Tax and Small Business

Last week the Small Business Council issued its report to Government. I am sure there are many wizard things in there maybe even some tax recs.

Also last week I had a friend to stay who is helping some workers that have lost thousands of dollars of wages and holiday pay when their employer went into receivership. Her expression was Wage Theft. It is a crime in Australia but not in New Zealand. Unlike theft as a servant which totally is.

Talking to her it was obvious that there was considerable overlap between what she is seeing and the issues considered by the TWG of closely held companies where the directors have an ownership interest not paying PAYE and GST (1).

And yes my friend’s friends are worried about their PAYE and KiwiSaver deductions. So really hope tightening up on this stuff is in the Small Business report along with the expected recs on compliance cost reduction.

I am also personally very interested in what the Group comes up with as the Productivity Commission noted that NZ has a lot of small low productivity firms without an up or out dynamic (2). That is firms tieing up capital that should be released for more productive purposes with the associated benefit of not staying on too long and dragging their workers and the tax base with them.

Now ever since I found that reference I have been concerned that there may be aspects of the tax system that may be driving that. Benefits or ‘opportunities’ that don’t arise for employees subject to PAYE or owners of widely held businesses subject to audits and outside shareholder scrutiny.

And it is true that there is nothing particularly special in a tax sense here to New Zealand. However given that New Zealand rates as number one in the ease of doing business index there may be more people going into business than would be the case in other countries.

Some of these aspects can be reduced through stricter enforcement by Inland Revenue but are otherwise largely structural in a self assessment tax system where the department doesn’t audit every taxpayer. One is a policy choice possibly because the alternative would add significant complexity to the tax system and the final example is a combination of the need for stronger enforcement and/or policy changes needed now that the company and top personal rate are destined to be permanently misaligned.

So what are these ‘aspects’?

Concealing income or deducting private expenses

Recent work by Norman Gemmell and Ana Cabal found that the self employed had 20% higher consumption than the PAYE employed at the same levels of taxable income.

Now it could be that for some reason the extra consumption of the self employed comes from inheritances or untaxed capital gains or taking loans from their business – more on that later – more so than those in the PAYE system or owners of widely held businesses. It might not be tax evasion at all.

But we just don’t know.

All we know is the 20% extra consumption and that there is a greater opportunity and fewer checks with closely held businesses to conceal income or deduct personal expenses. And Inland Revenue says such levels are comparable with other countries.

While things like greater withholding taxes and/or reporting can help, I am also concerned that with greater automation it also becomes much easier to have those personal expenses effortlessly charged against the business rather than recorded as personal drawings.

Interest Deductions

The second aspect is my specialist subject of interest deductions. Unlike concealing income or deducting personal expenditure – this one is totes legit.

Interest is fully deductible to a company and for everyone else it is deductible if it can be linked to a taxable income earning purpose or income stream aka tracing.

What that means is if a business person has a house of $2 million and a business of $1 million and has debt of $1 million – all the interest deductions on the debt can be tax deductible – if the debt can be linked to the business. This can be compared to a house of $2 million and debt of $1 million – and no business – where none of it is deductible.

To make this fairer with taxpayers who don’t have the opportunity to structure their debt there would need to be some form of apportionment over all assets – business and personal. So in the above example interest on only $330,000 should be allowed.

But yes – that would require a form of valuation of personal and business assets. And yes valuing goodwill brings up all the same – valid – concerns raised with taxing more capital gains.

So I guess we can say that under the status quo fairness – and possibly capital allocation – have been traded off against compliance costs.

Income Splitting

The third is the ability to income split with partners to take advantage of the progressive tax scale. Now this is only actually allowed if the partner is doing work for the business. But verifying the scale and degree of this work – even with burden of proof on Commissioner – is a big if not impossible task for the Commissioner.

Other mechanisms include loans from the partner to help max out the lower income tax bands.

And the statistics would support an argument that there is a degree of maxing out the lower bands just not that there necessarily is a lot of income splitting.

Interestingly both Canada and Australia have rules for personal services companies where these types of deductions are not allowed.

But this is ok if this is the amount of value going to the shareholders. Maybe our firms are so unproductive that they can only support shareholder salaries of $70k and below.

If that were the case though we wouldn’t be seeing the final aspect which is taking loans from companies you control instead of taxable dividends.

