Tax and small business (2) – company tax rate

Last week was a big week for your correspondent.

On Wednesday I got to upgrade my CA certificate to a FCA one at a posh dinner at Te Papa. As a third generation accountant I was absolutely tickled pink by that.

Interestingly of the 12 Wellington people there were 5 tax people: Me, Mike Shaw, Suzy Morrissey, Stewart Donaldson and Lara Ariel. All except Lara I have had the great pleasure to work with personally and professionally over the years.

I got to give a wee talk and so thanked my Wakefield (mother’s accountant line) genes; the balance sheet for being able to distinguish between the concept of capital as an asset or net equity – a framework other professions lack; and Inland Revenue Investigations as both the employer of my proposers and the place of some of the highlights of my personal and professional life.

I gave a slightly longer talk on the Tuesday. Twelve minutes instead of two.

The theme of that seminar was options to improve fairness now that extending the taxation of capital gains was off the table. The punchline of my talk was that the company tax rate should be raised.

I had come to that point following lots of feedback on my tax and small business post.

Very experienced tax people were sympathetic to my concerns but the ideas of mandating the LTCs rules or restricting interest deductions or even a weighted average small company tax rate sent them over the edge with the compliance costs involved. Their preference was that it was just simpler all round to increase the company tax rate with adjustments such as allowing the amount of deductible debt for non-residents.

And so on Tuesday I had a go at putting that argument.

Clearly not well as Michael Reddell described the argument as cavalier given NZ’s productivity issues.

Regular readers will know I am concerned about whether the tax system is a factor in New Zealand’s long tail of unproductive firms without an up or out dynamic. And that is before we get to any well meaning – but not always hitting the mark – collection of small companies tax debts inadvertently providing working capital for failing firms.

Although I had twelve minutes to talk on Tuesday, the company tax punchline really only got a minute or two to expand. So I’ll try and have a better go at it here. (1)

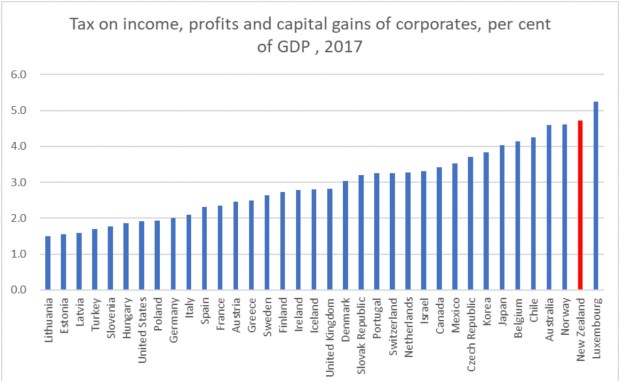

Now before we get to the arguments in favour of a company tax increase, Michael referred to this table as prima facie indicating that business income is not overtaxed.

Yep.

This table absolutely shows that second to – that other well known high tax country – Luxembourg, New Zealand’s company tax take is the highest in the OECD as a percentage of GDP.

My difficulty is that – in a New Zealand context – I struggle to call the company tax collected – a tax on business income.

Absolutely it includes business income.

But it also includes tax paid by NZ super fund – the country’s largest taxpayer and Portfolio Investment Entities which are savings entities. In other countries such income would be exempt or heavily tax preferred. And yes I know there are arguments about whether they are the correct settings or not but all that tax is currently collected as company tax.

Also, for all the vaunted advantages of imputation, the byproduct of entity neutrality is the potential blurring of returns from labour and capital for closely held companies. So – and particularly with a lower company than top personal rate – there will always be income from personal exertion taxed at the company rate.

And business income is also earned in unincorporated forms such as sole trader or partnership. All subject to the personal progressive tax scale rather than the flat company rate.

Australia’s company tax is also high but less so. Possibly a function of their lower taxation on superannuation than New Zealand or even that such income is classified according to its legal form of a trust.

And all that is before we get to issues like classical taxation in other countries encouraging small businesses to choose flow through options to avoid double taxation. An example is S Corp in the US. Tax paid under such structures will not be shown in the above numbers as the income is taxed in the hands of the shareholders.

It is true that we have a similar vehicle here in the look through company. But unsurprisingly, under imputation, this is used primarily for taxable incomes of under $10k. It is quite compliance heavy and does require tax to be paid by the shareholder while it is the company that has the underlying income and cash. But it is elective and seems to be predominantly currently used as a means of accessing corporate losses.

But back to tax fairness and company taxation.

The argument put to me by my friends – with more practical experience than I have – was: if you want to increase the level of taxation paid by the people with wealth – increase the company tax rate as that is the tax rich people pay. The logical tax rate would be the trust and top personal rate – currently 33%.

That company tax is the tax rich people pay is absolutely true. The 2016 IR work on the HWI population shows exactly that:

It would also mean that the rules that other countries have like personal services companies or accumulated earnings – that we absolutely need with a mismatch in rates – no longer become necessary.

But what about foreign investment through companies?

If the focus was New Zealanders owning closely held New Zealand businesses, an adjustment could be made either by increasing the thin capitalisation debt percentage or making a portion – most likely 5/33 – of the imputation credit refundable on distribution.

However there is also an argument not to do this. The relatively recent cut in the company tax rate has not particularly affected the level of foreign investment in New Zealand. (2)

Personally I am agnostic.

Listed companies?

Based on officials advice to the TWG (3) this group fully distributes its taxable income. So if the company tax rate increased all this would mean was that resident shareholders received a full imputation credit at 33% rather than one at 28% and withholding tax at 5%.

What happened to non-resident shareholders would depend on the decision above on non-resident investors. Either they would pay more tax on income from NZ listed companies or there could be a partially refundable imputation credit to get back to 28c.

The top PIR rate for PIEs could now also be increased to the top marginal tax rate for individuals as I keep being told the 28c rate is not a concession – more to align it with the unit trust or company tax rate. Or maybe KiwiSavers stay at 28% alongside an equivalent reduction for lower rates.

Start ups already have access to the look through company rules and so some more may access those rules if the shareholders marginal rates were below an increased company tax rate.

So an increase in the company tax rate need not have a material impact on foreign investment, listed companies and start ups.

Which then brings us to profitable closely held companies. Ones where the directors have an economic ownership of the company. A lower tax rate should, on the face of it, have allowed retained earnings and capital to grow faster. And therefore allow greater investment.

And on the face of it that is what has seemed to happen with this group. Imputation credit balances have climbed since the 28% tax rate meaning that tax paid income has not been distributed to shareholders.

However loans from such companies to their shareholders have also climbed indicating that value is still being passed on to shareholders – just not in taxable dividend form.

Now yes shareholders should be paying non-deductible – to them – interest to the company for these loans but it is more than coincidental that this increase should happen when there is a gap between the company rate and that of the trust and top personal tax rate.

And alongside this was an increase in dividend stripping as a means of clearing such loans.

So an increase in the company tax rate would reduce those avoidance opportunities and align the tax paid by incorporated and unincorporated businesses.

And with more tax collected from this sector, Business would have a strong argument for more tax spending on the things they care about. Things like tax deductions in some form for seismic strengthening, setting up a Tax Advocate, or the laundry list of business friendly initiatives that get trotted out such as removing rwt on interest paid within closely held groups.

Some of which might even be productivity enhancing.

For the next few months, I am returning to gainful – albeit non-tax – employment. As it is non-tax there should be no conflicts with this blog except for my energy and – possibly – inclination.

I am hopeful that at least two guest posts will land over this period and you may still get me in some form.

But otherwise I will be maintaining the blog’s Facebook page, and am on Twitter @andreataxyoga. I can also recommend Terry Baucher’s podcasts – the Friday Terry – when he isn’t swanning around the Northern Hemisphere.

