‘It’s a long way to paradise from here’

Let’s talk about tax.

Or more particularly let’s talk about non-resident trustees and the non-complying trust.

Like Ivanka Trump I had a punk phase.

Unlike Ivanka mine was actually punk and not grunge. And lasted longer than a day. Largely consisted of having orangish spiky hair from late seventh form until I had to get a real job as an accountant. And yeah ‘ real job as an accountant’ not very rock and roll. But I could do the safety pin in my ear thing – albeit through my piercing. And I just loved the music. Still do.

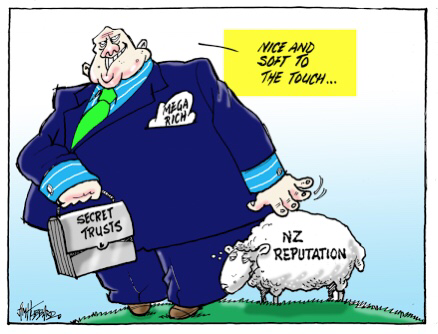

So much so that when the Paradise Papers broke – 30 years after I grew out the spikes – all I had in my head was the Stiff Little Fingers.

And the paradise reference now is not to an alternative Ulster. It is to Bermuda. A sunny place for shady people. Oh and the Queen.

So from British Virgin Islands to Panama to Bermuda. From Portcullis to Mossack Fonsceca to Appleby. The ICIJ strikes again. Well done boys. Rich people investing their money through complex structures involving sovereign Island nations.

Now of course investing in such places is only illegit if it conceals income that would otherwise be taxable somewhere else. And as for HM; she is a voluntary taxpayer – oxymoronic I know – so anything she does is totes legit. For everyone else it must be the amazing fund management service that Bermuda offers. Coz you know London is such a backwater.

But what does this all mean for New Zealand? To me this is a far bigger deal than the foreign trusts. With them our reputation was at risk. Here actual New Zealand tax could be at risk.

But first some background. Breathe and take it slowly. Rest when you need.

On the whole New Zealand – like pretty much all OECD countries taxes tax residents on New Zealand and foreign income and non-residents on New Zealand income only. And the corollary of that is not taxing the foreign income of non-residents. Which is a shame as you don’t get a bigger tax base. But mutually assured distruction if anyone tried.

So far so good. But issues abound when income is earned through companies or trusts and not directly by a real person. Maybe dear readers a good time to go back and refresh.

Now with trusts there is the person who hands over the dosh to the trust – settlor; the person wot legally owns the dosh – trustee and the person for whom this is all for – the beneficiary.

Anyone of them would be a reasonable target for the ‘who should we tax’ game of residence. Most countries target the trustee. As that is the legal owner. New Zealand targets the settlor. As they apparently call the shots. Which does seems bordeline fraudulent given they have given away legal ownership. But I digress.

All which is how foreign trusts generally have resident trustees. A foreign trust – and the associated foreign sourced income exemption – only happens if it is settled by someone who isn’t a New Zealand resident. So the foreign bit relates to the person putting the money into the trust rather than the legal owner; income source or beneficiary.

Distributions are tax free to foreigners; to New Zealanders just their normal tax rate.

The other two types of trust are:

Complying trust. Effectively full residence taxation with the wheeze that if tax is paid by the trustee; distributions can come out tax free. This is all trusts with New Zealand settlors and New Zealand trustees. Or New Zealand settlors and foreign trustees who have elected to be a complying trust.

Non-complying trust. A trust that isn’t a complying trust or a foreign trust. Effectively a trust with New Zealand settlors and foreign trustees. The potential world of the Paradise Papers.

Now distributions to New Zealand residents from a non-complying trusts are taxed at 45%. And there is often a view that so long as you don’t distribute there will be no tax consequences. Maybe. Except for:

Distributions – like dividends – have a transfer of value definition. So let’s say under a trust deed you get you to use a house rent free and that house is in a trust settled by a non-resident. Then the value of that stay is taxable at normal tax rates if it is a foreign trust. 45% if a New Zealander has given the trust any dosh as well and it is a non-complying trust. Have to assume Mojo Mathers was 100% comfortable with her tax compliance when she told her story.

Taxation of foreign income is still a thing for non-resident trustees if a New Zealander has made a settlement after December 1987. Now you might think hah – the trustee is offshore – bah hoo sux Mrs Commissioner. Well you might think that but you would be wrong. New Zealand settlors are liable – as agents – for that tax.

But surely no New Zealanders are involved?

