The Spike

Let’s talk about (the recent Greens’ press statement on) tax.

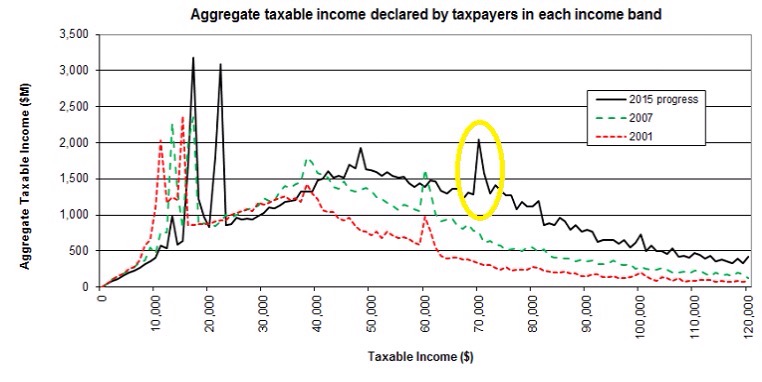

Recent data has shown there is a spike around $70,000 of reported taxable income for individuals – convienently the point where the top marginal tax rate of 33% starts. And according to the Greens this shows evidence of tax avoidance by rich people which can be fixed by – among other things – increasing Inland Revenue’s investigation budget. Mmm maybe.

Before I go on, I am working on the assumption that when the Greens talk about tax avoidance it is in the colloquial ‘not paying as much tax as I think you should’ kinda way rather than tax avoidance according to the actual law. All cool but unfortunately (or fortunately) the department is constrained by what Parliament has enacted and how the Courts have interpreted it.

Now in the mid 2000s – it is true – similar spikes were evidence of widespread tax avoidance among self-employed professionals. The wheeze was that they were employed by trusts which were taxed at 33% on the income the individuals earned – not the top individual’s rate of 39%. And then the trust paid the individuals a below market salary for their services to the trust.

Only the below market salary was taxed at 39% and the rest of the income at the lower trust rate. And then any tax paid income of the trust could then be distributed tax free to beneficiaries. Too easy and too good to be true. Hence tax avoidance according to the actual law.

Moving to 2017. The trust and top personal rate are the same so that particular wheeze won’t work. But now we just have misalignment between the company rate at 28% and the top personal rate of 33%.

Except that under a misalignment with the company rate there is no distributing the income tax free. When income is distributed from the company to the shareholder – a dividend – it is subject to another 5% tax. Now any ‘tax avoidance’ – in theory anyway – is just timing until the shareholder needs the money. There should be no ultimate reduction in tax. Although timing advantages can be a big deal and can also make something tax avoidance under the actual law.

But the only way I can see of moving this from tax avoidance – not paying as much tax as I think you should – to tax avoidance under the actual law is if the department can show that the $70k is not a market salary – as they did with the self employed professionals.

And while that wasn’t simple for the department last time – now all tax advisors know about the need for a market salary – possibly from painful personal experience. So anyone giving advice that $70k is an acceptable salary – when the market rate is higher – does so knowing it could be attacked by the department and will have all the supporting arguments ready.

But the Greens are right the spike is still there. Last time the spike was widespread tax avoidance according to the actual law – so why wouldn’t it be this time too? Not the first time I have lacked imagination.

Just in case tho I am right – I am also all about the solutions. And there is at least one way of getting rid of the spike without increasing anyone’s budget. Think of all that extra money Greens you could spend on cleaning up the rivers instead of tax inspectors.

One way is to increase the company tax rate to the top marginal rate.

Another way is to make the look-through company (LTC) rules compulsory.

Currently any company with five or fewer shareholders can choose not to be taxed as a company. Instead income and losses are taxed as if the shareholders had earned the money themselves. Except currently those rules are optional. Make them compulsory and the spike goes. No more income in more lowly taxed closely held companies as no more closely held companies for tax purposes. Simple.

And the really good news for the Greens is that there is currently a bill in the House making changes to the LTC rules; so a Supplementary Order Paper doing just that would be totes in scope. Oh and it is an ‘annual rates’ bill too so they could also have a go at the company tax rate at the same time. Awesome.

Now lots of people who haven’t made an LTC election may not like that and say so quite loudly. Coz that’s what you get when you are strong on policing tax avoidance – lots of upset people all with lots of incentive to write to you and come and tell you how upset they are.

