And another thing

Let’s (briefly) talk about tax (and donations to schools).

Following Monday‘s post I got to think about the other ‘advancement’ head of charity – education.

Now there is the whole controversy about whether donations that schools seek are really for extras and their role in an education system that is supposed to be free. And there is the thing about decile funding that the government gives less to higher decile schools coz they can fund raise.

But if that ‘fund raising’ comes from ‘donations’ then the government again gives one dollar for every two actually donated. So the bigger the donation and the higher level of actual payment – the more the government gives.

None of which is recorded in the education budget coz it is an off the books tax expenditure. So the schools with richer parents get more government help. Very progressive.

Probs not actually intended. More likely to just be an interface of separate policies and never actually thought through. Shame.

Now for those of you who are properly interested in the can of worms that is tax and charity stuff I’d recommend my friend CharitywatchNZ‘s blog. Not currently being updated as he has gone back inside (the bureaucracy) for a while. But still all good stuff.

Namaste

A plague on all your houses

Let’s talk about tax.

Or more particularly let’s talk about the tax free status of religion.

Your correspondent has just started the first stage of yoga teacher training (YTT). Three lots of 8 11 hour days spread over 6 months. It still surprises me as I have no desire to actually teach yoga. I do have a great desire to further learn the history and philosophy of a practice that has seriously helped me get my sh!t together. But not actually teach. Oh and anyone who is reading this who is doing it too and not already a teacher – totes non-deductible as it is a capital expense.

Now because I was about to get seriously busy I was planning to invoke the ‘except when there isn’t clause’ on my Monday posting commitment. But then as if we all hadn’t suffered enough with the earthquakes, floods, and closing of non-earthquake prone buildings – we got Brian Tamaki.

It’s the gays fault.

Awesome.

Strangely that pearl of post-truth wisdom from Bishop Brian has made some people so super mad that they have launched a petition to have Destiny Church’s tax free status removed. Interesting. Because of course the fact that they are a registered charity not only means they are tax exempt on any income but also that through the donations tax credit the government effectively gives them one dollar for every two given to them.

And now on my Facebook feed are coming questions – ‘so why is religion tax exempt?’. To which I’d reply ‘historic reasons‘. Advancement of religion is one of the four heads of charity. Alongside advancement of education, relief of poverty and other matters beneficial to the community.

Historically the churches were our welfare system. And even now a lot of social services are undertaken by church based groups. But that would still fit under the ‘relief of poverty’ head.

And religion and church going is beneficial to many people. In fact there is no additional ‘public benefit’ test for the religious head coz it is just presumed to be beneficial to the community.

Now I would argue I get similar benefits from my yoga practice. So yeah it does seem a tad anachronistic given the country is increasingly secular. And the gay thing is interesting too. As although the state has said marriage is between two consenting adults – that is a step too far for our churches.

But if advancement of religion were removed; churches would then have to make their case that what they did was a matter beneficial to the community and that it had a public benefit.

Perhaps not lead with Bishop Brian.

Namaste

Extra fox

Let’s talk about tax.

Or more particularly let’s talk about secondary tax.

Early on in my mothering life as a good middle class parent your correspondent – or probs a family member as I was pretty much exhausted for the first couple of years with each baby – bought Dr Seuss’ ABC.

Aunt Abigail’s Alligator A – A – A

All the letters had rhymes with words that started with the ‘profiled’ letter. The exception – pun coming – was the letter X. Because I guess xylophone and xenophophia were outside the target range for preschoolers – the rhyme became X is very useful for words like ax (with no fricken e) and extra fox.

Now while I was still 5 plus years away from discovering tax, Mr your correpondent and I always read that as extra tax. Coz I mean what is an extra fox for goodness sake? Aunt Abigail’s Alligator now that makes sense but – Dude really – an extra fox? What’s that about?

Now amonst the Precariat secondary tax is very much considered to be an extra tax. And according to the Council of Trade Unions the Labour party has promised – as they did last election – to repeal it on coming to government.

Thing is they haven’t actually promised that. They have said in the detail of recommendation S8 that the Government as part of Inland Revenue’s business transformation should look to remove secondary tax. These are subtle but important distinctions which we will come back to. Lucky for them Labour actually has someone on their team that gets tax.

So what is secondary tax?