Andrea

(1) Officials wrote a very good paper for the TWG on company tax rate issues. It can be found here: https://taxworkinggroup.govt.nz/sites/default/files/2018-09/twg-bg-appendix-2–company-tax-rate-issues.pd

(2) Paragraph 33 for a discussion of this graphs limitations. These include a reduction in the amount of deductible debt and depreciation allowances at the time of the reduction to 28% which would have worked in the opposite direction to the tax cut.

(3) Paragraph 11

Tax and Small Business

Last week the Small Business Council issued its report to Government. I am sure there are many wizard things in there maybe even some tax recs.

Also last week I had a friend to stay who is helping some workers that have lost thousands of dollars of wages and holiday pay when their employer went into receivership. Her expression was Wage Theft. It is a crime in Australia but not in New Zealand. Unlike theft as a servant which totally is.

Talking to her it was obvious that there was considerable overlap between what she is seeing and the issues considered by the TWG of closely held companies where the directors have an ownership interest not paying PAYE and GST (1).

And yes my friend’s friends are worried about their PAYE and KiwiSaver deductions. So really hope tightening up on this stuff is in the Small Business report along with the expected recs on compliance cost reduction.

I am also personally very interested in what the Group comes up with as the Productivity Commission noted that NZ has a lot of small low productivity firms without an up or out dynamic (2). That is firms tieing up capital that should be released for more productive purposes with the associated benefit of not staying on too long and dragging their workers and the tax base with them.

Now ever since I found that reference I have been concerned that there may be aspects of the tax system that may be driving that. Benefits or ‘opportunities’ that don’t arise for employees subject to PAYE or owners of widely held businesses subject to audits and outside shareholder scrutiny.

And it is true that there is nothing particularly special in a tax sense here to New Zealand. However given that New Zealand rates as number one in the ease of doing business index there may be more people going into business than would be the case in other countries.

Some of these aspects can be reduced through stricter enforcement by Inland Revenue but are otherwise largely structural in a self assessment tax system where the department doesn’t audit every taxpayer. One is a policy choice possibly because the alternative would add significant complexity to the tax system and the final example is a combination of the need for stronger enforcement and/or policy changes needed now that the company and top personal rate are destined to be permanently misaligned.

So what are these ‘aspects’?

Concealing income or deducting private expenses

Recent work by Norman Gemmell and Ana Cabal found that the self employed had 20% higher consumption than the PAYE employed at the same levels of taxable income.

Now it could be that for some reason the extra consumption of the self employed comes from inheritances or untaxed capital gains or taking loans from their business – more on that later – more so than those in the PAYE system or owners of widely held businesses. It might not be tax evasion at all.

But we just don’t know.

All we know is the 20% extra consumption and that there is a greater opportunity and fewer checks with closely held businesses to conceal income or deduct personal expenses. And Inland Revenue says such levels are comparable with other countries.

While things like greater withholding taxes and/or reporting can help, I am also concerned that with greater automation it also becomes much easier to have those personal expenses effortlessly charged against the business rather than recorded as personal drawings.

Interest Deductions

The second aspect is my specialist subject of interest deductions. Unlike concealing income or deducting personal expenditure – this one is totes legit.

Interest is fully deductible to a company and for everyone else it is deductible if it can be linked to a taxable income earning purpose or income stream aka tracing.

What that means is if a business person has a house of $2 million and a business of $1 million and has debt of $1 million – all the interest deductions on the debt can be tax deductible – if the debt can be linked to the business. This can be compared to a house of $2 million and debt of $1 million – and no business – where none of it is deductible.

To make this fairer with taxpayers who don’t have the opportunity to structure their debt there would need to be some form of apportionment over all assets – business and personal. So in the above example interest on only $330,000 should be allowed.

But yes – that would require a form of valuation of personal and business assets. And yes valuing goodwill brings up all the same – valid – concerns raised with taxing more capital gains.

So I guess we can say that under the status quo fairness – and possibly capital allocation – have been traded off against compliance costs.

Income Splitting

The third is the ability to income split with partners to take advantage of the progressive tax scale. Now this is only actually allowed if the partner is doing work for the business. But verifying the scale and degree of this work – even with burden of proof on Commissioner – is a big if not impossible task for the Commissioner.

Other mechanisms include loans from the partner to help max out the lower income tax bands.

And the statistics would support an argument that there is a degree of maxing out the lower bands just not that there necessarily is a lot of income splitting.

Interestingly both Canada and Australia have rules for personal services companies where these types of deductions are not allowed.

But this is ok if this is the amount of value going to the shareholders. Maybe our firms are so unproductive that they can only support shareholder salaries of $70k and below.

If that were the case though we wouldn’t be seeing the final aspect which is taking loans from companies you control instead of taxable dividends.

Overdrawn shareholder current accounts

Now to be fair for this to occur there should also be interest paid by the shareholder to the company on loans from the company to the shareholder. And unlike the interest in point 2 – none of this should be tax deductible to shareholder if it is funding personal expenditure while the interest received will be taxable. This on its own should be enough to not do it and receive taxable dividends instead.

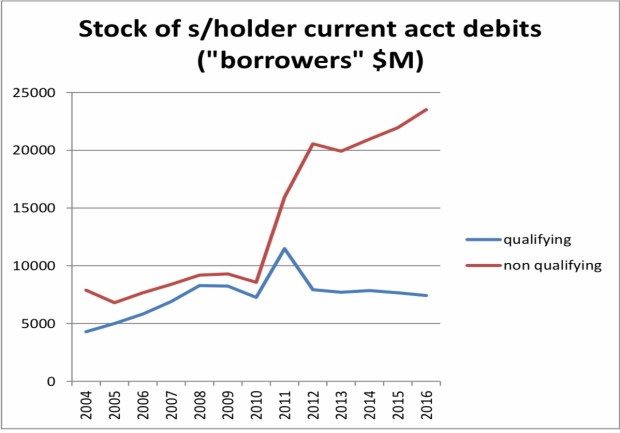

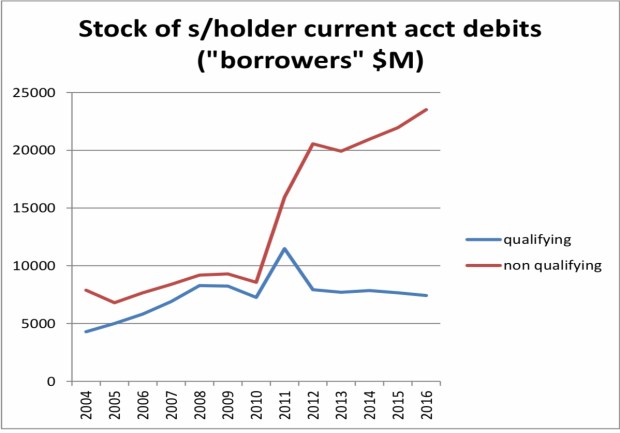

Unfortunately the facts also don’t seem to back this up. Imputation credit account balances – meaning tax has been paid but not distributed- have been climbing. Now this could be like totally awesome if it meant all the money was being retained in the company to grow.

Except that overdrawn current account balances – loans from the company to the shareholders- have been similarly growing too. Now sitting at about $25 billion.

And yes this all started from about 2010. And what happened in 2010? Why dear readers the company tax rate was cut to 28% while the trust rate remained at 33%.

Ironically the associated cut in top marginal rate was to stop the income shifting that went on between personal income and the trust rate.

Now one level it shouldn’t matter at all if these balances continue to climb so long as non- deductible assessable interest is paid on the debt. However an overdrawn current account is – imho – the gateway drug to dividend avoidance.