But unless the current law with closely held companies – or company tax rate – changes I can’t see any level of increased funding will get rid of that nasty spike.

Namaste.

Let’s rendez-vous in the Pacific

Let’s talk about tax (and interest deductions for capital gains).

While your correspondent is a confirmed Anglican – Episcopalian actually – I don’t consider myself a Christian anymore and haven’t taken communion for over twenty years. The same cannot be said for the rest of my extended family which is pretty hard core christian and includes three ordained priests. It used to be overrun with lawyers so priests is definitely pareto improvement.

From time to time at family gatherings when my darling christian family is discussing something theological – yes it is fun but I love them a lot – one of them will say ‘but of course it all went wrong at the Council of Nicaea’. That I think was when the Christian Church became a proper institution and started telling its followers what to do. And having seen public institutions operate at times for themselves rather than the people they are serving I am sympathetic to that view.

But for tax – in New Zealand – its Council of Nicaea was the 1986 Pacific Rendezvous case.

Pacific Rendezvous was – and is – a motel. They wanted to sell the business but to get a better price they decided they needed to do some capital works. They borrowed money to do that and claimed most of the interest as a tax deduction.

They were pretty open that the building works were because they wanted to get a better price for the sale of their business. And of course we all know dear readers that the proceeds from a sale of a business that was not started with the intention of sale is tax free.

Unsurprisingly the Commissioner – who was a he at the time – was not best pleased. Deductions to earn untaxed income you cannot be serious. And so he took Pacific Rendezvous to court to overturn the deductions associated with the tax free capital bit.

But the Courts were like ‘nah totes fine’. Coz – get this – the interest was also connected with earning taxable income. You know the like really small motel fees even tho the whole gig was an ‘enhancing the business ahead of sale’ thing.

Impressive.

And that dear readers is why I am so not a lawyer. Having to hold such stuff in my head as legit would totally make it explode.

But I digress.

Now of course Parliament or the government at the time still had the chance to overturn that case coz of course Parliament, not the courts, has the final say. Or it could have simply taxed the capital returns – sorry now I am just being silly.

What actually happened was some 13 years later after a fruitless interpretative tour of the provisions Bill English – when he was just a little baby MoF and long before his two stints at the leader thing – proposed and Michael Cullen enacted – that companies could have as many interest deductions as they wanted because compliance costs. You know coz otherwise ‘they’ll just use trusts’.

It was subject to the thin capitalisation rules and as the banks were to discover to their chagrin – the anti avoidance rules – but deductions to earn capital profits game on.

Now the capital profits thing was considered at the time – chapter 4 – and quite a compelling economic case was made for some form of interest restriction. But by Chapter 6 there became insurrountable practical issues that made this not possible. Those issues included:

- The need for rules to ensure that the deduction was not separated from the capital income;

- Difficulties with bringing in unrealised gains;

- If done on realisation – potential issues with retropective adjustments along period capital gain was earned;

- Need to factor in capital losses.

And it was true that in the past Muldoon – well then must be wrong – had attempted to do something by clawing back interest deductions to the extent a capital gain was made. Imaginatively it was called ‘clawback’ and everyone hated it. And yes people did use trusts and holding companies to avoid it. Oh and soz can’t find a decent link to reference this so you will just have to trust me on this.

But you know what? Tax policy is so much cleverer now and we group companies and treat them as one entity for losses and lots of other stuff all which could get around these issues. In fact the recent National governments in a bipartisan and a thinking only of the tax system way have enacted rules that mean interest restrictions for capital gains are no longer the insurrountable issue they apparently were in 1999. Who says John Key doesn’t have a legacy?

So working up the list.

- Can’t see the issue with capital losses as if that capital was lost in a closely held setting on deductible expenses it is already fully deductible. Outside that any interest limitation for capital gains would only apply to the extent there was untaxed capital income. And as we are talking about losses – not income – no interest restrictions. Simple.

- Would only do it on realisation. Taxing unrealised stuff while technically correct is a compliance nightmare. But the new R&D rules which claw back cashed out losses when a capital gain is made – from page 24 – could totes be made to work here. Interest deductions could be allowed on a current year basis but if a capital profit is made – they are clawed back in the year of sale. If deferral was still a big deal – a use of money charge could be added in too. Personally I would give up the interest charge. Simpler and an acknowledgement of the earning of taxed income.

- And the whole deduction being separated from income was fixed with the debt stacking rules for mixed use assets. So let’s use that.