Well it is the tax deducted on second jobs. It is a function of having the progressive tax scale that the left loves so much.

First jobs get code M which I guess stands for main job. It takes the pay and multiplies it by the number of pay periods to get an annual amount ; calculates the tax and then divides that by the number of pay periods to get the tax for the income in the period. While it is relatively simple it does mean those with lumpy pays – overtime; seasonal workers – are overtaxed as a high pay is assumed to be a high annual income.

Second jobs however people have to choose a flat rate – secondary tax – based on how much they earn from other jobs. And there is a view – clearly shared by the CTU – that this overtaxes their income. Now it is true that it taxes second jobs more than first jobs but this is really just to reflect that extra income means higher tax.

Coz remember how progressive taxation means the more income you earn the proportionally greater tax you pay? Yeah well this is how it is implemented for those with second jobs und the current PAYE system.

Now I fully get that as it is a flat rate and if you don’t earn as much as you thought you will be over taxed. But that is a function of our PAYE system being inherently middle class. As it works beautifully for those on stable incomes ie salaries.

Everyone else with unstable incomes – even if it is only from one job – runs the risk of being overtaxed and then yes needing the claim a refund. And then yes if you go to those refund companies they’ll take a cut. There is an IRD option but they don’t have the marketing budget of the refund firms so it is less well known.

The real issue though is the changing face of employment and precarious work – something the Labour Party is at least acknowledging and trying to address. Yeah I am not sure about the training levy either – but at least they are trying.

So yeah trying to get BT to address lumpy incomes is a good idea. So good that Hon Mike may have his officials on it already.

Just repealing secondary tax though is a really dumb idea.

Unless you are happy with undertaxation and people needing to file and/or becoming non-compliant with all the associated risks. Alternatively it is an argument for widening the bottom bands. But rich people will get that benefit too. So Labour Party – trying to get technology to solve it is the right direction.

Real issue though is the numbers outside the withholding systems coz they’re not employees.

Namaste

TGIF

No more Friday posts dear readers – except when there are.

The methadone programme that is this blog is working well. I am now getting increasingly busy on other stuff and tax is becoming less of my life.

Posts will now be on Monday except when they aren’t.

Keen beans – who haven’t already – may like to like this blog’s facebook page as I occasionally post other stuff there too – submissions and other articles.

Á lundi.

The Country Immunity

Let’s talk about tax.

Or more particularly let’s talk about private and domestic expenses for farmers.

One of the key reasons I spent the greater part of my working career in tax was that I was rarely bored. Challenged – often; frustrated -sometimes but bored rarely. Add in the sense that I was a small cog in a system that tried to make sure the tax rules applied to everyone and you get almost 2 decades of socially productive and largely personally satisfying work.

The thing though about tax is that you could never drop your guard. You might think you have the answer but then find a transitional exemption; an unexpected definition or an obscure case could mean that the answer of Orange you gave from careful analysis was wrong and it should have been Pink.

Now I had thought that with blogging I would be relatively safe from that experience: I was choosing my topics and they were all pretty general. At worst I could invoke the ‘Not tax advice. Follow at your peril’ disclaimer.

But no.

After the recent post on private mortgage costs a reader pointed out to me a recent public consultation document from the technical side of Inland Revenue with the innocous title of Deductibility of Farmhouse Expenditure.

Now there was nothing actually wrong in the OP – original post look at me being all real blogger like – as that post related to someone’s suburban house. However I extravagantly branched off and concluded that there was no ‘country immunity’ from the private and domestic test for deductibility of expenses.

Boy was I wrong.

Clearly I have spent far too long in international tax. As what that document makes clear was in the 60’s after ‘negotiation with the industry’ Inland Revenue allowed interest on private farmhouses to be fully deductible.

Wow. Just wow. Mind blown.

Now I guess it isn’t as bad as it seems as then farms would have been massive and houses small in comparison. And like didn’t Mrs Farmer have to feed shearers and stuff which is business related. And apportionments are such a pain so close enough is near enough and let’s call it fully deductible.

Only thing is didn’t actually comply with the law; was a concession and would defo have been a tax expenditure if it had been legislated for.

But it is kind of a while ago and things are different now. In the sixties women weren’t paid the same as men; the Rugby Union was criticised for its lack of diverse perspectives and a National government was approaching its fourth term. So you know like completely different.

