Tax and Small Business

Last week the Small Business Council issued its report to Government. I am sure there are many wizard things in there maybe even some tax recs.

Also last week I had a friend to stay who is helping some workers that have lost thousands of dollars of wages and holiday pay when their employer went into receivership. Her expression was Wage Theft. It is a crime in Australia but not in New Zealand. Unlike theft as a servant which totally is.

Talking to her it was obvious that there was considerable overlap between what she is seeing and the issues considered by the TWG of closely held companies where the directors have an ownership interest not paying PAYE and GST (1).

And yes my friend’s friends are worried about their PAYE and KiwiSaver deductions. So really hope tightening up on this stuff is in the Small Business report along with the expected recs on compliance cost reduction.

I am also personally very interested in what the Group comes up with as the Productivity Commission noted that NZ has a lot of small low productivity firms without an up or out dynamic (2). That is firms tieing up capital that should be released for more productive purposes with the associated benefit of not staying on too long and dragging their workers and the tax base with them.

Now ever since I found that reference I have been concerned that there may be aspects of the tax system that may be driving that. Benefits or ‘opportunities’ that don’t arise for employees subject to PAYE or owners of widely held businesses subject to audits and outside shareholder scrutiny.

And it is true that there is nothing particularly special in a tax sense here to New Zealand. However given that New Zealand rates as number one in the ease of doing business index there may be more people going into business than would be the case in other countries.

Some of these aspects can be reduced through stricter enforcement by Inland Revenue but are otherwise largely structural in a self assessment tax system where the department doesn’t audit every taxpayer. One is a policy choice possibly because the alternative would add significant complexity to the tax system and the final example is a combination of the need for stronger enforcement and/or policy changes needed now that the company and top personal rate are destined to be permanently misaligned.

So what are these ‘aspects’?

Concealing income or deducting private expenses

Recent work by Norman Gemmell and Ana Cabal found that the self employed had 20% higher consumption than the PAYE employed at the same levels of taxable income.

Now it could be that for some reason the extra consumption of the self employed comes from inheritances or untaxed capital gains or taking loans from their business – more on that later – more so than those in the PAYE system or owners of widely held businesses. It might not be tax evasion at all.

But we just don’t know.

All we know is the 20% extra consumption and that there is a greater opportunity and fewer checks with closely held businesses to conceal income or deduct personal expenses. And Inland Revenue says such levels are comparable with other countries.

While things like greater withholding taxes and/or reporting can help, I am also concerned that with greater automation it also becomes much easier to have those personal expenses effortlessly charged against the business rather than recorded as personal drawings.

Interest Deductions

The second aspect is my specialist subject of interest deductions. Unlike concealing income or deducting personal expenditure – this one is totes legit.

Interest is fully deductible to a company and for everyone else it is deductible if it can be linked to a taxable income earning purpose or income stream aka tracing.

What that means is if a business person has a house of $2 million and a business of $1 million and has debt of $1 million – all the interest deductions on the debt can be tax deductible – if the debt can be linked to the business. This can be compared to a house of $2 million and debt of $1 million – and no business – where none of it is deductible.

To make this fairer with taxpayers who don’t have the opportunity to structure their debt there would need to be some form of apportionment over all assets – business and personal. So in the above example interest on only $330,000 should be allowed.

But yes – that would require a form of valuation of personal and business assets. And yes valuing goodwill brings up all the same – valid – concerns raised with taxing more capital gains.

So I guess we can say that under the status quo fairness – and possibly capital allocation – have been traded off against compliance costs.

Income Splitting

The third is the ability to income split with partners to take advantage of the progressive tax scale. Now this is only actually allowed if the partner is doing work for the business. But verifying the scale and degree of this work – even with burden of proof on Commissioner – is a big if not impossible task for the Commissioner.

Other mechanisms include loans from the partner to help max out the lower income tax bands.

And the statistics would support an argument that there is a degree of maxing out the lower bands just not that there necessarily is a lot of income splitting.

Interestingly both Canada and Australia have rules for personal services companies where these types of deductions are not allowed.

But this is ok if this is the amount of value going to the shareholders. Maybe our firms are so unproductive that they can only support shareholder salaries of $70k and below.

If that were the case though we wouldn’t be seeing the final aspect which is taking loans from companies you control instead of taxable dividends.