Overdrawn shareholder current accounts

Now to be fair for this to occur there should also be interest paid by the shareholder to the company on loans from the company to the shareholder. And unlike the interest in point 2 – none of this should be tax deductible to shareholder if it is funding personal expenditure while the interest received will be taxable. This on its own should be enough to not do it and receive taxable dividends instead.

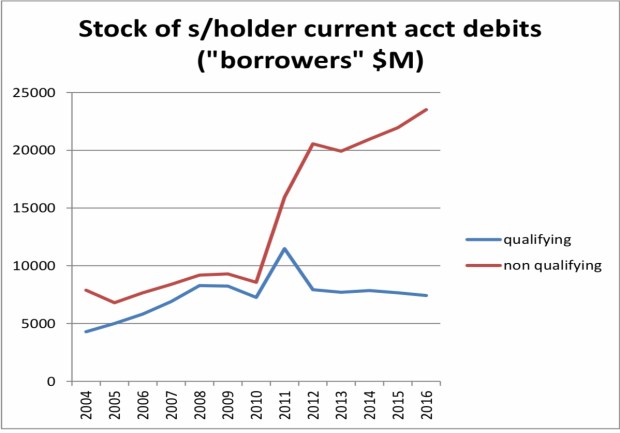

Unfortunately the facts also don’t seem to back this up. Imputation credit account balances – meaning tax has been paid but not distributed- have been climbing. Now this could be like totally awesome if it meant all the money was being retained in the company to grow.

Except that overdrawn current account balances – loans from the company to the shareholders- have been similarly growing too. Now sitting at about $25 billion.

And yes this all started from about 2010. And what happened in 2010? Why dear readers the company tax rate was cut to 28% while the trust rate remained at 33%.

Ironically the associated cut in top marginal rate was to stop the income shifting that went on between personal income and the trust rate.

Now one level it shouldn’t matter at all if these balances continue to climb so long as non- deductible assessable interest is paid on the debt. However an overdrawn current account is – imho – the gateway drug to dividend avoidance.

And yes that can be tax avoidance but much like the tax evasion opportunities, income splitting and interest on overdrawn current accounts – all of this requires enforcement by Inland Revenue. And as they can’t audit everyone there will always be a degree that is structural in a self assessment tax system.

But the underlying driver of people wanting to take loans from their company rather than imputed dividends is that our top personal tax rate and company tax rate are not the same. Paying a dividend would require another 5% tax to be paid.

Possible options

Now other countries have always had a gap between the top rate and either the company or trust rate so this shouldn’t be the end of the world. But those countries have buttressing rules that we don’t have in New Zealand. The personal services company rules discussed above or the accumulated earnings tax in the US (3) or the Australian rule that deems such loans to be dividends.

Until recently I had been a fan of making the look through company rules compulsory for any company that was currently eligible. (4) I couldn’t see the downside. The closely held business really is an extension of its shareholder so why not stop pretending and tax them correctly.

However some very kind friends have been in my ear and pointed out the difficulties of taxing the shareholder when all the income and cash to pay the tax was in the company. It works ok when it is just losses being passed through. So maybe I am less bullish now.

An alternative approach could be to apply a weighted average of the shareholders tax rates on the basis that all the income would be distributed. Similar to PIEs. The tax liability is with the entity but the rate is based on the shareholders. I guess you then do a mock distribution to the shareholders which can then be distributed to them tax free. And yes only to closely held companies. Wider would be a nightmare.

Kind of a PIE meets LTC.

Or you could just old school it and raise the company tax rate to 33% for all companies. Shareholders with tax rates below that could use the LTC rules and make the assessment of whether the compliance of the rules was greater or less than the extra tax.

It would require an adjustment to the thin capitalisation rules by increasing the deductible debt levels to ensure foreign investment didn’t pay more tax. But for some of you dear readers increased taxation on foreign investment might even be a plus.

But all in all I don’t think the status quo with small business is a goer. Whether it is for fairness reasons, or capital allocation reasons or simply stopping me worrying – doing something is a really good idea.

Because I would hate to think any of this was enabling behaviours that kept people in business longer than they should. And even with the most whizziest of new IRD computers – there will always be limits on enforcement.

Andrea

(1) Page 116 Paragraph 68

(2) Page 19

(3) Although it would make more sense to only apply this to the extend that the income hasn’t been retained in the business and distributed in non- dividend form.