And while I could make a number of cheap shots like – seriously it has taken you 50 years to apply the law properly – I won’t. It would have required a high degree of intestinal fortitude to take the small farmers concession away. So nice one. Carry on Mrs Commissioner.

Only thing is while proposed change is a massive improvement, the practical compliance cost friendly option for large farms is still in your correspondent’s view unnecessarily concessionary. Particularly as there is no actual reduction in compliance costs.

So in terms of my dinner party companion’s comment: ‘This is the country – we get tax deductions for all sorts of things…’ Yeah mate you do. Fewer than before and more than I realised. But yeah you do.

Namaste

Bonne chance Madam Secretary

No post today but I’ll leave you with this instead.

Ruining childhoods one tax working group at a time

Let’s talk about tax.

Or more particularly let’s talk about who Labour should put on their tax working group if/when they become the next government.

Earlier this year Ghostbusters was remade with women in the lead roles. Reviews were quite binary being ‘absolutely brilliant’ or ‘its ruined my childhood’. The latter review is quite a big call when as a mother I am sure I messed up my children far more than any movie. Clearly these gentlemen – and I use the term very loosely – were blessed with parental experiences far superior to wot I provided.

But it got me thinking what would a tax working group remix look like with women in the key roles. In 2001 Shirley Jones – who wasn’t the mother of David Cassidy – was one of the five members of the review group and in 2008 Susan St John was a kinda ring in member in the 2008 Tax Working group. That’s it. Hardly stellar or at all representative of the smart kick arse women I came across in my time in tax.

So I thought I’d put together a long list for the next lefty government to pick from.

All these women I have either worked with, professionally disagreed with – often strenuously – and/or been influenced by. They span academia, private practice and the judiciary. They are all top of their game. I have excluded current public servants.

And yeah a number are personal friends – I hope even after this post – but that has never been a limiting factor for people putting such lists together in the past.

So who are the Daraenys Targaryens of tax best able to advise a next government wanting to ‘rebalance the tax system’.

Chair Dame Susan Glazebrook have no idea if sitting judges can serve on working groups but hey this is a blog post I can assume all the can openers I want. She was co author of the still widely used book on financial arrangements which are seriously hard. She had a distinguished career as a tax lawyer and was well respected on both sides before going to the High Court in 2001. A serious brain mixed with good judgement. Couldn’t think of anyone better as Chair.

Members

Lisa Marriott – Chartered Accountant and Associate Professor in tax at Victoria. Author of the seminal work on the differences of treatment of tax evasion and benefit fraud in the criminal justice system.

Susan St John – Economist and Associate Professor at Auckland University. Expert on tax benefit interface – or lack thereof.

Teresa Farac – Chartered Accountant and Partner at Deloittes. Never met anyone with her depth of technical knowledge. On technical issues she is always right. Just accept it.

Joanne Hodge – Lawyer and former Bell Gully partner. Astute and insightful mind. Has now given up tax twice. So seriously impressive judgement.

Kirsty Keating – Lawyer; Partner at EY law and former Senior Solicitor at IRD. A tax disputes expert – or tax controversy as they delightfully call it. Sees the results of when good tax policy goes bad as well as the operation of the department in its full technicolour glory.

Emma Richards – Lawyer; Director at PwC and a million years ago was an analyst in IRD’s Rulings unit. One of New Zealand’s top tax technicians. If I ever had a hard transaction – I would want her on it.

Deborah Russell – Senior Lecturer in Tax at Massey, former Senior Analyst at IRD and a woman with views. Her inclusion on the list is a tad surreal though. Not through lack of merit – but more that she could be the Minister of Revenue commissioning this group on a change of government.

Susan Guthrie – Economist and co author with Gareth Morgan on the Big Kahuna. Whatever its practical or political acceptability issues, it does interface tax and benefits and is always worth coming back to as a counterfactual.

Anne-Marie Brook – Economist, Policy Fellow at Motu and former senior Treasury Official. Past work on tax and savings now looking at Human Rights and economic success. Macroeconomics background including stints at Reserve Bank and OECD.

In fact I don’t know about a ‘long list’. It all looks pretty good to me – albeit a bit too white. Whether it is enough to make little girls want to grow up to be tax geeks – couldn’t tell you. Need to ask a little girl.