And yes that can be tax avoidance but much like the tax evasion opportunities, income splitting and interest on overdrawn current accounts – all of this requires enforcement by Inland Revenue. And as they can’t audit everyone there will always be a degree that is structural in a self assessment tax system.

But the underlying driver of people wanting to take loans from their company rather than imputed dividends is that our top personal tax rate and company tax rate are not the same. Paying a dividend would require another 5% tax to be paid.

Possible options

Now other countries have always had a gap between the top rate and either the company or trust rate so this shouldn’t be the end of the world. But those countries have buttressing rules that we don’t have in New Zealand. The personal services company rules discussed above or the accumulated earnings tax in the US (3) or the Australian rule that deems such loans to be dividends.

Until recently I had been a fan of making the look through company rules compulsory for any company that was currently eligible. (4) I couldn’t see the downside. The closely held business really is an extension of its shareholder so why not stop pretending and tax them correctly.

However some very kind friends have been in my ear and pointed out the difficulties of taxing the shareholder when all the income and cash to pay the tax was in the company. It works ok when it is just losses being passed through. So maybe I am less bullish now.

An alternative approach could be to apply a weighted average of the shareholders tax rates on the basis that all the income would be distributed. Similar to PIEs. The tax liability is with the entity but the rate is based on the shareholders. I guess you then do a mock distribution to the shareholders which can then be distributed to them tax free. And yes only to closely held companies. Wider would be a nightmare.

Kind of a PIE meets LTC.

Or you could just old school it and raise the company tax rate to 33% for all companies. Shareholders with tax rates below that could use the LTC rules and make the assessment of whether the compliance of the rules was greater or less than the extra tax.

It would require an adjustment to the thin capitalisation rules by increasing the deductible debt levels to ensure foreign investment didn’t pay more tax. But for some of you dear readers increased taxation on foreign investment might even be a plus.

But all in all I don’t think the status quo with small business is a goer. Whether it is for fairness reasons, or capital allocation reasons or simply stopping me worrying – doing something is a really good idea.

Because I would hate to think any of this was enabling behaviours that kept people in business longer than they should. And even with the most whizziest of new IRD computers – there will always be limits on enforcement.

Andrea

(1) Page 116 Paragraph 68

(2) Page 19

(3) Although it would make more sense to only apply this to the extend that the income hasn’t been retained in the business and distributed in non- dividend form.

(4) Yes there is the issue that companies could start adding an extra class of share to get around this. But I don’t believe this is insurmountable with de minimis levels of additional categories and the odd antiavoidance rule for good measure. It is even the advice of KPMG so clearly not that wacky.

Source country taxation, the environment and oil rigs

Last week sometime I found myself in a Twitter discussion with PEPANZ – of all people – as they were saying the TWG had supported the recent extension of the tax exemption for oil rigs. It is an exemption that is theoretically timelimited for non-resident companies involved in exploration and development activities in an offshore permit area. Theoretically because it will have been in force for 20 years if it actually does expire this time.

Having been a little involved with the TWG – as well as the Treasury official on the last rollover – I was somewhat surprised by PEPANZ’s comment. But in the end they were referring to an Officials paper for the TWG rather than a TWG paper per se. A subtle and easily missed difference.

And one they unfortunately also made in their submission to the Finance and Expenditure Committee (1). Although it was a little odd that they needed to make a submission as everyone has known for 5 years that the exemption was expiring.

But in that thread PEPANZ encouraged people to read the Cabinet paper and so for old time sake I did. The analysis was quite familiar to me but the thing that gave me pause was the fiscal consequences were said to be positive.

Yes positive.

Implementing a tax exemption would increase the tax take. A veritable tax unicorn.

No wonder it had such support. I guess this exemption will now have to come off the tax expenditure statement.

Personally I am not a fan of this exemption or its extension. And although I accept the prevailing arguments – much like the difference between a paper for the TWG and a paper of the TWG – it is less clear cut than it seems.

International framework for taxing income from natural resources

Now followers of the digital tax debate will know all about how source countries can tax profits earned in their country if these profits are earned through a physical presence in their country aka permanent establishment. And because it is super easy to earn profits from digital services without a permanent establishment there is a problem.

However for land or natural resource based industries a physical presence is – by definition – super easy.

And if you properly read treaties there is a really strong vibe through the individual articles that source countries keep all profits from its physical environment (2) while returns from intellectual property belong to the residence or investor country.

So before tax fairness or stopping multinational tax evasion was a thing, there was source country taxing rights based on natural resources.

Then to make it super super clear Article 5(2)(f) of the model treaty makes a well or a mine a permanent establishment just in case there was any argument.

To be fair to our friends the visiting oil rigs, other than the physical environment vibe there is no actual mention of exploration in the model article. But the commentary says it is up to individual countries how they wish to handle this. (3)

What does New Zealand do?

The best one to look at is the US treaty. In that exploration is specifically included as creating a permanent establishment but periods of up to 6 months are also specifically excluded (4).

This is interesting for two reasons.

First the negotiators of the treaty clearly specifically wanted exploration to create a taxing right as this paragraph is not in the model treaty. Secondly it stayed in the treaty even after a protocol was negotiated in 2010. That is if this provision and the 6 month carve out were a ‘bad’ thing for New Zealand it would have made sense for it to have come out at that point. Either unilaterally or as a tradeoff for something else.

So in other words anything to do with the taxation of oil rigs involved in exploration cannot be considered to be a glitch with the treaty that could be fixed with renegotiation. Unless of course it was oversight in the 2010 negotiations.

What are the facts?

The optimal commercial period for these rigs to be in New Zealand seems to be about 8 months. That is two months or so too long to access the exemption. But rather than pay tax they will leave and another rig will come in with associated extra costs and environmental damage.

This is what was happening before the exemption came into place in 2004 and so does prima facie seem a reasonable case for just having an outright exemption. However:

The 2019 Regulatory Impact Statement says that the contracts have a tax indemnity clause meaning that any tax payable by the non-resident company must be paid by the New Zealand permit holder. (5)

This means that the outcomes would be broadly similar to this table. This is on the basis that rigs could be substituted albeit with delay at additional cost rather than exploration simply being deferred to another year. (6)

Why don’t I like the exemption?

Much like the difference between TWG reports and reports for the TWG it is all pretty nuanced.

Pre 2004, as there were tax indemnities, the only reason to have the rigs leave and another one come in was if the cost to the company of the churning was less than the cost – paying the tax – of the rig staying put.

However while that would be a completely reasonable business decision for the company it is highest cost for the country as a whole and the highest cost to the tax base of all the options.

And so the argument for an exemption was framed. An exemption lowers the cost to the Crown and also to the company. Win Win.

However the tax base does best in a world without the exemption but where the rigs stay put and the company pays the non-resident operators tax.

Now requiring that would be somewhat stalinist but it does feel that Government has had its hand forced when it wasn’t party to any of the original decisions. The Government has no control over the cost structure of the industry but:

- Needs to exempt income of a class of non-resident at a time when it is looking to expand taxing rights over other non-residents;

- Weakens its claim on the tax base associated with natural resources,

- Gets offside with a major stakeholder of its confidence and supply partner.

And all of this is before you get to the precedential risk associated with moving away from the otherwise broad base low rate framework. Which by definition involves winners and losers.

I am also not convinced by the revenue positive argument. The RIS states that as the exemption has been going on forever the forecasts have already factored in the exemption (7). This means an extension of the exemption has no fiscal effect.