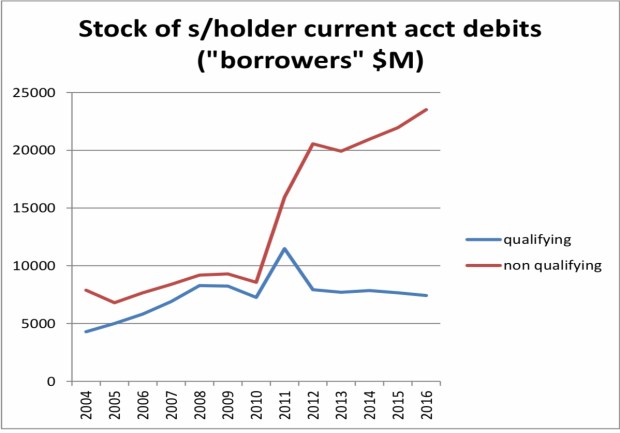

Overdrawn shareholder current accounts

Now to be fair for this to occur there should also be interest paid by the shareholder to the company on loans from the company to the shareholder. And unlike the interest in point 2 – none of this should be tax deductible to shareholder if it is funding personal expenditure while the interest received will be taxable. This on its own should be enough to not do it and receive taxable dividends instead.

Unfortunately the facts also don’t seem to back this up. Imputation credit account balances – meaning tax has been paid but not distributed- have been climbing. Now this could be like totally awesome if it meant all the money was being retained in the company to grow.

Except that overdrawn current account balances – loans from the company to the shareholders- have been similarly growing too. Now sitting at about $25 billion.

And yes this all started from about 2010. And what happened in 2010? Why dear readers the company tax rate was cut to 28% while the trust rate remained at 33%.

Ironically the associated cut in top marginal rate was to stop the income shifting that went on between personal income and the trust rate.

Now one level it shouldn’t matter at all if these balances continue to climb so long as non- deductible assessable interest is paid on the debt. However an overdrawn current account is – imho – the gateway drug to dividend avoidance.

And yes that can be tax avoidance but much like the tax evasion opportunities, income splitting and interest on overdrawn current accounts – all of this requires enforcement by Inland Revenue. And as they can’t audit everyone there will always be a degree that is structural in a self assessment tax system.

But the underlying driver of people wanting to take loans from their company rather than imputed dividends is that our top personal tax rate and company tax rate are not the same. Paying a dividend would require another 5% tax to be paid.

Possible options

Now other countries have always had a gap between the top rate and either the company or trust rate so this shouldn’t be the end of the world. But those countries have buttressing rules that we don’t have in New Zealand. The personal services company rules discussed above or the accumulated earnings tax in the US (3) or the Australian rule that deems such loans to be dividends.

Until recently I had been a fan of making the look through company rules compulsory for any company that was currently eligible. (4) I couldn’t see the downside. The closely held business really is an extension of its shareholder so why not stop pretending and tax them correctly.

However some very kind friends have been in my ear and pointed out the difficulties of taxing the shareholder when all the income and cash to pay the tax was in the company. It works ok when it is just losses being passed through. So maybe I am less bullish now.

An alternative approach could be to apply a weighted average of the shareholders tax rates on the basis that all the income would be distributed. Similar to PIEs. The tax liability is with the entity but the rate is based on the shareholders. I guess you then do a mock distribution to the shareholders which can then be distributed to them tax free. And yes only to closely held companies. Wider would be a nightmare.

Kind of a PIE meets LTC.

Or you could just old school it and raise the company tax rate to 33% for all companies. Shareholders with tax rates below that could use the LTC rules and make the assessment of whether the compliance of the rules was greater or less than the extra tax.

It would require an adjustment to the thin capitalisation rules by increasing the deductible debt levels to ensure foreign investment didn’t pay more tax. But for some of you dear readers increased taxation on foreign investment might even be a plus.

But all in all I don’t think the status quo with small business is a goer. Whether it is for fairness reasons, or capital allocation reasons or simply stopping me worrying – doing something is a really good idea.

Because I would hate to think any of this was enabling behaviours that kept people in business longer than they should. And even with the most whizziest of new IRD computers – there will always be limits on enforcement.

Andrea

(1) Page 116 Paragraph 68

(2) Page 19

(3) Although it would make more sense to only apply this to the extend that the income hasn’t been retained in the business and distributed in non- dividend form.

(4) Yes there is the issue that companies could start adding an extra class of share to get around this. But I don’t believe this is insurmountable with de minimis levels of additional categories and the odd antiavoidance rule for good measure. It is even the advice of KPMG so clearly not that wacky.

PIEs, timebar and tax fairness

My lovely young friends had a great time with their guest post last week and were delighted with the reception they received. Including getting picked up by interest.co.nz – something they like to point out I have never managed.

