Tax and small business (2) – company tax rate

Last week was a big week for your correspondent.

On Wednesday I got to upgrade my CA certificate to a FCA one at a posh dinner at Te Papa. As a third generation accountant I was absolutely tickled pink by that.

Interestingly of the 12 Wellington people there were 5 tax people: Me, Mike Shaw, Suzy Morrissey, Stewart Donaldson and Lara Ariel. All except Lara I have had the great pleasure to work with personally and professionally over the years.

I got to give a wee talk and so thanked my Wakefield (mother’s accountant line) genes; the balance sheet for being able to distinguish between the concept of capital as an asset or net equity – a framework other professions lack; and Inland Revenue Investigations as both the employer of my proposers and the place of some of the highlights of my personal and professional life.

I gave a slightly longer talk on the Tuesday. Twelve minutes instead of two.

The theme of that seminar was options to improve fairness now that extending the taxation of capital gains was off the table. The punchline of my talk was that the company tax rate should be raised.

I had come to that point following lots of feedback on my tax and small business post.

Very experienced tax people were sympathetic to my concerns but the ideas of mandating the LTCs rules or restricting interest deductions or even a weighted average small company tax rate sent them over the edge with the compliance costs involved. Their preference was that it was just simpler all round to increase the company tax rate with adjustments such as allowing the amount of deductible debt for non-residents.

And so on Tuesday I had a go at putting that argument.

Clearly not well as Michael Reddell described the argument as cavalier given NZ’s productivity issues.

Regular readers will know I am concerned about whether the tax system is a factor in New Zealand’s long tail of unproductive firms without an up or out dynamic. And that is before we get to any well meaning – but not always hitting the mark – collection of small companies tax debts inadvertently providing working capital for failing firms.

Although I had twelve minutes to talk on Tuesday, the company tax punchline really only got a minute or two to expand. So I’ll try and have a better go at it here. (1)

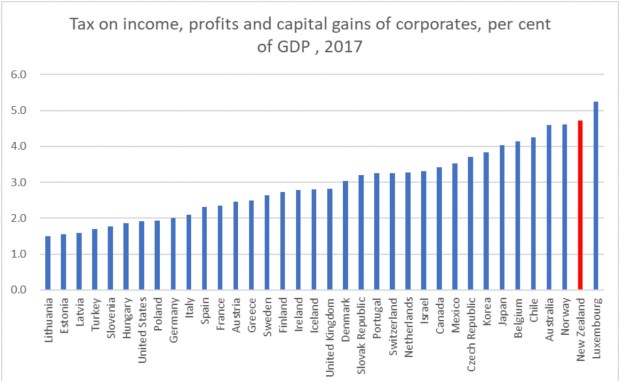

Now before we get to the arguments in favour of a company tax increase, Michael referred to this table as prima facie indicating that business income is not overtaxed.

Yep.

This table absolutely shows that second to – that other well known high tax country – Luxembourg, New Zealand’s company tax take is the highest in the OECD as a percentage of GDP.

My difficulty is that – in a New Zealand context – I struggle to call the company tax collected – a tax on business income.

Absolutely it includes business income.

But it also includes tax paid by NZ super fund – the country’s largest taxpayer and Portfolio Investment Entities which are savings entities. In other countries such income would be exempt or heavily tax preferred. And yes I know there are arguments about whether they are the correct settings or not but all that tax is currently collected as company tax.

Also, for all the vaunted advantages of imputation, the byproduct of entity neutrality is the potential blurring of returns from labour and capital for closely held companies. So – and particularly with a lower company than top personal rate – there will always be income from personal exertion taxed at the company rate.

And business income is also earned in unincorporated forms such as sole trader or partnership. All subject to the personal progressive tax scale rather than the flat company rate.

Australia’s company tax is also high but less so. Possibly a function of their lower taxation on superannuation than New Zealand or even that such income is classified according to its legal form of a trust.

And all that is before we get to issues like classical taxation in other countries encouraging small businesses to choose flow through options to avoid double taxation. An example is S Corp in the US. Tax paid under such structures will not be shown in the above numbers as the income is taxed in the hands of the shareholders.