Coz the thing is while no one seems to be bringing in a capital gains tax anymore it is still massively anomalous that deductions are allowed for earning untaxed income just coz some incidental income was earned as well.

Now Labour is planning to have a bit of a go in this area by going after negative gearing through ringfencing losses. Better than nothing I guess. But still kinda partial as only touches people with not enough rental income to offset the deductions. And Grant, Phil and the new Michael – even for this – you totes will need the debt stacking rules or else ‘they’ll just use trusts’ or holding companies.

And yeah extending the brightline test to 5 years. Again better than nothing but there is still lots of scope to play the whole deductions for untaxed gains for property holdings over 5 years or – as with Pacific Rendezvous themselves – businesses.

But for any other political party with an allergy to a capital gains tax but big on the whole tax fairness thing perhaps you might want to look again at interest clawback on sale? This time thanks to the foresight and the public spirited nature of the John Key led governments – it would actually work.

Namaste

Timothy W Edgar (1960 – 2016)

2016 has been some year.

Donald Trump; Brexit and then the deaths of Leonard Cohen; David Bowie; Prince; George Martin; Helen Kelly; Zsa Zsa Gabor, George Michael as well as the heart attack of Carrie Fisher. But one friend has had a baby and two have got engaged – although not to each other – so not a complete write off.

One death though – that has recently made the international tax community poorer – was that of Tim Edgar a Canadian tax academic.

Tim originally trained as a lawyer – and taught at law schools – but a less lawyery person you could not meet. Cases drove him mental. Once in conversation he suggested that instead of the Courts we should just use a random number generator for tax avoidance. Although to be fair it would also work for any of the objective subjective cases like capital/revenue or residence.

Odd numbers for the Commissioner – even for the taxpayer. Very fair. And would – he argued – have the effect that taxpayers would just stay away from anything that would get them put in the generator in the first place. Good policy outcomes with reduced fiscal cost. What’s not to love?

Tim came to Wellington with his family on sabbatical in early 2000s and worked in Inland Revenue policy. I can’t remember what he was supposed to be working on – GST possibly – but because of his ability and good humour very quickly became a sounding board and contributor to pretty much every team in the division. He also lived close to me and our families had a lot to do with each other over that time. We introduced the Edgar family to the joys of Fish and Chips.

After that period in Wellington, we kept in touch and our paths crossed a number of times including a joint stint presenting an OECD course in India. Again his depth of knowledge and good humour made him very popular with the participants while his North American tipping practices made him popular with the staff at the hotel.

By the mid 2000s I had become completely obsessed by hybrids in the way my children were with pokemon. So I wanted to analyse them and their effects for my masters dissertation. There was a small difficulty in that there was no one in New Zealand with the expertise who could supervise me. So I approached Tim.

With his usual good humour and generosity – although possibly it was the opportunity to earn $100 in NZ foreign exchange that clinched it – he agreed. And within 2 weeks I had a parcel of the key items of the hybrids literature in my mailbox. Not sure that is standard operating practice for most supervisors. But then Tim wasn’t most people.

At the time (2004- 2006) there were two views on hybrids. The first – dude get over it countries can do what they like aka the sovereignty argument and the second – it is double non -taxation/ bad aka the economic distortion argument. I wasn’t fully convinced by either view. Tim, however, was very firmly in the latter camp and – quelle surprise – history has proved him right.

Tim was a high level strategic person – but in the sense that he did actually have big picture insights – rather than just someone who can’t cope with complexity or detail. He was expert in Financial Arrangements; GST; international tax; tax structuring or pretty much anything he decided to have a look at.

I particularly remember him sharing his views on formulary apportionment which is touted by parts of the left as the ‘fair’ way to allocate worldwide tax revenues. The thing is – he said – there is nothing normative about allocating through source and residence. What that has going for it though – is that all the countries agree. Formulary apportionment throws all that up in the air – and who knows where you’ll end up?’

We last caught up around his fiftieth birthday – which I am embarrassed to see is almost 5 years ago. He shared with me the changes in his personal and professional life and how proud he was with how his children were doing. He was more subdued than previously but was looking forward to the next stage of his life.

I don’t think this and similar articles was what he had in mind though – particularly as he was always so fit. I struggled to find a photo that represented how I remember him. Even this one which I swiped from his uni’s obituary doesn’t show the exuberant enthusiasm he had for discussing any one of the topics around his head.

I had him on my list of people to contact now I have left the reservation but sadly this post will have to do instead. I will however always remember the laughter, the low ego/high ability combo and the non-standard approach to thinking about tax.