However by the time it gets to the Cabinet Paper – albeit close to a year after the RIS was signed off – a $4 million cost of not extending the exemption has now been incorporated into the forecasts (8). And so – hey presto by extending the exemption – an equivalent revenue benefit arises that can go on the scorecard (9). From which other revenue negative tax policy changes can be funded.

Every Minister of Revenue’s dream.

So like I said – not a fan. There is a narrow supporting argument. Absolutely. But the whole thing makes me very uncomfortable. To make matters worse – it is only extended for 5 years. It hasn’t been made permanent. Even after 20 years. SMH.

Hope I am doing something else in 5 years time.

Andrea

(1) Curiously officials write up of the submission in the Departmental report page 171 is far more fulsome than the written submission. I guess it must reflect an empassioned verbal submission from PEPANZ.

(2) Article 6 of the model treaty makes this explicit without any reference to a permanent establishment.

(3) Paragraph 48 Page 128

(4) Article 5(4)

(5) Paragraph 6. This comment isn’t the the recent RIS but as the analysis is based around the New Zealand permit holder wearing the additional costs associated changing the non-resident operator it is reasonable to assume that equivalent clauses are in the new contracts.

(6) Section 2.3 of RIS discusses the delays associated with changing operators.

(7) Page 11

(8) Paragraphs 21-23

(9) Section 4.6

Taxing multinationals (3) – Digital Services Tax

I had thought this might be a good post for my young friends to sub in on. But quite quickly into the conversation it became clear there would need to be too many ‘but Andrea says’ interjections to make it technically right. So we decided that I should go it alone.

Background

Now first of all the whole making multinationals pay tax thing is a bit of a comms mess so I thought I’d have a go at unpicking it.

The underlying public concern was, and is, based around large – often multinational – companies not paying enough tax. A recent article on my Twitter feed on Amazon earning $11.2 billion but paying no tax is pretty representative of the underlying concern.

Technically there were/are two reasons for this:

1) The ability to earn income without physically being in the country you earn the money from. This is primarily the digital issue.

2) Arbitraging and finding their way through different countries rules to overall lower tax paid worldwide. This is primarily an issue with foreign investment as such techniques really only worked with locally resident companies or branches.

In terms of the OECD work while it was 1) that kicked off the work – most of their action points have previously related to 2). That is – the base erosion part of base erosion and profit shifting.

In New Zealand there was a 2017 discussion document that was advanced by Judith Collins and Steven Joyce on the New Zealand specific bits of 2) which was then picked up and implemented by Stuart Nash and Grant Robertson.

And while the speech read by Michael Wood after Speaker Trevor got upset with Stuart for sitting down opens with a discussion of ‘the digital issue’, the bill was about increasing the taxation of foreign investment – ie 2) – not the tech giants. (1)

Current NZ proposal

Now Ministers Robertson and Nash have issued a discussion document proposing – maybe – a digital services tax if the OECD doesn’t get its act together.

Before we go any further one very key aspect here is the potential revenue to be raised. $30- $80 million dollars a year.

Now that may seem like a lot of money – and of course it is – but not really in tax terms. As a comparison $30 million was the projected revenue from a change to the employee shares schemes. Only insiders and my dedicated readers would even have been aware of this.

Now given the public concern and the size of the tech giants – with $30 million projected revenue – I would say either there really isn’t a problem or the base is wrong.

So what is the base? What is it that this tax will apply to?

Much like the Michael Wood/Stuart Nash speech, the problem is set out to be broad – digital economy including ecommerce (2) but then the proposed solution is narrow – digital services which rely on the participation of their user base (3).

This tax will apply to situations where the user is seen to be creating value for the company but this value is not taxed. The examples given are the content provided for YouTube and Facebook , the network effects of Google or the intermediation platforms of Uber and AirBnB.

And because of this, the base for the tax is the advertising revenue and fees charged for the intermediation services. Contrary to what the Prime Minister indicated it will not be taxing the underlying goods or services (4). It will tax the service fee of the Air BnB but not the AirBnB itself. That is already subject to tax. Well legislatively anyway.

There are some clever things in the design as, to ensure it doesn’t fall foul of WTO obligations, it applies to both foreign and New Zealand providers of such services. But then sets a de minimis such that only foreign providers are caught (5).

Officials – respect.

But then it takes this base and applies a 2-3% charge and gets $30 million. Right. Hardly seems worth it for all the anguish, compliance cost and risk of outsider status.

The other issue that seems to be missing is recognition of the value being provided to the user with the provision of a free search engine, networking sites, or email. In such cases while the user does provide value to the business in the form of their data, the user gets value back in the form of a free service.

For the business it is largely a wash. They get the value of the data but bear the cost of providing the service. That is there is no net value obtained by the business. (6)

For the individual the way the tax system works is that private costs are non deductible but private income is taxable. Yep that is assymetric but without assymetries there isn’t a tax base.

In some ways this free service is analogous to the free rent that home owners with no mortgage get – aka an imputed rent and the associated arguments for taxing it. That is the paying of rent is not deductible but the receipt of rent should be taxable.

Under this argument it is the user that should be paying tax on the value that has been transferred to them via the free service not the business. While I think the correct way to conceptualise digital businesses, taxing users is as likely as imputed rents becoming taxable.

But key thing is that the tax base is quite narrow and doesn’t pick up income from the sale or provision of goods and services from suppliers such as Apple, Amazon and Netflix. None of this is necessarily wrong as there has never been taxation on the simple sale of goods but it is a stretch to say this will meet the publics demand for the multinationals to pay more tax.

And it is true such sales are subject to GST but last time I looked GST was paid by the consumer not the business.

Technically there are also a number of issues.

The tax won’t be creditable in the residence country because it is more of a tariff than an income tax hence the concern with the WTO. It is also a poster child for high trust tax collecting as the company liable for the tax by definition has no presence in New Zealand and it is also reliant on the ultimate parent’s financial accounts for information.

This is all before you get to other countries seeing the tax as inherently illegitimate and risking retaliation.

OECD proposals

The alternative to this is what is going on at the OECD.

They have divided their work into 2 pillars.

Pillar one

Pillar one is about extending the traditional ideas of nexus or permanent establishment to include other forms of value creation.

The first proposal in this pillar is to use user contribution as a taxing right. It is similar to the base used for the digital services tax and faces the same conceptual difficulty – imho – with the value provided to users.

However unlike the DST it would be knitted into the international framework, be reciprocal and there would/should be no risk of retaliation or double taxation.

The second proposal is to extend a taxing right based on the marketing intangibles created in the user or market country. The whole concept of a marketing intangible is one I struggle with. Broadly it seems to be the value created for the company – such as customer lists or contribution to the international vibe of the product – from marketing done in the source/user/market jurisdiction.

This is a whole lot broader than the user contribution idea and has nothing really to do with the digital economy – other than it includes the digital economy.

Some commentators have suggested it is a negotiating position of the US. Robin Oliver has suggested that the US seems to be saying – if you tax Google we’ll tax BMW. In NZ what this would mean is that if we could tax Google more then China could tax Fonterra more based on marketing in China that supported the Anchor brand.

Both options explicitly exclude taxation on the basis of sales of goods or services (7).

There is a third option under this option pithily known as the significant economic presence proposal. The Ministers discussion document describes it essentially as a form of formulary apportionment that could be an equal weighting of sales, assets and employees. (8) Now that sounds quite cool.

I do wonder whether it would also be reasonable to include capital in such an equation as no business can survive without an equity base.

In the OECD discussion document they state that while revenue is a key factor it also needs one or more other things like after sales service in the market jurisdiction, volume of digital content, responsibility for final delivery or goods (9). Such tests should catch Apple and Amazon in Australia as they have a warehouse there but they are likely to be caught already with the extension of the permanent establishment rules.