It is true that we have a similar vehicle here in the look through company. But unsurprisingly, under imputation, this is used primarily for taxable incomes of under $10k. It is quite compliance heavy and does require tax to be paid by the shareholder while it is the company that has the underlying income and cash. But it is elective and seems to be predominantly currently used as a means of accessing corporate losses.

But back to tax fairness and company taxation.

The argument put to me by my friends – with more practical experience than I have – was: if you want to increase the level of taxation paid by the people with wealth – increase the company tax rate as that is the tax rich people pay. The logical tax rate would be the trust and top personal rate – currently 33%.

That company tax is the tax rich people pay is absolutely true. The 2016 IR work on the HWI population shows exactly that:

It would also mean that the rules that other countries have like personal services companies or accumulated earnings – that we absolutely need with a mismatch in rates – no longer become necessary.

But what about foreign investment through companies?

If the focus was New Zealanders owning closely held New Zealand businesses, an adjustment could be made either by increasing the thin capitalisation debt percentage or making a portion – most likely 5/33 – of the imputation credit refundable on distribution.

However there is also an argument not to do this. The relatively recent cut in the company tax rate has not particularly affected the level of foreign investment in New Zealand. (2)

Personally I am agnostic.

Listed companies?

Based on officials advice to the TWG (3) this group fully distributes its taxable income. So if the company tax rate increased all this would mean was that resident shareholders received a full imputation credit at 33% rather than one at 28% and withholding tax at 5%.

What happened to non-resident shareholders would depend on the decision above on non-resident investors. Either they would pay more tax on income from NZ listed companies or there could be a partially refundable imputation credit to get back to 28c.

The top PIR rate for PIEs could now also be increased to the top marginal tax rate for individuals as I keep being told the 28c rate is not a concession – more to align it with the unit trust or company tax rate. Or maybe KiwiSavers stay at 28% alongside an equivalent reduction for lower rates.

Start ups already have access to the look through company rules and so some more may access those rules if the shareholders marginal rates were below an increased company tax rate.

So an increase in the company tax rate need not have a material impact on foreign investment, listed companies and start ups.

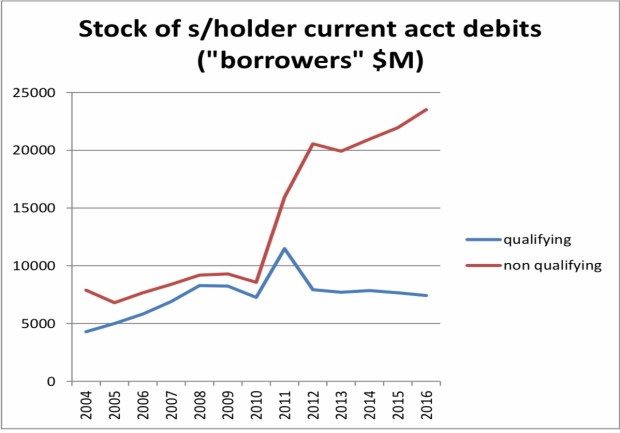

Which then brings us to profitable closely held companies. Ones where the directors have an economic ownership of the company. A lower tax rate should, on the face of it, have allowed retained earnings and capital to grow faster. And therefore allow greater investment.

And on the face of it that is what has seemed to happen with this group. Imputation credit balances have climbed since the 28% tax rate meaning that tax paid income has not been distributed to shareholders.

However loans from such companies to their shareholders have also climbed indicating that value is still being passed on to shareholders – just not in taxable dividend form.

Now yes shareholders should be paying non-deductible – to them – interest to the company for these loans but it is more than coincidental that this increase should happen when there is a gap between the company rate and that of the trust and top personal tax rate.

And alongside this was an increase in dividend stripping as a means of clearing such loans.

So an increase in the company tax rate would reduce those avoidance opportunities and align the tax paid by incorporated and unincorporated businesses.

And with more tax collected from this sector, Business would have a strong argument for more tax spending on the things they care about. Things like tax deductions in some form for seismic strengthening, setting up a Tax Advocate, or the laundry list of business friendly initiatives that get trotted out such as removing rwt on interest paid within closely held groups.

Some of which might even be productivity enhancing.

For the next few months, I am returning to gainful – albeit non-tax – employment. As it is non-tax there should be no conflicts with this blog except for my energy and – possibly – inclination.