So go well my dear friend. Hail and farewell.

Andrea

The Christmas Post

Let’s (not) talk about tax.

Let’s talk about a couple of Christmas related things.

Christmas thing one – Holy Innocents Day.

Many many years ago when I was a late teenager and a Christian I went to church with my father on the Sunday after Christmas. Taking the service was one Canon John Froud. The Canon. A retired priest who took the unglamorous – 8am – or the respite services after the major festivals for the main priest.

The Canon also looked after the Servers of which I was one. Main advice for us was – particularly if something went wrong – ‘whatever you do – do it slowly’. Could be a yoga motto. He loved us young people in a fairly direct unsentimental way – all completely appropriately so sad I have to say this – and had time for us in the way the main priest who had a parish to run couldn’t possibly.

He did however like things done properly and the crewcut may have reflected a military background at one time. I still have a memory of turning up for serving duty at the 8am service – what I thought was on time and correctly presented. No idea what time I had got to bed tho. But before entering the church I was told ‘Open your eyes Andrea – they are at half mast.’ I duly opened my eyes.

Now on the Sunday after Christmas, the Canon as he was leading the service gave the sermon. And the topic he chose was Holy Innocents Day. As apparently that is the Sunday after Xmas in the Anglican calendar. What he said has stuck with me to today. And I can’t think of many other things that have had a similar impact.

Holy Innocents Day is to honour all the baby boys that were slaughtered on the orders of Herod when he heard of the birth of the King of the Jews. Now in the mid eighties there was no Wikipedia link to challenge the veracity of the Canon’s sermon. But to me it seems quite likely given what a nasty bugger Herod was – better to be his pig than his son – and would explain the whole going to Egypt thing.

At this point I could start to reference ‘trade-offs’; or make yin/yang or omelette analogies. But I won’t. All I wish to do is note that even with a festival as joyous as Christmas – there is another side that should be remembered. As that was what the Canon wanted us to do.

Christmas thing two – Pavlova

Changing the subject completely. Because dear readers you have all been so fabulous – I am going to give you my pavlova recipe. I make an absolutely state of the art top draw pavlova. And you can now too.

Background

This recipe comes from my grandmother and the proportions are one egg white to 2 ounces of caster sugar. Yes ounces soz. I have a jug that measures sugar in ounces. I don’t think it is too critical though as I have used less than that in the past and it all worked fine. I have also used this recipe for 4 egg whites and 16 and the proportions still work. I use – broadly – one egg white to one person. But then I have been feeding teenage boys up until now.

Also – key message- it needs to be made the night before.

Recipe

- Turn oven to 200 degrees Celsius. Line a tray – or even roasting dish if a big pav – with cooking paper.

- Get out cornflour and a vinegar like white or red wine. Not balsamic vinegar. Put on bench.

- Get a large bowl and make sure it is scrupulously clean and dry.

- In a measuring jug or equivalent measure out the caster sugar you need in the one egg white to two ounces proportion. Leave in jug/container until needed.

- Separate egg white from egg yolks. Use actual eggs. Tried egg whites in a packet once and could not get the proportions right. Make sure there are absolutely no specks of yoke in the white. If you crack an egg and the yolk breaks – put it all with the yolks. Much like the dry bowl. Any speck of yolk and the pavlova won’t work.

- Beat egg whites until they are so stiff that you could upend bowl and nothing would come out. Up to you if you actually want to try it.

- Beat in caster sugar.

- Add a slurp of vinegar and a teaspoon or so of cornflour. Beat again.

- Take pavlova mixture and mound as high as possible on tray.

- Put into oven at 200 degrees. Immediately turn it down to 125 degrees and cook for an hour. Possibly a bit longer for very large pavlovas.

- After an hour turn off the oven but leave the pavlova inside. Leave everything exactly as it is overnight until the pavlova and the oven are completely cold. This technique should give you a pavlova with a crunchy outside and a marshmallow inside.

- Cream and fruit immediately before eating. Not before. Otherwise the crunchy bits will go soggy.

- You’re welcome.

But otherwise dear readers – Merry Christmas and Happy New (election) Year to you and yours. Back sometime mid January.

Namaste.

Imputed what?

Let’s talk about tax (and imputed rents).

In one part of the now infamous interview between Gareth Morgan and Paul Henry; when Gareth is trying to explain to Paul that Paul owning a big house or a flash car did have value to Paul – Gareth is talking about imputed rents.