It is less clear whether this would mean New Zealand could tax a portion of their profits but if that is what is wanted – this seems the best option as it is getting much closer to a form of formulary apportionment.

Pillar two

The other pillar – Pillar 2 – sets up a form of minimum taxation either for a parent when a subsidiary company has a low effective tax rate or when payments are made to associated companies with low effective tax rates. Again much broader than just the digital economy and similar to what I suggested a million years ago as an alternative to complaining about tax havens.

For high tax parents with low tax subsidiaries this is effectively an extension of the controlled foreign company rules and would bring in something like a blacklist where there could be full accrual taxation or just taxation up to the ordained minimum rate.

For high tax subsidiaries making payments to low tax sister or holding companies, they have the option of either denying a tax deduction for the payment or imposing a withholding tax. This could be useful in cases where royalties and the like are going to companies with low effective tax rates. On the face of it, it could also apply to payments for goods and services made by subsidiary companies.

It might also be effective against stories of Amazon not paying any tax – as zero is a pretty low effective tax rate.

The underlying technology seems to be based on the hybrid mismatch rules which also had an income inclusion and a deduction denial rule. Such rules were ultimately aimed at changing tax behaviour rather than explicitly collecting revenue.

Pillar 2 seems similar. If there will be clawing back of under taxation it is better to have no under taxation in the first place. So it may mean the US starts taxing more rather than subsidiary companies paying more tax.

Pillar 2 by being based around payments within a group will have no effect when there is no branch or subsidiary as is often the case with the cross border sale of goods and services to individuals .

My plea

Now the reason for all this work – both the DST and the OECD – is the issue of tax fairness and the public’s perception of fairness.

DST – imho – is really not worth it. All that risk for $30 million per year. No thank you.

But it has come about because even after the BEPS changes they still aren’t catching the underlying concern of the public – the lack of tax paid by the tech giants.

And there is no subtlety to that concern. In all my discussions no one is separating Apple, Amazon and Netflix from Google, Facebook and YouTube.

But it is time to be honest.

There are good reasons for that distinction. NZ is a small vulnerable net exporting country. Our exporters may also find themselves on the sharp end of any broader extension of taxation.

So policy makers please stop asserting the problem is the entire digital economy and then move straight to a technical discussion of a narrow solution without explaining why.

It gives the impression that more is being done than actually is. And quite frankly this will bite you on the bum when people realise what is actually going on.

And front footing an issue is Comms 101 after all.

Andrea

(1) To be fair that bill did also include a diverted profits tax light which was directed at the likes of Facebook who just do ‘sales support’ in New Zealand rather than full on sales. But that was a very minor part of the bill.

(2) Paragraphs 1.2-1.4

(3) Paragraphs 1.5 onwards

(4) I had a link for her press conference but it has been taken down. She suggested that it was only fair that if motels in NZ paid tax so should AirBnBs. I completely agree but the AirBnBs are already in the tax base and if they aren’t currently paying tax that is an enforcement issue not a DST issue.

(5) Paragraph 3.24

(6) Paragraph 60 of the OECD interim report also notes this issue.

(7) Paragraph 67

(8) Paragraph 4.47

(9) Paragraph 51

PIEs, timebar and tax fairness

My lovely young friends had a great time with their guest post last week and were delighted with the reception they received. Including getting picked up by interest.co.nz – something they like to point out I have never managed.

They were really keen to post this week on the digital services tax discussion document which they think is awesome. But I need to have a little chat to them before they do.

We also had a chat about whether the Andrea Tax Party is really a goer. Much like Alfred Ngaro we have concluded it all seems a bit hard. Also the move from thinking about things to politics hasn’t been the smoothest for TOP. So as the evidence led people that we are, we have decided to conserve our emotional energy and not fall out over boring constitutional issues.

I’ll stay as your correspondent and my young friends will come back from time to time when they can fit it in between their three jobs and studying. They are also checking out Organise Aotearoa who recently put up this sign in Auckland and seem to be to the left of Tax Justice Aotearoa.

As well as the digital services tax proposal – which I’ll save for my (briefed) young friends – the other tax story this week was how thanks to the Department upgrading its computer system it has found a number of people – 450,000 – haven’t been paying enough tax on their PIE investments. And while that is the case the Department has said that it won’t chase this tax on any past years.

Behind this story are two interesting – to me anyway – tax concepts.

Portfolio investment entities (PIEs)

These are a Michael Cullen special and came in at the same time as KiwiSaver. Before their introduction all managed funds were taxed at the trust rate of 33% and were taxed on any gains they made on shares sales – because they were in business.

Alongside all this was passive investment or index funds who had managed to convince Inland Revenue that because they only sold because they had to, those gains weren’t taxable.

Individual investors weren’t taxed on their capital gains and otherwise they were taxed at less than 33% if they had taxable income below the 33% threshold. This was particularly the case for retired investors.

The status quo did though give a minor tax benefit to high income people who were otherwise paying tax at 39%.

So it was all a bit of a hot mess.

Added into the equation was that, unlike now, the Department’s computer wasn’t up to much so all policy was based on ‘keeping people out of the system’.

So where the PIE stuff landed was income of the fund would be broken up in terms of who owned it and taxed at the rate of the owners. Except for the high earners – as their alternative was a unit trust taxed at the company rate – the top rate was capped at the company rate.

Low income people were now taxed at their own rate rather than the trust rate and high income people kept their low level tax benefit.

Happiness all round.

But it all depended on the individual investor telling the fund what the correct rate was and boy did the funds send out lots of reminders. I got totally sick of them.

Particularly when not filling them out meant you got taxed at 28% which was the top rate anyway.

So the people getting caught out this week would have once told the fund to tax them at a lower rate. It wouldn’t have happened by accident.

Although it is entirely possible they were on a lower rate at the time – because they had losses or something – and then ‘forgot’ to update it. Such people though would probably had a tax agent who would normally pick this stuff up. So not these people,

The caught people I would suggest are people, without tax agents, who accidentally or intentionally chose the wrong rate at the time or are PAYE earners whose income has increased over time and didn’t think to tell their fund.

But really only a tax audit would tell the difference between the two groups even if the effect is the same.

Time Bar

The other thing this week has shone light on is something known in the tax community as timebar (2).

It is a balance between the Government’s right to the correct amount of revenue and taxpayer’s ability to live their lives not worrying about a future tax audit. The deal is that if you have filed your tax return and provided all the necessary information – but you are wrong in the Government’s favour – Inland Revenue can only go back and increase your tax for four years.

If you haven’t filed and/or provided the necessary information – usually in cases of tax evasion – game on. The Department has no time constraints.

But the thing is none of this is an obligation on Inland Revenue. It is a right but not an obligation.

Under the Care and Management provisions (1) – the Commissioner must only collect the highest net revenue over time factoring in compliance costs and the resources available to her.

And so on that basis – I must presume – she has decided to not go back and collect tax for the last three years underpaid PIE income. In the same way he – as it was then – decided to only pursue two years of tax avoidance that arose from the Penny and Hooper tax avoidance cases.

Now I am sure this is completely above board legally in much the same way as the use of current accounts or the non-taxation of capital gains.

But with a tax fairness lens, it makes discussions with my young friends quite tricky.

They only have their personal labour which, to them, is taxed higher than I was at the same age. They don’t have capital and see this recent story as another way the tax system is slanted against them.

So I am not sure we have seen the last of the motorway signs.

Andrea

(1) Section 6A(3)

(2) Section 108

Tax and politics (2)

Kia ora koutou

Andrea has handed over to us on the youth wing of the Andrea Tax Party for this week’s blog post so we can set out our views on tax.