(4) Yes there is the issue that companies could start adding an extra class of share to get around this. But I don’t believe this is insurmountable with de minimis levels of additional categories and the odd antiavoidance rule for good measure. It is even the advice of KPMG so clearly not that wacky.

Tax and politics

Your correspondent is back from Sydney. Had a great time because – well – Sydney.

Managed to score a gig on a panel at the TP Minds conference talking about international policy developments for transfer pricing. An interesting experience as I am pretty strong in most tax areas except GST – and you guessed it – transfer pricing.

But it was ok as I did a bit of prep and all those years of working with the TP people paid off. And of course I do know a little bit about international tax and BEPS so alg.

Even a techo tax conference again reminded me just how different – socially and culturally – Australia is to New Zealand. Examples include: the expression man in the pub being used without any sense of irony or embarrassment and one of the presenters – a senior cool woman from the ATO – wearing a hijab.

Can’t imagine either in tax circles in NZ.

My particular favourite though was watching the telly which showed a clip of Bill Shorten describing franking (imputation) credits as something you haven’t earned and a gift from the government. Now Australia does cash out franking credits but – wow – seriously just wow. Kinda puts any gripes I might have about Jacinda talking about a capital gains tax into perspective.

And in the short time I have been away yet another minor party has formed as well as the continuation of the utter dismay from progressives over the CGT announcement.

In the latter case I am fielding more than a few queries as to what the alternatives actually are to tax fairness is a world where a CGT has been ruled out pretty much for my lifetime.

Now while I have previously had a bit of a riff as to what the options could be, I have been having a think about what I would do if I were ever the ‘in charge person’ – as my kids used to say – for tax.

To become this ‘in charge person’ I guess I’d also have to set up a minor party although minor parties and tax policies are both historically pretty inimical to gaining parliamentary power.

But in for a penny – in for a pound what would be the policies of an Andrea Tax Party be?

Here goes:

Policy 1: All income of closely held companies will be taxed in the hands of its shareholders

First I’d look to getting the existing small company/shareholder tax base tidied up.

On one hand we have the whole corporate veil – companies are legally separate from their shareholders – thing. But then as the closely held shareholders control the company they can take loans from the company – which they may or may not pay interest on depending on how well IRD is enforcing the law – and take salaries from the company below the top marginal tax rate.

On the other hand we have look through company rules – which say the company and the shareholder are economically the same and so income of the company can be taxed in the hands of the shareholder instead. But because these rules are optional they will only be used if the company has losses or low levels of taxable income.

My view is that given the reality of how small companies operate – company and shareholders are in effect the same – taking down the wall for tax is the most intellectual honest thing to do. Might even raise revenue. Would defo stop the spike of income at $70,000 and most likely the escalating overdrawn current account balances.

So look through company rules – or equivalent – for all closely held companies. FWIW was pretty much the rec of the OG Tax Review 2001 (1).

Now that the tax base is sorted out – if someone wants to add another higher rate to the progressive tax scale – fill your boots. But my GenX and tbh past relatively high income earning instincts aren’t feeling it.

Policy 2: Extensive use of withholding taxes

The self employed consume 20% more at the same levels of taxable income as the employed employed. Sit with that for a minute.

20% more.

Now the self employed could have greater levels of inherited wealth, untaxed capital gains or like really awesome vegetable gardens.

Mmm yes.

Or its tax evasion. Cash jobs, not declaring income, income splitting or claiming personal expenses against taxable income.

Now in the past I have got a bit precious about the use of the term tax evasion or tax avoidance but I am happy to use the term here. This is tax evasion.

IRD says that puts New Zealand at internationally comparable levels (2). Gosh well that’s ok then.

Not putting income on a tax return needs to be hit with withholding taxes. Any payment to a provider of labour – who doesn’t employ others – needs to have withholding taxes deducted.

Cash jobs need hit by legally limiting the level of payments allowed. Australia is moving to $10,000 but why not – say $200? I mean who other than drug dealers carries that much cash anyway?

Claiming personal expenses is much harder. This we will have to rely on enforcement for.

Policy 3: Apportion interest deductions between private and business

Currently all interest deductions are allowable for companies – because compliance costs. Otherwise interest is allowed as a deduction if the funding is directly connected to a business thing.

Seems ok.

What it means though is that for someone with a small business and personal assets such as a house, all borrowing can go against the business and be fully deductible.

