Deregos

Let’s talk about tax.

Or more particularly let’s talk about the tax rules for deregistering charities.

It has been a big intellectual week for your correspondent. Tuesday night White Man Behind a Desk. No tax. An interesting riff on immigration that Michael Reddell clearly wasn’t the tech checker for. Wednesday night Aphra Green Harkness Fellow on US criminal justice reform coz States just ran out of money. I tried to run an argument that this was the good side of low taxes. Didn’t resonate – go figure. And Wednesday morning – Roger Douglas on turning taxes into savings coz #taxesaregross.

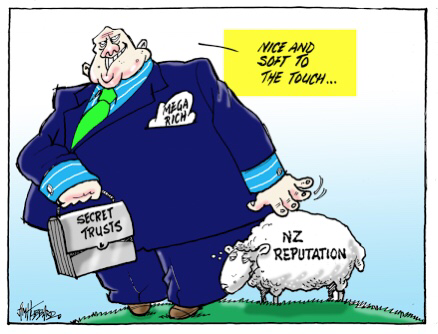

And it was on the lovely Roger I planning to write but on Friday was the Greens on how there were bugg@r all foreign trusts reregistering. So I thought I’d write about that and the genius decision to require disclosure rather than taxation.

And as if that wasn’t enough. Saturday morning the latest Matt Nippert on a US and charities thing. An elderly couple with no heirs wanting to transfer wealth to a charitable institution – awh lovely. So nice they chose NZ. But also Panama, low distributions and references to the IRS. Ok. Initial reaction was it looks like FATCA avoidance coz NZ charities are outside its scope of reporting to IRS. Really must get on to my ‘US citizenship is not a good thing for tax’ post. It has been in the can for longer than this blog has been running. So embarrassed.

But one thing really caught my eye. The charities had voluntarily deregistered. Mmm interesting.

Your correspondent now moves a tiny bit in the Charities NGO sector. And from time to time I hear ‘should we stay a charity? Coz need to be careful over advocacy and ActionStation isn’t a charity and it is alg for them.’

To which I try to reply in my best talking to Ministers language: ‘ That’s one option. It would mean handing over a third of your reserves in taxes or all of your reserves to another registered charity. But totes – if that is what you want.’

Strangely the conversation doesn’t continue.

Coz the law changed in 2014 to stop the rort of charities getting lots of lovely tax subsidised donations, not distributing; deregistering and then keeping all that lovely taxpayer dosh for themselves. Go Hon Todd!

Now on the face of it this should apply to our friends here very soon. Section HR 12 applies a year after deregistration and turns the reserves – less wot go to another charity – into taxable income.

Except there doesn’t seem to be anything explicit that makes it New Zealand source income. Possibly personal property or maybe indirectly sourced from New Zealand. But the source rules are kind of old school and want to bite on real stuff not deemed income. No matter how worthy of New Zealand source taxing rights it should be.

And of course none of this matters dear readers if the entity is New Zealand resident. Coz everything gets taxed! And as the trustees are a New Zealand company – high chance it will be. So alg.

Well almost.

Coz if the dosh in the charity all came completely from non-residents – the trust rules make it a foreign trust. And foreign source income aka income wot doesn’t have a New Zealand source is not taxed. So initial view – unless the source rules can bite on this deemed income or the trust isn’t a foreign one – there will be no wash up for our friends here.

Now on one level that is cool. The final tax was all about clawing back the tax benefits given on the initial donations and the charitable tax exemption on income. Here it would have been tax exempt anyway. So alg.

The other argument is that these guys intentionally registered as a New Zealand charity. Got all the good stuff like potentially non- disclosure to IRS as well as being to say they are a legit NZ charity. But now don’t get the bad stuff.

And NZ gets the bad name but not the income. What does that sound like? Oh yes the NZ Foreign Trust rules.

So glad that – according to the Greens – is coming to an end. Shame it had to be such a resource intensive way of doing it.

Andrea

Everything is connected to everything else

Let’s talk about tax.

Or more particularly let’s talk about about a case I mentioned last week in the alignment post. It was quite controversial at the time within the tax community and did leak out a bit into the general public. As is often the ‘case’ tax is just an overlay on other interesting stuff.

Also thought of it again wot with the junior doctors strike and how the consultants would be helping over that period. I guess coz its Health that means its not strike breaking?

Anyway back to the case. Penny and Hooper (last names) were both specialist doctors earning shed loads of cash in Christchurch fixing the bung knees of those who were in denial about the length of their running careers and had yet to find yoga.

Now these gentlemen were unremarkable in that they weren’t big on paying tax according to the progressive tax scales that applied to little people and so adopted a structure recommended by their accountant. I mean everyone was doing it and what could possibly go wrong. In fact even John Shewan – of Shewan report fame – said it was bog standard behaviour.

The wheeze was that they put their businesses into a trust which at that time had a lower tax rate (33%) than the little people faced who earned over $60,000 ( threshold increased at some point but detail not relevant) 39%.

The Commissioner who was a he at the time – yes Virginia men can be senior public servants – was not best pleased. He used a bunch of words like ‘tax avoidance’,’market salary’ and ‘not’and made them pay tax like the little people. Go Team Commissioner.

The tax community also used a bunch of words like ’emmently foreseeable’; ‘lack of certainty’; and ‘chilling effect on investment’. Well maybe not the last set but that is never far away when the big people are being made to pay tax.