Well that might be true. The past incarnation of this – Portcullis – picked up a Green Party donor. Now he admitted to the Trust but as he was based in the United Kingdom potentially no tax issue for New Zealand. There is also an unnamed blog that details quite interesting tax behaviour of people who look awfully like New Zealanders. And last time in 2013 IRD was pretty hot on it all.

Can we improve the situation?

Absolutely we can dear readers. Thanks for asking.

Disclosure

Now IMHO it is completely insane that there is no form of disclosure of settlements or interests in offshore trusts. Now the underlying law is pretty ok but should we have to rely on the ICIJ to get tax compliance? Taxpayers know if they have these interests but Inland Revenue would have no clue without the ICIJ.

There are disclosures of interests in foreign companies and now foreign trusts have to tell IRD about their inner workings. But offshore trusts of New Zealanders who just might be hiding things. Nowt.

Now there is the argument that if people want to be deceptive they also won’t disclose. And that is true. But all these people will have tax agents who as part of their compliance will need to ask each year if they have any. This will give them the opportunity to explain the law and the risks. And yeah they might lie to their agents too. But this is all narrowing the non-compliant group who then become super at risk next time ICIJ gets busy.

And this may even help our National Accounts. Coz you know that thing about how New Zealanders don’t save? Maybe some of this lost money is in an undisclosed offshore trust? Just maybe.

Inland Revenue Capability

This stuff is just hard. And in a world where the department is salary cutting or simply disestablishing the jobs of the people that can do this work; I am nervous. Service just won’t deal with these people. Hard nosed enforcement is needed. Please Hon Stu fix this.

Exchange agreements

Over the last ten years or so officials in OECD countries have been signing Tax Information Exchange Agreements with countries formerly known as tax havens. Wonderful PR for Ministers who look like they are actually doing something.

And when this all broke I thought cool; the Bermuda TIEA could be used. Except while it was signed in 2009. It is not yet in force. Ie we are totally on a promise until that happens.

Now Hon Stu. Your colleagues are busy sorting out the messes from the last government. Looking forward to you fixing this after you have sorted out the restructure.

Because until this is all done, without the ICIJ, offshore Trusts really can be paradise for New Zealanders who want to hide.

Andrea

#Doubletaxationisgross

Let’s talk about tax.

Or more particularly let’s talk about tax and companies.

Well dear readers what a week it has been in the Beltway. Secret recordings down south and secret payouts from Wellington. All the more bizarre as – Mike Williams confirmed – MPs staffers pretty much have sack at will contracts. If your MP doesn’t like you – that’s it you’re out. No lengthy performance management for them. Facepalm. So maybe this factoid could get added to new MPs induction?

But as always the key issue gets missed. Exactly who under 40 years old knows what a dictaphone is?

And into this maelstom Inland Revenue released a paper on taxation of individuals and some stuff on debt. Both worthy topics of discussion. But then Ryman released its results. And their CEO said like tax is paid – just not like income tax and just like not by them.

So after last week’s post I thought I’d have a look.

Oh yes the real tax is very easily found in the Income Tax Note. Tax losses of $28.9 million in the 2017 year. Up from last year when they were only $15 million of losses. They are a growth stock after all. Quite different from the tax expense which was $6m tax payable.

To your correspondent this looks awfully like her specialist subject of interest deductions for capital profits. All mixed up in a world where interest expense isn’t in the P&L but instead added to the asset value. Complying with both accounting and tax. And yeah totes a tax loophole but one from like whenever.

And again in Ryman’s accounts the rent equivalent from the time value of money of the occupancy advances is in neither the accounting nor the tax profit. Because reasons.

Now expecting controversy the CEO front footed the issue saying that the shareholders paid tax and that Ryman had actually paid GST. He then also referred to the PAYE deducted as they were employers. Kinda going to ignore that bit tho coz the whole claiming credit for other people’s tax really gets on my nerves.

And I’ll take his word on the GST angle coz I am cr@p at GST. But with his shareholders paid the tax comment – he is talking about imputation. And as I haven’t covered that before dear readers – today you get imputation. Oh and other random thoughts on tax and companies.

Now the official gig about imputation is how – notwithstanding that they are separate legal peeps – the company is merely a vehicle for their shareholders to do stuff. So for tax purposes the company structure should – sort of – get looked through to its shareholders. And this means dividends are in substance the same income as company profits and so should get a credit for tax paid by the company.

And as a tax person this stuff is considered to be in the stating the flaming obvious category.

