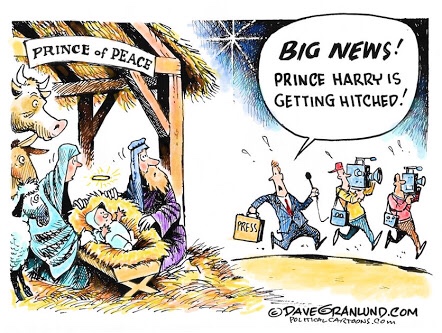

When Harry met FATCA

Let’s talk about tax.

Or more particularly let’s talk about the taxation of US citizens living abroad.

I just love the Royal Family. Yeah I know it goes against any and every possible progressive and egalitarian ideal I hold but phish.

I grew up reading my grandmother’s Women’s Weekly and their coverage of Princess Anne’s (first) wedding and the Silver Jubilee. Over time this progressed to Diana, Fergie and their babies. And the Womens Weekly became the Hello magazine. Complete with Princess Beatrice aged two at a society wedding. So good.

And season two of The Crown has landed. Brilliant. I mean seriously- what about Philip?

Of course season one was dominated by the spectre of the abdication of a King who wanted to marry a divorced American woman. As well as the sister of the Queen who wanted to marry a divorced man.

So it was with every sense of delighted irony that I watched the recent engagement of Prince Harry to a divorced older mixed race American woman. Whose father might be catholic. ROFLMAO.

And my delight became complete when the Washington Post pointed out Meghan and Harry’s children will be subject to FATCA and US residence taxation. Oh and I have been meaning to write about the joys of US citizen taxation since like forever. So finally here was my angle.

The British Royal family – the gift that keeps on giving.

First key thing is that all people born in the United States or born to at least one US parent – like Harry’s children will be – are US citizens. And at this point such people who don’t live in America can get a little over excited. I can work in America woohoo. No green card or resident alien stuff for me! Transiting through LAX will be a breeze.

All true. But much like the British Royal Family – US citizenship is also the gift that keeps on giving.

Now dear readers we have covered tax residence of individuals before. The tests that determine whether a country can tax on the foreign income of its inhabitants. And most countries have some version of the being here or owning stuff rule to work out whether someone is tax resident.

But thanks to American exceptionalism they go one step further. The US applies residence taxation to its citizens even the ones who don’t live there. So with foreign income and US citizens it is now possible to have the country of the source of the income, the country of ‘main’ residence and the US in the mix. So for Harry’s kids: with that Bermuda dosh: there could be Bermuda; United Kingdom and the United States all with their hand out. Just as well Bermuda not big on taxation. Such a relief. That is if Hazza pays tax in the first place.

Now for lesser New Zealand mortals who might be born in the US or have a Meghan Markle equivalent mum or dad: the US/NZ tax treaty is kinda important. And if they have income from any other country that country’s US treaty will also be your friend.

Because in all those treaties is a nifty little clause called Relief of Double Taxation. Aka such a relief – no double taxation. So let’s look a a situation where a New Zealand tax resident with a US born mum – NZUSM – earns $100 Australian interest income. Australia will deduct 10% tax or $10. New Zealand will also tax that income and another $23 ($33-$10) tax will be paid in New Zealand.

Then – because who doesn’t love a party – so will the United States. Giving an Australian tax credit of $10 and a New Zealand tax credit of $23. Depending on the US tax rate for the NZUSM – they will have to pay more tax; pay no more tax; or get surplus credits to carry forward.

Now for something like interest or any other income source New Zealand taxes; this is just annoying. Maybe a bit more tax to pay but not the end of the world.

The full horror comes when NZUSM has types of income that the US taxes but NZ doesn’t. You know like capital gains? Taxable in the US. And the horror becomes squared when NZUSM realises that the US uses its – not NZ’s – tax rules and classifications to calculate the income. Who would have thought?

So that look through company or loss attributing qualifying company where income has been taxed in hands of shareholders – treated as company the US – maybe not so clever after all. Coz what about a LTC loss that was offset against the taxable income of NZUSM – coz it is all like the same economic owner? US – no loss offset allowed – full tax now due. In the US the LTC is discrete NZ company. Nothing to do with NZUSM.

And then of course there is FATCA. For like ever the US has a requirement that its foreign based citizens report their balances with foreign banks. Now quelle surprise – compliance wasn’t great. So the US then said they would collect the information from the foreign banks directly and if they didn’t comply they’d impose a 30% tax on fund flows from the US. Did concentrate the mind somewhat.