Grant and James – you’re welcome. But how about doing the same for your own parties economic representatives? The Nats have Paula. Do you want them to out progressive you?

Namaste

Thickness of a prison wall

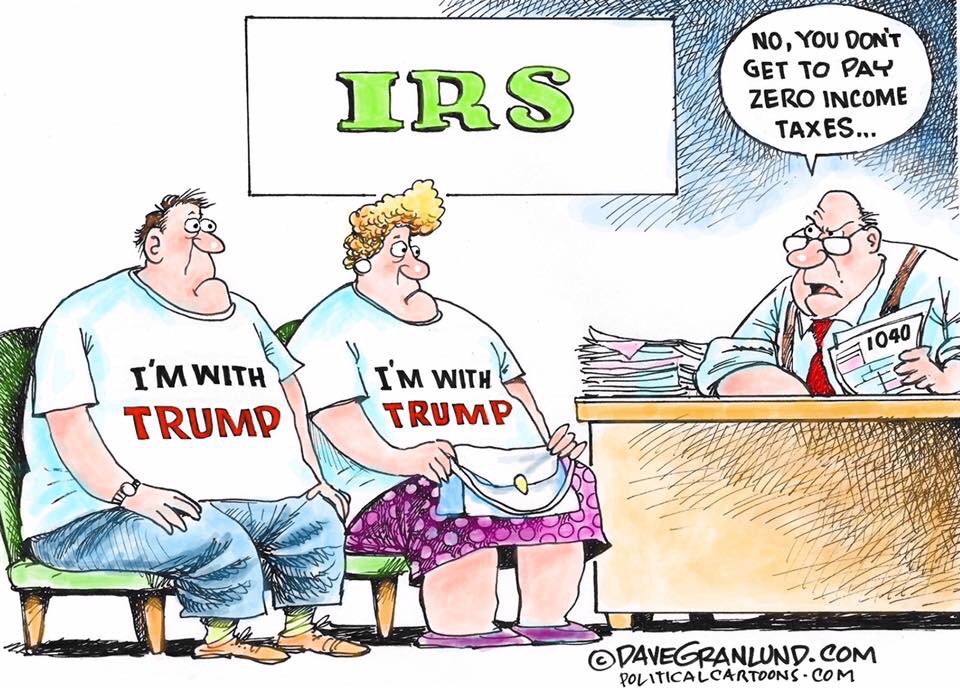

Let’s talk about tax (and tax avoidance).

Last week the government announced it was building yet another prison. Another moral and fiscal failure. Skilfully continuing to over turn the falling crime rate dividend we had in 2013 before the bail laws changed.

Also last week a reader made a comment about how wasn’t tax avoidance ‘legal’.

Another such observation on tax avoidance came from Denis Healey who said that the difference between tax avoidance and tax evasion is the thickness of a prison wall. She said trying to link two quite independent things together.

Now both maybe right in the United Kingdom but they really don’t directly translate to the New Zealand situation. So being the public spirited individual I am I thought I’d have a go at a layman’s guide to tax avoidance for New Zealanders. And no more mention of prison stuff – promise.

First of all tax avoidance is a term defined in the Income Tax Act. It comes in and overrides everything else in the Income Tax Act. So any provison in the Act theoretically runs the risk of tax avoidance coming in and saying – ‘you know what’ just kidding – bog off.

And it is defined in a way – directly or indirectly altering the incidence of tax – that could mean that anything you do that has the effect of reducing your tax could be caught. This could mean cutting your hours; paying off your mortgage instead of putting the money on term deposit; selling dividend paying shares to buy a car all could be classed as tax avoidance. As they were all plans or understandings – where the result was less tax was paid than before or less tax was paid than could have been.

Mmm yeah.

Now as that couldn’t possibly be right the courts – helped by the Commissioner taking cases – has said it only applies when the outcome wouldn’t have been intended by Parliament. Right. Awesome. So much clearer now. Thanks for playing.

To be fair there is a little more to it than that. But largely it all boils down to:

1) strip away the clever stuff

2) work out tax result on stripped down ‘arrangement’

3) compare 2) to what went of tax return

4) Difference is tax avoidance.

Now most of the dispute between taxpayers and Commissioner is over what if any is the ‘clever stuff’.