But as I am no longer an insider – I am increasingly finding it interesting just how public policy on companies manages to talk out of both sides of its mouth. And how – much like the sack at will contracts or milliennials using dictaphones – no one has noticed.

On one hand we have the Companies Act which sets up companies with separate legal personalities from its shareholders. Meaning that if you transact with a company and it doesn’t pay you. Bad luck bucko. Nothing to do with the shareholders. Limited liability; corporate veil and all that.

But for tax if you only have a few shareholders those losses can flow through to the shareholders and be offset against against other income. The negative gearing thing but using a company. Coz in substance the company and shareholders are like the same.

And a similar thing happens with the Trust rules. Trust law says that it is trustees that own the assets. And once you have handed stuff over to them as settlor – that’s it – that stuff isn’t yours anymore. So if that settlor owes you money – also bad luck bucko. Don’t for a second think you can approach the trustees – coz whoa – settlor nothing to do with them.

But then tax says – for trusts – as settlors call the shots; it’s the residence of the settlor that is important. Mmmm. This means that a trust with a New Zealand resident trustee and a foreigner wot gave the stuff to the trustee – foreign trust – isn’t taxed on foreign income. Coz that would be like wrong. Even though the assets are owned by a New Zealand resident. And New Zealand residents normally pay tax on foreign income.

Right. Awesome. Thanks for playing.

Anyway back to imputation.

Now put any thoughts of separate legal personalities outside your pretty heads dear readers and think substance. Think companies are vehicles for shareholders. Don’t think about small shareholders having no say or liability if anything goes wrong. Just think one economic unit.

And then you will have no problem seeing potential double taxation if profit and dividends are both taxed. Coz #doubletaxationisgross.

So as part of the uber tax reforms in the late eighties imputation was brought in. Tax paid by the company can be magically turned into a tax credit called – imaginatively – an imputation credit which then travels with a dividend. Creating light and laughter in the capital markets. Or as I have put to me – increased inequality. As when imputation came in it gave dividend recipients – aka well off people – an income boost courtesy of the tax system. Probs also a tax free boost in the share price too.

Now putting aside such inconvenient facts – your correspondent has always defended imputation. Because in order to get the light and laughter or increased inequality – companies actually have to pay tax. And of that – big fan.

But all of this is only useful if shareholders are resident. Coz the credits only have value to New Zealand residents. And this is kind of why foreign companies may not care about paying tax here. And did I mention tax has to actually be paid?

And this last point that brings me back to Ryman’s chairman. He is right. If the company doesn’t pay tax – then the shareholders do when a dividend is paid. So honestly what are we all getting excited about?

Well – profits have to be like actually distributed before that happens and shareholders have to be taxpayers. And Ryman distributes less than 25% of their accounting profit.

And the residence of shareholders? Who knows. Lots of nominee companies listed which could mean KiwiSavers or non-residents. Oh and Ngai Tahu. Who seems to be a charity.

So yeah maybe. Some tax will be paid by some shareholders. That is true. Let’s hope it exceeds the tax losses Ryman is producing.

Andrea

PS. This will be the last post – except if it isn’t – for the next couple of weeks. Your correspondent is getting all her chickens back for a while. And much as I love you all dear readers – I love them more. Until Mid July. Xx

Deregos

Let’s talk about tax.

Or more particularly let’s talk about the tax rules for deregistering charities.

It has been a big intellectual week for your correspondent. Tuesday night White Man Behind a Desk. No tax. An interesting riff on immigration that Michael Reddell clearly wasn’t the tech checker for. Wednesday night Aphra Green Harkness Fellow on US criminal justice reform coz States just ran out of money. I tried to run an argument that this was the good side of low taxes. Didn’t resonate – go figure. And Wednesday morning – Roger Douglas on turning taxes into savings coz #taxesaregross.

And it was on the lovely Roger I planning to write but on Friday was the Greens on how there were bugg@r all foreign trusts reregistering. So I thought I’d write about that and the genius decision to require disclosure rather than taxation.

And as if that wasn’t enough. Saturday morning the latest Matt Nippert on a US and charities thing. An elderly couple with no heirs wanting to transfer wealth to a charitable institution – awh lovely. So nice they chose NZ. But also Panama, low distributions and references to the IRS. Ok. Initial reaction was it looks like FATCA avoidance coz NZ charities are outside its scope of reporting to IRS. Really must get on to my ‘US citizenship is not a good thing for tax’ post. It has been in the can for longer than this blog has been running. So embarrassed.

But one thing really caught my eye. The charities had voluntarily deregistered. Mmm interesting.