Michael Cullen’s tax review in 2001 – the one that had Shirley Jones as a member that wasn’t the mother of David Cassidy – produced an interim issues paper. In that paper from page 37 there is a proposal to tax imputed rents. I will define it in a minute promise – currently just doing the preamble flow. The media and news – coz in those days people didn’t get their news anywhere else – went absolutely nuts. There was a line doing the rounds that the Beehive’s switchboard was jammed following the release of the issues paper – and that was just from the 9th Floor (HC) to the 7th (MC).

I don’t think Helen Clark’s government could distance themselves from it fast enough.

So what is an imputed rent? Told you I would get there in the end. The way I like to think of it is the rent you save to the extent you own your own place. That value is then income to you as is the case with the dividend rules where a shareholder lives rent free in a house owned by the company.

Strictly speaking the ‘correct technical’ analysis has you both paying non- deductible rent and receiving taxable rent. In the same way renters pay non-deductible rent to landlords for whom it is taxable income. In this analysis you are both renter and landlord.

Yep I prefer my way too.

So it is a benefit or a tax break that owner occupiers get that renters don’t get. And it has been there for like EVAH so no one really realises. Except in their heart they do. Imputed rents is the basis of the received wisdom that you should always pay off your mortage ahead of making other (taxable) investments.

Now the thing is that strictly speaking under the ‘correct technical’ analysis if you start taxing the income you need to also allow deductions. But I am not sure if our friend the private and domestic exclusion for deductions would let it thru.

This isn’t a problem for TOP as their tax will be based on productive capital as measured in the capital account of the National Income Accounts. Ok good. There is though the small matter that nothing else in the tax system is actually based on this concept . So maybe – just maybe – there could be some tax design issues.

Now being the solutions focussed individual that I am – I thought I’d put together another way of taxing imputed rents. Yes I know there is more to the TOP tax policy than this – but there are limits to my powers. I also can’t do a blind thing about political acceptability either – so I am sticking with what I know.

How to tax imputed rents in four easy steps.

Step one. Divide the value of your mortgage by the value of your property. Council valuations will be fine.

Step two. Go to the MBIE website and look up your area, number of bedrooms and find the potential rent for your property. There are three bands. Take the median one. Why? Made it up. No one can be trusted not to self assess the lower band and I can’t cope with the arguing.

Step three. Take the rent in step two and multiply by 52 weeks or how ever long you have lived in your property. If no mortgage put this number in your tax return in the rents box. Joint owners – yes you can divide it by number of owners. Put that number on your tax return.

Step four. Those with mortgages who are still playing. Multiply step one’s number by step three’s number. This is the amount you aren’t paying tax on. Deduct it from the full amount in step three and put it on your tax return. Yes joint owners can divide here to.

Of course it still suffers from the problem all made up or presumptive taxes do that there hasn’t been any cash come in to help pay the tax. But I would hope – to paraphrase one of my commentators – it was more intuitive and less weird to the punters than something based on a percentage of value. Even if the outcome is broadly similar.

Now of course the economists may hate it. But as economists don’t have to explain things to clients or taxpayers – give the accountants this one.

Namaste.

Nineteen to Nine

Let’s talk about tax (and Michael Woodhouse).

Any reader of these august pages would be left in no doubt I have a bit of a professional crush on the outgoing Minister of Revenue.

Now all of that may seem seriously weird given that he is a member of a centre right government and I am an out lefty – social progressive please. Except that here’s the thing. So is he.

And before you protest Hon Mike let’s look at your record. Highlights include:

- Tightening up the foreign trust rules;

- Making foreign debt capital pay tax in a way they haven’t for decades;

- Releasing a discussion document to remove the too good to be true hybrid mismatches and

- Is thinking about considering finally taxing multinationals properly.

All stuff that would be more at home in a Green Party manifesto than the Business Growth Agenda. Now until this week I would have thought him a solid performer but not exactly a political operator. And its not like that is a bad thing. Chilled out entertainers get on my nerves.

But then the Herald stuff started on Wednesday. Bylines and headlines of the government taking unilateral action and the Opposition saying it wasn’t going far enough. What? How was any of this news?

Going through all the detail – coz that is what I do – here are the facts:

- In June Hon Bill and Hon Mike announced they were doing lots of multinational stuff including reviewing the interest limitation rules which is a big ticket way of not paying tax.

