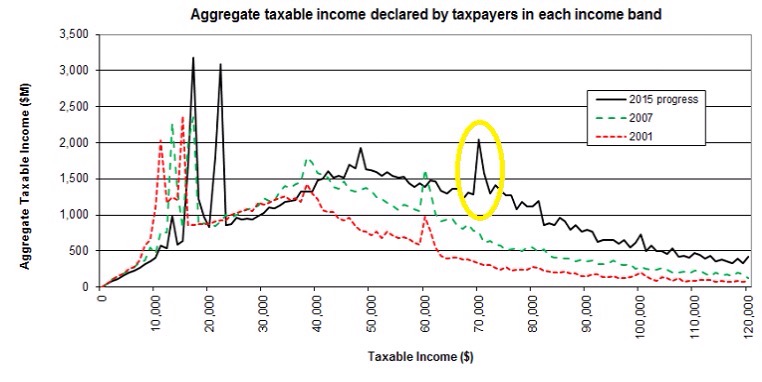

The Spike

Let’s talk about (the recent Greens’ press statement on) tax.

Recent data has shown there is a spike around $70,000 of reported taxable income for individuals – convienently the point where the top marginal tax rate of 33% starts. And according to the Greens this shows evidence of tax avoidance by rich people which can be fixed by – among other things – increasing Inland Revenue’s investigation budget. Mmm maybe.

Before I go on, I am working on the assumption that when the Greens talk about tax avoidance it is in the colloquial ‘not paying as much tax as I think you should’ kinda way rather than tax avoidance according to the actual law. All cool but unfortunately (or fortunately) the department is constrained by what Parliament has enacted and how the Courts have interpreted it.

Now in the mid 2000s – it is true – similar spikes were evidence of widespread tax avoidance among self-employed professionals. The wheeze was that they were employed by trusts which were taxed at 33% on the income the individuals earned – not the top individual’s rate of 39%. And then the trust paid the individuals a below market salary for their services to the trust.

Only the below market salary was taxed at 39% and the rest of the income at the lower trust rate. And then any tax paid income of the trust could then be distributed tax free to beneficiaries. Too easy and too good to be true. Hence tax avoidance according to the actual law.

Moving to 2017. The trust and top personal rate are the same so that particular wheeze won’t work. But now we just have misalignment between the company rate at 28% and the top personal rate of 33%.

Except that under a misalignment with the company rate there is no distributing the income tax free. When income is distributed from the company to the shareholder – a dividend – it is subject to another 5% tax. Now any ‘tax avoidance’ – in theory anyway – is just timing until the shareholder needs the money. There should be no ultimate reduction in tax. Although timing advantages can be a big deal and can also make something tax avoidance under the actual law.

But the only way I can see of moving this from tax avoidance – not paying as much tax as I think you should – to tax avoidance under the actual law is if the department can show that the $70k is not a market salary – as they did with the self employed professionals.

And while that wasn’t simple for the department last time – now all tax advisors know about the need for a market salary – possibly from painful personal experience. So anyone giving advice that $70k is an acceptable salary – when the market rate is higher – does so knowing it could be attacked by the department and will have all the supporting arguments ready.

But the Greens are right the spike is still there. Last time the spike was widespread tax avoidance according to the actual law – so why wouldn’t it be this time too? Not the first time I have lacked imagination.

Just in case tho I am right – I am also all about the solutions. And there is at least one way of getting rid of the spike without increasing anyone’s budget. Think of all that extra money Greens you could spend on cleaning up the rivers instead of tax inspectors.

One way is to increase the company tax rate to the top marginal rate.

Another way is to make the look-through company (LTC) rules compulsory.

Currently any company with five or fewer shareholders can choose not to be taxed as a company. Instead income and losses are taxed as if the shareholders had earned the money themselves. Except currently those rules are optional. Make them compulsory and the spike goes. No more income in more lowly taxed closely held companies as no more closely held companies for tax purposes. Simple.