I am hopeful that at least two guest posts will land over this period and you may still get me in some form.

But otherwise I will be maintaining the blog’s Facebook page, and am on Twitter @andreataxyoga. I can also recommend Terry Baucher’s podcasts – the Friday Terry – when he isn’t swanning around the Northern Hemisphere.

Andrea

(1) Officials wrote a very good paper for the TWG on company tax rate issues. It can be found here: https://taxworkinggroup.govt.nz/sites/default/files/2018-09/twg-bg-appendix-2–company-tax-rate-issues.pd

(2) Paragraph 33 for a discussion of this graphs limitations. These include a reduction in the amount of deductible debt and depreciation allowances at the time of the reduction to 28% which would have worked in the opposite direction to the tax cut.

(3) Paragraph 11

Tax and politics

Your correspondent is back from Sydney. Had a great time because – well – Sydney.

Managed to score a gig on a panel at the TP Minds conference talking about international policy developments for transfer pricing. An interesting experience as I am pretty strong in most tax areas except GST – and you guessed it – transfer pricing.

But it was ok as I did a bit of prep and all those years of working with the TP people paid off. And of course I do know a little bit about international tax and BEPS so alg.

Even a techo tax conference again reminded me just how different – socially and culturally – Australia is to New Zealand. Examples include: the expression man in the pub being used without any sense of irony or embarrassment and one of the presenters – a senior cool woman from the ATO – wearing a hijab.

Can’t imagine either in tax circles in NZ.

My particular favourite though was watching the telly which showed a clip of Bill Shorten describing franking (imputation) credits as something you haven’t earned and a gift from the government. Now Australia does cash out franking credits but – wow – seriously just wow. Kinda puts any gripes I might have about Jacinda talking about a capital gains tax into perspective.

And in the short time I have been away yet another minor party has formed as well as the continuation of the utter dismay from progressives over the CGT announcement.

In the latter case I am fielding more than a few queries as to what the alternatives actually are to tax fairness is a world where a CGT has been ruled out pretty much for my lifetime.

Now while I have previously had a bit of a riff as to what the options could be, I have been having a think about what I would do if I were ever the ‘in charge person’ – as my kids used to say – for tax.

To become this ‘in charge person’ I guess I’d also have to set up a minor party although minor parties and tax policies are both historically pretty inimical to gaining parliamentary power.

But in for a penny – in for a pound what would be the policies of an Andrea Tax Party be?

Here goes:

Policy 1: All income of closely held companies will be taxed in the hands of its shareholders

First I’d look to getting the existing small company/shareholder tax base tidied up.

On one hand we have the whole corporate veil – companies are legally separate from their shareholders – thing. But then as the closely held shareholders control the company they can take loans from the company – which they may or may not pay interest on depending on how well IRD is enforcing the law – and take salaries from the company below the top marginal tax rate.

On the other hand we have look through company rules – which say the company and the shareholder are economically the same and so income of the company can be taxed in the hands of the shareholder instead. But because these rules are optional they will only be used if the company has losses or low levels of taxable income.

My view is that given the reality of how small companies operate – company and shareholders are in effect the same – taking down the wall for tax is the most intellectual honest thing to do. Might even raise revenue. Would defo stop the spike of income at $70,000 and most likely the escalating overdrawn current account balances.

So look through company rules – or equivalent – for all closely held companies. FWIW was pretty much the rec of the OG Tax Review 2001 (1).

Now that the tax base is sorted out – if someone wants to add another higher rate to the progressive tax scale – fill your boots. But my GenX and tbh past relatively high income earning instincts aren’t feeling it.

Policy 2: Extensive use of withholding taxes

The self employed consume 20% more at the same levels of taxable income as the employed employed. Sit with that for a minute.

20% more.

Now the self employed could have greater levels of inherited wealth, untaxed capital gains or like really awesome vegetable gardens.

Mmm yes.

Or its tax evasion. Cash jobs, not declaring income, income splitting or claiming personal expenses against taxable income.

Now in the past I have got a bit precious about the use of the term tax evasion or tax avoidance but I am happy to use the term here. This is tax evasion.