Your correspondent now moves a tiny bit in the Charities NGO sector. And from time to time I hear ‘should we stay a charity? Coz need to be careful over advocacy and ActionStation isn’t a charity and it is alg for them.’

To which I try to reply in my best talking to Ministers language: ‘ That’s one option. It would mean handing over a third of your reserves in taxes or all of your reserves to another registered charity. But totes – if that is what you want.’

Strangely the conversation doesn’t continue.

Coz the law changed in 2014 to stop the rort of charities getting lots of lovely tax subsidised donations, not distributing; deregistering and then keeping all that lovely taxpayer dosh for themselves. Go Hon Todd!

Now on the face of it this should apply to our friends here very soon. Section HR 12 applies a year after deregistration and turns the reserves – less wot go to another charity – into taxable income.

Except there doesn’t seem to be anything explicit that makes it New Zealand source income. Possibly personal property or maybe indirectly sourced from New Zealand. But the source rules are kind of old school and want to bite on real stuff not deemed income. No matter how worthy of New Zealand source taxing rights it should be.

And of course none of this matters dear readers if the entity is New Zealand resident. Coz everything gets taxed! And as the trustees are a New Zealand company – high chance it will be. So alg.

Well almost.

Coz if the dosh in the charity all came completely from non-residents – the trust rules make it a foreign trust. And foreign source income aka income wot doesn’t have a New Zealand source is not taxed. So initial view – unless the source rules can bite on this deemed income or the trust isn’t a foreign one – there will be no wash up for our friends here.

Now on one level that is cool. The final tax was all about clawing back the tax benefits given on the initial donations and the charitable tax exemption on income. Here it would have been tax exempt anyway. So alg.

The other argument is that these guys intentionally registered as a New Zealand charity. Got all the good stuff like potentially non- disclosure to IRS as well as being to say they are a legit NZ charity. But now don’t get the bad stuff.

And NZ gets the bad name but not the income. What does that sound like? Oh yes the NZ Foreign Trust rules.

So glad that – according to the Greens – is coming to an end. Shame it had to be such a resource intensive way of doing it.

Andrea

Switzerland of the South Pacific

Let’s talk about tax (and foreign trusts).

Your (foreign) correspondent is having a lovely holiday – thanks for asking – and is about to get on a train to visit a friend in Geneva.

Several lifetimes ago – my children and hers – and long before I discovered tax or yoga, as young women we worked for a US oil company in London as management accountants. As well as being pleased to see her I am always interested to see how she is doing in a parallel lives kind of way. She stayed and career tracked and I – well – didn’t. In a substantive sense though our lives are very similar other than maybe her husband had to give up work and my french is better.

Before the Panama Papers our prime minister – bless him – gave an interview where he had a vision for New Zealand as the Switzerland of the South Pacific. Interesting desire as it is a country where women only got the vote in 1971 and one in which a senior employee of a major US company cannot afford to live comfortably. It is french speaking though so maybe it could grow on me as an idea. But then maybe he was just thinking rich with awesome mountains and great chocolate rather than exclusive and secretive. Somehow I doubt it.

And pre Panama Papers foreign trusts fitted a little too well into that vision. Professional advisors charging fees to help rich foreigners hide their money from others. Or maybe not.

In ‘Thank you for Smoking‘ a favourite line of mine is that:

[cigarettes] are cool, available and addictive. The job’s almost done for us!.

And with foreign trusts there was no tax, little disclosure and no requirement for the money to actually ever come to New Zealand – the job was almost done for them! But after 25 years our valiant foreign trust industry with extensive marketing had only managed to earn $24 million a year with $3 million in tax.

In all the arguments about whether New Zealand was a tax haven or not, one argument got missed by the opposing side. Tax havens charge fees or levies or require the dosh to be parked in the country concerned. None of which applied here. So as a country we got the bad name but not the income – genius.

Now we have the Shewan report and John had recommended increased disclosure as had other commentators and the Greens. And I agree this should staunch any reputational damage. The difficulty I have with this though as this simply replaces one cost – our reputational damage – with another cost – additional Inland Revenue administration and distraction from their real job of ensuring compliance with our tax system.

All for $3 million in tax which may well reduce once increased disclosure is in place. At least Hon Mike please reconsider Mr S’s rec for registration fees. $50 upfront and $270 per year – really? I had no idea the department could do its job so cheaply.

Personally I prefer taxation as these are ultimately entity hybrids creating double non-taxation in the same way as the limited partnership or the unlimited liability company – both of which are registered. And it appears from paragraph 7.29 Hons Bill and Mike are open to it. Whether it survives consultation is another thing entirely.