- A month ago Hon Mike announced there would be a discussion document on the whole diverted profits tax thing and interest deductions in February. I never covered it coz it looked quite sane and thought I’d wait for the detail.

- The reality of a discussion document in February is that while it might make a bill before the election. There is no way it can be passed into law by the time we go to the polls. So it will be become the next government’s problem to actually make it happen.

- Wednesday the Herald gets an advance copy of a cabinet paper probs also written a month ago. It says no to an actual diverted profits tax but proposes a bunch of stuff based on the work the OECD that should broadly have the same effect but without the drama of overriding our tax treaties.

- Oh and of course tax is inherently unilateral. Some how that seems to have got missed.

- The other thing that got missed is there was no detail on any moves to counter interest deductions. That is important but hard. And according to the June statement from both the boys was coming out this year. Waiting. Waiting.

Now from these little factoids Hon Mike got four articles in the Herald and me tomorrow in The Spinoff. Wow. Breathtaking. And – it is worth repeating – all on a subject announced at least a month ago that cannot become law in this term of government. And and he got a complete free pass on what he didn’t mention – interest deductions.

Sir. I have underestimated you. A solid performer AND a player.

And now you are leaving me and picking up ACC. But the real news is the change in your ranking from 19 to 9. This week has paid off for you.

Now I am not sure if I am going to find that Hon Judith is a closet lefty. But just in case my advice is:

- Carry on with the work on withholding taxes and particularly look at how vulnerable workers are treated and their risk of tax evasion;

- Interest deductions. Coz it is actually a key plank of work of OECD and is on a permanent foreshadow; and

- Keep an eye of those intermediaries and what they are doing with taxpayer data.

But otherwise good luck. I am pleased that Revenue is going to a senior Minister and none of this ‘outside cabinet’ nonsense. Michael Wood is going to have his work cut out for him marking you.

Namaste

Gareth responds

I wouldn’t normally create an entire post for a commentator. But hey it is my blog and not everyone is dedicating themselves to overhauling our country in a socially progressive way. Also I did devote an entire post to them so only seems ‘fair’ – as much as I dislike that term – to do the same for the response.

There must be a technologically prettier way to reproduce his comments – but until number one son comes home for Xmas – this is the best I can do.

Namaste.

‘But if, baby, I’m the bottom you’re the top’

Let’s talk about tax.

Or more particularly let’s talk about the recently announced tax policy of The Oppportunities Party – TOP. They are proposing to impose a tax on a deemed or imputed return on capital to the extent tax of that level is not paid already. Kinda like a minimum tax. With proceeds going to fund income tax reductions on labour income.

TOP is a party set up by millionaire businessman and commentator Gareth Morgan to change the political discourse in New Zealand. Your correspondent is particularly fascinated as her eighteen year old self voted for a party set up by a millionaire businessman and commentator Bob Jones who set out to change the political discourse in New Zealand. I was righty then and lefty now and both parties were set up to scratch itches on the body politick.

Bob Jones got no seats but he did get 20% of the vote. Today that would be almost the Greens and New Zealand First level of representation.

Now the New Zealand Party never really got into policy much beyond Freedom and Prosperity. TOP however is much geekier and actually plans to release policy ahead of even deciding to register. And their first released policy is one on tax. And and it seeks to tax capital more heavily and lessen the tax on labour. Woohoo. Speak to me baby.

Now New Zealand’s tax system is one designed by economists, drafted by lawyers and administered by accountants – so what could possibly go wrong. Nonetheless all three groups have their own languages and blind spots. It is a marriage that mostly works but only if all three groups keep their eye on the policy development and respect each other’s strengths.

Another perspective is that of the high level ‘strategic’ people versus the detail people. Again each have their strengths but also the ability to talk past and frustrate the snot out of each other. Working at Treasury I was surrounded by the former. To the younger members of this cohort I would always consul them to stay with the process – even when it became boring. As because detail people speak last – they speak best. And what eventuates may not be what the high level strategic people with the higher number of hay points actually had in mind.

In tax a classic example is the Portfolio Investment Entities rules. If you look at the early high level papers it was all about taking away the tax barriers to diversified pooled investment in shares. What we ended up with was the ability to have cash PIEs, land PIEs and single equity investments. Giving us almost a nordic tax system with the taxation of savings. So somewhere the high level strategic people disengaged or conceded to technical design issues that gave some unintended and quite important consequences.