What she proposed is ok but we can’t help feeling it was more than a little influenced by her Gen X, neoliberal, tax free capital gain and imputed rent earning privilege. A bit like the recent Budget – more foundational than transformational.

But we have also worked out that – by definition – any capital gains tax that applied from a valuation day or worse still grandparenting would have hit any gains our generation would have earned rather than the gains that have arisen to date.

And don’t get us started about the exemption for a family home. The only members of our generation who will buy a house – with exorbitant mortgages – are those whose parents can help financially. Again more revealed Gen X privilege.

So we aren’t super sad it is off the table.

TOP are still promoting an alternative minimum tax and CPAG want to tax a risk free return on residential property. Both reasonable and we may yet move over to them but it the meantime we are seeing if we can do better.

This is what we are thinking:

Land tax on holdings over $500,000. Limited targetted exemptions.

This was a proposal under National’s tax working group (1) in 2009/10 that was also then ignored by the Government at the time.

The deal is that there would be a tax on the value of land. That’s pretty much it. There could be exemptions for conservation land, maybe land locked up for ecological services and Maori freehold land.

The last one might be controversial but we are completely over the race baiting that goes on anytime different treatment for Maori assets comes up. Settlement assets were a fraction of that taken by the Crown and until such time as Maori indicators – not the least the prison population – gets anywhere near non-Maori, we are open to different treatment to improve outcomes.

As this tax is certain what tends to happen is that the price of land falls by an NPV of the tax. The effect therefore is the same as a one off tax on existing landowners. And to be honest – we’d be open to that. Seems much lower compliance cost something Andrea and her friends get so excited about.

Now we know there is an argument that because of the effect on existing land owners – this is unfair.

However to a generation locked out of land ownership in any form due to the high prices – we are deeply underwhelmed by that argument. It was equally unfair that existing owners got the unearned gains over the last 10 years or so. And yes they might not be the same people who are affected – but again – underwhelmed.

So all holdings of land over $500,000 – other than those mentioned above – will be subject to a land tax. And honestly maybe we have the threshold too low.

GST – no change

This one causes us pain.

We really want to drop the rate as poor people spend so such more of their income than rich people. But rich people who might be living off tax free capital gains still have to buy food – and they spend more on food than poor people. So a cut in GST is – in absolute terms – a greater tax cut for the rich.

However the prevailing wisdom that increases in GST don’t matter if you increase benefits is also BS. This is for a couple of reasons:

Benefits – until this Budget kicks in – are increased by CPI but low income households have higher inflation than high income households.

Benefit increases do not survive National Governments. The associated rise in benefits from the GST introduction were unwound by the benefit cuts in 1992 and more recently benefits were eroded through changes to the administration by WINZ.

And even Andrea witnessed the changed behaviour of WINZ as she was in receipt of the Child Disability Allowance from 2007 to 2012. She went from having a super helpful empathetic case manager to having the allowance stopped when they lost her paperwork.

If anyone wants to argue instead that the last government increased benefits – bring it on – because if that is how Andrea was treated by them just imagine how WINZ behaved to people who weren’t senior public servants.

So we are recommending no change here unless there was some way of making it progressive.

Inheritance tax on all estates over $500,000

Andrea might be fixated with taxing people when they are alive but all this means is that the huge untaxed gains that have been earned get to be passed on to the next generation. And yes that might be some of us but anything to reduce the wealth inequality in New Zealand has to be considered.

We take Andrea’s point about this also applying to death of settlors (and maybe beneficiaries) but all estates over $500,000 will be taxed at the GST rate as it is inherently deferred consumption.

Make the personal tax scale more progressive

When Andrea started work in 1985 – as an almost grad – she earned $15,000 and paid $5,000 of that in tax. That is an average tax rate of 33% and probably a marginal tax rate of something like 45%.

She had no student loan because University was free. In fact she also got a bursary of about $700 three times a year. There was no GST.

Grads in 2019 start on about $50,000. Income tax is about $9,000. This is an average tax rate of about 18% and a marginal tax rate of 30%. Student loan repayments are 12% and GST is probably about 10% allowing for rent and savings. This gives a marginal tax rate of 52% which will then climb to 55% if they ever get a well paying job. So 10% higher tax than 1985 on pretty middling incomes.

We get that including student loans might upset Andrea’s tax friends but we are also guessing none of those people have 12% of their earnings going to Inland Revenue every pay day.

Team if it looks like a duck and quakes like a duck….

In fairness we also know her father in 1985 had a marginal tax rate of 66% although he got deductions for life insurance and ‘work related’ expenses. Now parents top out at 33% plus say 10% for GST – 43%.

We guess then parents should pay more but 1) not everyone has middle class parents 2) declining labour share of GDP and 3) the ones who can are already helping us and that is a recipe for entrenched privilege.

So our policy proposal is:

1) Make the changes Andrea suggests to stop all the tax avoidance and tax evasion.

2) Extend the bottom tax rate of 10.5% to $40,000

3) Increase the next tax rate to 25% from $40,000 to $70,000

4) Bring in a new threshold of 40% at $100,000

Or something like that.

The bottom threshold needs extending to include anyone who can still receive any sort of welfare benefit while also earning income. That reduction in tax then needs to be clawed back for higher earners and really high earners just need to pay more.

Emissions trading scheme

And please if there isn’t going to be any sensible carbon tax or any environmental taxes could we at least put a proper price on carbon in the Emissions Trading Scheme.

It is only human life on this planet we are talking about.

We think that is it for us. Andrea and her Gen X biases will be back next week.

Ngā mihi

Young friends of Andrea

(1) Page 50

Online shopping

Taking a break from TWG report proper stuff for a bit. Although very pleased to see that when the government said no further work on a Tax Advocate they actually meant no further work except for its inclusion in a soon discussion document.

Silly me and everyone else. Clearly misread the Government’s response. Recommendation 73 but getting over myself …

And there has just been a tax bill passed back in the (tax) real world.

R&D tax credits which seems largely to be a grants based system administered by IRD (1) and not anything I would recognise as a tax credit. But hey all the benefits of a grant while still calling it a tax thing. What’s not to love.

And coming up strongly behind is the GST and low value goods bill which also has the loss ring fencing for residential rental property.

Now the latter is pretty much loathed by the tax community. But as interest deductions in the face of untaxed capital gains is a bit of specialist subject/anguish for your correspondent I may write some more on that. As with no more capital gains being taxed I would say this is technology that should get a broader look.

But today I am going to have a bit of a chat about the GST stuff. Now as your correspondent’s taste in clothes tends toward vintage reproduction, she is a big online shopper from relatively obscure American and now Swedish suppliers. And my one piece of tax avoidance has always been keeping purchases below $225 so that no GST would be triggered. Often a struggle – albeit a financially useful one – when the NZ dollar is weak.

Now the $225 comes from the $60 de minimis Customs has where it won’t collect tax and duty up to that amount coz the admin to do so would be higher than the tax collected. So for clothes and shoes – another specialist subject but no anguish here – as there is a duty of 10% when you work it back this means $225 of clothes and shoes can be imported free of taxation and while for everything else it is $400.

And yeah it is not a total free ride as there is postage involved and if things don’t fit sending things back is probs not worth it.

Now this implicit tax exemption is only ever an administrative thing. It wasn’t like Parliament ever said ‘Off you go Andrea, have a foreign tax free dress, just keep it under $225 and only one at a time mind’. And so I have been expecting this loophole to be closed since forever.

And now there is a bill to do just that a select committee. The vibe is that offshore suppliers will collect GST for goods under $1000 and Customs over $1000. Cool. So far so good.