In our friend Penny and Hopper putting a business into a trust was never challenged – coz you know creditor protection or keeping it from the missus wasn’t ‘clever’ it was just like ‘commercially acceptable’. In that case what was challenged as ‘clever’ was the trust paying the highly skilled doctors the same salary as they would earn in the public system – I mean Dude seriously who works for that?

The other recent case that made the tax community super mad – Alesco – involved the New Zealand business being funded by an optional convertible note. Now dear readers you may say ‘ ah yes I’ve read I choose you Pikachu ‘ an optional convertible note now that is ‘clever’ and so that is tax avoidance. Glad you are keeping up – but no. No what was clever here was that the option should have no value as Alesco Australia already owned all the shares – Duh. Other highlights of that case included the taxpayer arguing that while it was tax avoidance – it was Australian not New Zealand tax avoidance. All class.

Compare these then to the cutting your hours; paying off your mortgage or buying a car from savings. Nothing clever there – so long as that is all you are doing. Bit like our gentlemen below.

Now of course there is a line between a bit of tax planning – paying off your mortage before earning taxable income; funding a project with deductible debt or even investing offshore and receiving an exempt dividend – and tax avoidance. And because there is this line there will always be a Tax Administration and tax practitioners.

The thing is though that even if it is ‘tax avoidance’ it is a Civil thing and so no one goes to jail. They can lose the tax benefits; get hit with a 100% penalty plus interest of 8% – but no prison wall. Not even Home D.

Tax evasion however game on – Criminal charges defo in the mix. Now generally there is nothing clever with tax evasion. Just dirty fraudulent or deceptive behaviour: taking money out of the till; cashies – yes cashies; billing for a lower/higher number than is actually the case. Here jail time is totes on the cards and does happen. As well as a penalty of 150% and interest. And yes there is a line between avoidance and evasion too.

So is tax avoidance legal if Wikiquote says so too? Dunno it certainly isn’t criminal but does have high penalties.

So keep away from the clever sh@te and my former colleagues will probs keep away from you.

Namaste

Working on my playstation tan

Let’s talk about tax (and multinationals).

In her time your correspondent has been mistaken for a number of things. This has included being a

- Catholic;

- Card player; and

- Lawyer

But – you know what – apologist for foreign capital really hasn’t ever been one of them. So with this in mind I have been following the campaigns against multinationals and their non-taxpaying behaviour. And much as I hate to say this – I actually feel a bit sorry for them. Not a lot mind – but a bit.

A year or so ago while I was still at Treasury I went to the Accountants tax conference. Highlights included a Hip Hop presentation from a group in South Auckland in lieu of an after dinner speech. Pretty progressive for a bunch of tax geeks.

Also one of the main presentations showed the UK enquiry on multinationals where politicians – with no sense of irony – were giving Apple and the likes biffo for how they structured their businesses in response to the laws the politicians had enacted. Facepalm.

Now the public information surrounding multinationals non-taxpaying isn’t pretty. Double Dutch Irish sandwiches and the like. Great for headlines but not for taxbases.

All done through a combination of being in a country in substance but not for tax – the preparatory and auxillary out from a permanent establishment; treaty shopping in the form of royalties going to low tax counties and/ or excessive royalty payments. None of it – even to me – is the behaviour of a good corporate citizen.

But here’s the thing – in New Zealand a country where tax laws can be changed and cases can be run successfully in the courts – one of two things will be the case:

Option one. It is tax avoidance.

Now when I say ‘tax avoidance ‘ – this is tax avoidance in terms of the statutory provisions not tax avoidance coz people think they should pay more tax than they are.

If it is tax avoidance according to the law then my former colleagues will be getting right stuck in. Now Corporate Legal – remember breathe out – all these issues are beyond public domain. They would – Corporate Legal note conditional tense -be getting right stuck in as they/we did with the banking cases; avoidance of the top marginal rate; and the hybrid instrument cases. None of which required public outcry before that happened. Just a tax department getting on with its job.

However public outcry is pretty awesome for the front line in tax policing. Always good to know you are on same page as people you are serving.

Now there is quite a delay from problem indentification to going to court – dispute rules; fully discussing the issue with the taxpayer; briefing experts and ensuring all parts of the department are on board or at least don’t disagree and so on. And then there is the possiblity a taxpayer settles; in which case it is never public.