All of this came back to me when I read the TOP tax policy. Clearly designed by economists – and cleverly so – but sadly lacking in input of the other two tax disciplines. So as a tax accountant who is regularly mistaken for a lawyer I thought I’d step up and help them out. Here goes:

General aka random irrelevant points that say more about the reviewer than the reviewee.

One. While Gareth didn’t – I enjoyed the envy tax reference. Coz does this mean taxing labour is a pity tax, or a tax on despair or a tax on barely getting ahead? I am all in favour of taxing envy. Let’s also tax greed, sloth, lust and the rest of the hell pizzas. There’s no risk of that tax distorting those human behaviours after all.

Two. For readers who have been keeping up, a regular whinge of mine is how we effectively give deductions for loss of capital when gains are not taxed. This would be overcome through the minimum tax on wealth (or assets). So under this proposal such capital losses would effectively become valueless. Rejoice.

Three. If you are going to get a bunch of extra money – instead of reducing taxes on labour income – the tax welfare interface is IMHO a much more worthy candidate for any spare money. But maybe the universal basic income is the next cab off the rank.

Specific points that might actually be helpful

One. It is true property ownership is a feature of the rich list but so is serial entrepeneurship – Graeme Hart, Diane Foreman and someone Morgan. Now a key part of entrepeneurship is loss making in the early years. There is some attempt to address this with a potental deferral of up to three years of the tax. The question I have is this long enough? Isn’t Xero still loss making?

Now the received wisdom is that innovation is a good thing hence all the fricken R&D subsidies. With a much less benign tax system for innovation – will this mean that some of the dosh is simply recycled back to small firms via Callaghan? And so maybe not all will go to reduce taxes on labour income?

Two. Is it a tax based on wealth or assets? Both are mentioned in the proposal but they aren’t the same. Capital is used a lot in the proposal and depending on whether you are talking to an accountant or an economist can mean either assets or wealth. But here is why it matters. Assets is the total of all the stuff you have legal title to, wealth is the amount that no one else has claims on. And the difference between the two is usually debt but could also be trade creditors, intercompany advances or provisons or accruals. Not all of these generate tax deductions.

So if it is a tax on assets, is it fair to tax people on stuff that other have claims on? I doubt it. A bit of language tightening here would be cool.

Three. Valuation. For property and things like shares market valuations are not too hard. Businesses – however – wow. There will be what the financial accounts say but then there will be what someone is prepared to pay. Usually some multiple of Earnings Before Interest and Tax – EBIT. And what about valuing implicit parental guarantees from non- residents. The choice then is to be completely fair between all forms of wealth and be a bit arbitrary and compliance cost heavy or not but not tax all forms of wealth evenly. Up to you.

Four. Who owns the wealth? From the vibe of the proposal I would say the intention is that the ultimate owner of the wealth pays the tax. However structurally wealth is likely to be held through many trusts, holding companies , limited partnerships and possibly in individuals own names. This is not insurmountable for design but will involve complicated grouping rules and possibly flows of notional credits to make it work. Perhaps have a look at the actual tax rules for imputation, mixed use assets or cashing out R&D losses to see if you still have the intestinal fortitude for what it will mean to make this work.

Five. Compliance costs. Now I don’t want to overplay this but comforting assurances that if you’re paying enough tax you’ll be fine means – two sets of calculations. The old rules will need to be applied which are not compliance lite and then the new rules willl need to be applied. And after addressing the issues above – they won’t be any picnic either.

But good luck. Perhaps in practice a tax solely on property might work. But after working through their policy I can’t help feeling all this is why countries just cut their losses with a realised capital gains tax.

And thanks for playing. First policy – one on tax – still impressed.

Namaste

Unconditional – it’s what it means

Let’s (briefly) talk about tax ( and education). Again – yes I know.

The headline of today’s Dominion Post showed that in 2015 schools collected $11 million in donations more than they had previously. Now dear readers after And another thing you all know that this means that of the extra $11 million the government subsidied this by a third.

Also interesting if you follow the embedded Stuff links you see that decile 10 schools dominate the donations stakes. By about $329 million to $2.8 million. Mega yuck given this just happens automatically and doesn’t go through Parliament every year as Education budget does.

Now this we have discussed before and promise I am not interrupting your Saturday to moan again about that.

The reason for this postette is the reference to how music lessons and school camps and the like are now being reclassified as donations.

No just no.

IRD guidance is very clear that donations need to be an ‘unconditional gift’. Nothing in return. A cash version of seva although they will probs never use that analogy.