IRD says that puts New Zealand at internationally comparable levels (2). Gosh well that’s ok then.

Not putting income on a tax return needs to be hit with withholding taxes. Any payment to a provider of labour – who doesn’t employ others – needs to have withholding taxes deducted.

Cash jobs need hit by legally limiting the level of payments allowed. Australia is moving to $10,000 but why not – say $200? I mean who other than drug dealers carries that much cash anyway?

Claiming personal expenses is much harder. This we will have to rely on enforcement for.

Policy 3: Apportion interest deductions between private and business

Currently all interest deductions are allowable for companies – because compliance costs. Otherwise interest is allowed as a deduction if the funding is directly connected to a business thing.

Seems ok.

What it means though is that for someone with a small business and personal assets such as a house, all borrowing can go against the business and be fully deductible.

Options include some form of limitation like thin capitalisation or debt stacking rules. I’d be keen though on apportionment. If you have $2 million in total assets and $1 million of debt – then only 50% of the interest payable is deductible.

Policy 4: Clawback deductions where capital gains are earned

Currently so long as expenditure is connected with earning taxable income it is tax deductible. It doesn’t matter how much taxable income is actually earned or if other non-taxable income is earned as well.

Most obvious example is interest and rental income. So long as the interest is connected with the rent it is deductible even if a non-taxable capital gain is also earned.

One way of limiting this effect is the loss ringfencing rules being introduced by the government. Another way would be – when an asset or business is sold for a profit – clawback any loss offsets arising from that business or asset. Yes you would need grouping rules but the last government brought in exactly the necessary technology with its R&D cashing out losses (4).

Policy 5: Publication of tax positions

And finally just to make sure my party is never elected – taxable income and tax paid of all taxpayers – just like in Scandinavia will be published. Because if everyone is paying what they ought. Nothing to hide. And would actually give public information as to what is going on.

Options not included

What’s not there is any form of taxation of imputed income like rfrm. It isn’t a bad policy but taxing something completely independent of what has actually happened – up or down – doesn’t sit well with me.

Also no mention of inheritance tax. Again not a bad policy I’d just prefer to tax people when they are alive.

And for international tax I think keep the pressure on via the OECD because the current proposals plus what has already been enacted in New Zealand is already pretty comprehensive.

Now I know none of this is exactly exciting and so I’ll get the youth wing to do the next post.

Andrea

(1) Overview IX

(2) Paragraph 6

(3) Treatment of interest when asset held in a corporate structure

(4) Page 11 onward

#Doubletaxationisgross

Let’s talk about tax.

Or more particularly let’s talk about tax and companies.

Well dear readers what a week it has been in the Beltway. Secret recordings down south and secret payouts from Wellington. All the more bizarre as – Mike Williams confirmed – MPs staffers pretty much have sack at will contracts. If your MP doesn’t like you – that’s it you’re out. No lengthy performance management for them. Facepalm. So maybe this factoid could get added to new MPs induction?

But as always the key issue gets missed. Exactly who under 40 years old knows what a dictaphone is?

And into this maelstom Inland Revenue released a paper on taxation of individuals and some stuff on debt. Both worthy topics of discussion. But then Ryman released its results. And their CEO said like tax is paid – just not like income tax and just like not by them.

So after last week’s post I thought I’d have a look.

Oh yes the real tax is very easily found in the Income Tax Note. Tax losses of $28.9 million in the 2017 year. Up from last year when they were only $15 million of losses. They are a growth stock after all. Quite different from the tax expense which was $6m tax payable.

To your correspondent this looks awfully like her specialist subject of interest deductions for capital profits. All mixed up in a world where interest expense isn’t in the P&L but instead added to the asset value. Complying with both accounting and tax. And yeah totes a tax loophole but one from like whenever.

And again in Ryman’s accounts the rent equivalent from the time value of money of the occupancy advances is in neither the accounting nor the tax profit. Because reasons.

Now expecting controversy the CEO front footed the issue saying that the shareholders paid tax and that Ryman had actually paid GST. He then also referred to the PAYE deducted as they were employers. Kinda going to ignore that bit tho coz the whole claiming credit for other people’s tax really gets on my nerves.