They were really keen to post this week on the digital services tax discussion document which they think is awesome. But I need to have a little chat to them before they do.

We also had a chat about whether the Andrea Tax Party is really a goer. Much like Alfred Ngaro we have concluded it all seems a bit hard. Also the move from thinking about things to politics hasn’t been the smoothest for TOP. So as the evidence led people that we are, we have decided to conserve our emotional energy and not fall out over boring constitutional issues.

I’ll stay as your correspondent and my young friends will come back from time to time when they can fit it in between their three jobs and studying. They are also checking out Organise Aotearoa who recently put up this sign in Auckland and seem to be to the left of Tax Justice Aotearoa.

As well as the digital services tax proposal – which I’ll save for my (briefed) young friends – the other tax story this week was how thanks to the Department upgrading its computer system it has found a number of people – 450,000 – haven’t been paying enough tax on their PIE investments. And while that is the case the Department has said that it won’t chase this tax on any past years.

Behind this story are two interesting – to me anyway – tax concepts.

Portfolio investment entities (PIEs)

These are a Michael Cullen special and came in at the same time as KiwiSaver. Before their introduction all managed funds were taxed at the trust rate of 33% and were taxed on any gains they made on shares sales – because they were in business.

Alongside all this was passive investment or index funds who had managed to convince Inland Revenue that because they only sold because they had to, those gains weren’t taxable.

Individual investors weren’t taxed on their capital gains and otherwise they were taxed at less than 33% if they had taxable income below the 33% threshold. This was particularly the case for retired investors.

The status quo did though give a minor tax benefit to high income people who were otherwise paying tax at 39%.

So it was all a bit of a hot mess.

Added into the equation was that, unlike now, the Department’s computer wasn’t up to much so all policy was based on ‘keeping people out of the system’.

So where the PIE stuff landed was income of the fund would be broken up in terms of who owned it and taxed at the rate of the owners. Except for the high earners – as their alternative was a unit trust taxed at the company rate – the top rate was capped at the company rate.

Low income people were now taxed at their own rate rather than the trust rate and high income people kept their low level tax benefit.

Happiness all round.

But it all depended on the individual investor telling the fund what the correct rate was and boy did the funds send out lots of reminders. I got totally sick of them.

Particularly when not filling them out meant you got taxed at 28% which was the top rate anyway.

So the people getting caught out this week would have once told the fund to tax them at a lower rate. It wouldn’t have happened by accident.

Although it is entirely possible they were on a lower rate at the time – because they had losses or something – and then ‘forgot’ to update it. Such people though would probably had a tax agent who would normally pick this stuff up. So not these people,

The caught people I would suggest are people, without tax agents, who accidentally or intentionally chose the wrong rate at the time or are PAYE earners whose income has increased over time and didn’t think to tell their fund.

But really only a tax audit would tell the difference between the two groups even if the effect is the same.

Time Bar

The other thing this week has shone light on is something known in the tax community as timebar (2).

It is a balance between the Government’s right to the correct amount of revenue and taxpayer’s ability to live their lives not worrying about a future tax audit. The deal is that if you have filed your tax return and provided all the necessary information – but you are wrong in the Government’s favour – Inland Revenue can only go back and increase your tax for four years.

If you haven’t filed and/or provided the necessary information – usually in cases of tax evasion – game on. The Department has no time constraints.

But the thing is none of this is an obligation on Inland Revenue. It is a right but not an obligation.

Under the Care and Management provisions (1) – the Commissioner must only collect the highest net revenue over time factoring in compliance costs and the resources available to her.

And so on that basis – I must presume – she has decided to not go back and collect tax for the last three years underpaid PIE income. In the same way he – as it was then – decided to only pursue two years of tax avoidance that arose from the Penny and Hooper tax avoidance cases.

Now I am sure this is completely above board legally in much the same way as the use of current accounts or the non-taxation of capital gains.

But with a tax fairness lens, it makes discussions with my young friends quite tricky.

They only have their personal labour which, to them, is taxed higher than I was at the same age. They don’t have capital and see this recent story as another way the tax system is slanted against them.

So I am not sure we have seen the last of the motorway signs.

Andrea

(1) Section 6A(3)

(2) Section 108

Tax and politics

Your correspondent is back from Sydney. Had a great time because – well – Sydney.

Managed to score a gig on a panel at the TP Minds conference talking about international policy developments for transfer pricing. An interesting experience as I am pretty strong in most tax areas except GST – and you guessed it – transfer pricing.

But it was ok as I did a bit of prep and all those years of working with the TP people paid off. And of course I do know a little bit about international tax and BEPS so alg.

