The Spike

Let’s talk about (the recent Greens’ press statement on) tax.

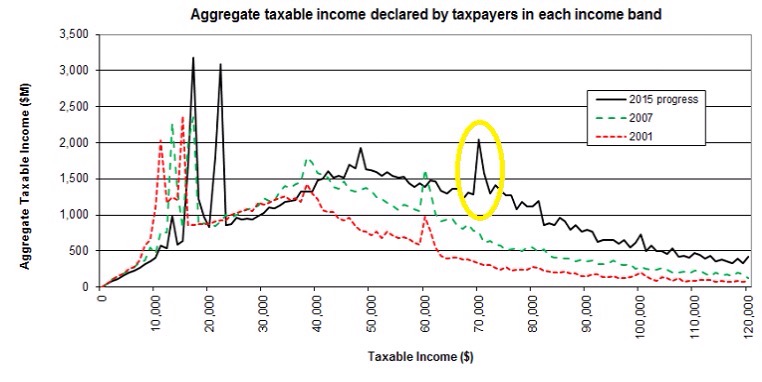

Recent data has shown there is a spike around $70,000 of reported taxable income for individuals – convienently the point where the top marginal tax rate of 33% starts. And according to the Greens this shows evidence of tax avoidance by rich people which can be fixed by – among other things – increasing Inland Revenue’s investigation budget. Mmm maybe.

Before I go on, I am working on the assumption that when the Greens talk about tax avoidance it is in the colloquial ‘not paying as much tax as I think you should’ kinda way rather than tax avoidance according to the actual law. All cool but unfortunately (or fortunately) the department is constrained by what Parliament has enacted and how the Courts have interpreted it.

Now in the mid 2000s – it is true – similar spikes were evidence of widespread tax avoidance among self-employed professionals. The wheeze was that they were employed by trusts which were taxed at 33% on the income the individuals earned – not the top individual’s rate of 39%. And then the trust paid the individuals a below market salary for their services to the trust.

Only the below market salary was taxed at 39% and the rest of the income at the lower trust rate. And then any tax paid income of the trust could then be distributed tax free to beneficiaries. Too easy and too good to be true. Hence tax avoidance according to the actual law.

Moving to 2017. The trust and top personal rate are the same so that particular wheeze won’t work. But now we just have misalignment between the company rate at 28% and the top personal rate of 33%.

Except that under a misalignment with the company rate there is no distributing the income tax free. When income is distributed from the company to the shareholder – a dividend – it is subject to another 5% tax. Now any ‘tax avoidance’ – in theory anyway – is just timing until the shareholder needs the money. There should be no ultimate reduction in tax. Although timing advantages can be a big deal and can also make something tax avoidance under the actual law.

But the only way I can see of moving this from tax avoidance – not paying as much tax as I think you should – to tax avoidance under the actual law is if the department can show that the $70k is not a market salary – as they did with the self employed professionals.

And while that wasn’t simple for the department last time – now all tax advisors know about the need for a market salary – possibly from painful personal experience. So anyone giving advice that $70k is an acceptable salary – when the market rate is higher – does so knowing it could be attacked by the department and will have all the supporting arguments ready.

But the Greens are right the spike is still there. Last time the spike was widespread tax avoidance according to the actual law – so why wouldn’t it be this time too? Not the first time I have lacked imagination.

Just in case tho I am right – I am also all about the solutions. And there is at least one way of getting rid of the spike without increasing anyone’s budget. Think of all that extra money Greens you could spend on cleaning up the rivers instead of tax inspectors.

One way is to increase the company tax rate to the top marginal rate.

Another way is to make the look-through company (LTC) rules compulsory.

Currently any company with five or fewer shareholders can choose not to be taxed as a company. Instead income and losses are taxed as if the shareholders had earned the money themselves. Except currently those rules are optional. Make them compulsory and the spike goes. No more income in more lowly taxed closely held companies as no more closely held companies for tax purposes. Simple.

And the really good news for the Greens is that there is currently a bill in the House making changes to the LTC rules; so a Supplementary Order Paper doing just that would be totes in scope. Oh and it is an ‘annual rates’ bill too so they could also have a go at the company tax rate at the same time. Awesome.