And I’ll take his word on the GST angle coz I am cr@p at GST. But with his shareholders paid the tax comment – he is talking about imputation. And as I haven’t covered that before dear readers – today you get imputation. Oh and other random thoughts on tax and companies.

Now the official gig about imputation is how – notwithstanding that they are separate legal peeps – the company is merely a vehicle for their shareholders to do stuff. So for tax purposes the company structure should – sort of – get looked through to its shareholders. And this means dividends are in substance the same income as company profits and so should get a credit for tax paid by the company.

And as a tax person this stuff is considered to be in the stating the flaming obvious category.

But as I am no longer an insider – I am increasingly finding it interesting just how public policy on companies manages to talk out of both sides of its mouth. And how – much like the sack at will contracts or milliennials using dictaphones – no one has noticed.

On one hand we have the Companies Act which sets up companies with separate legal personalities from its shareholders. Meaning that if you transact with a company and it doesn’t pay you. Bad luck bucko. Nothing to do with the shareholders. Limited liability; corporate veil and all that.

But for tax if you only have a few shareholders those losses can flow through to the shareholders and be offset against against other income. The negative gearing thing but using a company. Coz in substance the company and shareholders are like the same.

And a similar thing happens with the Trust rules. Trust law says that it is trustees that own the assets. And once you have handed stuff over to them as settlor – that’s it – that stuff isn’t yours anymore. So if that settlor owes you money – also bad luck bucko. Don’t for a second think you can approach the trustees – coz whoa – settlor nothing to do with them.

But then tax says – for trusts – as settlors call the shots; it’s the residence of the settlor that is important. Mmmm. This means that a trust with a New Zealand resident trustee and a foreigner wot gave the stuff to the trustee – foreign trust – isn’t taxed on foreign income. Coz that would be like wrong. Even though the assets are owned by a New Zealand resident. And New Zealand residents normally pay tax on foreign income.

Right. Awesome. Thanks for playing.

Anyway back to imputation.

Now put any thoughts of separate legal personalities outside your pretty heads dear readers and think substance. Think companies are vehicles for shareholders. Don’t think about small shareholders having no say or liability if anything goes wrong. Just think one economic unit.

And then you will have no problem seeing potential double taxation if profit and dividends are both taxed. Coz #doubletaxationisgross.

So as part of the uber tax reforms in the late eighties imputation was brought in. Tax paid by the company can be magically turned into a tax credit called – imaginatively – an imputation credit which then travels with a dividend. Creating light and laughter in the capital markets. Or as I have put to me – increased inequality. As when imputation came in it gave dividend recipients – aka well off people – an income boost courtesy of the tax system. Probs also a tax free boost in the share price too.

Now putting aside such inconvenient facts – your correspondent has always defended imputation. Because in order to get the light and laughter or increased inequality – companies actually have to pay tax. And of that – big fan.

But all of this is only useful if shareholders are resident. Coz the credits only have value to New Zealand residents. And this is kind of why foreign companies may not care about paying tax here. And did I mention tax has to actually be paid?

And this last point that brings me back to Ryman’s chairman. He is right. If the company doesn’t pay tax – then the shareholders do when a dividend is paid. So honestly what are we all getting excited about?

Well – profits have to be like actually distributed before that happens and shareholders have to be taxpayers. And Ryman distributes less than 25% of their accounting profit.

And the residence of shareholders? Who knows. Lots of nominee companies listed which could mean KiwiSavers or non-residents. Oh and Ngai Tahu. Who seems to be a charity.

So yeah maybe. Some tax will be paid by some shareholders. That is true. Let’s hope it exceeds the tax losses Ryman is producing.

Andrea

PS. This will be the last post – except if it isn’t – for the next couple of weeks. Your correspondent is getting all her chickens back for a while. And much as I love you all dear readers – I love them more. Until Mid July. Xx

‘You’re not one of those people are you?’

Let’s talk about tax (and tax rate alignment).

Your (foreign) correspondent is finishing up her ‘retirement cruise’ and gearing up to make that execrable journey home – also known as long distance economy class travel.

The yoga is going well too – thanks for asking – even without regular access to a studio. In large part to now knowing how alignment needs to work with my skeleton rather than that of a textbook Indian man.