Even a techo tax conference again reminded me just how different – socially and culturally – Australia is to New Zealand. Examples include: the expression man in the pub being used without any sense of irony or embarrassment and one of the presenters – a senior cool woman from the ATO – wearing a hijab.

Can’t imagine either in tax circles in NZ.

My particular favourite though was watching the telly which showed a clip of Bill Shorten describing franking (imputation) credits as something you haven’t earned and a gift from the government. Now Australia does cash out franking credits but – wow – seriously just wow. Kinda puts any gripes I might have about Jacinda talking about a capital gains tax into perspective.

And in the short time I have been away yet another minor party has formed as well as the continuation of the utter dismay from progressives over the CGT announcement.

In the latter case I am fielding more than a few queries as to what the alternatives actually are to tax fairness is a world where a CGT has been ruled out pretty much for my lifetime.

Now while I have previously had a bit of a riff as to what the options could be, I have been having a think about what I would do if I were ever the ‘in charge person’ – as my kids used to say – for tax.

To become this ‘in charge person’ I guess I’d also have to set up a minor party although minor parties and tax policies are both historically pretty inimical to gaining parliamentary power.

But in for a penny – in for a pound what would be the policies of an Andrea Tax Party be?

Here goes:

Policy 1: All income of closely held companies will be taxed in the hands of its shareholders

First I’d look to getting the existing small company/shareholder tax base tidied up.

On one hand we have the whole corporate veil – companies are legally separate from their shareholders – thing. But then as the closely held shareholders control the company they can take loans from the company – which they may or may not pay interest on depending on how well IRD is enforcing the law – and take salaries from the company below the top marginal tax rate.

On the other hand we have look through company rules – which say the company and the shareholder are economically the same and so income of the company can be taxed in the hands of the shareholder instead. But because these rules are optional they will only be used if the company has losses or low levels of taxable income.

My view is that given the reality of how small companies operate – company and shareholders are in effect the same – taking down the wall for tax is the most intellectual honest thing to do. Might even raise revenue. Would defo stop the spike of income at $70,000 and most likely the escalating overdrawn current account balances.

So look through company rules – or equivalent – for all closely held companies. FWIW was pretty much the rec of the OG Tax Review 2001 (1).

Now that the tax base is sorted out – if someone wants to add another higher rate to the progressive tax scale – fill your boots. But my GenX and tbh past relatively high income earning instincts aren’t feeling it.

Policy 2: Extensive use of withholding taxes

The self employed consume 20% more at the same levels of taxable income as the employed employed. Sit with that for a minute.

20% more.

Now the self employed could have greater levels of inherited wealth, untaxed capital gains or like really awesome vegetable gardens.

Mmm yes.

Or its tax evasion. Cash jobs, not declaring income, income splitting or claiming personal expenses against taxable income.

Now in the past I have got a bit precious about the use of the term tax evasion or tax avoidance but I am happy to use the term here. This is tax evasion.

IRD says that puts New Zealand at internationally comparable levels (2). Gosh well that’s ok then.

Not putting income on a tax return needs to be hit with withholding taxes. Any payment to a provider of labour – who doesn’t employ others – needs to have withholding taxes deducted.

Cash jobs need hit by legally limiting the level of payments allowed. Australia is moving to $10,000 but why not – say $200? I mean who other than drug dealers carries that much cash anyway?

Claiming personal expenses is much harder. This we will have to rely on enforcement for.

Policy 3: Apportion interest deductions between private and business

Currently all interest deductions are allowable for companies – because compliance costs. Otherwise interest is allowed as a deduction if the funding is directly connected to a business thing.

Seems ok.

What it means though is that for someone with a small business and personal assets such as a house, all borrowing can go against the business and be fully deductible.

Options include some form of limitation like thin capitalisation or debt stacking rules. I’d be keen though on apportionment. If you have $2 million in total assets and $1 million of debt – then only 50% of the interest payable is deductible.

Policy 4: Clawback deductions where capital gains are earned

Currently so long as expenditure is connected with earning taxable income it is tax deductible. It doesn’t matter how much taxable income is actually earned or if other non-taxable income is earned as well.

Most obvious example is interest and rental income. So long as the interest is connected with the rent it is deductible even if a non-taxable capital gain is also earned.

One way of limiting this effect is the loss ringfencing rules being introduced by the government. Another way would be – when an asset or business is sold for a profit – clawback any loss offsets arising from that business or asset. Yes you would need grouping rules but the last government brought in exactly the necessary technology with its R&D cashing out losses (4).