The law is very clear and any ‘reclassification’ will be very easily overturned by the department. Please apply your brain. If you get anything in return – it ain’t a donation and so no donations tax credit.

Simple. Please carry on.

Namaste

What a capital affair!

Let’s talk about tax (havens).

After eight days on a yoga course the role of balance in postures and in life was a recurring theme. And upon finishing the course this was brought home to me quite starkly. As after eight days of sequencing Sun A and B without naming the poses, understanding my inner child and hugging people that were a week ago complete strangers – your correspondent spent the subsequent week talking about multinationals and tax havens.

Yin and yang. Perhaps not as it is traditionally known but defo in my life.

Now my views on multinationals are ‘on the record’ but I realised I haven’t ever properly discussed tax havens.

Putting aside for a moment that no country has ever owned up to being a tax haven. And so much like the term ‘fat’ – it is in the eye of the beholder.

There are a number of criteria floating around but really they can be summarised as:

- low or no tax and

- secrecy.

So yeah for New Zealand and foreign trusts pre Shewan report probs more tax haveny than not and post Shewan less tax haveny than not.

In the campaigns against them, tax havens are often swept up with the ‘multinationals – bad’ messaging. And the story goes something like this:

Multinationals strip profits from developing countries to tax havens. No tax paid in developing country or tax haven. Profits then not sent home coz they don’t want to pay tax on them. Double non-taxation – bad thing – everyone loses.

But in that story there are 2 quite distinct players:

- The developing country who is capital importing and

- the home country who is capital exporting.

The concerns of the developing or capital importing country – of which New Zealand is one – is to ensure that some tax is paid for the use of resources or on the location specific rents.

The concerns of the home or capital exporting country is to ensure that it receives some tax – after foreign tax is paid – for the capital invested.

Traditionally these two concerns have been reconciled through the OECD model for tax treaties. Broadly the approach is to let the source or capital importing country tax first but not too much. Then let the residence country also tax the income but give a tax credit for tax paid at the source country level.

Now that all works beautifully when structures are very simple and the person earning the money in the source country belongs to the capital exporting country. It becomes much more complicated when even simple entites like companies are in the mix. And it all starts to completely break down when tax paid in the capital importing country has no value as a tax credit to the ultimate owner of the capital.

Coming back to tax havens. For capital exporting countries where the multinationals are headquartered, tax havens then are a complete bugg@r. They potentially – will come back to this – put a block on the return on capital from the source country to them.

For capital importing countries like NZ the issue is not so clear. As IMHO isn’t the real concern returns leaving the country untaxed rather than where they go? Coz we have already seen with the use of hybrids it is quite possible for tax to be paid nowhere without a tax haven in sight. Also that income could also be directed to companies in the international group that were otherwise loss making – cross border loss refreshment. So really for capital importing countries, tax havens are just a tool in the mix rather than the definitive source of tax badness.

The story with tax havens being a blight on developing nations is also more nuanced than would first appear as they are often tax havens themselves. Vanuatu? Cooks? Admittedly more low rent – and therefore I would imagine more exploitable – than say Jersey or Bermuda but they still turn up on lists of potential havens.

Also capital exporting and importing countries are not as powerless against tax havens as it would first appear.

For capital exporting countries there is a 50 plus year old tool called the controlled foreign company rules that can be used against tax havens. The way it works is to say – you know if any foreign company is ultmately controlled by anyone in our country – well guess what we want to tax that income too. Trick can be knowing that income exists and so that is why the disclosure campaigns, TIEAs and automatic exchange of information are so useful. And if there continues to be non- disclosure this ups the ante with the tax administration to become potentially tax evasion and the spectre of the prison wall.

For capital importing countries its weapon of choice is the even more old school withholding taxes. Payments made to tax havens can have tax withheld at what ever rate you choose if you don’t have a tax treaty with that country. And if the treaty is a problem – it can strictly speaking be withdrawn.

The fact that these don’t happen really – IMHO – comes down to an international consensus to tax capital income more lightly than labour income. Aggravated by:

- The zero rate of tax borne by charities and pension funds;

- The active income exemption from the controlled foreign company rules;

- Classical taxation of dividends.

None of which provide any incentive to pay tax at the source country or even the home country.

Now tax havens can still be annoying to New Zealand to the extent our people have undisclosed money offshore – and the non- complying trust is worthy of its own future post – but as a country we are a net capital importer and so have much the same issues as the developing countries. And at times the label tax haven comes our way too – fairly or not.

Namaste