Options include some form of limitation like thin capitalisation or debt stacking rules. I’d be keen though on apportionment. If you have $2 million in total assets and $1 million of debt – then only 50% of the interest payable is deductible.

Policy 4: Clawback deductions where capital gains are earned

Currently so long as expenditure is connected with earning taxable income it is tax deductible. It doesn’t matter how much taxable income is actually earned or if other non-taxable income is earned as well.

Most obvious example is interest and rental income. So long as the interest is connected with the rent it is deductible even if a non-taxable capital gain is also earned.

One way of limiting this effect is the loss ringfencing rules being introduced by the government. Another way would be – when an asset or business is sold for a profit – clawback any loss offsets arising from that business or asset. Yes you would need grouping rules but the last government brought in exactly the necessary technology with its R&D cashing out losses (4).

Policy 5: Publication of tax positions

And finally just to make sure my party is never elected – taxable income and tax paid of all taxpayers – just like in Scandinavia will be published. Because if everyone is paying what they ought. Nothing to hide. And would actually give public information as to what is going on.

Options not included

What’s not there is any form of taxation of imputed income like rfrm. It isn’t a bad policy but taxing something completely independent of what has actually happened – up or down – doesn’t sit well with me.

Also no mention of inheritance tax. Again not a bad policy I’d just prefer to tax people when they are alive.

And for international tax I think keep the pressure on via the OECD because the current proposals plus what has already been enacted in New Zealand is already pretty comprehensive.

Now I know none of this is exactly exciting and so I’ll get the youth wing to do the next post.

Andrea

(1) Overview IX

(2) Paragraph 6

(3) Treatment of interest when asset held in a corporate structure

(4) Page 11 onward

Coz everyone else pays their taxes

Now the most logical next post would be a discussion of the OECD digital proposals as that is the international consensus thing I am so keen on and also fits nicely into the thread of these posts.

The slight difficulty is that this requires me to do some work which is always a bit of a drag and when I am suffering badly from jetlag – an insurmountable hurdle.

So as a bit of light relief I thought I’d have a bit of a pick into the narrative around multinationals and why their non-taxpaying is particularly egregious.

You know the whole small business pays tax so large business should too thing.

Now because of the tax secrecy thing, we can never know for def whether this is the case. But there is some stuff in the public domain, so let’s see what we can do as a bit of an incomplete records exercise.

In one of the early papers for the TWG, officials had a look at tax paying of certain industries. Now while the punchline – industries with high levels of capital gains pay less tax – is well known, there are some other factoids that are worth considering.

Factoid 1 The majority of small businesses are in loss (1). Ok wow. But that could be fine if all the income was being paid out to shareholders.

Factoid 2 Spike of incomes at $70k. Ok suspicious I’ll give you that. But maybe there are lots of tax paid trust distributions.

Factoid 3 Shareholder borrowings from the company (2) – aka overdrawn current account balances – have been climbing since the reduction in the company tax rate in 2010. Oh and the imputation credit balances have been climbing over that period too (3). But that could be fine if interest and/or fringe benefit tax is paid on the balances.

Factoid 4 Consumption by the self employed is 20% higher than by the employed for the same taxable income levels. But this could be fine if the self employed have tax paid or correctly un-tax paid – like capital gains – sources of wealth that the employed don’t have.

Factoid 5 In 2014 high wealth individuals had $60 million in losses (4) in their own name. But that could be ok because if companies and trusts have been paying tax and they have been receiving tax paid distributions from their trusts.

Factoid 6 Directors with an economic ownership in their company are rarely personally liable for any tax their company doesn’t pay. Because corporate veil. And that even includes PAYE and Kiwisaver they have deducted from their employees.

Now all of this is before you get to the ability small business has to structure their personal equity so that any debt they take on is tax deductible. Not to mention the whole accidentally putting personal expenditure through the business accounts thing.

And of course I am sure none of this has any relevance to the Productivity Commission’s concern that New Zealand has long tail of low productivity firms [without] an “up or out” dynamic. (5)

But is it all ok?

- Are there lots of taxpaid trust distributions? We know the absolute level (6) but not whether it is ‘enough’.

- Is interest or FBT being paid on overdrawn current accounts?

- Do the self employed have sources of taxpaid wealth that the employed don’t have?

- Why have some of our richest people still got losses?