Policy 5: Publication of tax positions

And finally just to make sure my party is never elected – taxable income and tax paid of all taxpayers – just like in Scandinavia will be published. Because if everyone is paying what they ought. Nothing to hide. And would actually give public information as to what is going on.

Options not included

What’s not there is any form of taxation of imputed income like rfrm. It isn’t a bad policy but taxing something completely independent of what has actually happened – up or down – doesn’t sit well with me.

Also no mention of inheritance tax. Again not a bad policy I’d just prefer to tax people when they are alive.

And for international tax I think keep the pressure on via the OECD because the current proposals plus what has already been enacted in New Zealand is already pretty comprehensive.

Now I know none of this is exactly exciting and so I’ll get the youth wing to do the next post.

Andrea

(1) Overview IX

(2) Paragraph 6

(3) Treatment of interest when asset held in a corporate structure

(4) Page 11 onward

#WeareallMetiria

Let’s talk about tax.

Or more particularly let’s talk about tax, debt and approach to law changes.

Twenty plus years ago I came back to New Zealand a little bit pregnant. And before 1992 – unless you were in the public service – pregnancy meant (job) resignation. A stage up I guess from marriage or engagement meaning resignation but pretty antediluvian even with today’s – Is Jacinda having a baby? – eyes.

Parental Leave had come in two years before I came back but couldn’t apply to me as I had left a job in the UK – not New Zealand. I was also more than a little over being an accountant – I was young what can I say – and fascinated by economics. Again young.

So decided I would use this time to retrain as an economist. I mean seriously how hard could raising children be? Again young. And of course in reality studying was a blissful break from domesticity – not the other way around.

One of the super perks of studying was the Student creche. Super high quality childcare; very reasonable pricing and super flexible. Why sure Andrea: Tuesday 10-1; Thursday 3-5; and all day Friday is completely fine. Please pay by the hour. One child or two?

And at that creche there were two types of mothers – yes mothers; men appeared only occasionally. There were the middle class married women – like me – late twenties early/ mid thirties doing post graduate work or retraining and then there were the late teens/early twenties single women who were at university for the first time.

The young women had a number of things in common:

- Straight A students;

- Determined and resourceful;

- Highly motivated; and

- Dirt poor.

The other thing they had in common is that pretty much all of them were lying to WINZ in some form. Part time undeclared untaxed income was very common as was parental financial help. I don’t remember extra flat mates but I am sure that was in the mix. Because resourceful.

But all of this just meant that they could have their kids nits treated as I did, pay rent and eat. Although I do remember one of them brightly telling me that just eating potatoes for a week was an easy way of managing when unexpected bills came in. Right ok.

So in other words they were all Metiria. And the actual amounts of money involved were absolutely trifling. $20 or $30 a week max for a relatively short period of time. But it was the difference between sinking and not sinking. Swimming didn’t come into it.

Of course this was when there was a training incentive allowance to help with creche fees. And while it was post Mother of all Budgets the relative value of the welfare system was more than it is now. So I guess the current generation of young women just don’t go to university. Social Investment anyone?

And from time to time I run into them. Also like Metiria they are now professionals, (re)partnered and have other (step) children. Taxpaying, respectable pillars of society.

Now into this discourse has come Lisa Marriott’s seminal work on how we as a society treat tax evasion v welfare fraud. And I have nothing to add to this. Coz yup she is right. Nailed it.

But the two things I would like to add to the conversation – assuming there still is one now Jacinda has arrived – is a bit of a comparison with how we treat tax debt and how we treat widespread tax non-compliance.

In the early days of the last Labour government changes were made to the rules governing tax debt. Basically the intent was to get the department to calm the F down in terms of collecting tax debt. The rules were changed so that debt will not be recovered if it:

- is an inefficient use of the Commissioner’s resources or

- would leave a taxpayer in serious hardship.

And note the all important or. Not only should the Commissioner not pursue debt when there isn’t a bang for the buck but even when there is – if it would be unkind. At least these are the rules that apply to Working for Families overpayments.

But looking at some of the cases taken by WINZ, clearly these criteria are not in their legislation.

The other thing that made me realise how differently tax is treated to welfare are situations where there is widespread non-compliance. Either through a misunderstanding with how the law applied; wilful blindless; or a desire to put the past in the past; the law can be changed to make the illegal legal. And at times retrospectively.