So I have been thinking about this, how foreign tax systems are pretty much all misaligned, and that I promised to talk about the tail chasing stuff needed to make a higher top marginal tax rate work – or at least not not work. Because like misaligned bodies in yoga; misaligned tax systems also need props to work.

So today dear readers you get top personal tax rate alignment issues.

A couple of years ago while I was still a Treasury official I was at a social engagement and found myself talking to a Greens’ supporter. We were talking about the Christchurch earthquake and the rebuild and stuff – yes I do have all the fun – and the convo went something like this:

GS: You may remember that Russel proposed an earthquake levy as a means for the whole of the country to support Christchurch.

Me: yeah I remember that and on the face of it it did have merit – the problem is that whenever you increase the gap between the personal rates and the trust and company rate – you get people moving income into different forms. You may not collect all you think you will.

GS: [eye roll] you’re not one of those people are you? Other countries cope.

Well yeah I am ‘one of those people’. I really do like alignment and again not from a ‘purity of the tax system’ thing but because – like keeping R&D tax incentives out of the tax system – it serves us. It serves us because no matter how clever people want to get with their structuring – you always get the same result.

HOWEVER

Alignment – like a capital gains tax is not a silver bullet and – doesn’t mean:

- everyone magically starts earning income in their own names or

- income that isn’t taxed magically starts becoming taxed

It just means that there is no incentive to start finding a bunch of non-tax commercial reasons that coincidently mean current taxable income is now earned in different lower taxed forms.

But next lefty government if you do want to raise the top rate for individuals – you are going to need some tax props to stop or reduce the tax injuries. That is how othe countries cope. Have a look at page 36 of IRD’s 2005 BIM.

First thing that is beyond key is the trust or trustee tax rate. This must be raised too as income taxed at the trustee rate can be then given to beneficiaries without any more tax to pay. Australia has. All the Penny and Hooper drama happened because the trustee rate wasn’t raised too.

However there are potentially some collateral damage issues from this – aka political risk:

- Will estates

- Trusts for the ‘handicapped child’ or the disabled relative

Australia deals with these respectively by taxing at the progressive tax scale and giving the Commissioner a discretion to alter the rate. In the last – and possibly both – cases face palm. Given our tax administration’s aging computer and business transformation programme – a better option would be treating them like widely held superannuation funds and giving them the company tax rate.

You could also do something like giving them a non-refundable tax credit to get the rate back down to 33%. That technology was used in cashing out R&D losses. But this is all second order design detail and nothing officials and/or your working group can’t sort out. No biggie. It might be a bit messy but nothing compared to the carnage involved with not aligning the trust rate.

Next issue is companies and that is a bit harder. I am assuming raising the company tax rate is off the agenda – yeah thought so.

Misalignment with the company rate – as we do now – is marginally less risky as distributions from companies – dividends – are taxed in the hands of the shareholders. And they use my personal favourite technology – the withholding tax. There is currently an additional withholding tax on dividends when they are paid bringing total tax up to 33%.

You could keep the additional withholding tax at 5% and make people file who need to pay more tax – as there was no withholding at all last time there was a 33% company rate and a 39% top rate. But there also wasn’t alignment with trusts and that went well.

Or you could raise the withholding tax to – say – 11c and people who need refunds would then need to file. Or possibly a progressive withholding system from say 5c to 11c. All technically possible. But all options will raise compliance costs on taxpayers and/or administration costs on IRD. And remember the aging computer thing?

The real issue is whether our dividend rules last properly looked at almost 25 years ago can stand the strain of say a 11c difference between the company rate and top personal rate. There are ultimately limits to how long people can pay themselves $70k salaries but have a $200k lifestyle. You need to make sure you get that extra 11c when they decide to sort out that gap.

Alternatively you may like to consider making the look through company rules compulsory for all closely held companies. This would mean the company wasn’t taxed and all the income went to shareholders personally.

Neither issue will need to be part of the first 100 days tax changing under urgency that is de rigeur for new governments. It can be sorted out with consulation and will be better for it. But you will need to be prepared to use these tax props if you don’t want the 2000 – 2009 mess again.

Think that’s it.

Hardest thing will be reprioritising the existing BT and BEPS work programme to get space for this and your new fairness working group stuff.

Namaste