- How much tax do directors of companies in which they have an economic interest walk away from?

- What is the level of personal expenditure being claimed against business income? Or at least what is the level that IRD counters?

Dunno.

Combination of tax secrecy and information not currently collected. But IRD are working towards an information plan and the TWG have called for greater transparency.

Awesome.

Coz most of this is currently totes legit. In much the same way as the multinationals structures are.

Just saying.

Andrea

(1) Footnote 9

(2) Page 11

(3) Page 10

(4) Page 15

(5) Page 19

(6) Page 9

Taxing multinationals (2) – the early responses

Ok. So the story so far.

The international consensus on taxing business income when there is a foreign taxpayer is: physical presence – go nuts; otherwise – back off.

And all this was totally fine when a physical presence was needed to earn business income. After the internet – not so much. And with it went source countries rights to tax such income.

Tax deductions

However none of this is say that if there is a physical presence, or investment through a New Zealand resident company, the foreign taxpayer necessarily is showering the crown accounts in gold.

As just because income is subject to tax, does not necessarily mean tax is paid.

And the difference dear readers is tax deductions. Also credits but they can stand down for this post.

Now the entry level tax deduction is interest. Intermediate and advanced include royalties, management fees and depreciation, but they can also stand down for this post.

The total wheeze about interest deductions – cross border – is that the deduction reduces tax at the company rate while the associated interest income is taxed at most at 10%. [And in my day, that didn’t always happen. So tax deduction for the payment and no tax on the income. Wizard.]

Now the Government is not a complete eejit and so in the mid 90’s thin capitalisation rules were brought in. Their gig is to limit the amount of interest deduction with reference to the financial arrangements or deductible debt compared to the assets of the company.

Originally 75% was ok but then Bill English brought that down to 60% at the same time he increased GST while decreasing the top personal rate and the company tax rate. And yes a bunch of other stuff too.

But as always there are details that don’t work out too well. And between Judith and Stuart – most got fixed. Michael Woodhouse also fixed the ‘not paying taxing on interest to foreigners’ wheeze.

There was also the most sublime way of not paying tax but in a way that had the potential for individual countries to smugly think they were ok and it was the counterparty country that was being ripped off. So good.

That is – my personal favourite – hybrids.

Until countries worked out that this meant that cross border investment paid less tax than domestic investment. Mmmm maybe not so good. So the OECD then came up with some eyewatering responses most of which were legislated for here. All quite hard. So I guess they won’t get used so much anymore. Trying not to have an adverse emotional reaction to that.

Now all of this stuff applies to foreign investment rather than multinationals per se. It most certainly affects investment from Australia to New Zealand which may be simply binational rather than multinational.

Diverted profits tax

As nature abhors a vacuum while this was being worked through at the OECD, the UK came up with its own innovation – the diverted profits tax. And at the time it galvanised the Left in a way that perplexed me. Now I see it was more of a rallying cry borne of frustration. But current Andrea is always so much smarter than past Andrea.

At the time I would often ask its advocates what that thought it was. The response I tended to get was a version of:

Inland Revenue can look at a multinational operating here and if they haven’t paid enough tax, they can work out how much income has been diverted away from New Zealand and impose the tax on that.

Ok – past Andrea would say – what you have described is a version of the general anti avoidance rule we have already – but that isn’t. What it actually is is a form of specific anti avoidance rule targetted at situations where companies are doing clever things to avoid having a physical taxable presence. [Or in the UK’s case profits to a tax haven. But dude seriously that is what CFC rules are for]

It is a pretty hard core anti avoidance rule as it imposes a tax – outside the scope of the tax treaties – far in excess of normal taxation.

And this ‘outside the scope of the tax treaties’ thing should not be underplayed. It is saying that the deals struck with other countries on taxing exactly this sort of income can be walked around. And while it is currently having a go at the US tech companies, this type of technology can easily become pointed at small vulnerable countries. All why trying for an new international consensus – and quickly – is so important.

In the end I decided explaining is losing and that I should just treat the campaign for a diverted profits tax as merely an expression of the tax fairness concern. Which in turn puts pressure on the OECD countries to do something more real.

Aka I got over myself.

In NZ we got a DPT lite. A specific anti avoidance rule inside the income tax system. I am still not sure why the general anti avoidance rule wouldn’t have picked up the clever stuff. But I am getting over myself.