Because they are doing it already; not in the forecast; can’t audit our way out or taxpayer friendly. The latter of course meaning friendly to specific taxpayers rather than friendly to taxpayers as a whole. Examples include:

- GST registration for body corporates was made optional. Of course meaning will only register if can get refunds;

- Use of tax pooling was allowed in circumstances that weren’t previously allowed for in the legislation;

- Canterbury Earthquake employee accommodation allowances were specifically made tax free;

- crews on super yachts income was made tax free;

- The contingent liability associated with conduit relief was extinguished.

Now these are just a few examples. Most tax bills contain versions of these. And all have good reasons behind them and help make the tax system breathe. I am comfortable with – pretty much – all of them.

But all were at some stage against the legislation. In all cases, at some stage, some people were ‘incorrectly’ on the wrong side of the law. Usually individually or cumulatively with quite large amounts of money at stake. Far more than a trifling $20/ week.

But rather than ruthlessly enforce the ‘incorrect’ legislation; the legislation changed. It changed following representations made to Ministers and officials by affected parties. In the same way I see welfare advocates make similar representations. The only difference is that the tax advocates get listened to. Because structural imbalances.

So even though tax and welfare are mirror images of each other, this is another case where public policy talks out of both sides of its mouth. And unfortunately as there is little or no overlap between the two worlds; joined up government just means easier detection of welfare discrepancies.

Now finally in case I have been a little too subtle:

To all the people baying for Metiria’s blood – did you ever do babysitting; lawnmowing or car washing when you were younger and not put it on your tax return? I know that is me.

Well that is what tax evasion looks like. We committed a tax crime. We lied to Inland Revenue. FFS #WeareallMetiria.

Should we fall on our swords. No. We should get on with our taxpaying lives. And section 176(2)(b) – the bang for buck provision – quite correctly stops the department from chasing us.

Shame the same approach can’t be taken to Welfare.

Andrea

Deregos

Let’s talk about tax.

Or more particularly let’s talk about the tax rules for deregistering charities.

It has been a big intellectual week for your correspondent. Tuesday night White Man Behind a Desk. No tax. An interesting riff on immigration that Michael Reddell clearly wasn’t the tech checker for. Wednesday night Aphra Green Harkness Fellow on US criminal justice reform coz States just ran out of money. I tried to run an argument that this was the good side of low taxes. Didn’t resonate – go figure. And Wednesday morning – Roger Douglas on turning taxes into savings coz #taxesaregross.

And it was on the lovely Roger I planning to write but on Friday was the Greens on how there were bugg@r all foreign trusts reregistering. So I thought I’d write about that and the genius decision to require disclosure rather than taxation.

And as if that wasn’t enough. Saturday morning the latest Matt Nippert on a US and charities thing. An elderly couple with no heirs wanting to transfer wealth to a charitable institution – awh lovely. So nice they chose NZ. But also Panama, low distributions and references to the IRS. Ok. Initial reaction was it looks like FATCA avoidance coz NZ charities are outside its scope of reporting to IRS. Really must get on to my ‘US citizenship is not a good thing for tax’ post. It has been in the can for longer than this blog has been running. So embarrassed.

But one thing really caught my eye. The charities had voluntarily deregistered. Mmm interesting.

Your correspondent now moves a tiny bit in the Charities NGO sector. And from time to time I hear ‘should we stay a charity? Coz need to be careful over advocacy and ActionStation isn’t a charity and it is alg for them.’

To which I try to reply in my best talking to Ministers language: ‘ That’s one option. It would mean handing over a third of your reserves in taxes or all of your reserves to another registered charity. But totes – if that is what you want.’

Strangely the conversation doesn’t continue.

Coz the law changed in 2014 to stop the rort of charities getting lots of lovely tax subsidised donations, not distributing; deregistering and then keeping all that lovely taxpayer dosh for themselves. Go Hon Todd!

Now on the face of it this should apply to our friends here very soon. Section HR 12 applies a year after deregistration and turns the reserves – less wot go to another charity – into taxable income.

Except there doesn’t seem to be anything explicit that makes it New Zealand source income. Possibly personal property or maybe indirectly sourced from New Zealand. But the source rules are kind of old school and want to bite on real stuff not deemed income. No matter how worthy of New Zealand source taxing rights it should be.

And of course none of this matters dear readers if the entity is New Zealand resident. Coz everything gets taxed! And as the trustees are a New Zealand company – high chance it will be. So alg.

Well almost.

Coz if the dosh in the charity all came completely from non-residents – the trust rules make it a foreign trust. And foreign source income aka income wot doesn’t have a New Zealand source is not taxed. So initial view – unless the source rules can bite on this deemed income or the trust isn’t a foreign one – there will be no wash up for our friends here.