Now lots of people who haven’t made an LTC election may not like that and say so quite loudly. Coz that’s what you get when you are strong on policing tax avoidance – lots of upset people all with lots of incentive to write to you and come and tell you how upset they are.

But unless the current law with closely held companies – or company tax rate – changes I can’t see any level of increased funding will get rid of that nasty spike.

Namaste.

Timothy W Edgar (1960 – 2016)

2016 has been some year.

Donald Trump; Brexit and then the deaths of Leonard Cohen; David Bowie; Prince; George Martin; Helen Kelly; Zsa Zsa Gabor, George Michael as well as the heart attack of Carrie Fisher. But one friend has had a baby and two have got engaged – although not to each other – so not a complete write off.

One death though – that has recently made the international tax community poorer – was that of Tim Edgar a Canadian tax academic.

Tim originally trained as a lawyer – and taught at law schools – but a less lawyery person you could not meet. Cases drove him mental. Once in conversation he suggested that instead of the Courts we should just use a random number generator for tax avoidance. Although to be fair it would also work for any of the objective subjective cases like capital/revenue or residence.

Odd numbers for the Commissioner – even for the taxpayer. Very fair. And would – he argued – have the effect that taxpayers would just stay away from anything that would get them put in the generator in the first place. Good policy outcomes with reduced fiscal cost. What’s not to love?

Tim came to Wellington with his family on sabbatical in early 2000s and worked in Inland Revenue policy. I can’t remember what he was supposed to be working on – GST possibly – but because of his ability and good humour very quickly became a sounding board and contributor to pretty much every team in the division. He also lived close to me and our families had a lot to do with each other over that time. We introduced the Edgar family to the joys of Fish and Chips.

After that period in Wellington, we kept in touch and our paths crossed a number of times including a joint stint presenting an OECD course in India. Again his depth of knowledge and good humour made him very popular with the participants while his North American tipping practices made him popular with the staff at the hotel.

By the mid 2000s I had become completely obsessed by hybrids in the way my children were with pokemon. So I wanted to analyse them and their effects for my masters dissertation. There was a small difficulty in that there was no one in New Zealand with the expertise who could supervise me. So I approached Tim.

With his usual good humour and generosity – although possibly it was the opportunity to earn $100 in NZ foreign exchange that clinched it – he agreed. And within 2 weeks I had a parcel of the key items of the hybrids literature in my mailbox. Not sure that is standard operating practice for most supervisors. But then Tim wasn’t most people.

At the time (2004- 2006) there were two views on hybrids. The first – dude get over it countries can do what they like aka the sovereignty argument and the second – it is double non -taxation/ bad aka the economic distortion argument. I wasn’t fully convinced by either view. Tim, however, was very firmly in the latter camp and – quelle surprise – history has proved him right.

Tim was a high level strategic person – but in the sense that he did actually have big picture insights – rather than just someone who can’t cope with complexity or detail. He was expert in Financial Arrangements; GST; international tax; tax structuring or pretty much anything he decided to have a look at.

I particularly remember him sharing his views on formulary apportionment which is touted by parts of the left as the ‘fair’ way to allocate worldwide tax revenues. The thing is – he said – there is nothing normative about allocating through source and residence. What that has going for it though – is that all the countries agree. Formulary apportionment throws all that up in the air – and who knows where you’ll end up?’

We last caught up around his fiftieth birthday – which I am embarrassed to see is almost 5 years ago. He shared with me the changes in his personal and professional life and how proud he was with how his children were doing. He was more subdued than previously but was looking forward to the next stage of his life.

I don’t think this and similar articles was what he had in mind though – particularly as he was always so fit. I struggled to find a photo that represented how I remember him. Even this one which I swiped from his uni’s obituary doesn’t show the exuberant enthusiasm he had for discussing any one of the topics around his head.

I had him on my list of people to contact now I have left the reservation but sadly this post will have to do instead. I will however always remember the laughter, the low ego/high ability combo and the non-standard approach to thinking about tax.

So go well my dear friend. Hail and farewell.

Andrea

Thickness of a prison wall

Let’s talk about tax (and tax avoidance).

Last week the government announced it was building yet another prison. Another moral and fiscal failure. Skilfully continuing to over turn the falling crime rate dividend we had in 2013 before the bail laws changed.

Also last week a reader made a comment about how wasn’t tax avoidance ‘legal’.