Of course no form of diverted profits tax is of any use when there is no form of cleverness. It doesn’t work where there is a physical presence or when business income can be earned – totes legit – without a physical presence.

And isn’t this the real issue?

Andrea

Let’s rendez-vous in the Pacific

Let’s talk about tax (and interest deductions for capital gains).

While your correspondent is a confirmed Anglican – Episcopalian actually – I don’t consider myself a Christian anymore and haven’t taken communion for over twenty years. The same cannot be said for the rest of my extended family which is pretty hard core christian and includes three ordained priests. It used to be overrun with lawyers so priests is definitely pareto improvement.

From time to time at family gatherings when my darling christian family is discussing something theological – yes it is fun but I love them a lot – one of them will say ‘but of course it all went wrong at the Council of Nicaea’. That I think was when the Christian Church became a proper institution and started telling its followers what to do. And having seen public institutions operate at times for themselves rather than the people they are serving I am sympathetic to that view.

But for tax – in New Zealand – its Council of Nicaea was the 1986 Pacific Rendezvous case.

Pacific Rendezvous was – and is – a motel. They wanted to sell the business but to get a better price they decided they needed to do some capital works. They borrowed money to do that and claimed most of the interest as a tax deduction.

They were pretty open that the building works were because they wanted to get a better price for the sale of their business. And of course we all know dear readers that the proceeds from a sale of a business that was not started with the intention of sale is tax free.

Unsurprisingly the Commissioner – who was a he at the time – was not best pleased. Deductions to earn untaxed income you cannot be serious. And so he took Pacific Rendezvous to court to overturn the deductions associated with the tax free capital bit.

But the Courts were like ‘nah totes fine’. Coz – get this – the interest was also connected with earning taxable income. You know the like really small motel fees even tho the whole gig was an ‘enhancing the business ahead of sale’ thing.

Impressive.

And that dear readers is why I am so not a lawyer. Having to hold such stuff in my head as legit would totally make it explode.

But I digress.

Now of course Parliament or the government at the time still had the chance to overturn that case coz of course Parliament, not the courts, has the final say. Or it could have simply taxed the capital returns – sorry now I am just being silly.

What actually happened was some 13 years later after a fruitless interpretative tour of the provisions Bill English – when he was just a little baby MoF and long before his two stints at the leader thing – proposed and Michael Cullen enacted – that companies could have as many interest deductions as they wanted because compliance costs. You know coz otherwise ‘they’ll just use trusts’.

It was subject to the thin capitalisation rules and as the banks were to discover to their chagrin – the anti avoidance rules – but deductions to earn capital profits game on.

Now the capital profits thing was considered at the time – chapter 4 – and quite a compelling economic case was made for some form of interest restriction. But by Chapter 6 there became insurrountable practical issues that made this not possible. Those issues included:

- The need for rules to ensure that the deduction was not separated from the capital income;

- Difficulties with bringing in unrealised gains;

- If done on realisation – potential issues with retropective adjustments along period capital gain was earned;

- Need to factor in capital losses.

And it was true that in the past Muldoon – well then must be wrong – had attempted to do something by clawing back interest deductions to the extent a capital gain was made. Imaginatively it was called ‘clawback’ and everyone hated it. And yes people did use trusts and holding companies to avoid it. Oh and soz can’t find a decent link to reference this so you will just have to trust me on this.

But you know what? Tax policy is so much cleverer now and we group companies and treat them as one entity for losses and lots of other stuff all which could get around these issues. In fact the recent National governments in a bipartisan and a thinking only of the tax system way have enacted rules that mean interest restrictions for capital gains are no longer the insurrountable issue they apparently were in 1999. Who says John Key doesn’t have a legacy?

So working up the list.

- Can’t see the issue with capital losses as if that capital was lost in a closely held setting on deductible expenses it is already fully deductible. Outside that any interest limitation for capital gains would only apply to the extent there was untaxed capital income. And as we are talking about losses – not income – no interest restrictions. Simple.

- Would only do it on realisation. Taxing unrealised stuff while technically correct is a compliance nightmare. But the new R&D rules which claw back cashed out losses when a capital gain is made – from page 24 – could totes be made to work here. Interest deductions could be allowed on a current year basis but if a capital profit is made – they are clawed back in the year of sale. If deferral was still a big deal – a use of money charge could be added in too. Personally I would give up the interest charge. Simpler and an acknowledgement of the earning of taxed income.