Now on one level that is cool. The final tax was all about clawing back the tax benefits given on the initial donations and the charitable tax exemption on income. Here it would have been tax exempt anyway. So alg.

The other argument is that these guys intentionally registered as a New Zealand charity. Got all the good stuff like potentially non- disclosure to IRS as well as being to say they are a legit NZ charity. But now don’t get the bad stuff.

And NZ gets the bad name but not the income. What does that sound like? Oh yes the NZ Foreign Trust rules.

So glad that – according to the Greens – is coming to an end. Shame it had to be such a resource intensive way of doing it.

Andrea

Thickness of a prison wall

Let’s talk about tax (and tax avoidance).

Last week the government announced it was building yet another prison. Another moral and fiscal failure. Skilfully continuing to over turn the falling crime rate dividend we had in 2013 before the bail laws changed.

Also last week a reader made a comment about how wasn’t tax avoidance ‘legal’.

Another such observation on tax avoidance came from Denis Healey who said that the difference between tax avoidance and tax evasion is the thickness of a prison wall. She said trying to link two quite independent things together.

Now both maybe right in the United Kingdom but they really don’t directly translate to the New Zealand situation. So being the public spirited individual I am I thought I’d have a go at a layman’s guide to tax avoidance for New Zealanders. And no more mention of prison stuff – promise.

First of all tax avoidance is a term defined in the Income Tax Act. It comes in and overrides everything else in the Income Tax Act. So any provison in the Act theoretically runs the risk of tax avoidance coming in and saying – ‘you know what’ just kidding – bog off.

And it is defined in a way – directly or indirectly altering the incidence of tax – that could mean that anything you do that has the effect of reducing your tax could be caught. This could mean cutting your hours; paying off your mortgage instead of putting the money on term deposit; selling dividend paying shares to buy a car all could be classed as tax avoidance. As they were all plans or understandings – where the result was less tax was paid than before or less tax was paid than could have been.

Mmm yeah.

Now as that couldn’t possibly be right the courts – helped by the Commissioner taking cases – has said it only applies when the outcome wouldn’t have been intended by Parliament. Right. Awesome. So much clearer now. Thanks for playing.

To be fair there is a little more to it than that. But largely it all boils down to:

1) strip away the clever stuff

2) work out tax result on stripped down ‘arrangement’

3) compare 2) to what went of tax return

4) Difference is tax avoidance.

Now most of the dispute between taxpayers and Commissioner is over what if any is the ‘clever stuff’.

In our friend Penny and Hopper putting a business into a trust was never challenged – coz you know creditor protection or keeping it from the missus wasn’t ‘clever’ it was just like ‘commercially acceptable’. In that case what was challenged as ‘clever’ was the trust paying the highly skilled doctors the same salary as they would earn in the public system – I mean Dude seriously who works for that?

The other recent case that made the tax community super mad – Alesco – involved the New Zealand business being funded by an optional convertible note. Now dear readers you may say ‘ ah yes I’ve read I choose you Pikachu ‘ an optional convertible note now that is ‘clever’ and so that is tax avoidance. Glad you are keeping up – but no. No what was clever here was that the option should have no value as Alesco Australia already owned all the shares – Duh. Other highlights of that case included the taxpayer arguing that while it was tax avoidance – it was Australian not New Zealand tax avoidance. All class.

Compare these then to the cutting your hours; paying off your mortgage or buying a car from savings. Nothing clever there – so long as that is all you are doing. Bit like our gentlemen below.

Now of course there is a line between a bit of tax planning – paying off your mortage before earning taxable income; funding a project with deductible debt or even investing offshore and receiving an exempt dividend – and tax avoidance. And because there is this line there will always be a Tax Administration and tax practitioners.

The thing is though that even if it is ‘tax avoidance’ it is a Civil thing and so no one goes to jail. They can lose the tax benefits; get hit with a 100% penalty plus interest of 8% – but no prison wall. Not even Home D.

Tax evasion however game on – Criminal charges defo in the mix. Now generally there is nothing clever with tax evasion. Just dirty fraudulent or deceptive behaviour: taking money out of the till; cashies – yes cashies; billing for a lower/higher number than is actually the case. Here jail time is totes on the cards and does happen. As well as a penalty of 150% and interest. And yes there is a line between avoidance and evasion too.

So is tax avoidance legal if Wikiquote says so too? Dunno it certainly isn’t criminal but does have high penalties.

So keep away from the clever sh@te and my former colleagues will probs keep away from you.

Namaste

The Kiwi Temp

Let’s talk about tax, (withholding and labour hire firms).

