. Deductible in New Zealand and not taxable in Australia. Or even the well old vehicle the New Zealand unit trust, like Snorlax always there. Loss consolidatable in Australia and New Zealand – until it wasn’t.

Charizard, or repos, played a major part in the Structured Finance transactions. Full bodied and lethal. Here legal ownership was recognised in New Zealand but not in the United States. Whoa. Definitely an evolved form.

There were also lesser known ones. The New Zealand unlimited company – like a company but with no ltd at the end. Kind of an Ekans with no tail. Company treatment in New Zealand and partnership in United States. Losses counted twice – Awesome.

And not to be out done New Zealand also created its own. The New Zealand Limited Partnership; like an Australian Limited Partnership but newer. So Raichu in other words.

There were also exotic ones. My particular favourite was the mandatory preferred partnership interest aka the redeemable preference share for limited partnerships. Like Togepie (or Jigglypuff) just so cute.

So many pokemon hybrids so little time!

But now Hons Bill and Mike have decided they should all get back in their balls; pokemongo should be deactivated; and the gameboys should be retired. Good call boys good call. Because like pokemon they were glorious but now it is time for us all to do some real work.

Namaste