Another such observation on tax avoidance came from Denis Healey who said that the difference between tax avoidance and tax evasion is the thickness of a prison wall. She said trying to link two quite independent things together.

Now both maybe right in the United Kingdom but they really don’t directly translate to the New Zealand situation. So being the public spirited individual I am I thought I’d have a go at a layman’s guide to tax avoidance for New Zealanders. And no more mention of prison stuff – promise.

First of all tax avoidance is a term defined in the Income Tax Act. It comes in and overrides everything else in the Income Tax Act. So any provison in the Act theoretically runs the risk of tax avoidance coming in and saying – ‘you know what’ just kidding – bog off.

And it is defined in a way – directly or indirectly altering the incidence of tax – that could mean that anything you do that has the effect of reducing your tax could be caught. This could mean cutting your hours; paying off your mortgage instead of putting the money on term deposit; selling dividend paying shares to buy a car all could be classed as tax avoidance. As they were all plans or understandings – where the result was less tax was paid than before or less tax was paid than could have been.

Mmm yeah.

Now as that couldn’t possibly be right the courts – helped by the Commissioner taking cases – has said it only applies when the outcome wouldn’t have been intended by Parliament. Right. Awesome. So much clearer now. Thanks for playing.

To be fair there is a little more to it than that. But largely it all boils down to:

1) strip away the clever stuff

2) work out tax result on stripped down ‘arrangement’

3) compare 2) to what went of tax return

4) Difference is tax avoidance.

Now most of the dispute between taxpayers and Commissioner is over what if any is the ‘clever stuff’.

In our friend Penny and Hopper putting a business into a trust was never challenged – coz you know creditor protection or keeping it from the missus wasn’t ‘clever’ it was just like ‘commercially acceptable’. In that case what was challenged as ‘clever’ was the trust paying the highly skilled doctors the same salary as they would earn in the public system – I mean Dude seriously who works for that?

The other recent case that made the tax community super mad – Alesco – involved the New Zealand business being funded by an optional convertible note. Now dear readers you may say ‘ ah yes I’ve read I choose you Pikachu ‘ an optional convertible note now that is ‘clever’ and so that is tax avoidance. Glad you are keeping up – but no. No what was clever here was that the option should have no value as Alesco Australia already owned all the shares – Duh. Other highlights of that case included the taxpayer arguing that while it was tax avoidance – it was Australian not New Zealand tax avoidance. All class.

Compare these then to the cutting your hours; paying off your mortgage or buying a car from savings. Nothing clever there – so long as that is all you are doing. Bit like our gentlemen below.

Now of course there is a line between a bit of tax planning – paying off your mortage before earning taxable income; funding a project with deductible debt or even investing offshore and receiving an exempt dividend – and tax avoidance. And because there is this line there will always be a Tax Administration and tax practitioners.

The thing is though that even if it is ‘tax avoidance’ it is a Civil thing and so no one goes to jail. They can lose the tax benefits; get hit with a 100% penalty plus interest of 8% – but no prison wall. Not even Home D.

Tax evasion however game on – Criminal charges defo in the mix. Now generally there is nothing clever with tax evasion. Just dirty fraudulent or deceptive behaviour: taking money out of the till; cashies – yes cashies; billing for a lower/higher number than is actually the case. Here jail time is totes on the cards and does happen. As well as a penalty of 150% and interest. And yes there is a line between avoidance and evasion too.

So is tax avoidance legal if Wikiquote says so too? Dunno it certainly isn’t criminal but does have high penalties.

So keep away from the clever sh@te and my former colleagues will probs keep away from you.

Namaste

‘But I’m a director of a land-owning company!’

Let’s talk about tax.

Or more particularly let’s talk about tax; interest deductions and private expenditure in companies.

Your correspondent has returned from her ‘retirement cruise’; is recovering from jetlag and has returned to what passes for work these days. That will dear readers include a return to twice weekly posting. As a change from some of the more political posts I thought I’d return to a technical issue for a bit of light relief.

Earlier this year while I was still inside I went to a dinner party in a provincial city. At the party was a delightful gentleman I had met previously and was more than pleased to see again. The feeling appeared to be mutual and our conversation broadly went like this:

DG – Now Andrea tell me – which is better? To pay my mortgage or to pay my tax?