And the really good news for the Greens is that there is currently a bill in the House making changes to the LTC rules; so a Supplementary Order Paper doing just that would be totes in scope. Oh and it is an ‘annual rates’ bill too so they could also have a go at the company tax rate at the same time. Awesome.

Now lots of people who haven’t made an LTC election may not like that and say so quite loudly. Coz that’s what you get when you are strong on policing tax avoidance – lots of upset people all with lots of incentive to write to you and come and tell you how upset they are.

But unless the current law with closely held companies – or company tax rate – changes I can’t see any level of increased funding will get rid of that nasty spike.

Namaste.

Gareth responds

I wouldn’t normally create an entire post for a commentator. But hey it is my blog and not everyone is dedicating themselves to overhauling our country in a socially progressive way. Also I did devote an entire post to them so only seems ‘fair’ – as much as I dislike that term – to do the same for the response.

There must be a technologically prettier way to reproduce his comments – but until number one son comes home for Xmas – this is the best I can do.

Namaste.

Extra fox

Let’s talk about tax.

Or more particularly let’s talk about secondary tax.

Early on in my mothering life as a good middle class parent your correspondent – or probs a family member as I was pretty much exhausted for the first couple of years with each baby – bought Dr Seuss’ ABC.

Aunt Abigail’s Alligator A – A – A

All the letters had rhymes with words that started with the ‘profiled’ letter. The exception – pun coming – was the letter X. Because I guess xylophone and xenophophia were outside the target range for preschoolers – the rhyme became X is very useful for words like ax (with no fricken e) and extra fox.

Now while I was still 5 plus years away from discovering tax, Mr your correpondent and I always read that as extra tax. Coz I mean what is an extra fox for goodness sake? Aunt Abigail’s Alligator now that makes sense but – Dude really – an extra fox? What’s that about?

Now amonst the Precariat secondary tax is very much considered to be an extra tax. And according to the Council of Trade Unions the Labour party has promised – as they did last election – to repeal it on coming to government.

Thing is they haven’t actually promised that. They have said in the detail of recommendation S8 that the Government as part of Inland Revenue’s business transformation should look to remove secondary tax. These are subtle but important distinctions which we will come back to. Lucky for them Labour actually has someone on their team that gets tax.

So what is secondary tax?

Well it is the tax deducted on second jobs. It is a function of having the progressive tax scale that the left loves so much.

First jobs get code M which I guess stands for main job. It takes the pay and multiplies it by the number of pay periods to get an annual amount ; calculates the tax and then divides that by the number of pay periods to get the tax for the income in the period. While it is relatively simple it does mean those with lumpy pays – overtime; seasonal workers – are overtaxed as a high pay is assumed to be a high annual income.

Second jobs however people have to choose a flat rate – secondary tax – based on how much they earn from other jobs. And there is a view – clearly shared by the CTU – that this overtaxes their income. Now it is true that it taxes second jobs more than first jobs but this is really just to reflect that extra income means higher tax.

Coz remember how progressive taxation means the more income you earn the proportionally greater tax you pay? Yeah well this is how it is implemented for those with second jobs und the current PAYE system.

Now I fully get that as it is a flat rate and if you don’t earn as much as you thought you will be over taxed. But that is a function of our PAYE system being inherently middle class. As it works beautifully for those on stable incomes ie salaries.

Everyone else with unstable incomes – even if it is only from one job – runs the risk of being overtaxed and then yes needing the claim a refund. And then yes if you go to those refund companies they’ll take a cut. There is an IRD option but they don’t have the marketing budget of the refund firms so it is less well known.

The real issue though is the changing face of employment and precarious work – something the Labour Party is at least acknowledging and trying to address. Yeah I am not sure about the training levy either – but at least they are trying.

So yeah trying to get BT to address lumpy incomes is a good idea. So good that Hon Mike may have his officials on it already.

Just repealing secondary tax though is a really dumb idea.

Unless you are happy with undertaxation and people needing to file and/or becoming non-compliant with all the associated risks. Alternatively it is an argument for widening the bottom bands. But rich people will get that benefit too. So Labour Party – trying to get technology to solve it is the right direction.