Your (foreign) correspondent is in London this week catching up with friends and family over a quarter of a century since she arrived for her big OE. My timing was exquisite as the month I arrived – April 1990 – almost perfectly corresponded with the start of the Exchange Rate Mechanism recession and my departure in December 1993 with its ending.

Having lived through that I never want to live in a country again that does not have control of its monetary policy. For all Michael Reddell has concerns over Graeme Wheeler’s stewardship; what New Zealand is facing currently is nothing compared to what England in the early 90’s faced. That is being in recession with high interest rates all because Germany had inflationary pressures due to reunification.

The experience was all the more wonderful as my working career in New Zealand in the late 80’s as a junior accountant had involved losing my job twice without redundancy. Unlike a number of my peers though I was never unemployed. Had some less than wonderful employment experiences but never unemployed.

In April 1990 I had no idea though of the forthcoming recession and did what every other young antip professional did when arriving in London – I became a temp.

I worked for Warner Music using Lotus 123 to put together the monthly management accounts. This largely consisted on taking the general ledger and repackaging it into a usable form. It sounds easy but it wasn’t. My colleague whose desk was in front of mine did the same thing for the balance sheet. After several days and lots of checking with each other we would get the same number and we would stand up and high five each other. Yes we were cool. And our manager would then breathe a sigh of relief that he would be able to deliver that month.

I imagine Xero now does what Serjit and I did then.

Warner Music was based in North London – Alperton – and was a huge eyeopener for the white girl from Christchurch. Highlights included:

- My (Jewish) manager eating his bacon sandwich complaining like mad about the bombing of Jerusalem by Iraq because – it had interfered with the football game he was watching.

- Asking my very happily married (Sikh) colleague how he met his wife and being told it was arranged.

- That lots of the happily married young people in the warehouse and the office had arranged marriages.

- Being asked if New Zealand celebrated Christmas.

- Wearing jeans to work – it was a record company.

- Discovering that the white South African auditor was not only a perfectly reasonable human being – but that I had more in common with him than I did the English. FWIW the two of us discussing issues used to have the office in hysterics with our accents.

Anyway back to New Zealand tax. As a temp I worked for a labour hire company and not for Warner Music. The received wisdom was there were two ways I could be employed. Through my own personal services company which is what the cool kids did. They all had accountants and could claim expenses. Or through having PAYE deducted.

I cannot for the life of me remember why – but I went into the PAYE system. And oh man that was the right thing to do. I saved myself a world of pain because ultimately I saw the cool kids having to make appointments with accountants during chargeable work time; organise all their bank statements; and find cash for large tax payments. Although I didn’t see it I would imagine there was also a degree of just letting it all go and getting on a plane – effectively with their tax money -when their visa ended.

But all this ‘I am an independent contractor employed through a company’ stuff was a complete nonsense as they were employed by their labour hire firm as much as I was by mine.

Now Hon Mike is having a go at this nonsense in New Zealand. Nice one Hon Mike nice one. In the recent bill he is making labour hire firms withhold from all payments to all people and ‘companies’ they place. A good start. There is still all the people who contract outside those firms and whose activities are not on those schedules. You know – policy analysts for example. Next bill will be fine.

Recently the Labour party also had a go in this area trying to get the minimum wage legislation extended to contactors. The select committee report discusses the issues quite well including the general issue of the move from employees to contactors in the labour market which is of course a move out of withholding with the consequent risks to the PAYE tax base.

I was also pleased to see this discussion as in Budget 2012 the government replaced the child’s tax credit with a tax exemption for non PAYE income for children at school. David Cunliffe – I think – called it the Paper boy Tax budget. Nice line. But from the opposition there was a lot of wailing that these children would earn $20 for 5 hours work and now they would only get $17 because of tax. At the time I remember thinking:

- gosh that is a low hourly wage

- seriously – it is the tax that concerns you in that scenario?

But to be fair it was removed under budget night urgency where the opposition gets zero prep time. So with more prep we got the entirely sane and well thought out bill from David Parker. Tax however was missing.

It is entirely likely that such low income workers are using every dollar they earn and not meeting their tax obligations. Now Hon Mike you and I both know that this is called tax evasion. And you and I know this is a criminal offence; carrying a risk of a 150% penalty and jail time.

So Hon Mike how about a bit of joined up government. You already control the Revenue and Labour officials. Treasury whether it is Tax, Labour Markets and Welfare or Social Inclusion must also have a view.

And your government has made such an artform of swiping the best ideas from the opposition.

So go on. Nick this one too. Slap withholding obligations on the payer and call it your own.

Namaste