Coz Hon Mike you are right to be considering it and I’m right behind you. If we really aren’t a tax haven then isn’t it fair that the NZ foreign trust is treated the same way as all other entity hybrids? Isn’t consistency a hall mark of a good tax system? And aren’t the foreign trusts in New Zealand for a bunch of legitimate reasons that have nothing to do with tax?

So – On y va!

Namaste

Taking the Michael

Let’s talk about tax.

Or more particularly let’s talk about the current Minister of Revenue Hon Michael Woodhouse.

There were lots of cool things I got to do when I was at the Treasury. My particular fave though was getting to coordinate the legislation that went through on Budget Night under urgency. I probs didn’t have to be there the whole time but through a combination of excessive diligence and deep love of the atmosphere in the House I was.

Urgency can go to 10pm on a Thursday and midnight on a Friday. So you can imagine it can get pretty surreal at times. And pretty much the only people who are there the whole time are the respective chief whips – or is that chieves whip – and an overly conscientious Treasury legislation coordinator. Although the formers and the latter NEVER interact.

It was in my first year of doing this gig that I noticed the Government Chief Whip Michael Woodhouse. There was just something about him that I liked. Whether it was the way he said: New Zealand National Party – twelve thousand million, Maori Party three, Act 1, United Future 1; or the way he seemed to be part of the National Party team while also not being part of some of the rougher baracking; I couldn’t say. Regardless the man impressed me.

Fast forward to him joining the Cabinet and becoming Hon Mike. He was Minister in charge of the changes to workplace safety. Now your correspondent with her left leaning tendencies was not best pleased with the final outcome but in her view Hon Mike took one for the team. Let me explain.

The original Bill was one that was widely consulted on and had agreeement of Business and the CTU. That would not have happened without Hon Mike’s ministerial sanction and support. Cabinet as well but a Minister has to take a paper to Cabinet and that would have been MW or a predecessor.

As an aside this would have been a great piece of work to have been an official on – at the beginning anyway. A chance to make the world a better place and a form of redeemption after Pike River. Although I understand that the Forestry death toll was also uppermost in the heads of those involved in this work. Regardless at times like this there is nothing better than being a Public Servant.

As a further aside I really do hope there were some juniors on this work. As watching how this piece of work turned from a ‘hands across the water’ bipartisan love fest into a partisan bureaucrat’s nightmare would seriously season a junior official and be the stuff of a Treasury senior analyst interview. Either that or send them screaming into the waiting arms of the private sector. And as I tell my children, and anyone who will listen, good experiences are not always pleasant ones.

But back to the topic and enter backbench revolt stage left. Hon Mike and his officials were then scrambling to make the best of a bad job. And it wasn’t pretty – worm and lavender farmers but not dairy farmers – geez. Big ups to Sue Moroney for spotting that – shows an attention to detail that politicans are often not big on. But here’s the thing – in all the resulting fallout all of it landed on Mr Woodhouse. Not the PM, not the Cabinet, not the National Party – all on Hon Mike. I was so impressed.

For his sterling work on this he was then ‘rewarded’ with the Revenue portfolio. Since Michael Cullen handed it on, it has been a pretty junior Ministerial position – often outside Cabinet. This continues to surprise me as it can be one of the harder gigs. For everyone else, they have to make decisions on giving stuff to people or not giving stuff to people. The MoR has to make decisions on taking people’s stuff off them in the first place. And none of them go quietly.

So how is the boy going?

- Took some of the crap on foreign trusts. Tick. Didn’t manage to shield the PM this time – but geez there are limits to anyone’s powers on that one.

- Commissioned and got the Shewan report through Cabinet. Tick.

- Got the changes to the non-resident withholding rules which make foreign capital pay tax on interest income in a way they haven’t done in decades – through Cabinet and into a bill. Tick.

- Plans to extend the scope of withholding taxes generally. Tick.

- When proposed to give away money – it was at least intelligent. Tick.

- Plans to do other base maintenance – On verra.

Now some could argue this stuff should have happened years ago. And maybe it could but Hon Mike wasn’t in charge then. So for an interim ranking I’ll give him the same ranking I always got at the Treasury as a Principal Advisor -‘meets expectations’. Because like the Treasury my expectations are always very high.

For the final review and ranking we will have the benefit of the 2017 tax expenditure statement which will show just how good a gatekeeper he is. More that statement on Friday.

Namaste