Except…

First it is the poster child for high trust tax collecting. It requires the offshore supplier to register with IRD, collect GST and then pay it to the department. Three steps where – just saying – something might go wrong. Would hate to think I pay GST and it isn’t passed on. But for the big guys at least they face ‘reputational risk’ if things go wrong.

Now yes we do have the bright, shiny, newish Convention of Mutual Administrative Assistance (2) that does include GST and yes the Department has tried hard to make the whole thing simple so yes the big people should get caught/ and or voluntarily comply.

2) Suppliers paying to GST registered buyers don’t have to charge coz that would be compliance without tax. Fair enough but I am now GST registered, how will the offshore supplier know my single dress isn’t just like a sample? Or will they even care so long as they have an IRD number?

3) Offshore suppliers only have to register if they are selling more than NZD 60k to people who aren’t GST registered. And yes this is self assessed by taxpayers outside out tax base.

But how will IRD know if the supplier or I am not compliant? There really will be limits to the whole Convention for Mutual Assistance. And anyway if they sell less than $60k no GST is totes legit.

But ultimately none of this should matter as any tax not collected by the offshore supplier will be picked up by Customs. Except …

4) De minimis raised to $1000 value of item for goods not GSTed by supplier. Sorry wot? So if GST is not charged – correctly by my new obscure foreign retailer – or incorrectly because reputational risk isn’t a thing for them – my GST free band has increased? Yup.

SMH.

To be fair this is all sort of covered in the RIS (3) but I can’t find anything that discusses why the de minimis or threshold had to be increased.

Interestingly the Tax Working Group explicitly looked at these issues and concluded that the de minimis should only be NZD 400. And this is the right answer particularly when fairness is the lens. Although I would have thought there was now a case to bring the de minimis right down to incentivise collecting at source.

It is true that all the marketplaces and Youshops will get caught but anyone like me with any form of obscure foreign importing – which I am guessing is much like capital gains and a feature of a higher income/wealth profile – can now buy more tax free than before.

And why this is important is that the official primary reason for this policy change was to increase the fairness of the tax system. Not efficiency or even revenue but fairness.

And the thing about increasing fairness is that it might not reduce administrative costs. It might not improve the customer experience. But it says that tax is paid by everyone not just when it is easy to collect and people don’t get upset with you.

So a day or so after discovering I won’t be taxed on capital gains, surely I am not also up for more GST free shopping? Hope not.

Really hope this isn’t the beginning of fairness going back to Khloe or Pippa status.

Andrea

(1) In year approval page 6.

(2) Article 2(b)(iii)(c)

(3) Page 5 Potential behavioural changes by consumers

Coz everyone else pays their taxes

Now the most logical next post would be a discussion of the OECD digital proposals as that is the international consensus thing I am so keen on and also fits nicely into the thread of these posts.

The slight difficulty is that this requires me to do some work which is always a bit of a drag and when I am suffering badly from jetlag – an insurmountable hurdle.

So as a bit of light relief I thought I’d have a bit of a pick into the narrative around multinationals and why their non-taxpaying is particularly egregious.

You know the whole small business pays tax so large business should too thing.

Now because of the tax secrecy thing, we can never know for def whether this is the case. But there is some stuff in the public domain, so let’s see what we can do as a bit of an incomplete records exercise.

In one of the early papers for the TWG, officials had a look at tax paying of certain industries. Now while the punchline – industries with high levels of capital gains pay less tax – is well known, there are some other factoids that are worth considering.

Factoid 1 The majority of small businesses are in loss (1). Ok wow. But that could be fine if all the income was being paid out to shareholders.

Factoid 2 Spike of incomes at $70k. Ok suspicious I’ll give you that. But maybe there are lots of tax paid trust distributions.

Factoid 3 Shareholder borrowings from the company (2) – aka overdrawn current account balances – have been climbing since the reduction in the company tax rate in 2010. Oh and the imputation credit balances have been climbing over that period too (3). But that could be fine if interest and/or fringe benefit tax is paid on the balances.

Factoid 4 Consumption by the self employed is 20% higher than by the employed for the same taxable income levels. But this could be fine if the self employed have tax paid or correctly un-tax paid – like capital gains – sources of wealth that the employed don’t have.

Factoid 5 In 2014 high wealth individuals had $60 million in losses (4) in their own name. But that could be ok because if companies and trusts have been paying tax and they have been receiving tax paid distributions from their trusts.

Factoid 6 Directors with an economic ownership in their company are rarely personally liable for any tax their company doesn’t pay. Because corporate veil. And that even includes PAYE and Kiwisaver they have deducted from their employees.

Now all of this is before you get to the ability small business has to structure their personal equity so that any debt they take on is tax deductible. Not to mention the whole accidentally putting personal expenditure through the business accounts thing.

And of course I am sure none of this has any relevance to the Productivity Commission’s concern that New Zealand has long tail of low productivity firms [without] an “up or out” dynamic. (5)

But is it all ok?

- Are there lots of taxpaid trust distributions? We know the absolute level (6) but not whether it is ‘enough’.

- Is interest or FBT being paid on overdrawn current accounts?

- Do the self employed have sources of taxpaid wealth that the employed don’t have?

- Why have some of our richest people still got losses?

- How much tax do directors of companies in which they have an economic interest walk away from?

- What is the level of personal expenditure being claimed against business income? Or at least what is the level that IRD counters?

Dunno.

Combination of tax secrecy and information not currently collected. But IRD are working towards an information plan and the TWG have called for greater transparency.

Awesome.

Coz most of this is currently totes legit. In much the same way as the multinationals structures are.

Just saying.

Andrea

(1) Footnote 9

(2) Page 11

(3) Page 10

(4) Page 15

(5) Page 19

(6) Page 9

Taxing multinationals (2) – the early responses

Ok. So the story so far.

The international consensus on taxing business income when there is a foreign taxpayer is: physical presence – go nuts; otherwise – back off.

And all this was totally fine when a physical presence was needed to earn business income. After the internet – not so much. And with it went source countries rights to tax such income.

Tax deductions

However none of this is say that if there is a physical presence, or investment through a New Zealand resident company, the foreign taxpayer necessarily is showering the crown accounts in gold.

As just because income is subject to tax, does not necessarily mean tax is paid.

And the difference dear readers is tax deductions. Also credits but they can stand down for this post.

Now the entry level tax deduction is interest. Intermediate and advanced include royalties, management fees and depreciation, but they can also stand down for this post.

The total wheeze about interest deductions – cross border – is that the deduction reduces tax at the company rate while the associated interest income is taxed at most at 10%. [And in my day, that didn’t always happen. So tax deduction for the payment and no tax on the income. Wizard.]

Now the Government is not a complete eejit and so in the mid 90’s thin capitalisation rules were brought in. Their gig is to limit the amount of interest deduction with reference to the financial arrangements or deductible debt compared to the assets of the company.

Originally 75% was ok but then Bill English brought that down to 60% at the same time he increased GST while decreasing the top personal rate and the company tax rate. And yes a bunch of other stuff too.

But as always there are details that don’t work out too well. And between Judith and Stuart – most got fixed. Michael Woodhouse also fixed the ‘not paying taxing on interest to foreigners’ wheeze.

There was also the most sublime way of not paying tax but in a way that had the potential for individual countries to smugly think they were ok and it was the counterparty country that was being ripped off. So good.

That is – my personal favourite – hybrids.

Until countries worked out that this meant that cross border investment paid less tax than domestic investment. Mmmm maybe not so good. So the OECD then came up with some eyewatering responses most of which were legislated for here. All quite hard. So I guess they won’t get used so much anymore. Trying not to have an adverse emotional reaction to that.