Real issue though is the numbers outside the withholding systems coz they’re not employees.

Namaste

Thickness of a prison wall

Let’s talk about tax (and tax avoidance).

Last week the government announced it was building yet another prison. Another moral and fiscal failure. Skilfully continuing to over turn the falling crime rate dividend we had in 2013 before the bail laws changed.

Also last week a reader made a comment about how wasn’t tax avoidance ‘legal’.

Another such observation on tax avoidance came from Denis Healey who said that the difference between tax avoidance and tax evasion is the thickness of a prison wall. She said trying to link two quite independent things together.

Now both maybe right in the United Kingdom but they really don’t directly translate to the New Zealand situation. So being the public spirited individual I am I thought I’d have a go at a layman’s guide to tax avoidance for New Zealanders. And no more mention of prison stuff – promise.

First of all tax avoidance is a term defined in the Income Tax Act. It comes in and overrides everything else in the Income Tax Act. So any provison in the Act theoretically runs the risk of tax avoidance coming in and saying – ‘you know what’ just kidding – bog off.

And it is defined in a way – directly or indirectly altering the incidence of tax – that could mean that anything you do that has the effect of reducing your tax could be caught. This could mean cutting your hours; paying off your mortgage instead of putting the money on term deposit; selling dividend paying shares to buy a car all could be classed as tax avoidance. As they were all plans or understandings – where the result was less tax was paid than before or less tax was paid than could have been.

Mmm yeah.

Now as that couldn’t possibly be right the courts – helped by the Commissioner taking cases – has said it only applies when the outcome wouldn’t have been intended by Parliament. Right. Awesome. So much clearer now. Thanks for playing.

To be fair there is a little more to it than that. But largely it all boils down to:

1) strip away the clever stuff

2) work out tax result on stripped down ‘arrangement’

3) compare 2) to what went of tax return

4) Difference is tax avoidance.

Now most of the dispute between taxpayers and Commissioner is over what if any is the ‘clever stuff’.

In our friend Penny and Hopper putting a business into a trust was never challenged – coz you know creditor protection or keeping it from the missus wasn’t ‘clever’ it was just like ‘commercially acceptable’. In that case what was challenged as ‘clever’ was the trust paying the highly skilled doctors the same salary as they would earn in the public system – I mean Dude seriously who works for that?

The other recent case that made the tax community super mad – Alesco – involved the New Zealand business being funded by an optional convertible note. Now dear readers you may say ‘ ah yes I’ve read I choose you Pikachu ‘ an optional convertible note now that is ‘clever’ and so that is tax avoidance. Glad you are keeping up – but no. No what was clever here was that the option should have no value as Alesco Australia already owned all the shares – Duh. Other highlights of that case included the taxpayer arguing that while it was tax avoidance – it was Australian not New Zealand tax avoidance. All class.

Compare these then to the cutting your hours; paying off your mortgage or buying a car from savings. Nothing clever there – so long as that is all you are doing. Bit like our gentlemen below.

Now of course there is a line between a bit of tax planning – paying off your mortage before earning taxable income; funding a project with deductible debt or even investing offshore and receiving an exempt dividend – and tax avoidance. And because there is this line there will always be a Tax Administration and tax practitioners.

The thing is though that even if it is ‘tax avoidance’ it is a Civil thing and so no one goes to jail. They can lose the tax benefits; get hit with a 100% penalty plus interest of 8% – but no prison wall. Not even Home D.

Tax evasion however game on – Criminal charges defo in the mix. Now generally there is nothing clever with tax evasion. Just dirty fraudulent or deceptive behaviour: taking money out of the till; cashies – yes cashies; billing for a lower/higher number than is actually the case. Here jail time is totes on the cards and does happen. As well as a penalty of 150% and interest. And yes there is a line between avoidance and evasion too.

So is tax avoidance legal if Wikiquote says so too? Dunno it certainly isn’t criminal but does have high penalties.

So keep away from the clever sh@te and my former colleagues will probs keep away from you.

Namaste