- And the whole deduction being separated from income was fixed with the debt stacking rules for mixed use assets. So let’s use that.

Coz the thing is while no one seems to be bringing in a capital gains tax anymore it is still massively anomalous that deductions are allowed for earning untaxed income just coz some incidental income was earned as well.

Now Labour is planning to have a bit of a go in this area by going after negative gearing through ringfencing losses. Better than nothing I guess. But still kinda partial as only touches people with not enough rental income to offset the deductions. And Grant, Phil and the new Michael – even for this – you totes will need the debt stacking rules or else ‘they’ll just use trusts’ or holding companies.

And yeah extending the brightline test to 5 years. Again better than nothing but there is still lots of scope to play the whole deductions for untaxed gains for property holdings over 5 years or – as with Pacific Rendezvous themselves – businesses.

But for any other political party with an allergy to a capital gains tax but big on the whole tax fairness thing perhaps you might want to look again at interest clawback on sale? This time thanks to the foresight and the public spirited nature of the John Key led governments – it would actually work.

Namaste

Trumping the tax system

Let’s (briefly) talk about tax (and Donald Trump).

Your (foreign) correspondent is very comfortably ensconced in the spare bedroom of her darling friend in Geneva. Reviewing my Facebook newsfeed – as well as giving me the most recent memory of my son and his girlfriend looking totally adorable going to a ball last year – was someone sharing this:

It discusses that Donald Trump claimed a $915 million loss in 1995 that could then be offset against any taxable income for the next 15 years.

Now the thing dear readers is – as I discussed in ‘The apple doesn’t fall far from the tree’ that is technically totes possible in New Zealand too. Putting capital into a business – spending it on business expenses – and then losing it will give you future losses to offset against other taxable income. But unlike in the US if you sell the business – rather than the company – for a capital gain the company keeps the losses and gets a capital gain that can be distributed tax free on liquidation.

And if it is done through a Look through Company the losses and the capital gains can pass through to the individual shareholders.

Now all of this could be totes fabulous as a means of encouraging entrepeneurship and innovation or simply entrencing dynastic behaviours. Couldn’t tell you.

Maybe Grant something for your ‘Fairness’ working group?

Namaste

‘I choose you – Pikachu!’

Let’s tax about tax (and hybrids).

Early in my first stint in the field I properly discovered hybrids. I was just so impressed. Impressed in a German high command discovering Enigma had been cracked kinda way – but impressed none the less. Here were instruments/entities/transfers that could render up tax benefits without tax authorities getting exercised and using words like avoidance, unacceptable or frustration. In the midst of the Structured Finance investigations to look at something so clean and so simple but so (tax) deadly was awe inspiring.

Some people may remember where they were when JFK was shot. I remember when I fully analysed my first Australian Limited Partnership – sitting at my desk at work – ticking off all the legs; finding it fully complied with Australia AND New Zealand’s law but it generated a net deduction. Like I say – completely blown away. As time went on I started to see a place for those words avoidance, unacceptable and frustration- but first love is a very special thing. Ash Ketchem may have got subsequent pokemon but Pikachu was always his first love; and the Australian Limited Partnership was my Pikachu.

And then like pokemon once you see/catch one – you start seeing them everywhere. There were your every day hybrids hiding in plain sight like the workhorse the redeemable preference share. Like Bulbasaur, solid and dependable. Deductible in Australia and imputable in New Zealand – until they weren’t. Then came blasts from the past the convertible note sisters – mandatory and optional – Squirtle and Charmander respectively. Deductible in New Zealand and not taxable in Australia. Or even the well old vehicle the New Zealand unit trust, like Snorlax always there. Loss consolidatable in Australia and New Zealand – until it wasn’t.

Charizard, or repos, played a major part in the Structured Finance transactions. Full bodied and lethal. Here legal ownership was recognised in New Zealand but not in the United States. Whoa. Definitely an evolved form.

There were also lesser known ones. The New Zealand unlimited company – like a company but with no ltd at the end. Kind of an Ekans with no tail. Company treatment in New Zealand and partnership in United States. Losses counted twice – Awesome.

And not to be out done New Zealand also created its own. The New Zealand Limited Partnership; like an Australian Limited Partnership but newer. So Raichu in other words.