But dear readers never assume that just because you haven’t heard anything that nothing is happening. Because secrecy provisons. The very same ones I spend every blog post negotiating.

Option two. It is not tax avoidance in terms of the statutory provisions.

Now if that is the case this means the outcome was intended by Parliament. In the same way currently:

- Sales of businesses; houses; farms and other assets such as shares bought without the intention of resale are not taxed;

- Interest deductions for capital assets that may have incidental income are allowed and can be offset against other unrelated income;

- Income earned by contractors who do very similar work to employees are allowed work related deductions;

- Imputed rents are untaxed;

- Industries such as bloodstock and forestry either have accelerated deductions or deductions for capital;

- Businesses operated by charities are untaxed;

- There can be significant delay between income earned at the company level and when it is paid out to shareholders

- Transfer pricing or associated persons rules don’t apply to consortiums acting together as one entity;

- The thin capitalisation rules allow businesses funded by creditors the ability to strip profits by way of excessive interest.

Now there is also a move to make multinationals disclose how much tax they pay. Ok cool. But why is it only multinationals and not any beneficiary – which would include a lot of you dear readers I know it would include me – of the above list? Why is their non taxpaying so special?

And here’s the thing. Parliament – or really the government of the day – can change its mind. So if any or all of the above is ok but the multinational thing isn’t – Hon Mike can propose a law change. The current solution du jour is a diverted profits tax.

So maybe the target of the campaigns should be the politicans who continue to allow it rather than some companies that couldn’t help themselves? Just saying.

The campaigns will have been very useful in giving Hon Mike an ’empowering environment’. But maybe coz Hon Mike hasn’t done anything yet maybe it is tax avoidance. Even then taking avoidance cases ad infinitem is no way to run tax system.

So Hon Mike GET ON WITH IT!

Coz it is not like boycotting products is an option. At least for me. I am an Apple addict. Not so sure about ios 10 though.

One final thing dear readers – although I am now back to posting twice a week – Monday is Labour Day. So as a good lefty I am downing tools and will be back next Friday.

Namaste.

Everything is connected to everything else

Let’s talk about tax.

Or more particularly let’s talk about about a case I mentioned last week in the alignment post. It was quite controversial at the time within the tax community and did leak out a bit into the general public. As is often the ‘case’ tax is just an overlay on other interesting stuff.

Also thought of it again wot with the junior doctors strike and how the consultants would be helping over that period. I guess coz its Health that means its not strike breaking?

Anyway back to the case. Penny and Hooper (last names) were both specialist doctors earning shed loads of cash in Christchurch fixing the bung knees of those who were in denial about the length of their running careers and had yet to find yoga.

Now these gentlemen were unremarkable in that they weren’t big on paying tax according to the progressive tax scales that applied to little people and so adopted a structure recommended by their accountant. I mean everyone was doing it and what could possibly go wrong. In fact even John Shewan – of Shewan report fame – said it was bog standard behaviour.

The wheeze was that they put their businesses into a trust which at that time had a lower tax rate (33%) than the little people faced who earned over $60,000 ( threshold increased at some point but detail not relevant) 39%.

The Commissioner who was a he at the time – yes Virginia men can be senior public servants – was not best pleased. He used a bunch of words like ‘tax avoidance’,’market salary’ and ‘not’and made them pay tax like the little people. Go Team Commissioner.

The tax community also used a bunch of words like ’emmently foreseeable’; ‘lack of certainty’; and ‘chilling effect on investment’. Well maybe not the last set but that is never far away when the big people are being made to pay tax.

Anyway the Commissioner won; tax accountants lost; largely graciously ate that and everyone moved on to the next tax dept v tax community stousch.

There was some commentary at the time about how this was more than a tax case – at which point I got very excited – only to find it was about trusts could be looked through and weren’t as inviolable as people thought.

But what was never discussed was how two men who were educated at the state’s expense presumably before student loans; weren’t bonded; and whose business was almost wholly paid for by the taxpayer via ACC were earning so much money. I guess it was before the days of ‘joined up government’.

I also guess Labour’s ‘three years free’ policy will also remove what little royalty we currently get from the taxpayers’ investment in such lovely people.

All the more reason then guys to make sure misalignment works and they do actually pay the top tax rate.

Namaste