Now the US is using this information to enforce compliance. And the NZUSMs of the world are not best pleased. Finding out there was a dark side – albeit one pretty well known – to the whole I can work in the US thing. Unsurprisingly there is a wave of people seeking to renounce their citizenship. Alg except the tax thing goes on for ten years after such renunciation. And such renunciation can’t be done by parents for their children.

So while Harry may have finally found his bride; he has also found the US tax system. What could possibly go wrong?

Andrea

Deregos

Let’s talk about tax.

Or more particularly let’s talk about the tax rules for deregistering charities.

It has been a big intellectual week for your correspondent. Tuesday night White Man Behind a Desk. No tax. An interesting riff on immigration that Michael Reddell clearly wasn’t the tech checker for. Wednesday night Aphra Green Harkness Fellow on US criminal justice reform coz States just ran out of money. I tried to run an argument that this was the good side of low taxes. Didn’t resonate – go figure. And Wednesday morning – Roger Douglas on turning taxes into savings coz #taxesaregross.

And it was on the lovely Roger I planning to write but on Friday was the Greens on how there were bugg@r all foreign trusts reregistering. So I thought I’d write about that and the genius decision to require disclosure rather than taxation.

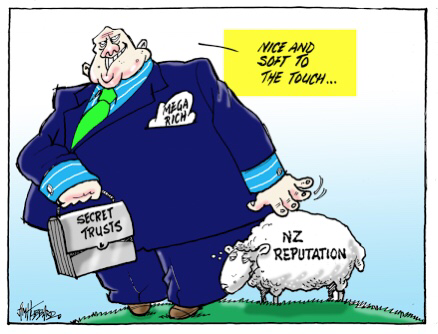

And as if that wasn’t enough. Saturday morning the latest Matt Nippert on a US and charities thing. An elderly couple with no heirs wanting to transfer wealth to a charitable institution – awh lovely. So nice they chose NZ. But also Panama, low distributions and references to the IRS. Ok. Initial reaction was it looks like FATCA avoidance coz NZ charities are outside its scope of reporting to IRS. Really must get on to my ‘US citizenship is not a good thing for tax’ post. It has been in the can for longer than this blog has been running. So embarrassed.

But one thing really caught my eye. The charities had voluntarily deregistered. Mmm interesting.

Your correspondent now moves a tiny bit in the Charities NGO sector. And from time to time I hear ‘should we stay a charity? Coz need to be careful over advocacy and ActionStation isn’t a charity and it is alg for them.’

To which I try to reply in my best talking to Ministers language: ‘ That’s one option. It would mean handing over a third of your reserves in taxes or all of your reserves to another registered charity. But totes – if that is what you want.’

Strangely the conversation doesn’t continue.

Coz the law changed in 2014 to stop the rort of charities getting lots of lovely tax subsidised donations, not distributing; deregistering and then keeping all that lovely taxpayer dosh for themselves. Go Hon Todd!

Now on the face of it this should apply to our friends here very soon. Section HR 12 applies a year after deregistration and turns the reserves – less wot go to another charity – into taxable income.

Except there doesn’t seem to be anything explicit that makes it New Zealand source income. Possibly personal property or maybe indirectly sourced from New Zealand. But the source rules are kind of old school and want to bite on real stuff not deemed income. No matter how worthy of New Zealand source taxing rights it should be.

And of course none of this matters dear readers if the entity is New Zealand resident. Coz everything gets taxed! And as the trustees are a New Zealand company – high chance it will be. So alg.

Well almost.

Coz if the dosh in the charity all came completely from non-residents – the trust rules make it a foreign trust. And foreign source income aka income wot doesn’t have a New Zealand source is not taxed. So initial view – unless the source rules can bite on this deemed income or the trust isn’t a foreign one – there will be no wash up for our friends here.

Now on one level that is cool. The final tax was all about clawing back the tax benefits given on the initial donations and the charitable tax exemption on income. Here it would have been tax exempt anyway. So alg.

The other argument is that these guys intentionally registered as a New Zealand charity. Got all the good stuff like potentially non- disclosure to IRS as well as being to say they are a legit NZ charity. But now don’t get the bad stuff.

And NZ gets the bad name but not the income. What does that sound like? Oh yes the NZ Foreign Trust rules.

So glad that – according to the Greens – is coming to an end. Shame it had to be such a resource intensive way of doing it.

Andrea