Now all of this stuff applies to foreign investment rather than multinationals per se. It most certainly affects investment from Australia to New Zealand which may be simply binational rather than multinational.

Diverted profits tax

As nature abhors a vacuum while this was being worked through at the OECD, the UK came up with its own innovation – the diverted profits tax. And at the time it galvanised the Left in a way that perplexed me. Now I see it was more of a rallying cry borne of frustration. But current Andrea is always so much smarter than past Andrea.

At the time I would often ask its advocates what that thought it was. The response I tended to get was a version of:

Inland Revenue can look at a multinational operating here and if they haven’t paid enough tax, they can work out how much income has been diverted away from New Zealand and impose the tax on that.

Ok – past Andrea would say – what you have described is a version of the general anti avoidance rule we have already – but that isn’t. What it actually is is a form of specific anti avoidance rule targetted at situations where companies are doing clever things to avoid having a physical taxable presence. [Or in the UK’s case profits to a tax haven. But dude seriously that is what CFC rules are for]

It is a pretty hard core anti avoidance rule as it imposes a tax – outside the scope of the tax treaties – far in excess of normal taxation.

And this ‘outside the scope of the tax treaties’ thing should not be underplayed. It is saying that the deals struck with other countries on taxing exactly this sort of income can be walked around. And while it is currently having a go at the US tech companies, this type of technology can easily become pointed at small vulnerable countries. All why trying for an new international consensus – and quickly – is so important.

In the end I decided explaining is losing and that I should just treat the campaign for a diverted profits tax as merely an expression of the tax fairness concern. Which in turn puts pressure on the OECD countries to do something more real.

Aka I got over myself.

In NZ we got a DPT lite. A specific anti avoidance rule inside the income tax system. I am still not sure why the general anti avoidance rule wouldn’t have picked up the clever stuff. But I am getting over myself.

Of course no form of diverted profits tax is of any use when there is no form of cleverness. It doesn’t work where there is a physical presence or when business income can be earned – totes legit – without a physical presence.

And isn’t this the real issue?

Andrea

My fair tax review

So the details of this government’s tax review is out.

Depending on who you read it will either be revolutionary or not radical.

Now even though this blog has come as a response to the Left’s – and fairness’s – relatively recent introduction into the tax debate – I couldn’t see anything I could competently add to the random number generator that is the current public discussion. That was until I read one commentator – who actually understands tax – talk about the last Labour government’s tax review – the McLeod Report.

He referred to that report as having analysis that stood up 16 years later. And with the underlying analysis found in the issues report I would wholeheartedly agree. But in terms of the recommendations in the final report I would say, however, that it was very much of its time.

And by that I mean that while the issues report fully discussed all issues of fairness/equity as well as efficiency – when it came to the final report efficiency was clearly queen.

Now by efficiency I am meaning ‘limiting the effects tax has on economic behaviour’. And fairness as meaning all additions to wealth – aka income – are treated the same way.

The tax review kicked off in 2000 at about the same time I arrived at Inland Revenue Policy. In early 2000 there was:

- No working for families

- No Kiwisaver

- Top personal tax rate was about to increase to 39% but with no change to company or trust tax rate

- Interest was about to come off student loans while people studied.

That is the settings generally were the ones that had come from the Roger Douglas Ruth Richardson years.

Also in tax land the Commissioner was having a seriously hard time as the Courts were taking a very legalistic attitude to tax structuring. High water mark was a major loss in 2001. And unsurprisingly in such an environment the banks had started structuring out of the tax base. But it would be a while before that became obvious.

Housing was affordable. Families such as mine could be supported on one senior analyst salary – and live walking distance to town.

The tax review was headed by a leading practitioner Rob McLeod; and had two economists, a tax lawyer and a small business accountant. One woman. Because that is what progressive looked like 2000.

And so what were their recommendations/suggestions?

No capital gains tax but an imputed taxable return on capital This one is both efficient and fair. And did materialise in some form with the Fair Dividend rate changes to small offshore investment. It is the basis of TOP tax proposal. At the issues paper stage it was proposed to include imputed rents but the public (over) reaction caused it to be dropped. Interestingly it is explicitly out of scope with the Cullen review.

Flow through tax treatment for closely held businesses and separate tax treatment for large business

What this is about is saying entities that are really just extensions of the individuals concerned should be taxed like individuals not the entity chosen. This is effectively the basis of the Look Through Company rules – although they are optional. It means the top tax rate will always be paid. But it also means that capital gains and losses can be accessed immediately.

Now this is definitely efficient as the tax treatment will not be dependent on the entity chosen. And it is also arguably fair for the same reason.

It does mean though that if a company structure is chosen and the business gets into trouble: the tax losses can be accessed as it is effectively the loss of the shareholder but the creditors not paid because it is a separate legal entity. Which probably wouldn’t exactly feel fair to any creditor.

But all this is unreconciled public policy rather than the McLeod report.

Personal tax scale to be 18% up to $29,500 and 33% thereafter.

The tax scale at the time ranged from 9.5% to 39% at $60,000. The proposal would have had the effect of increasing the incentive to earn income over $60,000 as so would have been more efficient than the then 39% tax rate. As the company and trust rate were also 33% it would have returned the tax nirvana where the structure didn’t matter.

However it would have increased taxes on lower incomes and decreased taxes on higher incomes. So while efficient – not actually fair according to the vibe of the Cullen review terms of reference.

New migrants seven years tax free on foreign income

At this time our small foreign investment – aka foreign investment fund – rules were quite different to other countries. While we didn’t have a realised capital gains tax – for portfolio foreign investment we could have an accrued capital gains tax in some situations. This was considered off putting to potential high skilled high wealth migrants. So to stop tax preventing migration that would otherwise happen; the review proposed such migrants get seven years tax free on foreign income.

This proposal was the other one that was enacted with a four year tax free window – transitional migrants rules.

And again a policy that is efficient but arguably not fair. As the foreign income of New Zealanders in subject to full tax. However Australia and the United Kingdom also have these rules that New Zealanders can access.

The logical consequence though is that no one with capital lives in their countries of birth anymore. And not sure that is ultimately efficient.

New foreign investment to have company tax rate of 18%

Again this is the foreign investment – good – argument. But it ultimately comes from a place where foreign capital doesn’t pay tax because it is from a pension fund, sovereign wealth fund or charity. Or if it is tax paying that tax paid in New Zealand doesnt provide any form of benefit in its home or residence country. So by reducing the tax rate by definition this reduces the effect of tax on decision making.

However doesn’t factor in the loss of revenue if there are location specific rentswhich aren’tsensitive to tax. And not exactly fair that domestic capital pays tax at almost twice the tax rate. Unsurprisingly didn’t go ahead.

Tax to be capped at $1 million for individuals

This again comes from the place of removing a tax disincentive from investing and earning income. Yeah not fair and also didn’t go ahead.

Restricting borrowing costs against exempt foreign income

This was the basis of the banks tax avoidance schemes that ended up costing $2 billion. It is only briefly mentioned in the final report with no submissions. It is to the review team’s – probably most likely Rob McLeod – credit that it is there at all. This proposal was both efficient and fair. Stopping the incentive to earn foreign income as well as making sure tax was paid on New Zealand income.

It will be very interesting to see where this review comes out with the balance between efficiency and fairness. Because both matter. Without fairness we don’t get voluntary compliance and without efficiency we get misallocated capital and an underperforming economy. But the public reaction to the taxation of multinationals and ‘property speculators’ would indicate a bit more fairness is needed to preserve voluntary compliance.

And as indicated 16 years ago – taxation of capital is a good place to start.

Andrea