Anyway the Commissioner won; tax accountants lost; largely graciously ate that and everyone moved on to the next tax dept v tax community stousch.

There was some commentary at the time about how this was more than a tax case – at which point I got very excited – only to find it was about trusts could be looked through and weren’t as inviolable as people thought.

But what was never discussed was how two men who were educated at the state’s expense presumably before student loans; weren’t bonded; and whose business was almost wholly paid for by the taxpayer via ACC were earning so much money. I guess it was before the days of ‘joined up government’.

I also guess Labour’s ‘three years free’ policy will also remove what little royalty we currently get from the taxpayers’ investment in such lovely people.

All the more reason then guys to make sure misalignment works and they do actually pay the top tax rate.

Namaste

‘You’re not one of those people are you?’

Let’s talk about tax (and tax rate alignment).

Your (foreign) correspondent is finishing up her ‘retirement cruise’ and gearing up to make that execrable journey home – also known as long distance economy class travel.

The yoga is going well too – thanks for asking – even without regular access to a studio. In large part to now knowing how alignment needs to work with my skeleton rather than that of a textbook Indian man.

So I have been thinking about this, how foreign tax systems are pretty much all misaligned, and that I promised to talk about the tail chasing stuff needed to make a higher top marginal tax rate work – or at least not not work. Because like misaligned bodies in yoga; misaligned tax systems also need props to work.

So today dear readers you get top personal tax rate alignment issues.

A couple of years ago while I was still a Treasury official I was at a social engagement and found myself talking to a Greens’ supporter. We were talking about the Christchurch earthquake and the rebuild and stuff – yes I do have all the fun – and the convo went something like this:

GS: You may remember that Russel proposed an earthquake levy as a means for the whole of the country to support Christchurch.

Me: yeah I remember that and on the face of it it did have merit – the problem is that whenever you increase the gap between the personal rates and the trust and company rate – you get people moving income into different forms. You may not collect all you think you will.

GS: [eye roll] you’re not one of those people are you? Other countries cope.

Well yeah I am ‘one of those people’. I really do like alignment and again not from a ‘purity of the tax system’ thing but because – like keeping R&D tax incentives out of the tax system – it serves us. It serves us because no matter how clever people want to get with their structuring – you always get the same result.

HOWEVER

Alignment – like a capital gains tax is not a silver bullet and – doesn’t mean:

- everyone magically starts earning income in their own names or

- income that isn’t taxed magically starts becoming taxed

It just means that there is no incentive to start finding a bunch of non-tax commercial reasons that coincidently mean current taxable income is now earned in different lower taxed forms.

But next lefty government if you do want to raise the top rate for individuals – you are going to need some tax props to stop or reduce the tax injuries. That is how othe countries cope. Have a look at page 36 of IRD’s 2005 BIM.

First thing that is beyond key is the trust or trustee tax rate. This must be raised too as income taxed at the trustee rate can be then given to beneficiaries without any more tax to pay. Australia has. All the Penny and Hooper drama happened because the trustee rate wasn’t raised too.

However there are potentially some collateral damage issues from this – aka political risk:

- Will estates

- Trusts for the ‘handicapped child’ or the disabled relative

Australia deals with these respectively by taxing at the progressive tax scale and giving the Commissioner a discretion to alter the rate. In the last – and possibly both – cases face palm. Given our tax administration’s aging computer and business transformation programme – a better option would be treating them like widely held superannuation funds and giving them the company tax rate.

You could also do something like giving them a non-refundable tax credit to get the rate back down to 33%. That technology was used in cashing out R&D losses. But this is all second order design detail and nothing officials and/or your working group can’t sort out. No biggie. It might be a bit messy but nothing compared to the carnage involved with not aligning the trust rate.

Next issue is companies and that is a bit harder. I am assuming raising the company tax rate is off the agenda – yeah thought so.

Misalignment with the company rate – as we do now – is marginally less risky as distributions from companies – dividends – are taxed in the hands of the shareholders. And they use my personal favourite technology – the withholding tax. There is currently an additional withholding tax on dividends when they are paid bringing total tax up to 33%.

You could keep the additional withholding tax at 5% and make people file who need to pay more tax – as there was no withholding at all last time there was a 33% company rate and a 39% top rate. But there also wasn’t alignment with trusts and that went well.

Or you could raise the withholding tax to – say – 11c and people who need refunds would then need to file. Or possibly a progressive withholding system from say 5c to 11c. All technically possible. But all options will raise compliance costs on taxpayers and/or administration costs on IRD. And remember the aging computer thing?

The real issue is whether our dividend rules last properly looked at almost 25 years ago can stand the strain of say a 11c difference between the company rate and top personal rate. There are ultimately limits to how long people can pay themselves $70k salaries but have a $200k lifestyle. You need to make sure you get that extra 11c when they decide to sort out that gap.

Alternatively you may like to consider making the look through company rules compulsory for all closely held companies. This would mean the company wasn’t taxed and all the income went to shareholders personally.

Neither issue will need to be part of the first 100 days tax changing under urgency that is de rigeur for new governments. It can be sorted out with consulation and will be better for it. But you will need to be prepared to use these tax props if you don’t want the 2000 – 2009 mess again.

Think that’s it.

Hardest thing will be reprioritising the existing BT and BEPS work programme to get space for this and your new fairness working group stuff.

Namaste