Me – cough, splutter, mumble – well the thing is it isn’t a choice as tax is a legal obligation.

DG- oh don’t be silly of course I know that. What I mean is it better to have a mortgage on my house get the tax deductions and then have money to invest in shares and things for capital gains or have no mortgage not get the tax deductions but have more disposable income?

Me – Ah what makes you think you get a tax deduction for the mortgage on your house?

DG- This is the country – we get tax deductions for all sorts of things and besides I’m the director of a land owning company!

Me – Is that wine over there?

Now dear readers I am sure after Zen and the art of tax compliance you all know that to get tax deductions the expenditure has to be:

- Connected to the earning of income or in the ordinary course of a business and

- not private or domestic expenditure.

So therefore if DG owns his house in his own name – or in a family trust – as neither 1) or 2) is met there is no deduction for interest expenditure.

There is the possibility that if the money were borrowed on his house and used to buy shares THAT WERE DIVIDEND PAYING then the interest would be deductible. But if the money is borrowed to construct the house for him to live in – nuh.

The complication though is the comment about being a director of a land owning company. The rules above do not apply to a company and interest deductions. From about 2000 or so the rule broadly became:

- Are you a company resident in New Zealand?

- Have you incurred an interest expense?

If yes to both, then ‘would you like interest deductions with that?’

The private and domestic test still applies to such expenditure but I have always struggled to align any concept of private and domestic to a company.

So at first pass – yep – if DG holds his house in a company – in your correspondent’s view – he will get an interest deduction.

And yeah the Mixed Use Asset rules won’t apply here because ironically it isn’t a mixed use asset – it is wholly private and domestic.

But – not so fast – the music hasn’t stopped.

While there are special rules for companies and interest deductions there are also special (dividend) rules for transactions involving companies and shareholders aka ‘are policy makers really that dumb?’

These dividend rules say where ever there has been a transfer of value from a company to a shareholder there is a taxable dividend to the shareholder to the extent of the value transfer.

Ok again in English.

If a company gives a shareholder stuff – goods or services – that is a taxable dividend for the shareholder. Here the company has given the shareholder use of a house – so the shareholder DG – gets a taxable dividend.

And by ‘taxable dividend’ yes this means you need to put that value on your tax return and pay tax on it. And yes I know you didn’t get any actual cash but that doesn’t matter. You know how when you tick the box for dividend reinvestment on your publicly listed shares – you know how the dividend is still taxable even though you didn’t get any actual cash. Consider this as the same.

So what is the value that DG has received from the ‘land owning’ company? He has received the benefit of living in that house. And what do people usually pay for the benefit of living in a house they don’t own? You’re onto it – rent.

DG is then up for tax on the value of the rent not paid to the company as a dividend. And once more with feeling – it doesn’t matter that no cash has been paid from the company to the shareholder.

So the benefit DG received – use of the house without paying rent – is taxable to DG.

Now if DG has a tax rate of 33% – as the company tax rate is 28% – there will be a net 5% tax paid on the ‘imputed’ or deemed rent. That is he pays tax at 33% on the deemed rent and the company gets a deduction at 28% on the interest expense. In other words a gift to the people of New Zealand and how tax planning can go wrong. And if he didn’t know this was the case until my former colleagues come along – it will be 33% tax plus interest at about 8% plus a penalty of between 10% and 100%.

Awesome. Can only hope he didn’t also pay an agent for this wizard advice.

If his tax rate though is lower than the company rate this is where it could get really interesting. Technically even with DG putting the value of rent on his tax return there will still be a net tax deduction that ostensibly can be offset against other income.

In this case though the structure – or ‘arrangement’ as my former colleagues may start to call it – is really putting pressure on the whole ‘companies can’t have private expenditure’ thing. And from here we move into a complete world of pain – or ‘good case’ depending on which side you are on this – known as tax avoidance. Now the entire interest deduction is at risk with tax avoidance penalties of between 50% and 100%. Fun huh.

And don’t even think of paying rent to your company and making it a look through company so you get the deductions directly against your other income. The department was very clear with look through companies – the prequel – that this was tax avoidance too.

So DG I am not sure there really is any ‘country immunity’ for interest on your personal mortgage. Pay it but step away from the tax system. There be dragons.

Namaste