There were also exotic ones. My particular favourite was the mandatory preferred partnership interest aka the redeemable preference share for limited partnerships. Like Togepie (or Jigglypuff) just so cute.

So many pokemon hybrids so little time!

But now Hons Bill and Mike have decided they should all get back in their balls; pokemongo should be deactivated; and the gameboys should be retired. Good call boys good call. Because like pokemon they were glorious but now it is time for us all to do some real work.

Namaste

The apple doesn’t fall far from the tree

Let’s talk about tax.

Or more particularly let’s talk about how New Zealand doesn’t tax capital gains.

There was a delightful expression I learnt as a junior official to describe situations which make absolutely no sense but are absolutely impossible to change – historic reasons.

So for historic reasons we

- Drive on the left

- Start school at 5

- Don’t compulsorily learn our second official language

- Build houses as one offs

- Treat renting as a short term activity

- Have a 3 year electoral cycle

- Imprison Maori at a disproportionate rate to Pakeha.

And in tax we don’t (theoretically) tax capital gains. In the late 80’s the government of the day did try but that was a step too far for the populace to accept.

There is a vague intellectual basis to the distinction between taxable and non-taxable returns from capital that doesn’t apply to returns from labour which are always taxable. Class oppression anyone?

It comes from an American case – whose name escapes me – which set out that the fruit of the tree was taxable as income while the growth in the tree – wasn’t. Of course both the apple and the bigger tree made its owner richer. In accounting changes in the balance sheet are generally income but in tax income – something wot comes in – was only the apple and under an income tax only the apple could be taxed. Continues to amaze me that more of the Monty Pythons weren’t lawyers.

Now in yoga the tree pose is a great pose for balance, focus and clarity of thought but a practice consisting of just the tree pose would be very unbalanced.

And here’s the thing. All this apple – tree stuff is fabulous until such time as the tree says: ‘You know what? Following a strategic review of our business model we need to make efficiencies in our supply chain. Therefore we should get out of apple production and fully focus on opportunities reflected in the ‘getting bigger’ market. We are deeply offended that the Commissioner could suggest that this was in any way related to the tax settings.’

So in the face of all this completely non-tax driven strategic behaviour successive governments – all of whom would never bring in a capital gains tax – have brought in the following:

- Land rules for developers – returns on buying and selling land if a developer taxable

- Financial arrangement rules – tax tree like gains on financial instruments

- Dividend rules – distributions of capital gains to shareholders – other than on winding up – are taxed

- Foreign portfolio share rules – tax an imputed return

- Revenue account property – assets bought with the intention of resale (good luck on proving that Mrs Commissioner) are taxed when sold

- Taxed distributions from non-complying trusts

- Restraints of Trade and inducement payments are taxed

- Lease inducement payments are taxed

- Residential property sold within 2 years – aka the brightline test

The very major advantage to this approach is that when tree like returns are deemed to be apples, they are taxed fully at the receipient’s marginal rate. None of this 15% stuff which just reduces the incentive for the tree to get strategic rather than eliminates it.

But yeah even with all this fabulousness we still have holes in our base as a result of the residual apple-tree stuff. Aside from the whole appreciating Auckland residential property skewing intergenerational relations and exacerbating class boundries thing; sales of businesses and farms – even serial sales so long as they weren’t purchased with the intention of resale – are tree like returns and not subject to tax.

And as an extra bit of icing, expenses incurred in building up the farm or business, so long as they met the general deductibilty tests, are not clawed back. Arguably the income from those businesses and farms are still subject to tax but only if the purchase price wasn’t heavily debt funded.

So yeah lefty friends while 15% taxation on realised capital gains wasn’t as good as full marginal rates – I see what you were doing there. Incremental improvement and all that. Half the income at marginal rates might interface better with the existing system though.

Now tax peeps yep it is also true that tree-like falls in value are also not deductible so that there is a degree of symmetry there. And that is absolutely the case when there is no control of the company. So yep the two years savings I invested in the sharemarket 85-87 and lost in October 87 was a non-deductible capital loss.

However if capital is put into a company; spent on legitimate business expenses that are tax deductible and ultimately lost; that loss can be grouped with other companies that have the same or similar (67%) shareholding. And if that company is a look through company it can be offset against the income of the shareholders.

So yeah 15% on realised gains would have been a good start. Shame no one can get elected on it.

Namaste